Since the start of the year, all four of the major North American indexes – Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – finished the first half higher than they started, as did the three portfolios, thanks to a bull run in the Nasdaq and the S&P. Unfortunately, what had been a strong bull run for the first half of the year, saw the emergence of a bear or two in the third quarter.

Let’s look at what happened during the third quarter of 2023 ….

Third Quarter Portfolio Update

Portfolio 1 for the third quarter

Portfolio 2 for the third quarter

Portfolio 3 for the third quarter

Third Quarter Review

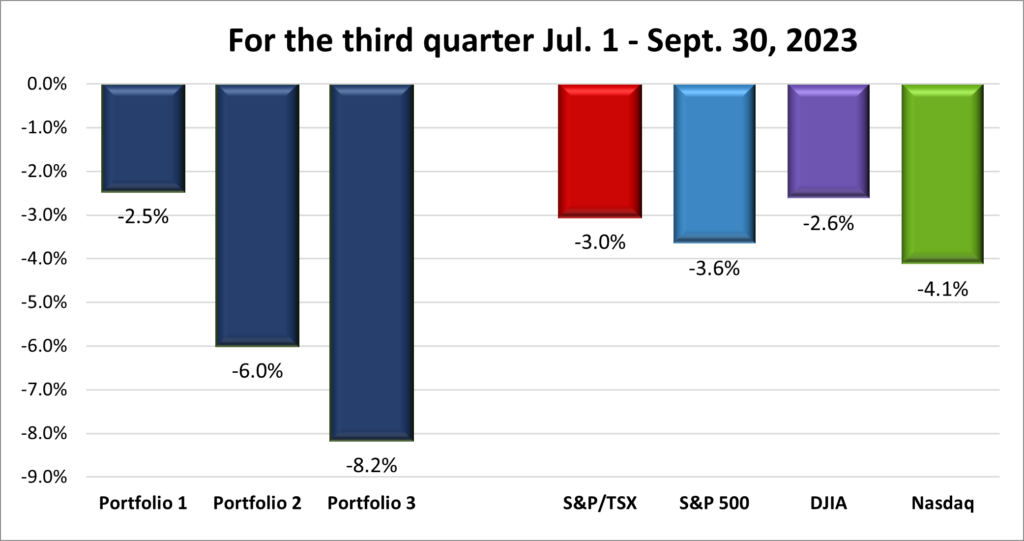

For the third quarter, the TSX (SPTSX) lost 3.0%, the S&P (SPX) fell 3.6%, the DJIA (INDU) declined 2.6% while the Nasdaq (CCMP) dropped 4.1%.

![]() As you can see in the chart above, all four major North American stock indexes experienced declines in the third quarter of 2023. This marked their first quarter in the red since the third quarter of 2022. While not dramatic drops, they contrasted with the strong gains seen in the first half of the year.

As you can see in the chart above, all four major North American stock indexes experienced declines in the third quarter of 2023. This marked their first quarter in the red since the third quarter of 2022. While not dramatic drops, they contrasted with the strong gains seen in the first half of the year.

Of the three major American indexes, the DJIA performed the best in the third quarter, or more acurately, declined the least. This was likely due to its focus on established companies with strong dividends. The S&P, which tracks a broader range of companies, was more negatively affected by the slowdown in earnings growth. Finally, the technology-heavy Nasdaq brought up the rear, as tech stocks are particularly sensitive to rising interest rates.

Canada’s TSX also lost ground in line with the broader market trends. The index experienced a modest decline compared to the major US indexes, but the energy sector remained a bright spot. Driven by rising oil prices, Canadian energy companies performed well during the quarter.

The key factors driving these market declines were the high interest rates implemented by the Fed and the BoC to combat inflation, plus the talk of higher rates for longer. These higher rates make it more expensive for companies to borrow money, which can lead to slower economic growth and lower corporate profits.

Overall, the third quarter of 2023 was a challenging period for the North American stock markets. The third quarter limped to the finish line, leaving the fourth quarter with the challenges of higher interest rates in Canada and the US, as well as a slowing economy in Canada.

Despite the indexes ending the third quarter with a whimper, these declines occurred after a strong run-up in the first half of the year. Hopefully the third quarter was just a breather before a strong bull run in the fourth quarter to finish out 2023. 😊

Third Quarter Portfolio Update

Like the bull market, the portfolios did not make it through the third quarter unscathed.

Portfolio 1 for the third quarter: DOWN

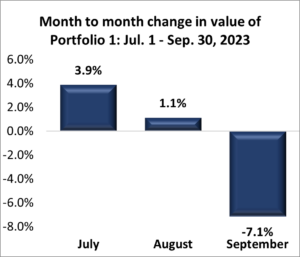

The third quarter started off on the right foot for Portfolio 1 but trended downward before dropping into negative territory for September.

Activity: bought shares in Cameco, Indie Semiconductor, Navitas Semiconductor. Received shares in Liberty Media – Atlanta Braves Holdings, and Liberty Media – Sirius XM Group as part of a split off by Liberty Media’s Formula 1 Group. Sold DocuSign, EnWave Corporation, and ZIM Integrated Shipping Services.

Portfolio 2 for the third quarter DOWN

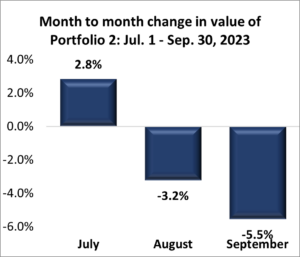

Portfolio 2 started well enough before taking two straight monthly declines.

Activity: bought shares in SmartCentres Real Estate Investment Trust and bought additional shares of Telus.

Portfolio 3 for the third quarter DOWN

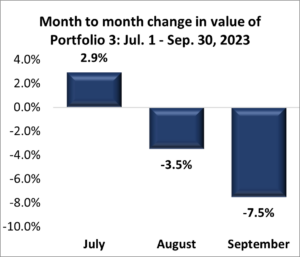

Portfolio 3 followed the same pattern as the other portfolios with a decent monthly gain to start the quarter before a sizable drop to end the quarter.

Activity: bought shares in SmartCentres Real Estate Investment Trust, and Lithium Americas.

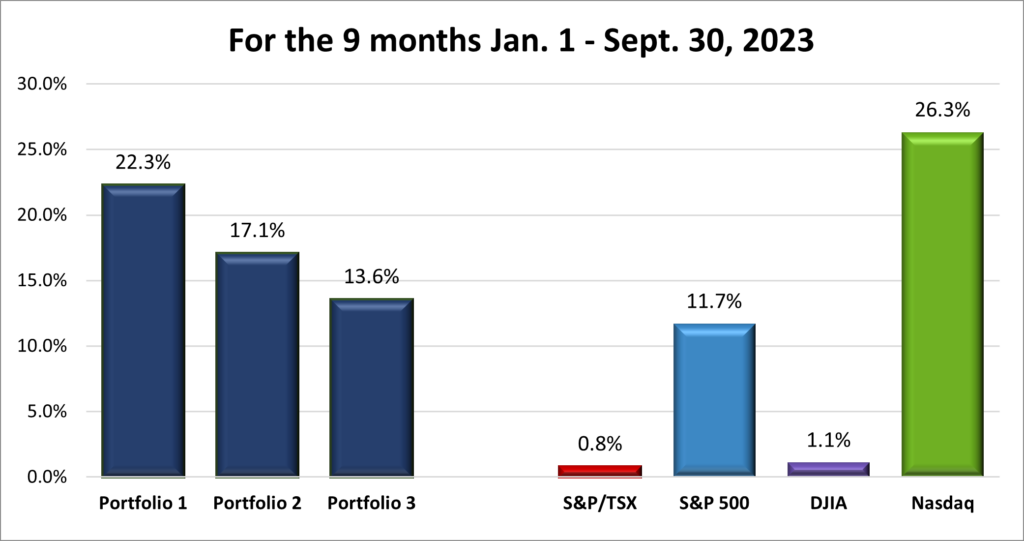

Nine Month Review

For the first nine months of 2023, the TSX (SPTSX) is up 0.8%, the S&P (SPX) gained 11.7%, the DJIA (INDU) rose 1.1% while the Nasdaq (CCMP) advanced 26.3%.

![]() As shown in the chart above, despite a disappointing third quarter, all four indexes remain in the green for the year, even if barely in the green as is the case with the TSX and the DJIA. Growth stocks and the AI boom powered the market for the first half of the year. However, the “higher for longer” interest rates of the third quarter (as the higher rates are referred to) have brought growth stocks back to earth and caused many investors to move to safer government bonds.

As shown in the chart above, despite a disappointing third quarter, all four indexes remain in the green for the year, even if barely in the green as is the case with the TSX and the DJIA. Growth stocks and the AI boom powered the market for the first half of the year. However, the “higher for longer” interest rates of the third quarter (as the higher rates are referred to) have brought growth stocks back to earth and caused many investors to move to safer government bonds.

Tailwinds of the North American stock markets include:

- Strong Corporate Earnings: Many companies, particularly in the technology and energy sectors, posted strong earnings reports exceeding analyst expectations, boosting investor confidence and driving stock prices upwards.

- Resilient Consumer Spending: Despite inflation concerns, consumer spending remained relatively stable throughout the first nine months, supporting economic growth and market optimism.

- Central Bank Policy: The BoC’s and the Fed’s cautious approach to raising interest rates aimed to manage inflation and slow down their respective economies without sending them into a recession. This helped maintain market stability.

- Technological Innovation: Continued advancements in various fields, especially artificial intelligence (AI) fueled investor interest in technology stocks, contributing to their outperformance.

- Geopolitical Stability: War still raged in Ukraine, and the US and China settled into a new cold war. However, the world had adapted to this situation and compared to previous years, the geopolitical environment was relatively less turbulent in 2023. This provided a more favorable climate for investment.

The first nine months of 2023 saw investors move into companies demonstrating long-term growth potential, and sustainability, influencing market dynamics. Value stocks also came back into favor as investors sought stability and undervalued assets during times of market volatility. From an investor point of view, energy company shares fuelled (pun intended 😊) by rising oil prices helped broaden the gains beyond the technology companies.

Another headwind of investing in 2023 was the US benchmark interest rates reached their highest level in 22 years in 2023, reached a peak of 5.5%. In Canada, the benchmark rate climbed to 5.0%, its highest since 2008. These significant increases impacted consumers and businesses across all sectors, leading to increased borrowing costs and dampening economic activity. As a result, many investors began shifting their investments from stocks to safer assets like government bonds, seeking stability and protection from market volatility.

In Canada and the US, the higher interest rates caused government bond yields to remain high. When bonds offer more attractive yields than equities, investors tend to favor them because they are safer and less risky. That can weigh on stock prices which can send the markets lower. However, its likely that both the BoC and the Fed will maintain their current Interest rates throughout the remainder of the year.

While the nine months ended with disappointing third quarter performance, the good news is that the markets were still in positive territory and in a much better place than they were a year ago.

Nine Month Portfolio Review

![]() As with indexes, the Portfolios withstood a challenging third quarter and remain solidly in the green. 😊 As depicted in the chart below, only the Nasdaq outperformed all three Portfolios. Due to all three Portfolios bias towards technology companies, the impressive performance by technology stocks, particularly the so called “Magnificent 7” companies, continues to increase the value of the portfolios.

As with indexes, the Portfolios withstood a challenging third quarter and remain solidly in the green. 😊 As depicted in the chart below, only the Nasdaq outperformed all three Portfolios. Due to all three Portfolios bias towards technology companies, the impressive performance by technology stocks, particularly the so called “Magnificent 7” companies, continues to increase the value of the portfolios.

Looking forward

The fourth quarter offers a fresh start after a challenging third quarter, particularly September. However, much of the investor excitement that fueled markets earlier this year has waned. The “Magnificent 7” technology stocks, once leading the charge, now face a slowdown as the AI hype fades. Additionally, neither central bank shows any signs of reducing interest rates soon, further dampening enthusiasm.

Economic headwinds loom large in the US, including the resumption of student loan payments, the auto workers strike, and the potential for another government shutdown. These factors could lead to lower consumer spending and impact America’s fourth-quarter Gross Domestic Product (GDP).

In Canada, slumping oil prices and lower earnings within the major banks (due to increased cash reserve requirements) pose significant challenges for the TSX. Energy and banking sectors combined represent over 31% of the index, making their participation crucial for any significant upward movement.

Technology companies, particularly the “Magnificent 7,” were instrumental in the first half’s market surge and continue to contribute to overall gains. These seven companies, representing a substantial 28% of the S&P’s market capitalization, highlight their considerable influence. However, their upward momentum has stalled recently, particularly in September. This pullback could present a buying opportunity for investors seeking long-term growth potential in these and other growth-oriented companies.

The future of the North American stock markets depends on numerous factors, including the global economic outlook, geopolitical developments, and the future monetary policy decisions of the BoC, and more importantly, the Fed. While uncertainties remain, continued technological innovation, potential economic growth, and the focus on sustainability offer promising opportunities for future market performance.

The fourth quarter will likely be shaped by continued uncertainty about interest rates and the global economy. However, the strong performance of certain sectors, such as energy and technology, offers hope for potential gains in the remainder of the year. For the 2023 rally to continue, broader sector participation and inclusion of mid and small-cap stocks are crucial.

Perhaps the biggest question for the next quarter and the new year is what the central banks will do with interest rates. Despite their strong rhetoric, I believe interest rates may have peaked. The larger question is when they will start to lower them, a move eagerly awaited by investors as it could lead to renewed confidence and optimism, potentially driving the markets higher.

After two bullish quarters, the third quarter saw the bears make an appearance. Here is hoping to a return of the bull in the fourth quarter. 😊