Nothing quite like watching your portfolio go from green to red during a market decline. In my case, I get three times the pleasure as all three portfolios took a significant plunge. There is no sugar coating it, the third quarter was bad, but it pales in comparison when looking at the nine months January 1 through September 30. If there is a Good, the Bad, the Ugly, there would be no Good but there is a Bad and there is an Ugly. So, let’s take a look at the damage ….

Contents

Third Quarter Review (The Bad)

Third Quarter Portfolio Update

Portfolio 1 for the third quarter

Portfolio 2 for the third quarter

Portfolio 3 for the third quarter

Going Forward: The Fourth Quarter

Third Quarter Review (The Bad)

The third quarter of 2022 (July 1 through September 30) was like a roller coaster ride that gradually drags you up the hill, plunges you down, up, and down smaller rises before a final downhill plunge to end the ride. As you can see in the chart below, the markets got the third quarter off to a good start as they moved upwards through July and into mid-August. Unfortunately, the rally turned out to be a bear trap (when markets rise for a few days before resuming their downward trajectory) when it plunged in mid-August. The Indexes rallied on hopes upcoming interest rates would be less aggressive than the previous hike, only to plummet once the US Federal Reserve (Fed) made its third straight 0.75% interest rate hike, bringing the US interest rate to 3.25%, and hinted more ‘pain’ was to come. And here we are, at the end of third quarter ride.

The third quarter of 2022 (July 1 through September 30) was like a roller coaster ride that gradually drags you up the hill, plunges you down, up, and down smaller rises before a final downhill plunge to end the ride. As you can see in the chart below, the markets got the third quarter off to a good start as they moved upwards through July and into mid-August. Unfortunately, the rally turned out to be a bear trap (when markets rise for a few days before resuming their downward trajectory) when it plunged in mid-August. The Indexes rallied on hopes upcoming interest rates would be less aggressive than the previous hike, only to plummet once the US Federal Reserve (Fed) made its third straight 0.75% interest rate hike, bringing the US interest rate to 3.25%, and hinted more ‘pain’ was to come. And here we are, at the end of third quarter ride.

In Canada, the ride was not quite as ‘exciting’ as it was in the USA, but there were ups and down, nonetheless. Because the Toronto Stock Exchange (TSX) is heavily weighted with energy and mining companies, which themselves were buffeted by volatile commodity and oil prices, the TSX did not experience the highs of the August rally, but it also did not fall as hard as the three American Indexes.

What caused this market roller coaster ride? The usual suspects of 2022: inflation making items more expensive; aggressive central bank (the Bank of Canada, and the US Federal Reserve Bank) interest-rate increases making debt more expensive; the ongoing Russian invasion of Ukraine impacting energy and food supplies (wheat); Covid-19 lockdowns in China lowering demand for products and reducing global manufacturing capacity; and investor’s growing fears of a recession.

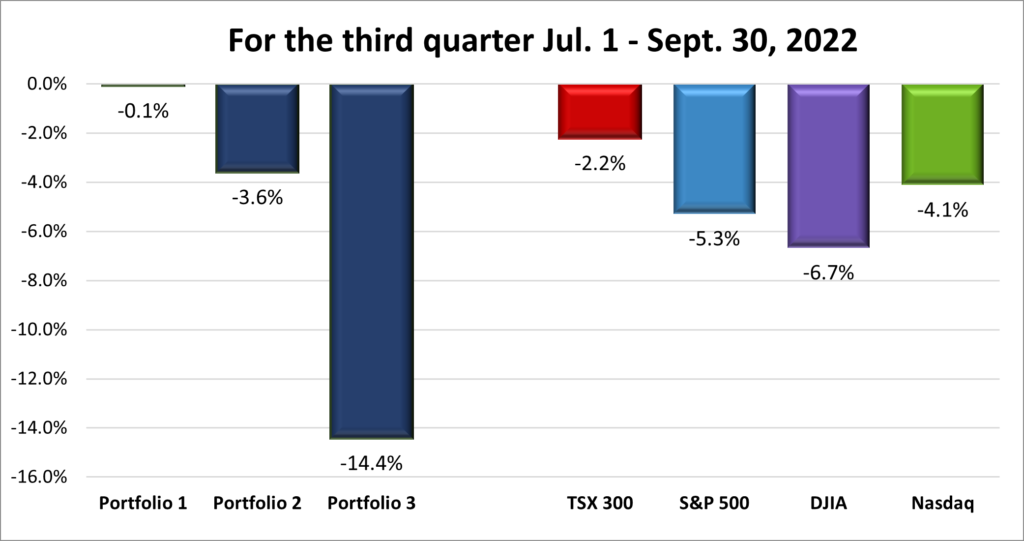

For the third quarter, the Toronto Stock Exchange Composite Index (TSX), fell 2.2%, the S&P 500 Index (S&P), dropped 5.3%, the Dow Jones Industrial Average (DJIA), plunged 6.7% and the Nasdaq Composite Index (Nasdaq ) tumbled 4.1%.

Third Quarter Portfolio Update

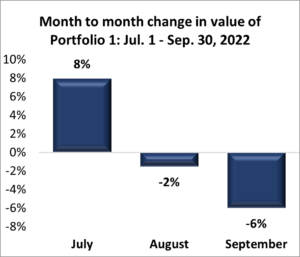

Portfolio 1 for the third quarter: DOWN

Portfolio 1 benefitted from the July to mid August rally but then sagged considerably towards the end of the quarter, ending the quarter down 0.1%. The portfolio was buoyed by the three energy companies in the portfolio, keeping its drop to a minimum for the quarter.

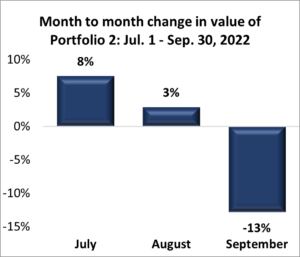

Portfolio 2 for the third quarter DOWN

The third quarter started off well for Portfolio 2, only to tumble into the red at the end of the quarter thanks to MongoDB (NASD:MDB) plunging almost 40% in September. Of the three portfolios it is the most ‘balanced’ and has the largest percentage of dividend paying companies to keep cash coming in during down markets, such as this one. Unfortunately, balance and dividends wasn’t enough to offset your best performer taking a nosedive.

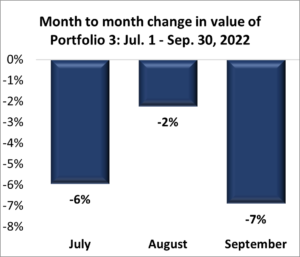

Portfolio 3 for the third quarter DOWN

Unlike the other two portfolios, Portfolio 3 did not even have one good month. Even the August rally was not enough to bump Portfolio 3 into the black. The portfolio grew tremendously on the back of technology companies during the Covid-19 lockdowns, especially Shopify (TSX:SHOP) which has plunged over 70% since its all-time high in November 2021. What the market gaveth from 2020 – 2021, the market taketh in 2022. ☹

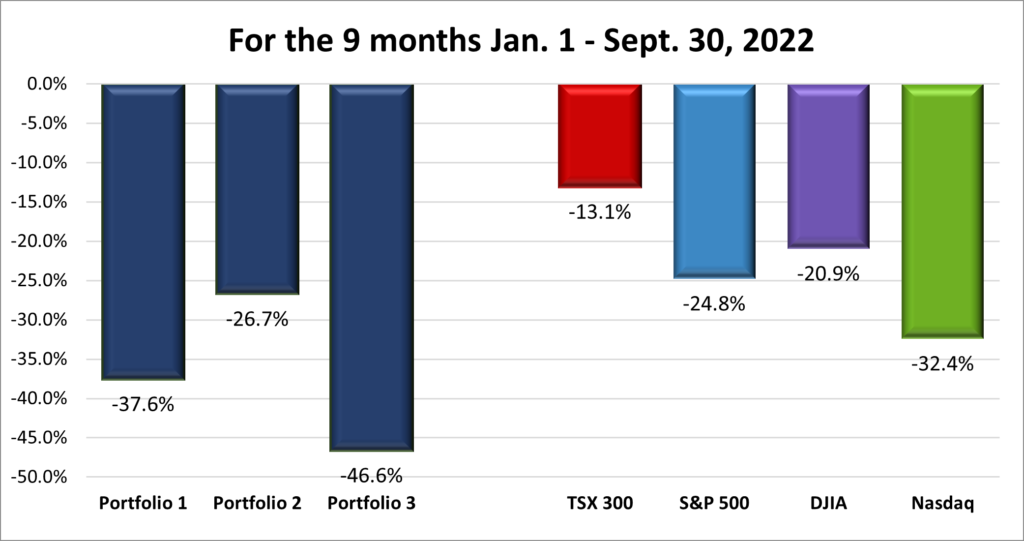

Nine Month Review (The Ugly)

You would be correct if you thought 2022 has not been a good year in the stock markets. Portfolio 3 aside, the third quarter does not look so bad, thanks to the mid summer rally. However, the nine-month chart paints a much uglier year to date picture. In the first nine months of 2022, Canada’s TSX declined 13%. That is bad, until you consider the declines of the American Indexes. The S&P, DJIA and Nasdaq suffered three quarterly declines in a row, the longest losing streak for the S&P and the Nasdaq since 2008, and the DJIA’s longest quarterly slump in seven years. The DJIA is down about 20% this year, putting it in a bear market (down 20% or more from recent highs) and trading close to its lowest levels since November 2020. The S&P has fallen almost 24% in 2022 putting it in line for its worst annual drop since 2008. The technology heavy Nasdaq is down more than 30% this year. With declines like that its no wonder investor sentiment has shifted decisively from optimism and greed in 2021 to fear and pessimism in 2022.

The main contributors to the overall decline of North America’s stock markets are the same as those that impacted the third quarter: inflation, interest rate hikes, supply constraints caused by China’s lockdowns in their fight against covid-19, and the ongoing war in Ukraine.

For the nine months end September 30, the TSX fell 13.1%,the S&P 500 plunged 24.8%, the Dow fell 20.9% and the Nasdaq plummeted 32.4%. Ouch!

Nine Month Portfolio Review

As was mentioned, 2022 has not been kind to the Indexes, however, as you can see in the chart below, it has been brutal on the Portfolios. Only the interest rate sensitive Nasdaq prevented the Portfolios from taking the three worst performers positions. Portfolios 1 & 3 were battered thanks to many of the technology companies in the respective portfolios having their share prices nearly cut in half. Portfolio 1 did not drop as much as Portfolio 3 thanks to broader diversification, as well as the energy companies which have all done well in 2022. As I have mentioned numerous times, Portfolio 2 is better balanced than the other two portfolios, but it still includes a few high growth technology companies which have also seen their shares hit hard. You know you are having a bad investing year when your best performing portfolio has plummeted 25%. ☹

Its hard seeing a chart like the one below but I keep telling myself selling would lock in significant losses, and I am investing for the long term. Once the market returns to its historically upward trend, all three portfolios will be back in the black (I hope).

Going Forward: The Fourth Quarter

All the events that roiled the stock markets during the third quarter – covid-19 lockdowns in China, the ongoing war in Ukraine, high inflation, rising interest rates, fears of a recession – remain in place for the fourth quarter. Analysts are already talking about interest rates in Canada and the US going north of 4% by the end of the year, with additional hikes in 2023. For companies with significant debt this is not good news. Adding downward pressure on share prices is negative investor sentiment. This is when no one cares about how companies are performing, all they want is their money out of the falling market, one they are helping to fuel. While the fourth quarter is likely to be rocky for the markets and the Portfolios, it is a good time to buy shares in good companies that have been dragged down in 2022.

I started off comparing the market to a rollercoaster, so I will end with the same analogy. As supply chain issues continue to work themselves out, along with falling demand and slowing wage growth, inflation should come back to the 2% – 3% range. The market rollercoaster will bottom and then head back uphill. The plan is to hold on through this white-knuckle plunge, take advantage of some of the bargains currently available, and be ready to ride the rollercoaster up. I do not know when the rollercoaster will head upward. But it will. Sooner rather than later would be nice. 😊