Tax double whammy

On April 7, the Canadian government introduced the latest federal budget. Once again, rather than living within its means or taking advantage of natural strengths to fund their pet projects, the government committed to spending more taxpayer money than they take in. Rather than debate the pros and cons of the various components in the budget that will leave less money in your wallet now and in the future, let us look at one short sighted item that impacts us as consumers and as investors.

As part of the budget, the Canadian government announced a retroactive 15% tax on financial and insurance companies that had revenues of more than CAD $1 billion in 2021. Imagine if the government decided to retroactively impose a tax of any amount on your past income. I suspect you would not be too happy. But wait, it gets better. The government also plans to permanently increase the tax rate for banks and insurance companies to 16.5% on income greater than 100 million.

While this makes a good sound bite – make the big companies pay more – in reality it hits us both as consumers of financial services and as investors. A couple of questions immediately come to mind.

First, what are the chances this government will eliminate a tax when it needs money? Governments in general, but this current one especially, likes to tax everything they can get away with. Have you ever known a government to completely drop a tax? As long as this government needs money, I think we will see some variation of this tax on top of the annual 16.5% tax banks and insurance companies must pay going forward.

Second, what are the chances the banks absorb this tax rather than pass it through to us consumers? Canada’s big five banks did not get big by absorbing costs. This tax will be passed through by raising existing bank charges or introducing new fees. In a sense, this new bank tax will be paid by us, not the banks,

Now, lets look at how these taxes will impact us as investors. Banks and insurance companies are mainstays of many portfolios and pensions because of their stability and their ability to pay and grow their dividends. These dividends come from the revenues these companies generate. The more revenues, the greater the dividends. When banks do well, shareholders benefit in the form of increasing dividends. With these new taxes, money that would normally be used to pay and increase dividends will now go to the government instead of shareholders. I do not see banks decreasing their dividends, but I also suspect dividends will not grow at the same rate they grew in the past.

At the end of the day, these new bank taxes will impact us as consumers in the form of higher bank fees as banks ‘pass through’ this tax. As investors, money that would have gone to shareholders, in the form of increased dividends, will now go to the government. In other words, this tax on big banks sounds good but it is us who will pay the tax, not the banks.

Enough about taxes, lets see what happened in the markets this past week…..

Weekly Market Review

Monday: The short week started with a decline as all four major North American Indexes opened with losses. On the Toronto Stock Exchange Composite Index (TSX), Financial and Materials sectors gains were not enough to overcome the drop in the price of oil and the resultant drop in Energy companies. Oil fell on concerns of slowing demand in China thanks to lockdowns caused by the spread of the latest covid-19 variant.

In the US, the Dow Jones Industrial Average (DJIA) had the ‘best’ day of the American Indexes, only falling 1.2%. On the S&P 500 Index (S&P), all 11 sectors in ended in the red, with the US Energy sector the biggest loser thanks to the fall in the price of a barrel of oil. Bringing up the rear or leading the charge downward depending on your point of view, the Nasdaq Composite Index (Nasdaq) had the biggest decline, led downward by the numerous Technology sector and interest rate sensitive growth stocks on the Exchange.

Tuesday: Despite morning advances, the Indexes extended their respective losing streaks for another day. It was the second day in a row for the TSX. Gains in the Energy and Materials sectors were not enough to overcome declines in all the other Canadian sectors. In America, Energy, Materials and Utilities were the only US sectors to post an increase.

The primary catalyst for the declines was a higher-than-expected US Consumer Price Index (CPI) which rose 8.5% in March, the highest in 40 years. Much of the CPI increase was a result of higher prices at the gas pumps which forced the cost of just about everything else higher. In Canada, on top of the high CPI in the US, the Bank of Canada is expected to announce a .5% interest rate hike tomorrow.

Wednesday: The losing streaks ended abruptly today with all four Indexes advancing. Is this a hiccup in a downward trend or the start of a move upward? We will see tomorrow.

The TSX continues to be driven by the Energy and Materials sectors. In the US, the Consumer Discretionary and Technology sectors led today’s rally. The big US banks kicked off first quarter earnings today, with JP Morgan leading off. The bank reported a 42% drop in quarterly profits and lower profits going forward. I am guessing a significant cause was tied to the Russian invasion of Ukraine.

In Canada, the Bank of Canada raised its interest rate by 50 basis points, or .5%, on Wednesday in an attempt to reverse soaring inflation. Another half dozen or so hikes are expected throughout the next year, with increases ranging from .25% – .5%. Canada has not seen inflation this high since the early 1990s. Following on that announcement, Canada’s big five banks will raise their prime lending rate to 3.2%, the highest it has been in two years, effective Thursday.

Thursday: In Canada, a good day for the Energy and Materials sectors pushed the TSX into the black, overcoming a decline in the Technology sector that was the result of higher interest rates announced Wednesday. Cash used to pay interest is cash that cannot be used to fund growth.

It is looking like Wednesday gain was a hiccup as all three American Indexes declined, led downward by the technology heavy Nasdaq. Thanks, to higher oil prices, the Energy sector was the only sector to end up on the positive side of the ledger.

The Energy sectors in both countries were driven higher on rumours the European Union might initiate a ban on Russian oil imports.

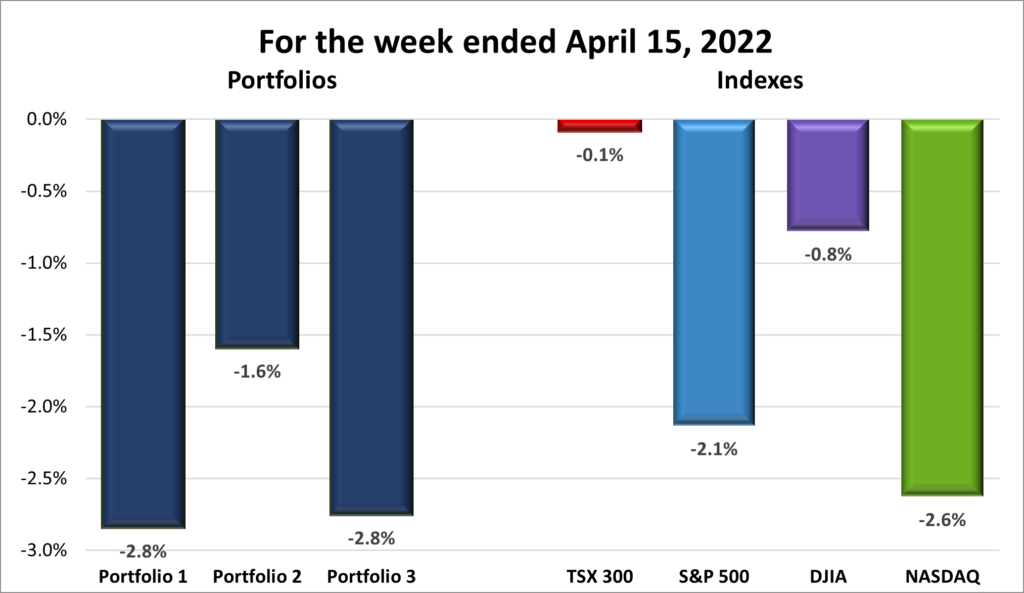

For the week, the TSX was down .1%, the S&P declined 2.1%, the DJIA fell .8% and the Nasdaq fell 2.6%.

Weekly Portfolio Review

Down, down, down, down. That is the direction for each of the Indexes this past week. Once again, the invasion of Ukraine and its impact on global supplies of oil and wheat; the continuing fluctuation in the demand for oil and the resulting price swings; the impact of higher oil prices on fuel and food leading to surging inflation in both countries; and the likelihood of higher and more interest rate hikes. All these issues put downward pressure on the Indexes.

With the Indexes falling, there was only one likely outcome for the Portfolios – down. There is nothing I can do to change the direction of the Indexes, so I must walk the walk of patience and discipline. Not particularly exciting but the alternative will increase costs and probably cause more damage to the portfolios than doing nothing.

Companies on the Radar

All quiet on the radar front. With limited cash, patience is the key in these falling markets. The usual suspects remain at the top of my list:

- Nvidia (NYSE:NVDA)

- Microsoft (NASD:MSFT)

- Apple (NASD:AAPL)

- Home Depot (NYSE:HD)

- American Tower (NYSE:AMT)

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended April 15, 2022: DOWN![]()

- Tales of Elon: No, its not a movie. For Tesla (NASD:TSLA) CEO and founder Elon Musk it has been a busy few weeks dealing with Twitter (NASD:TWTR). After announcing a 9.2% stake in Twitter the previous week, he was offered and accepted a seat on Twitter’s Board of Directors as an activist investor. Early this past week, he abruptly declined the seat on the Board (I suspect as a Director, his fiduciary responsibilities would prevent him saying/tweeting things that could run afoul of the Securities Exchange Commission). Late this past week, Musk announced a hostile takeover bid of Twitter for USD $41.4 billion, or $54.20 per share. On Friday, Twitter adopted a ‘poison pill’ to prevent this and any other hostile takeover bids. Good to see the CEO of Tesla spending so much time on another company that will not add value to Tesla. I expect we will hear more from Mr. Musk in the coming days.

- PayPal (NASD:PYPL) announced its Chief Financial Officer John Rainey will be stepping down. Walmart (NYSE:WMT) subsequently announced that Mr. Rainey will become its CFO effective June 6, 2022. This is a big move for Rainey, considering that he has been with PayPal for almost 7 years, and leaving a high growth technology company for a more traditional company (although Walmart does utilize a lot of cutting edge technology).

- Alphabet (NASD:GOOGL) is investing USD $9 billion in data centres and office space for its flagship company Google.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Shaw Communications Inc.

All currency listed in CAD dollars

Selected highlights from their second quarter 2022 financial results on April 13, 2022

- Consolidated revenue decreased by 2.0% to $1.36 billion, compared to the prior year

- On a year over year basis, net income decreased 9.7% to $196 million

- Free cash flow for the quarter of $217 million decreased 12.5% compared to the prior year.

Portfolio 2

Portfolio 2 for the week ended April 15, 2022: DOWN![]()

Noting to report for Portfolio 2 other than Brookfield Infrastructure Corp (TSX:BIPC) was the only company to post a gain this past week. Of the other companies in the portfolio, 14 were down and another 5 were essentially flat.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Telus Corp (TSX:T) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended April 15, 2022: DOWN![]()

Two announcements from Shopify (TSX:SHOP) to start the past week. The first announcement was a 10 for 1 share split, upon approval by shareholders. This will not change the value of the company (share price x shares outstanding) although it will make shares seem cheaper which will appeal to retail investors. While this does not change my ownership stake in the company, it does make it mentally easier for me to sell a few shares for diversification purposes. For example, selling 5 shares when I own 20 shares feels worse than selling 50 shares if I had 200 shares. In the first situation, I would have ‘only’ 15 shares remaining, while in the second case, I would have 150 shares left. I know it is a mental thing, but I would rather have 150 shares than 15 shares, even though the dollar value is the same.

The other announcement was a new class of shares – “Founder shares” – for founder and CEO Toby Lutke. The ‘founder shares’ will have a variable number of votes that when combined with Mr. Lutke’s other shares will ensure he has 40% of the total voting power. The new voting structure will ensure Lutke maintains control of Shopify as long as he is a Director or executive officer. The founder share is not transferable and should he leave Shopify, the founder share will expire. I have no problem with this as Shopify has done OK since he founded the company. 😊

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.