The First Quarter is behind us

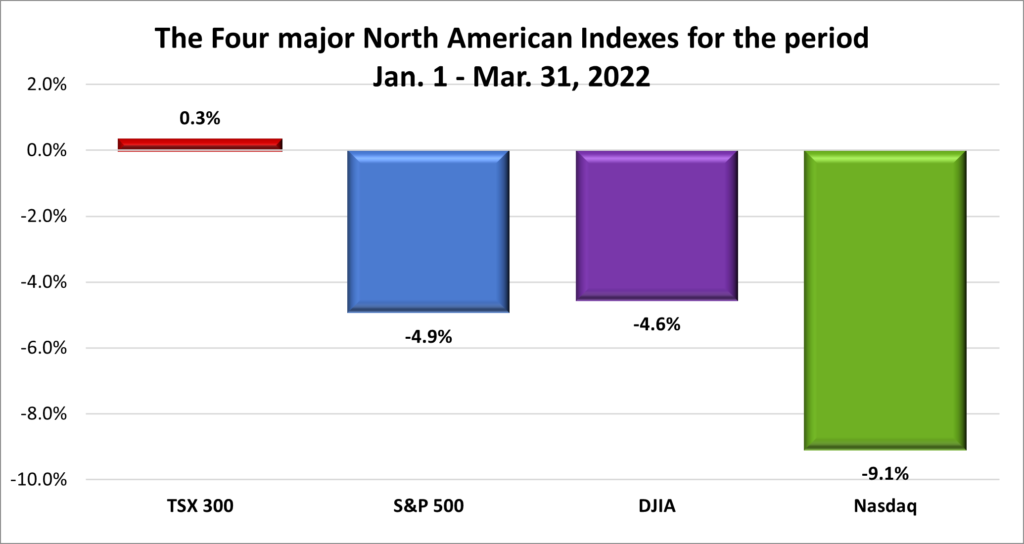

From an investment standpoint, the first quarter of 2022 was not good. The Canadian Index, the Toronto Stock Exchange Composite Index (TSX), was the only Index to post a gain for the first quarter. All three American Indexes, the S&P 500 Index (S&P) higher, the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) posted losses for the first quarter, and that was after a mild rally in March to make it look respectful.

During the first three months of 2022, all three US Indexes entered a correction (a drop of 10% – 20% from their respective highs), with the Nasdaq entering a bear market (a drop of 20% or more from its all time high). A few events contributed to the decline including the Russian invasion of Ukraine, inflation continued to climb in Canada and the US leading to fears of aggressive interest rate hikes by Canada’s Bank of Canada and the US’s Federal Reserve, and fears of how ongoing Covid-19 infections would impact global markets.

As we turn to the second quarter of 2022, fears of Covid-19 have diminished as most countries open and attempt to return to normal. In an attempt to control rising inflation, interest rates have gone up a quarter percentage point in both Canada and the US, with talks of another half percentage point hike in the coming weeks. Next week, the Bank of Canada is schedule to announce a rate hike. It is anticipated to be an increase of .5% bringing the Canadian interest rate to 1%. This is the interest rate banks pay, not the rate consumers or businesses will pay. You can be sure the rate we pay will be higher in order for the banks to make money on their loans.

On the other side of the world, the invasion of Ukraine has not gone how Russia imagined. Instead of rolling over Ukraine, the war continues with Russia now focusing on gaining control of eastern Ukraine after failing to gain control of Kyiv, the capital of Ukraine, and the surrounding region. Hopefully, all these issues will be resolved sooner rather than later, and no new events or issues will come along to rattle the markets. April has historically been the best month for US stocks since World War II. Let us see how April and the second quarter started out….

Weekly Market Review

Monday: The first week of trading got off to a good start with all four major North American Indexes posting a gain for the day. In Canada, the TSX, was led upward by the Technology and Energy sectors. I cannot remember the last time I saw those two sectors lead the way on the TSX on the same day. Usually if one is up, the other is down.

In the US, the mega market cap tech stocks Apple (NASD:APPL), Microsoft (NASD:MSFT) and Tesla (NASD:TSLA) help propel the Nasdaq and the S&P higher, with the DJIA getting lifted by the general market updraft.

Tuesday: US Federal Reserve Governor Lael Brainard said it was “of paramount importance to get inflation down.” With that, fears of a more aggressive US Federal Reserve rate caused the markets in the US to decline, with the TSX getting caught in the downdraft. In Canada, the TSX temporarily reached an all time high before falling back. The Canadian Energy, Materials and Technology sectors weighed down on the TSX. In the US, the Nasdaq had its worst day in a month with declines in technology mega cap companies such as Apple and Microsoft.

Wednesday: Tuesday’s words from the US Federal Reserve continue to haunt the North American markets with all four Indexes declining for a second straight day. The Fed released the minutes from their March meeting showing strong support by Fed members for more aggressive rate hikes, including multiple .5% rate hikes to control surging inflation.

Meanwhile, in the markets, the defensive Utilities sectors performed the best in both countries. On the downside in Canada, the Canadian Technology and Financial sectors dropped the most, while in the US, the S&P’s Technology and Consumer Cyclicals sectors fell the most.

Thursday: Despite ongoing concerns about the Russian invasion and a more aggressive US Federal Reserve, the four Indexes climbed back into positive territory today thanks to a late afternoon rally. In Canada, the TSX was led by the Materials and Energy sectors. As well, the Canadian government released the latest federal budget after the cIose of the Canadian markets. In the US, Healthcare and Energy sector stocks led the way.

Friday: The last day of the week was a mixed bag with the TSX and DJIA inching above the bar into positive territory while the technology heavier S&P and Nasdaq ended below the bar. The TSX was lifted by the resource sectors (Energy and Materials) and the Financial sector. In times of inflation and rising interest rates, these sectors tend to outperform the other eight sectors. Together these three sectors account for 57% of companies in the TSX Composite so when they do well the TSX tends to follow along, as has been the case in 2022.

In the US, investors also tend to move into US banks stocks when interest rates move higher, which is what happened Friday. The big US banks are a bigger component of the DJIA than the S&P and the Nasdaq, which is a main reason the DJIA gained on the day while the S&P and Nasdaq declined.

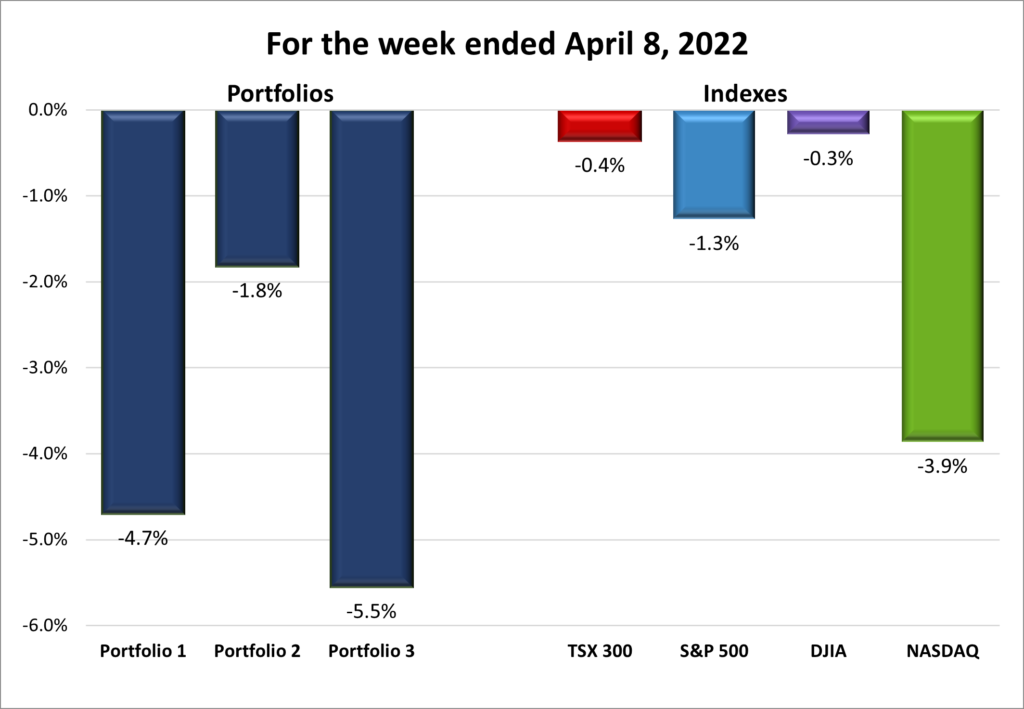

For the week, the TSX fell -.4%, the S&P dropped -1.16%, the DJIA declined -.28%, and the Nasdaq sank -3.86%. I am glad I am only following four Indexes as I am running out of ways to say declined. 😊

Where’s the weekly chart of the indexes ?

There will be no weekly chart for the Indexes. For the last few weeks, the change in the Indexes, as reported above, has not been reflected in the chart. This is very frustrating because the end of the week numbers used to calculate the change are easy to find by checking Yahoo Finance!, MSN Finance, Google Finance or your online trading account on a Friday after the extended market close (after 5:00 pm Pacific). After doing the math to compare these numbers to the previous Friday’s closing numbers, the calculations match the numbers provide by Refinitiv (formerly Thomson Reuters Finance). Even comparing the finance websites mentioned previously, the charts do not match. As I said, very frustrating. Once I figure out why the charts do not reflect the calculated changes in the Indexes, the weekly chart will re-appear.

Weekly Portfolio Review

With both the Bank of Canada and the US Federal Reserve indicating they are prepared to slow the economy to get inflation under control, this past week was not a good week all around. Higher interest rates are not good for technology companies or high growth companies that are using debt to fuel their growth (more money will be required to service the debt, therefore less money to grow the business). All the Indexes and all the Portfolios declined for the week. If April has historically been the best month for the American markets, it has gotten off on the wrong foot. Even the TSX which has done well throughout 2022 had an off week.

With all four Indexes falling for the week, its no surprise all the Portfolios are down. The technology heavy Portfolios 1 and 3 dropped over 4% and 5%, respectively, for the week, perhaps the worst single week since I have been writing this blog. By comparison, the more diversified Portfolio 2 dropped only 1.8%. I was not tracking the Portfolios during the high growth cycle of 2020 – 2021 so I do not know if Portfolios 1 and 3 significantly outperformed Portfolio 2, but I am interested to see how the Portfolios compare during a growth cycle. This current market pullback is not great for any of the Portfolios, but Portfolio 2 definitely seems to be holding up better in this current environment.

In the meantime, let us hope the markets revert to their historic norms and starting heading upward for the rest of April.

Companies on the Radar

Not much happening on the radar front. For now, I am content to sit on the sidelines rather than churn the account for the sake of doing something. I would rather do nothing than pay transaction fees and possible taxes. However, the usual suspects remain at the top of my list:

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended April 8, 2022: DOWN![]()

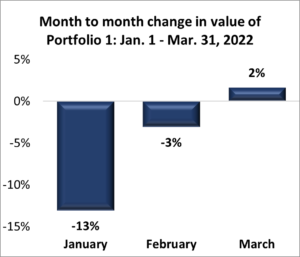

The first quarter was not good for Portfolio 1, dropping 14.2%. The technology companies and other high growth companies in Portfolio 1 felt the sting of the higher interest rates and anticipated future higher interest rates. Many of the earnings reports for the companies in the portfolio were good but that did not seem to matter as investors fled to more conservative companies, bonds, or cash. I am satisfied with most of the companies and expect them resume their upward ways once the markets start climbing again.

In other news relevant to Portfolio 1 companies:

- On a positive note, the investment in Berkshire Hathaway (NYSE:BRK.B) was one of the few companies that posted a gain this past week, although it is still a few dollars below the price I paid. Part of the reason I became an owner in Berkshire Hathaway was to gain exposure to a diverse mix of value-based stocks. When growth stocks are out of favour, as they currently are, it is great to own a company that has proven itself when value investing is the name of the game. No one does value investing better than Berkshire Hathaway.

- Speaking of value investing, Berkshire Hathaway took out a USD $4.2 billion dollar position in HP Inc. (NYSE:HPQ), giving at an 11.4% interest in the company.

- ZIM Integrated Shipping (NYSE:ZIM) paid out a whopping 117.6% dividend, or USD $17 per share, this past week. I doubt this will be a regular occurrence, but I would be pleased if it were. The only drawback is losing 25% of the dividend to the taxman. ☹

- GM (NYSE:GM) and Honda (NYSE:HMC) will co develop lower priced electric vehicles in an attempt to beat Tesla’s sales numbers. This follows on existing plans for GM to build two electric SUVs for Honda beginning in 2024.

- On Monday it was revealed that Elon Musk, CEO of Tesla, is the largest shareholder of Twitter (NASD:TWTR) with a 9.2% stake. On Tuesday, Twitter announced Musk had accepted a seat on their Board of Directors. Musk has filed a regulatory form indicating he intends to be an activist, rather than passive, investor. It will be interesting to see where this goes as Musk had previously tweeted about starting his own Twitter competitor.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Cargojet Inc. (TSX:CJT)

US $

ZIM Integrated Shipping (NYSE:ZIM)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended April 8, 2022: DOWN![]()

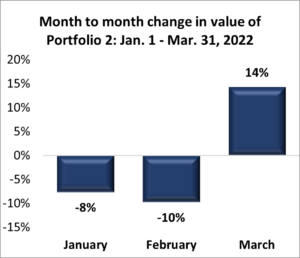

Portfolio 2 was the best of the three portfolios in the first quarter, only dropping 4.6%. You know it is a bad quarter when you describe your best performer as “only losing…”. Hope I do not have to use that phrase very often in the future. 😊 Portfolio 2’s fall was limited by its more conservative mix of companies and is therefore less volatile compared to the other two portfolios. The portfolio is more diversified and many of the companies in this portfolio are dependable dividend payers which also helped. With limited losses, this strategy seems to have paid off.

Elsewhere in Portfolio 2, Guardant Health (NASD:GH) announced a deal that will make its cancer tests available as part of routine medical care. Once setup, Doctors will be able to order Guardant’s tests and access those results directly from within patients’ records. Easier access to Guardant’s products and services should help boost Guardant’s revenue.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Alimentation Couche-Tard Inc (TSX:ATD)

Brookfield Renewable Partners LP (TSX:BEP.UN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended April 8, 2022: DOWN![]()

The first quarter was terrible for Portfolio 3, dropping 25.3%. Ouch! Being technology and growth oriented didn’t help but with Shopify (TSX:SHOP) accounting for nearly 40% of the portfolio value, its no surprise Portfolio 3 fell this hard. Shopify has dropped over 50% since its all time high in 2021. Given how far Shopify has dropped, I am glad the damage to the Portfolio was not worse. Fortunately the financial stocks, Royal Bank (TSX:RY), TD (TSX:TD) and goeasy (TSX:GSY), were able to limit the loss. As with the other two portfolios, I am satisfied with companies in this portfolio and expect their respective share prices to start to follow the growth of the businesses.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

TD U.S. Equity Index ETF (TSX:TPU)

Brookfield Asset Management Inc (TSX:BAM.A)

Brookfield Renewable Partners LP (TSX:BEP.UN)

goeasy Ltd (TSX:GSY)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.