The market can be a cruel place. Rising interest rates have hammered the stock market this year – tech stocks in particular, which become less attractive when interest rates go higher. The technology heavy Nasdaq Composite Index has fallen nearly 15% so far this year and fallen into a correction, wiping out nearly $3 trillion in value from the Nasdaq 100 Index (a subcategory of the Nasdaq Composite Index). The S&P 500 Index is down over 9%, on track for its worst start to a year, and is flirting with correction territory. Individual companies are taking a beating (of which I’m well aware ☹).

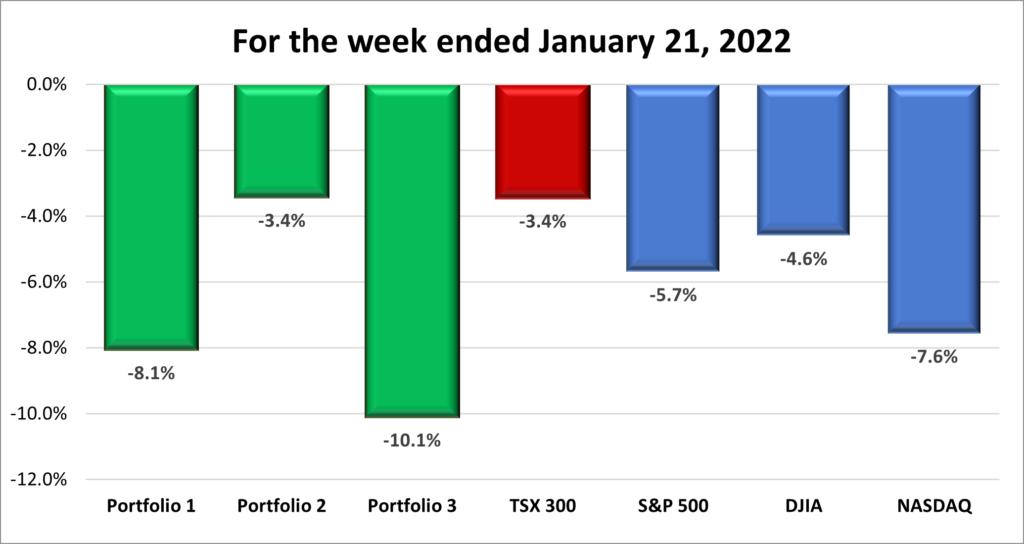

Since the start of the year the Toronto Stock Exchange Composite Index (TSX) has fallen nearly 3%, the S&P 500 Index is down 7%, the Dow Jones Industrial Average (DJIA) is down over 4%, and the Nasdaq Composite Index (Nasdaq) has dropped 12%.

Barring a stunning performance by all the Indexes on Monday, there will not be any January effect this year.

In late 2021, the Covid-19 variant Omicron and rising inflation weighed the market down. Now, while Omicron lurks in the background, it has been replaced in the forefront by tensions between Russia and the NATO countries over fears of a Russian invasion of Ukraine. Still weighing on investors is inflation and the associated interest rate hikes necessary to curb inflation. It is expected both the Bank of Canada (BoC) and the US Federal Reserve (Fed) will increase interest rates in March, but it is not known how many times they will hike interest rates, nor what those hikes will be, as both the BoC and the Fed attempt to wrestle inflation back below their respective 3% target.

But despite all those fears, Friday was a comeback day after a decidedly ugly January. Strong earnings from Apple (NASD:AAPL), Microsoft (NASD:MSFT) and few other large capitalization companies helped get bargain hunters back into the market. The question is, is that another upward feint or has the market found the bottom? As Captain Obvious would say, we’ll only know we’re at the bottom when prices stop going down and start going up. 😊

Now, lets see the week that was and how the portfolios faired…

Weekly Market Review

Monday: The week got off to an ominous start with the Toronto Stock Exchange Composite Index (TSX), S&P 500 Index (S&P), Dow Jones Industrial Average (DJIA) and Nasdaq Composite Index (Nasdaq) each falling sharply in the morning before a bargain hunter rally in the afternoon. The late rally pushed the American Indexes into the black, but the TSX was unable to climb out of the hole it dug itself in the morning. Ongoing tensions between Russia and Ukraine, and the upcoming US Federal Reserve meeting on Wednesday weighed on all four Indexes, with the upcoming Bank of Canada meeting an extra variable for the TSX.

Tuesday: The day started similar to Monday’s volatility with a sharp sell off to start the trading day, followed by an afternoon rally. However, this time it was the TSX that ended the day in the black and the US Indexes that were unable to get out of the red. In the US, the Energy sector was the top performer on fears of future supply issues due to potential conflict between Russia and Ukraine. The Technology sector was the biggest loser thanks to concerns of interest rakes hikes coming out of this weeks Federal Reserve meeting.

In Canada, similar sentiments regarding Ukraine lifted the Basic Materials sector (gold) and Energy sector (oil), pushing the TSX into positive territory. Those two sectors overcame the Technology sectors 3% decline, caused by concerns about an interest rate hike coming out of Wednesday’s Bank of Canada meeting caused.

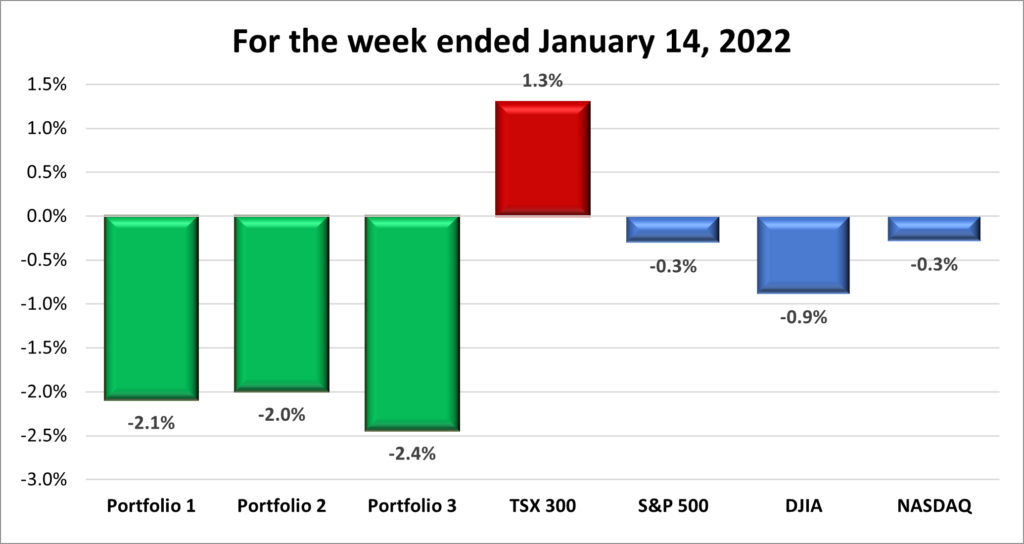

Wednesday: Today the markets were split with the TSX and Nasdaq eking out gains of .02%, while the S&P and DJIA barely lost ground. The big news was the US Federal Reserve announced it would leave interest rates at their current level. The markets responded positively to this news but retreated when the Fed warned it could raise interest rates as soon as March to cool off the highest inflation in 40 years. Rate hikes will make it more expensive, over time, for consumers and businesses alike to borrow for anything and everything.

In Canada, the Bank of Canada said it would start hiking interest rates ‘soon’. While the TSX ended the day in the black, like its American cousins, it dropped on news the US Federal Reserve planned to raise interest rates in March and ended the day 1.5% below its noon time high. On both sides of the border investors now know interest rates will very likely be going up in March. I’m curious to see how the market responds now that the Fed has removed the uncertainty of an impending rate hike.

Thursday: So much carrying over the momentum from Wednesday afternoon. All four Indexes started moving upward when the market opened, but reversed themselves a few hours later, Declines were fueled by fears the US Federal Reserve would hike interest rates up to five times in 2022, and ongoing geopolitical tensions. The interest rate sensitive technology, and consumer discretionary sectors fell the farthest. In the US, The Russel 2000 Index (a market index of 2,000 companies valued between $300 million – $2 billion) has fallen over 20% since early November, indicating it has been in a ‘bear’ market.

Friday: After a rollercoaster week of trading, it was a good day for all four Indexes. Finally! In a reversal of the last few days, the four Indexes dropped in the morning before zigzagging upward. The TSX’s Technology sector had a strong day, up over 4%, helping the TSX post a slight gain for the week. In the US, after a volatile week, all three Indexes ended the week with a flourish. Both the S&P and the DJIA ended the week higher while the Nasdaq ended the week flat.

For the month of January

Weekly Portfolio Review

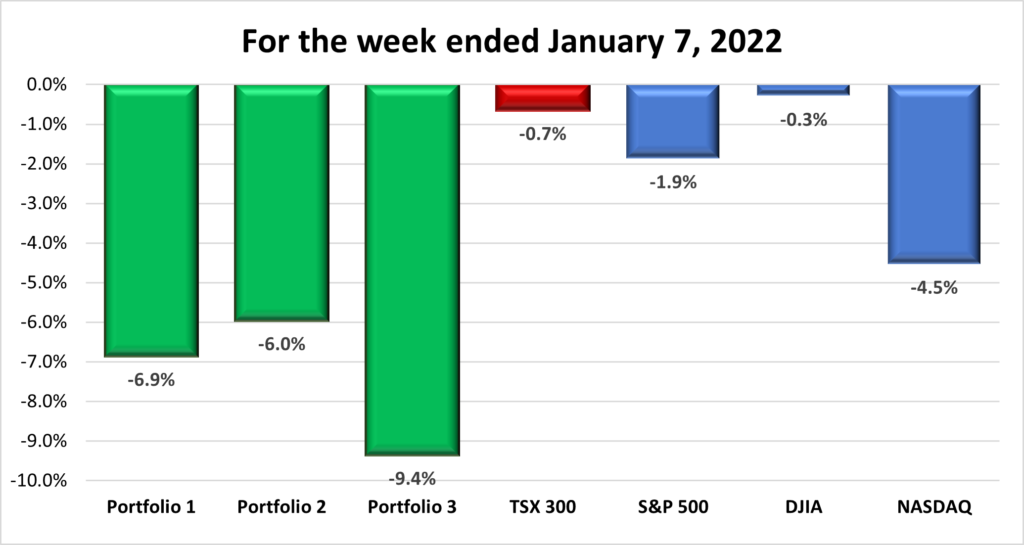

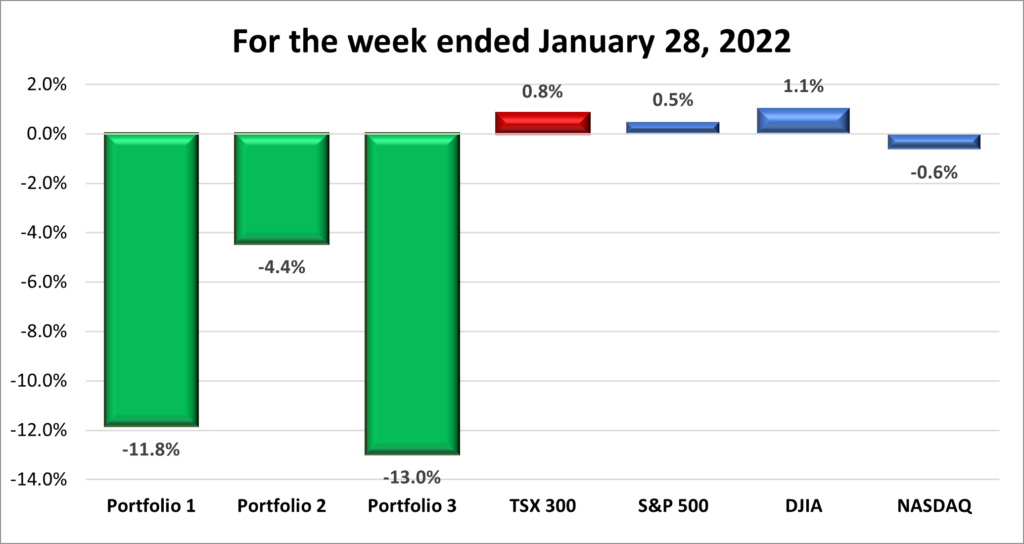

Prior to Friday I was expecting an ugly week. Well, it turned out to be an ugly week with Portfolios 1 and 2 suffering double digit falls. Portfolio 2 also was down for the week. Ongoing Inflation and fears of higher interest rates are good for good for the financial stocks in the three portfolios but not so good for their respective Technology sector companies, especially the high growth companies that use debt to fund their growth. The Friday rally was a ray of sunshine, perhaps a bottom is nearby. I look forward to the week when all three portfolios end a week in positive territory. For now, I’ll be happy if one of them can put up a positive week.

Companies on the Radar

While the market has been zigzagging up and down the past few weeks, I haven’t really looked at any specific companies. I don’t expect to be active in the market while the market continues its downward trend unless one of the big ‘blue-chip’, growth-oriented companies in any of the portfolios has a too good to pass up ‘sale’. For me, this includes:

Microsoft (NASD:MSFT)

Apple (NASD:AAPL)

Home Depot (NYSE:HD)

Nvidia (NASD:NVDA)

Visa (NYSE:V)

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended January 28, 2022: DOWN ![]()

Combine the loyalty of Apple fans with pent up demand for Apple’s latest products and you get a great first quarter report. Apple was able to navigate the supply chain headwinds and post double digit growth in revenue and earnings. I don’t know how they keep doing it but I’m glad I finally invested in Apple. Better late than never.😊

It turns out that Visa was everywhere people wanted to be in late 2021. Thanks to increased travel and e-commerce spending, Visa posted a strong first quarter report. Highlights include strong results for revenue, net income and EPS, all grew at 24% or more. Better than anticipated cross-border travel, and a record holiday-quarter sales, all contributed to an excellent quarter.

Although Tesla’s (NASD:TSLA) recent earning report beat expectations on the top and bottom line, its’ shares of fell after the company failed to provide guidance for what it expects in 2022. It also announced supply chain issues causing its factories to run below capacity.

Voyager Digital (TSX:VOYG), along with other cryptocurrency platforms, is being investigated by US regulators. With cryptocurrencies currently in a free fall, being under the microscope of regulators does not bode well for Voyager’s share price.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

BCE Inc (TSX:BCE) DRIP

Shaw Communications Inc (TSX:SJR.B) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

Canadian National Railway Co

All currency listed in CAD dollars

Selected highlights from their fourth quarter 2021 financial results on January 25, 2022

Fourth Quarter

- Revenues of C$3,753 million, an increase of C$97 million or three per cent

- Record fourth quarter operating income of C$1,566 million, an increase of 11 per cent

Full year 2021

- Revenues of C$14,477 million, an increase of C$658 million or five per cent

- Operating income of C$5,616 million, an increase of 18 per cent

- Record free cash flow for the year ended December 31, 2021, of C$3,296 million compared to C$3,227 million for the same period in 2020.

- Return on invested capital (ROIC) of 16.4 per cent, an increase of 3.7 points.

- 19% increase in the 2022 dividend; approved a plan to re-purchase up to 42 m common shares.

Tesla

All currency listed in US dollars

Selected highlights from their fourth quarter 2021 financial results on January 26, 2022

- delivered over 936,000 vehicles

- $2.3B GAAP net income

- $1.5B increase in cash and cash equivalents in Q4 to $17.6B

- expect to achieve 50% average annual growth in vehicle deliveries

Visa

All currency listed in US dollars

Selected highlights from their first quarter 2022 financial results on January 27, 2022

- GAAP net income of $4.0B or $1.83 per share

- Net revenues of $7.1B, an increase of 24%

- Returned $4.9B of capital to shareholders in the form of share repurchases and dividends

Apple

All currency listed in US dollars

Selected highlights from their first quarter 2022 financial results on January 27, 2022

- Posted an all-time revenue record of $123.9 billion, up 11 percent year over year.

- Quarterly earnings per diluted share of $2.10.

- Declared a cash dividend of $0.22 per share of the Company’s common stock.

Portfolio 2

Portfolio 2 for the week ended January 28, 2022: DOWN ![]()

A strong earnings report from Mitek Systems (NASD:MITK) which beat analyst’s expectations for earnings per share (USD$ .22 actual v USD$ .14 estimated) and revenues (USD$ 32.5 million actual v USD$ 28.5 million estimated), leading to a nice share price bump on Friday.

Once again, Microsoft had another strong earnings report, beating analysts’ expectations for revenue (USD$ 51.7 billion actual v USD$ 910 million) and earnings per share (USD$ 2.48 per share v USD$ 2.32 estimated). All three segments increased their revenues in an impressive earnings report.

Otherwise, it was a relatively good week for Portfolio 2 with 75% of the companies finishing the week higher than they started.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX:DIR.UN) DRIP

Brookfield Select Opportunities Income Fund (TSX:BSO.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

Microsoft Corp

All currency listed in US dollars

Selected highlights from their second quarter 2022 financial results on January 25, 2022

- Revenue was $51.7 billion and increased 20%

- Operating income was $22.2 billion and increased 24%

- Net income was $18.8 billion and increased 21%

Mitek Systems Inc (NASD:MITK)

All currency listed in US dollars

Selected highlights from their second quarter 2022 financial results on January 27, 2022

- Total revenue increased 25% year over year to a first quarter record $32.5 million.

- GAAP net income increased 44% year over year to $3.1 million, or $0.07 per diluted share.

- Cash flow from operations was $2.3 million.

Portfolio 3

Portfolio 3 for the week ended January 28, 2022: DOWN ![]()

Over half of the companies in Portfolio 3 ended the week higher than they started. It’s been a while since I’ve been able to say that. Prior to Friday, Shopify (TSX:SHOP) was down over 45% since its November high. On Friday, Shopify gained 10% to finish the week at CAD$ 1,113.98. Only $900 more to get back to its November high.

The other notable performers include the family of four Brookfield companies in the portfolio, all finished the week in the black. Microsoft also had a good week after a strong earnings report.

Finally, Real Matters (TSX:REAL) had a disappointing first quarter earnings. Both their revenues and net income were less than the 2021 first quarter numbers. However, during the shareholders’ meeting the CEO said they are confident they will attain their 2025 goals. He also announced they are taking advantage of the current lower share price and buying back shares to return value to shareholders (by increasing the size of each shareholder’s piece of the pie, so to speak). Nevertheless, the share price felt the investors’ wrath.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Microsoft Corp

All currency listed in US dollars

Selected highlights from their second quarter 2022 financial results on January 25, 2022

- Revenue was $51.7 billion and increased 20%

- Operating income was $22.2 billion and increased 24%

- Net income was $18.8 billion and increased 21%

Real Matters Inc.

All currency listed in CAD dollars

Selected highlights from their first quarter 2022 financial results on January 28, 2022

- Consolidated revenue of $107.8 million, a 10.4% drop versus the $120.3 million a year earlier

- Net income was $2.6 million, or $0.03 per diluted share, compared with $7.1 million, or $0.08 per diluted share, for the year ago period.

- Continue to buy back shares to return value to shareholders.