Yes Virginia, the market does go down.

After nearly two years of relentless gains, this week we were reminded that share prices, even those of the biggest companies, do in fact go down. If you started investing after the start of the pandemic, then welcome to the ‘exciting’ part of investing. Friday capped a dismal week for the four major North American Indexes. The S&P 500 notched its worst week since March 2020 and all four major North American Indexes – the Toronto Stock Exchange Composite Index (TSX), S&P 500 (S&P), Dow Jones Industrial Average (DJIA) and Nasdaq Composite Index (Nasdaq) – were below their 200-day moving averages on Friday. The last time they traded below their respective 200-day moving averages was in the second quarter of 2020, near the beginning of the Covid-19 pandemic. This is not a good sign as the 200-day moving average helps identify the underlying trend of the index and consecutive days below the 200-day average indicates an overall downward trend.

This type of fall hit the growth stocks hardest, although all stocks tend suffer when an Index falls. When the entire market falls, emotion starts to enter the decision-making process and nervous investors start selling, driving prices lower. The cycle becomes self fulfilling. The more the share prices decline, the more people panic and sell their shares, the more shares available, the lower the share price. Repeat. I remember checking the portfolios when the pandemic started in March 2020, and it wasn’t pleasant seeing them down over 30%. I didn’t sell any shares, but rather bought shares in several companies and rode the updraft when the market took off. For me, the best thing I can do is nothing. I’ll look over the holdings in all three Portfolios to try and identify the best companies so I can deploy any extra cash to add a few shares here and there while they are ‘on sale’.

Given the downward movement of the Indexes over the last few weeks, it will be interesting to see what the Bank of Canada and the US Federal Reserve do this coming week when they have their individual meetings to discuss their respective monetary policies and future interest rate hikes. It is also the start of earnings season, leading off with some of the largest technology companies. More aggressive interest rates hikes, combined with poor earnings reports, especially the larger companies such as Apple (NASD:AAPL) and Microsoft (NASD:MSFT), could make for a very unpleasant week. Enough about next week, lets see what happened this past week to the Indexes and the Portfolios (hint: not good).

Weekly Market Review

Monday: The Toronto Stock Exchange Composite Index (TSX) was driven upward by the energy and financial sectors, closing at its highest since late November. The week is off to a good start. Let’s see if it will last.

The US markets were closed in honour of Martin Luther King Jr. Day.

Tuesday: It turns out Monday’s upward momentum generated by the TSX was short lived. A rough day in the markets, with the TSX, S&P 500 (S&P), Dow Jones Industrial Average (DJIA) and Nasdaq Composite Index (Nasdaq) all down. In the US, The DJIA was dragged down by the financial sector which fell after US bank Goldman Sachs (NYSE:GS) missed their quarterly profit estimates. The S&P and Nasdaq were weighed down by the big technology stocks, including Apple and Microsoft, after a rapid rise in the yield of the benchmark US Treasury yields (in the form of T-bills, T-notes and T-bonds), which jumped to a two year high. Higher Treasury yields, in anticipation of forthcoming higher interest rates, tends to have an adverse effect on growth stocks, such as technology companies, because higher interest rates mean more money is put toward borrowing costs than into growing the business.

The Nasdaq is down nearly 10% since its record high in mid November, indicating a correction in the Index is taking place.

North of the border, the TSX was also impacted by the rise in US Treasury yields that caused the TSX’s technology sector to fall over 3%.

Wednesday: Rising inflation rates in Canada continue to fuel fears of sooner than anticipated interest rate hikes by the Bank of Canada to tamp down inflation which rose to 4.8% in December. That was the ninth consecutive month where inflation exceeded the Bank of Canada’s 1% – 3% range. On the TSX, the technology sector fell to its lowest level since May 2021 and has tumbled 25% since it peaked in September.

In the US, the Nasdaq is officially in a correction as it ended the day down 10.7% since mid November. Concerns that the US Federal Reserve will move aggressively to control inflation through sharper interest rate hikes continue to take a toll on all three US Indexes. The Nasdaq and S&P have been particularly battered as they are home to many technology companies and other growth stocks. Fears of rising interest rates weighed down the consumer discretionary sector stocks, as well as the technology sector.

Thursday: Despite a strong mid day rally caused by bargain hunters, all four Indexes faded when the bargain hunting lost steam, causing the four Indexes to end the day lower. Concerns about inflation and higher interest rates continue to weigh on the markets. On the TSX and S&P, ten of the 11 sectors fell today for a broad-based decline. Utilities barely made into positive territory for the day. The TSX, Nasdaq and DJIA slipped below their respective 200 day moving averages. The Nasdaq is now down nearly 12% from its all time high in November and at its lowest level since June 2021. The S&P is down nearly 6% in 2022.

Friday: Another rough day to end what has turned out to be a dreadful week for all four Indexes. In Canada, the TSX fell to a one month low thanks to its biggest 1-day decline since the end of November. Both the energy sector (lower oil prices) and technology sectors dropped nearly 3.5%. Shopify (TSX:SHOP) fell over 13%, knocking it down to the third most valuable company in Canada.

In the US, the DJIA fell for the sixth consecutive day, matching its longest losing streak since February 2020. Both the S&P and Nasdaq had their worst weeks since the start of the pandemic, with the S&P sinking below its 200-day moving average Friday afternoon. The catalyst for today’s selloff seems to have been a weak earnings report from streaming giant Netflix (NASD:NFLX) and they predicted weaker subscriber growth going forward. As a result, Netflix fell almost 22%, but it also dragged down other streaming competitors like Disney (NYSE:DIS) and Roku (NASD:ROKU).

Weekly Portfolio Review

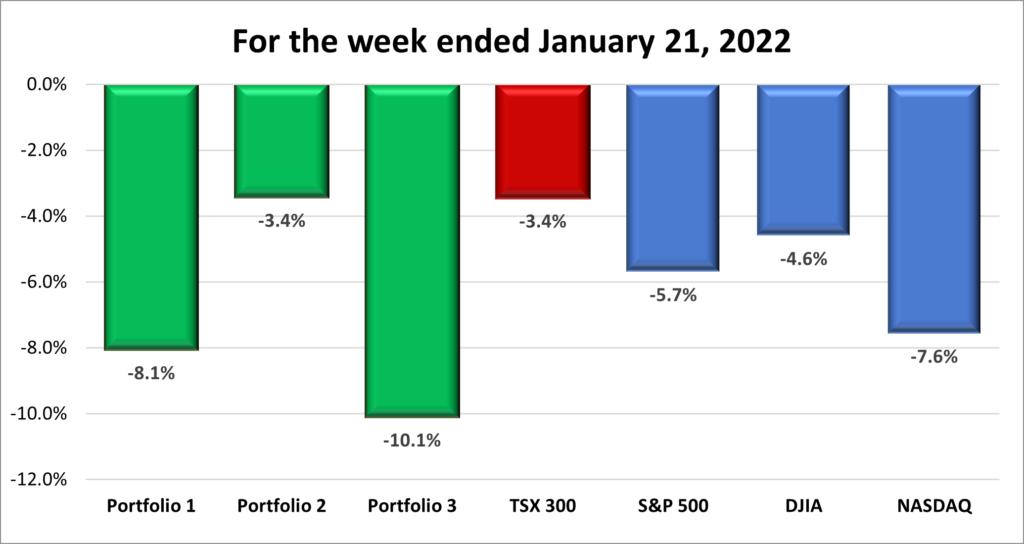

Considering how poorly the Indexes performed last week, the only surprise was Portfolio 2 was only down 3.4%, tied with the TSX for the top performer of the week (a dubious award this past week). Otherwise, Portfolio 1 almost had double digit losses, but Portfolio 3 did make it into double digit losses. The only positive I can take from the past week is the entire market was beaten down and there is little I could have done to prevent the losses short of changing my investing plan. And I’m not going to do that.

Companies on the Radar

There are a lot of good companies currently on ‘sale’ but there are five I’m focused on. Four of the companies are already in at least one of the portfolios: Nvidia (NASD:NVDA), Home Depot (NYSE:HD), Microsoft and Trisura (TSX:TSU). The only company not in a portfolio is American Tower (NYSE:AMT), which I like for the growing demand for 5G connectivity. The question with all these companies is, will share prices continue to fall, and if so, how far? For now, I’ll sit on the sideline while I look for the best deal.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended January 21, 2022: DOWN ![]()

Portfolio 1 benefited from the high growth technology companies for the last two years and now, unfortunately, its reaping the downside of all those growth stocks – volatility and sharp declines – as those good times have come to an end. Hopefully not for long. Many of the former highflyers are either setting new 52-week lows, or worse, all-time lows. For example, Roku dropped nearly 10% on Friday and is down 65% from its all time high in the summer of 2021. There was no Roku specific news causing the fall, but the company’s shares were likely impacted by Netflix’s 22% decline.

Unfortunately, this sharp fall is not unique to Roku as all the stocks in Portfolio 1 are down, but its most extreme with the high growth companies. I believe I invested in quality companies that will survive this downturn and will prosper in the long term. The only thing to do is stay calm and carrying on with my investing plan.

The good news, it was a good week for dividends (another dubious distinction when the dividends are greater than the increase in the share price for the entire portfolio).

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Automotive Properties Real Estate Investment Trust (TSX:APR.UN) DRIP

Andlauer Healthcare Group Inc (TSX:AND)

Algonquin Power & Utilities Corp (TSX:AQN) DRIP

Brookfield Select Opportunities Income Fund (TSX:BSO.UN)

US $

BSR Real Estate Investment Trust (TSX:HOM.U)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended January 21, 2022: DOWN ![]()

The best performer in a bad week but there was some good news. On January 18, Microsoft announced it would purchase Activision Blizzard (NASD:ATVI) for USD $68.7 billion. This will be Microsoft’s largest ever acquisition and make it the third largest gaming company in the world. Microsoft will acquire two of the largest gaming franchises in Call of Duty, World of Warcraft and the popular mobile game Candy Crush. These titles will not only help Microsoft’s Xbox gaming division become a gaming powerhouse but also help it put a stake in the ground in the growing ‘metaverse’. The deal is expected to close in 2023 but first must receive regulatory approval from various governments.

My Take: Currently, Microsoft’s cloud platform, Azure, sits in the number 2, behind market leader Amazon AWS (NASD:AMZN), and well ahead of number three Google (NASD:GOOGL). Microsoft is the leader in office applications thanks to its’ Office 365 platform. Google Workspace is the only competitor that comes to mind. With the acquisition of Activision Blizzard, they become a juggernaut in the growing gaming industry. While I’m not a gamer, I know lots of people who are, and I’m aware of the titles Call of Duty, World of Warcraft and Candy Crush. Activision brings games that can be played on computers, gaming consoles (like Xbox and PlayStation) and mobile devices like smartphones. With this acquisition, Microsoft has its foot in the door to all these platforms, and in some cases it’s a big foot. Their sites are clearly on #2 Sony (NYSE:SONY) (whose share price plunged on the deal announcement) and eventually challenging Nintendo for the #1 position. This provides Microsoft with another fast-growing source of revenue and the potential to overall ‘rule the cloud’.

I also see Microsoft using its subscription gaming service as a gateway to its own metaverse, if not the whole metaverse (a virtual world where people can interact and transact with each other). Gamers are already socializing through their game play so why not initially create virtual locations where people can hang out while waiting to play a game or embark on some other social adventure. Its much easier to get people to hang out at your virtual locations when they already have a reason to be online, such as a multiplayer game. Make these virtual locations the ‘place to be’ and sooner or later these ‘locations’ will be accessible by anyone and everyone. Microsoft’s virtual locations will become virtual destinations in the metaverse. I’m sure Microsoft will get a piece of any transactions that take place in that ‘world’.

Then again, I could be completely wrong. 😊

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended January 21, 2022: DOWN ![]()

It was not a good week for Portfolio 3. It was like the title of an old spaghetti western – The Good, The Bad, and The Ugly. Actually, that same title could apply to the three portfolios, with Portfolio 3 being the Ugly. For now, lets look at the Good, the Bad and the Ugly of Portfolio 3.

The good: Microsoft announced that they were acquiring gaming company Activision Blizzard, as outlined in Portfolio 2.

The bad: Live by the sword, die by the sword. Portfolio 3 rode Shopify up and now its riding it sharply down. Portfolio 3’s largest holding, fell 13.4% on news Shopify terminated contracts with several warehouse partners. Nothing has been made official, but rumour has it Shopify is moving from third party fulfillment centres to their own warehouses. According to Shopify, these changes will make fulfilling orders easier and less expensive to the benefit of merchants and consumers.

The ugly: The best performing stock over the 5-day period was Adyen (OTCM:ADYEY) which somehow only dropped USD $.08. All the other holdings were down, including the financial companies which had been one of the few bright spots so far in 2022. The biggest weight was Shopify which dropped nearly CAD $270 over the five days. Portfolio 3 is definitely undergoing a correction. ☹

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.