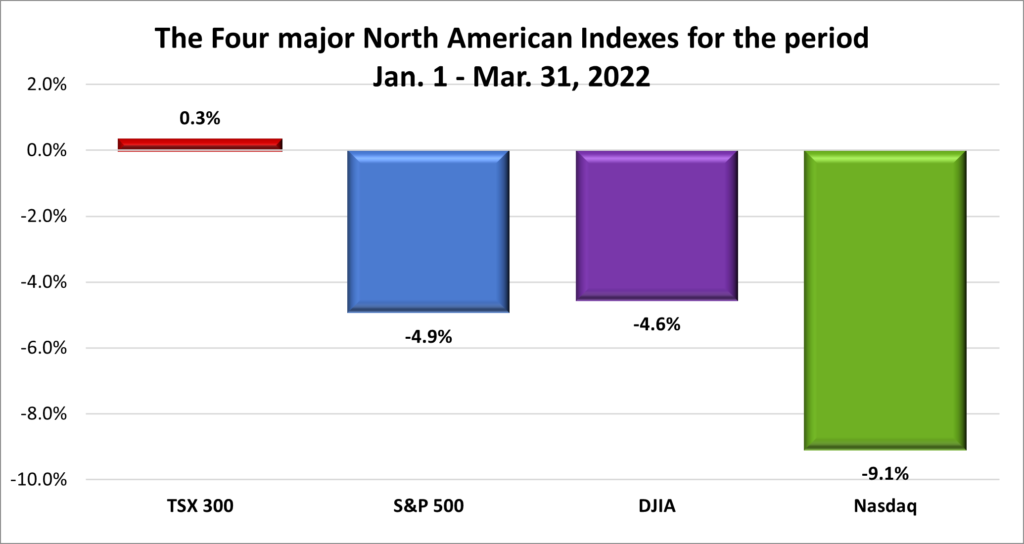

From an investment standpoint, the first quarter of 2022 was not good. The Canadian Index, the Toronto Stock Exchange Composite Index (TSX), was the only Index to post a gain for the first quarter. All three American Indexes, the S&P 500 Index (S&P) higher, the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) posted losses for the first quarter, and that was after a mild rally in March to make it look respectful.

Index performance for the first quarter of 2022

During the first three months of 2022, all three US Indexes entered a correction (a drop of 10% – 20% from their respective highs), with the Nasdaq entering a bear market (a drop of 20% or more from its all time high). A few events contributed to the decline including the Russian invasion of Ukraine, inflation continued to climb in Canada and the US leading to fears of aggressive interest rate hikes by Canada’s Bank of Canada and the US’s Federal Reserve, and fears of how ongoing Covid-19 infections would impact global markets.

As we turn to the second quarter of 2022, fears of Covid-19 have diminished as most countries open and attempt to return to normal. In an attempt to control rising inflation, interest rates have gone up a quarter percentage point in both Canada and the US, with talks of another half percentage point hike in the coming weeks. Next week, the Bank of Canada is schedule to announce a rate hike. It is anticipated to be an increase of .5% bringing the Canadian interest rate to 1%. This is the interest rate banks pay, not the rate consumers or businesses will pay. You can be sure the rate we pay will be higher in order for the banks to make money on their loans.

On the other side of the world, the invasion of Ukraine has not gone how Russia imagined. Instead of rolling over Ukraine, the war continues with Russia now focusing on gaining control of eastern Ukraine after failing to gain control of Kyiv, the capital of Ukraine, and the surrounding region. Hopefully, all these issues will be resolved sooner rather than later, and no new events or issues will come along to rattle the markets. April has historically been the best month for US stocks since World War II. Let us see how April and the second quarter started out….

Weekly Market Review

Monday: The first week of trading got off to a good start with all four major North American Indexes posting a gain for the day. In Canada, the TSX, was led upward by the Technology and Energy sectors. I cannot remember the last time I saw those two sectors lead the way on the TSX on the same day. Usually if one is up, the other is down.

In the US, the mega market cap tech stocks Apple (NASD:APPL), Microsoft (NASD:MSFT) and Tesla (NASD:TSLA) help propel the Nasdaq and the S&P higher, with the DJIA getting lifted by the general market updraft.

Tuesday: US Federal Reserve Governor Lael Brainard said it was “of paramount importance to get inflation down.” With that, fears of a more aggressive US Federal Reserve rate caused the markets in the US to decline, with the TSX getting caught in the downdraft. In Canada, the TSX temporarily reached an all time high before falling back. The Canadian Energy, Materials and Technology sectors weighed down on the TSX. In the US, the Nasdaq had its worst day in a month with declines in technology mega cap companies such as Apple and Microsoft.

Wednesday: Tuesday’s words from the US Federal Reserve continue to haunt the North American markets with all four Indexes declining for a second straight day. The Fed released the minutes from their March meeting showing strong support by Fed members for more aggressive rate hikes, including multiple .5% rate hikes to control surging inflation.

Meanwhile, in the markets, the defensive Utilities sectors performed the best in both countries. On the downside in Canada, the Canadian Technology and Financial sectors dropped the most, while in the US, the S&P’s Technology and Consumer Cyclicals sectors fell the most.

Thursday: Despite ongoing concerns about the Russian invasion and a more aggressive US Federal Reserve, the four Indexes climbed back into positive territory today thanks to a late afternoon rally. In Canada, the TSX was led by the Materials and Energy sectors. As well, the Canadian government released the latest federal budget after the cIose of the Canadian markets. In the US, Healthcare and Energy sector stocks led the way.

Friday: The last day of the week was a mixed bag with the TSX and DJIA inching above the bar into positive territory while the technology heavier S&P and Nasdaq ended below the bar. The TSX was lifted by the resource sectors (Energy and Materials) and the Financial sector. In times of inflation and rising interest rates, these sectors tend to outperform the other eight sectors. Together these three sectors account for 57% of companies in the TSX Composite so when they do well the TSX tends to follow along, as has been the case in 2022.

In the US, investors also tend to move into US banks stocks when interest rates move higher, which is what happened Friday. The big US banks are a bigger component of the DJIA than the S&P and the Nasdaq, which is a main reason the DJIA gained on the day while the S&P and Nasdaq declined.

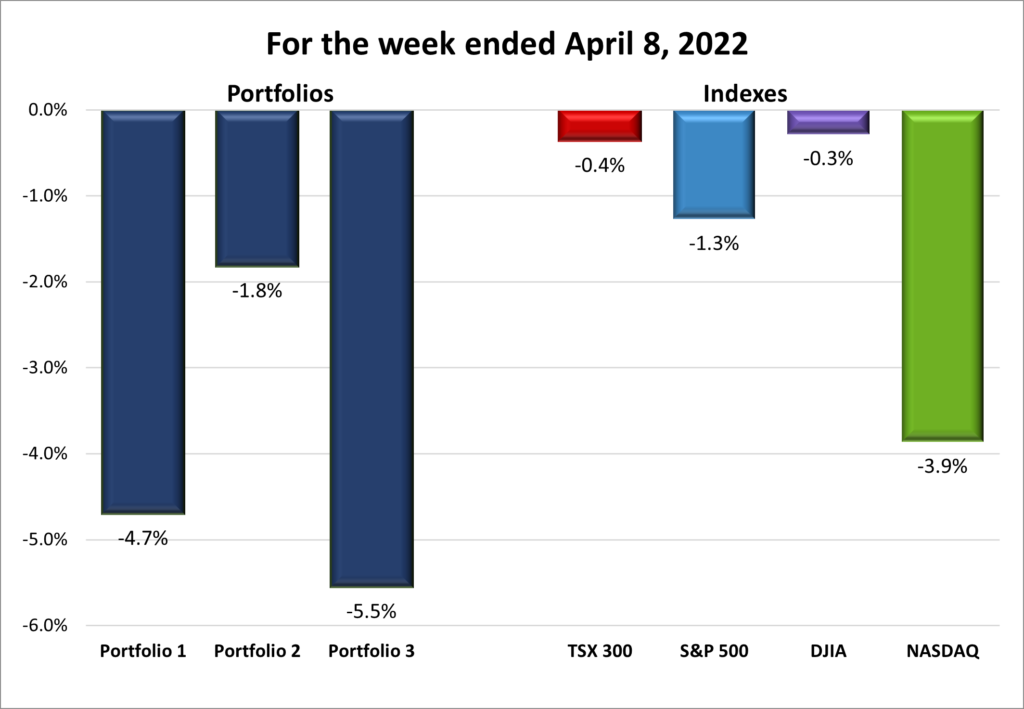

For the week, the TSX fell -.4%, the S&P dropped -1.16%, the DJIA declined -.28%, and the Nasdaq sank -3.86%. I am glad I am only following four Indexes as I am running out of ways to say declined. 😊

Where’s the weekly chart of the indexes ?

There will be no weekly chart for the Indexes. For the last few weeks, the change in the Indexes, as reported above, has not been reflected in the chart. This is very frustrating because the end of the week numbers used to calculate the change are easy to find by checking Yahoo Finance!, MSN Finance, Google Finance or your online trading account on a Friday after the extended market close (after 5:00 pm Pacific). After doing the math to compare these numbers to the previous Friday’s closing numbers, the calculations match the numbers provide by Refinitiv (formerly Thomson Reuters Finance). Even comparing the finance websites mentioned previously, the charts do not match. As I said, very frustrating. Once I figure out why the charts do not reflect the calculated changes in the Indexes, the weekly chart will re-appear.

Weekly Portfolio Review

With both the Bank of Canada and the US Federal Reserve indicating they are prepared to slow the economy to get inflation under control, this past week was not a good week all around. Higher interest rates are not good for technology companies or high growth companies that are using debt to fuel their growth (more money will be required to service the debt, therefore less money to grow the business). All the Indexes and all the Portfolios declined for the week. If April has historically been the best month for the American markets, it has gotten off on the wrong foot. Even the TSX which has done well throughout 2022 had an off week.

With all four Indexes falling for the week, its no surprise all the Portfolios are down. The technology heavy Portfolios 1 and 3 dropped over 4% and 5%, respectively, for the week, perhaps the worst single week since I have been writing this blog. By comparison, the more diversified Portfolio 2 dropped only 1.8%. I was not tracking the Portfolios during the high growth cycle of 2020 – 2021 so I do not know if Portfolios 1 and 3 significantly outperformed Portfolio 2, but I am interested to see how the Portfolios compare during a growth cycle. This current market pullback is not great for any of the Portfolios, but Portfolio 2 definitely seems to be holding up better in this current environment.

In the meantime, let us hope the markets revert to their historic norms and starting heading upward for the rest of April.

Weekly Portfolio & Index performance for the week ended Apr. 8, 2022.

Companies on the Radar

Not much happening on the radar front. For now, I am content to sit on the sidelines rather than churn the account for the sake of doing something. I would rather do nothing than pay transaction fees and possible taxes. However, the usual suspects remain at the top of my list:

Portfolio 1 for the week ended April 8, 2022: DOWN

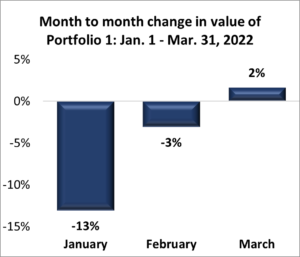

Month over month change in value.

The first quarter was not good for Portfolio 1, dropping 14.2%. The technology companies and other high growth companies in Portfolio 1 felt the sting of the higher interest rates and anticipated future higher interest rates. Many of the earnings reports for the companies in the portfolio were good but that did not seem to matter as investors fled to more conservative companies, bonds, or cash. I am satisfied with most of the companies and expect them resume their upward ways once the markets start climbing again.

In other news relevant to Portfolio 1 companies:

On a positive note, the investment in Berkshire Hathaway (NYSE:BRK.B) was one of the few companies that posted a gain this past week, although it is still a few dollars below the price I paid. Part of the reason I became an owner in Berkshire Hathaway was to gain exposure to a diverse mix of value-based stocks. When growth stocks are out of favour, as they currently are, it is great to own a company that has proven itself when value investing is the name of the game. No one does value investing better than Berkshire Hathaway.

Speaking of value investing, Berkshire Hathaway took out a USD $4.2 billion dollar position in HP Inc. (NYSE:HPQ), giving at an 11.4% interest in the company.

ZIM Integrated Shipping (NYSE:ZIM) paid out a whopping 117.6% dividend, or USD $17 per share, this past week. I doubt this will be a regular occurrence, but I would be pleased if it were. The only drawback is losing 25% of the dividend to the taxman. ☹

GM (NYSE:GM) and Honda (NYSE:HMC) will co develop lower priced electric vehicles in an attempt to beat Tesla’s sales numbers. This follows on existing plans for GM to build two electric SUVs for Honda beginning in 2024.

On Monday it was revealed that Elon Musk, CEO of Tesla, is the largest shareholder of Twitter (NASD:TWTR) with a 9.2% stake. On Tuesday, Twitter announced Musk had accepted a seat on their Board of Directors. Musk has filed a regulatory form indicating he intends to be an activist, rather than passive, investor. It will be interesting to see where this goes as Musk had previously tweeted about starting his own Twitter competitor.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Cargojet Inc. (TSX:CJT)

US $

ZIM Integrated Shipping (NYSE:ZIM)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended April 8, 2022: DOWN

Month over month change in value.

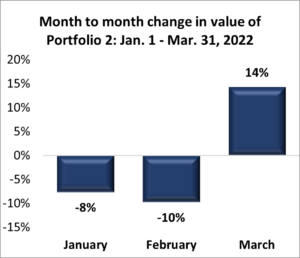

Portfolio 2 was the best of the three portfolios in the first quarter, only dropping 4.6%. You know it is a bad quarter when you describe your best performer as “only losing…”. Hope I do not have to use that phrase very often in the future. 😊 Portfolio 2’s fall was limited by its more conservative mix of companies and is therefore less volatile compared to the other two portfolios. The portfolio is more diversified and many of the companies in this portfolio are dependable dividend payers which also helped. With limited losses, this strategy seems to have paid off.

Elsewhere in Portfolio 2, Guardant Health (NASD:GH) announced a deal that will make its cancer tests available as part of routine medical care. Once setup, Doctors will be able to order Guardant’s tests and access those results directly from within patients’ records. Easier access to Guardant’s products and services should help boost Guardant’s revenue.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Alimentation Couche-Tard Inc (TSX:ATD)

Brookfield Renewable Partners LP (TSX:BEP.UN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended April 8, 2022: DOWN

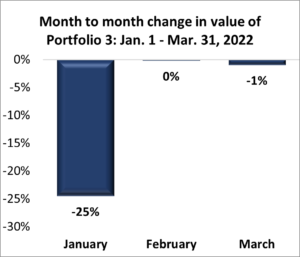

Month over month change in value.

The first quarter was terrible for Portfolio 3, dropping 25.3%. Ouch! Being technology and growth oriented didn’t help but with Shopify (TSX:SHOP) accounting for nearly 40% of the portfolio value, its no surprise Portfolio 3 fell this hard. Shopify has dropped over 50% since its all time high in 2021. Given how far Shopify has dropped, I am glad the damage to the Portfolio was not worse. Fortunately the financial stocks, Royal Bank (TSX:RY), TD (TSX:TD) and goeasy (TSX:GSY), were able to limit the loss. As with the other two portfolios, I am satisfied with companies in this portfolio and expect their respective share prices to start to follow the growth of the businesses.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Have you ever had one of those weeks where things just seem to go your way? The past week was one such week for me. I made three trades during the week, triggered by a busted thesis and a book. Let me explain.

Trade 1: I purchased shares in a Special Purpose Acquisition Company, Social Capital Hedosophia Holdings Corp VI (NYSE:IPOF.U), more commonly known as SPACs, in February 2021. A SPAC is basically a shell company created by an initial group of investors for the purpose of raising money through an Initial Purchase Offer (IPO) to buy another company. When you purchase shares in the SPAC the target company is not known but the SPAC must acquire a company within two years or return investors’ money. In a sense, I basically gambled that the management team of the SPAC would acquire a good company that would go on to do great things. The attraction of a SPAC is that retail investors, like me, can get in on an investment at a lower share price than if a company went public the traditional route. In 2020 and 2021, SPACs were the next greatest thing and I thought this would be a terrific opportunity.

As with all fads, this one fizzled out. There has been no news of a potential target company for over a year and the share price has only fallen since my investment in the SPAC. As well, for me anyway, the shine has worn off the CEO who seemed to have the Midas touch in 2020. Finally, I cannot recall any SPACs that have gone on to great heights, either the company or the share price. I decided I had a better chance to grow my money by cutting my losses and investing elsewhere while the market was down significantly.

Trade 2: In a serendipitous bit of luck, I was reading a book of Warren Buffet essays he had written over the years. Warren Buffet is the Chief Executive Officer of Berkshire Hathaway (NYSE:BRK.B) and is considered one of the greatest investors of all time. The more I read, the more I liked about him and his company. After looking closer at the company, I discovered it owns many of the top nontechnology, American companies (such as Kraft Heinz and GEICO) and has stakes in many other top American companies (such as Coca-Cola and Mastercard). I felt investing in Berkshire Hathaway would provide diversification (through all the companies it owns or has invested in), and act as a counterbalance to the more volatile technology companies in Portfolio 1 (something I identified during the current market decline and have been meaning to address). I decided being an owner (a tremendously small owner) of Berkshire Hathaway would be a terrific addition to Portfolio 1.

Trade 3: Several big technology companies have been on my radar for some time. I was interested in those companies because I felt they had good growth prospects and would be less volatile than other technology companies. However, after adding Berkshire Hathaway, I decided I could be more aggressive and focus on the two companies I added to my radar last week (add link): Marqeta (NASD:MQ) and Unity Software (NYSE:U). I decide to purchase additional shares in Unity because it already was a dominant player in the growing gaming industry, and it had a good chance of being a leading player in the growing virtual reality and augmented reality industry (think ‘metaverse’).

And there you have it. Three trades in one week, sparked by a broken thesis and the lucky coincidence of reading about one of the greatest investors of all time. For me, this many trades in one week is very unusual, but this time everything seemed to click. Sell a nonperformer to generate cash, happen upon a top company, and take advantage of depressed share prices. Even though I lost money when I sold the SPAC, I feel I have a much better chance of my investments growing with the two purchases I made this week.

It was a good week for me but let us see if it was another good week for the markets ….

Weekly Market Review

Monday: A good day for the American Indexes, the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq), with all three ending in positive territory. I cannot remember the last time all three ended a Monday in the black. While it was not a good day for the Toronto Stock Exchange Composite Index (TSX), it was not a bad either as the TSX ended the day barely in the red.

If the TSX is down and the US Indexes are up, there is a good chance Energy and Materials are down while Technology and Consumer cyclicals are up. Sure enough, that is the case today. In both countries the Energy sector was the worst performer as the price of oil fell on concerns of lower demand in China thanks to a lockdown in Shanghai after a covid-19 outbreak. Meanwhile, the Technology sector was among the top performers thanks to a surge in Tesla (NASD:TSLA) after the company announced it wanted to initiate a stock split.

Tuesday: Progress was made in talks between Russia and Ukraine, leading to lower oil prices which in turn calmed the inflation fears. All this good news led to a good day in the markets as all Indexes registered a gain, with the TSX setting a new high. Investors moved back into the high growth Technology and Consumer Cyclicals sectors. In Canada, Shopify (TSX:SHOP) was the main driver behind the TSX’s upward movement.

Wednesday: The day ended in the red for all four Indexes today. For the TSX, it was a very light shade of red as the TSX dropped .05%. Gains in the Energy and Materials sectors cushioned the blow from a drop in Technology sector stocks.

In the US, the S&P and the DJIA both snapped a four-day win streak after signs the Russians statements they made earlier this week about withdrawing troops is as sincere as statements they made earlier this year about not invading Ukraine. Investors are also concerned the US Federal Reserve will get more aggressive in attempting to tame rising inflation.

Thursday: For the second consecutive day all four Indexes declined. The price of oil fell on news the US initiated their largest ever release of oil from their emergency oil reserve. As a result of lower oil prices, the Canadian Energy sector dropped. Elsewhere on the TSX, concerns about the ongoing Russian invasion of Ukraine caused all sectors but the defensive sectors (Telecommunications, Utilities and Consumer Staples) to fall.

South of the border, concerns over the Russian invasion and its inflationary effect on already high inflation numbers caused a broad-based pullback with all 11 S&P sectors declining. The price of oil could jump again on Russian threats to freeze contracts for oil supplies to Europe unless the contracts are paid in rubles. So far European countries have resisted but it may not be as easy once the oil tap is turned off and fuel prices start to soar.

Friday: The second quarter of 2022 got off on the right foot with all four Indexes back in black at the end of the day. Despite finishing the day in the black, the TSX end the week in the red after five consecutive winning weeks. Canada’s resource companies have benefited from the embargo of Russian commodities such as energy, mining, and fertilizer companies.

In the US, a strong jobs report pushed the Indexes higher but also led to expectations of a more aggressive interest rate increase at the next meeting of the US Federal Reserve in May.

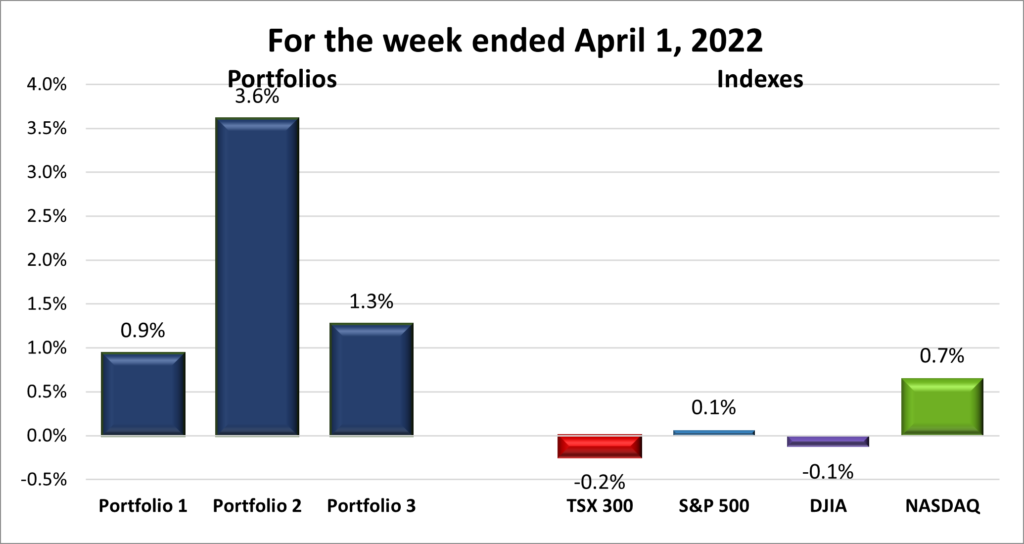

For the week, the TSX was down .2%, the S&P rose .1%, the DJIA: dell .1% and the NASD gained .7%

After falling for the first two months of the year, US stocks joined their Canadian cousin in the win column for the first time this year. For March, the TSX gained 3.6% (its ninth consecutive month of gains), the S&P gained 3.6%, the DJIA rose 2.3% and the Nasdaq climbed 3.4%. Historically, April has been a good month for the American markets and has the been the best month on average since 1950. Let us hope that continues in 2022.

It was a good start to 2022 for the TSX with an increase of 3.1% for the first quarter. However, the story wasn’t so good in the US. Considering all that was going on in the first quarter of 2022 – inflation, war, supply chain challenges, and a 2 year pandemic – it is no surprise all three American Indexes suffered their first losing quarter in two years. For the quarter, the S&P fell 4.9%, the DJIA declined 4.6% and the Nasdaq is dropped 9.1%.

Weekly Portfolio Review

The past week was essentially a flat week for the Indexes, with three of the Indexes just over or just under the breakeven bar. The exception was the Nasdaq which handily outperformed the other Indexes. It was not big week for the Nasdaq with a .7% increase but compared to the second place S&P at .1% growth, it looks much better. Its nice to see the Nasdaq lead the pack in upward movement after leading the pack in downward movement for most of 2022.

As for the Portfolios, not only did all three post gains for the week but they also beat the last week’s top performing Index. With the Nasdaq the best performing Index I did not expect to see Portfolio 2 leading the way this past week. Portfolio 1 had an OK week and Portfolio 3 performed slightly better. Always good to see all three Portfolios beat the best performing Index. 😊

Weekly Portfolio & Index performance for the week ended Apr. 1, 2022.

Companies on the Radar

With the purchase of Berkshire Hathaway shares and additional Unity Software shares, there is not much cash readily available. I would have to sell shares in another company to raise cash. For now, I will be sitting on the sidelines, but the usual suspects remain at the top of my list:

After expanding into India in October 2021, Shopee, the e-commerce arm of Sea Limited (NYSE:SE), is shutting down its Indian operation after India banned Sea’s gaming app ‘Free Fire.’ This follows Shopee’s decision in late February to exit France. With retreats from France and now India, so much for expanding outside of its southeast Asia base. Hopefully, they will have more success in Latin America.

Cargojet (TSX:CJT) announced a 5-year deal to provide air transportation services for DHL, with the possibility it could be renewed for an additional 2 years. Part of the deal allows DHL to purchase up to a 9.5% position in Cargojet. Business has soared for Cargojet (pun intended) thanks to the increasing demand to fulfill shipping requirements caused by rise in e-commerce brought on by the pandemic.

Boston Omaha (NYSE:BOC) reported their 2021 earnings this past week. They could take a lesson from CEO Alex Rozek’s uncle Warren Buffet about annual report presentations. Boston Omaha’s annual report is a bare 10-K report with few if any insights.

General Motors (NYSE:GM) said it was increasing production of its new electric Hummer trucks and SUVs to meet demand, due to reservations being higher than initial expectations. A good problem to have. 😊

Activity

Sold: Social Capital Hedosophia Holdings Corp VI. This stock was purchased in February 2021 for two reasons: the momentum of Special Purpose Acquisition Company, more commonly known as SPACs; the success of Chamath Palihapitiya, the Chairman of the Board, bringing other SPACs to market.

Fast forward a year, a SPAC has 24 months to bring a company public and I have heard nothing about prospective private companies that the SPAC might purchase. If they have not acquired a company, they must return the money or get an extension to bring a company public. I felt if the SPAC ran out of time to acquire a target company, they might settle for a lesser company just to avoid returning investors money.

Based on the drop in the number of SPAC deals in 2022, it appears SPACs were more of a fad than anything else. SPACs historically numbered in the low double digits up until 2020, when they quadrupled, and are on pace to fall back into the double digits in 2022. Reason number one busted.

With no news of potential acquisition targets, I started to lose confidence in Mr. Palihapitiya. He sold shares in his first SPAC, Virgin Galactic (NYSE:SPCE), in the second half of 2020. Then he stepped down as Chairman of Virgin Galactic earlier this year, 2 years after he brought it public. While this was a different SPAC than the one I invested in, for me, this indicated he was not in it for the long run as he had indicated. Reason number two busted.

This SPAC could still do well, but I felt the money could be put to better use elsewhere.

Lessonlearned: Be aware of a rush into new fads and pay attention to the motivations of those pushing the fad.

Note: I bought shares in Virgin Galactic in May 2020 and sold in March 2021 when founder Richard Branson and Chairman of the Board Mr. Palihapitiya sold their shares. I do not take it as a positive sign when the leaders sell their shares. As it was, I did OK on the transaction.

Bought: Berkshire Hathaway Inc. I have heard many people sing the praises of Berkshire Hathaway and its Chairman Warren Buffet and Vice President Charlie Munger. I finally got around to reading a book comprised of excerpts from many of his letters to shareholders – The Essays of Warren Buffett – and came away extremely impressed by him and how he managed Berkshire Hathaway. Reading their latest Annual Report, I saw the many companies Berkshire either owned or had invested in over the years. They were top American companies across a number of sectors.

Over the last few months, I have been concerned about the heavy technology and growth stock bias of this portfolio. I had been looking at nontechnology companies to lower the volatility and risk. I even considered an Index fund. I was impressed by Berkshire Hathaway’s performance over 55 years:

compounded annual gain of 20% compared to the S&P 500’s 10%,

an overall gain of 3,641,613% compared to the S&P 500’s 30,209%.

After seeing the companies Berkshire Hathaway owned or invested in, I felt this would be a great way to diversify the portfolio with one of the best companies in the world. I expect Berkshire Hathaway to continue to grow well into the future.

Bought: Unity Software. Of the growth stocks across all three portfolios, I felt this had as good a chance as any of the other growth companies, including the big-name companies on my radar. However, it seems to have tremendous upside in virtual reality/augmented reality market. It is a leader in the gaming industry and is making inroads with architects, manufacturers, engineers, automotive designers, and the film industry. I accept that the share price will be volatile as the company grows but I am confident it will continue to grow revenue and earnings, and the share price will follow those upward.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Record quarterly revenues of $115.7 million representing a 573% year-over-year (YoY) increase compared to the same period in the previous year

Delivered 700,359 total omni-channel patient visits in Q4-2021, representing a YoY increase of 123%. When combined with our asynchronous visits, the total number of visits was 972,740.

Net income of $707,000 compared to net income of $5,772,000 in the same period in 2020.

2021 full year highlights

Annual revenue for 2021 was $302.3 million, an increase of 502% compared to the prior year.

Net loss of $30,895,000 compared to a net loss of $3,247,000 in 2020.

Anticipate revenues more than half a billion in 2022.

Revenue for the fourth quarter of 2021 was $1.3M, compared to none for the same period in 2020.

Net loss of $22.0 million, compared to a net loss of $19.0 million for the three-month period ended December 31, 2020, largely due to expenses related to a merger and acquisitions.

2021 full year highlights

Revenue of $1.3M, compared to none in 2020.

Net loss of $61,798,000 compared to a net loss of $43,815,00 in 2020.

Recorded net revenues of $83.8 million in 2021, an increase of 79% compared to 2020.

Net loss of $33,754,000 compared to $87,431,000 in 2020.

Portfolio 2

Portfolio 2 for the week ended April 1, 2022: UP

The Bank of Nova Scotia (TSX:BNS), Canada’s third-largest bank, increased its stock-buyback program to 36 million shares, approximately three per cent of its outstanding shares as of November 2021. This is good for me and other shareholders as it increases our respective share of the earnings.

Kneat.com (TSX:KSI) shares commenced trading on the US OTCQX under the ticker FBAYF. The OTCQX is the premier tier of the US over the counter (OTC) marketplace. This US listing will increase Kneat’s profile among US investors and make it easier for them to invest in Kneat. While it is easy for Canadians to invest in the US stock markets, it is not as simple for Americans to invest in companies solely listed on Canadian stock exchanges. Hopefully Kneat will continue to grow earnings and American investors will start investing in the company, driving the share price higher.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Following up on a previous Microsoft news item, the European Union antitrust chief announced Microsoft, Amazon and Alphabet/Google does not raise competition concerns, at this time.

The Royal Bank of Canada (RBC) (TSX:RY) made a cash offer of 1.6 billion pounds for British wealth manager Brewin Dolphin. This acquisition would make RBC, Canada’s largest bank, the third largest wealth management company in Britain and Ireland.

Ethereum is up to CAD $4,307 as of early evening April 1. That is better than it was in late January but still far from my purchase price of over $6,100 in November 2020. So much for getting rich quick on cryptocurrency. ☹

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Do you like rollercoasters? If you do, the markets went on a bit of a ride this past week. The Indexes were up and down throughout the week. Do you ever wonder what causes the markets to move like this? Investor sentiment for sure but let us look at the culprits that moved the market this past week.

There are two main items pushing and pulling the markets: inflation is the big concern, but the Russian invasion of Ukraine has been like fuel to the inflation fire. Inflation in both Canada and the USA has been haunting the markets for the last few months. The monetary policies in both countries left people with a fair amount of money. When the pandemic induced restrictions started to ease, people had pent up demand to do the things that they were unable to do for over a year. As well, with production and manufacturing capacities down due to the pandemic, companies were short staffed and unable to meet the surging demand, both for other companies further down the supply chain, and for the end consumers. Essentially, the perfect storm developed:

Lots of money

Surging demand

Inability to meet the demand due to labour and supply chain issues

As of February, the inflation rate in Canada was 5.7% and, in the US, it was 7.9%. With inflation running well above the target of 2% – 3%, the Bank of Canada (BoC) and the US Federal Reserve (Fed) increased their respective interest rates by .25% to .5%. However, analysts in both countries are hinting more aggressive increases are required. The BoC has said it will act “forcefully” to return inflation to the 2% – 3% range, and the Fed has started talking about a .5% interest rate hike at their next meeting in May.

While the Russian invasion has had a terrible impact on Ukrainians, it has also been felt around the world in the form of rising prices (also known as inflation) for almost everything. The price of oil has surged on supply fears as Russia is one of the top global suppliers of oil. Every time I put gas in my car, I feel inflation at work. Both Canada and the US have pledged to increase output to supply oil and natural gas to Europe to ease the dependence on Russian energy products and help lower sky-high energy costs, but that will take a while to kick in.

Along with being a top supplier of oil, Russia and Ukraine are also leading global suppliers of wheat. However, you can expect those sources of wheat to dry up, especially in the case of Ukraine. More concerning, Russia and its ally Belarus provide over 40% of global exports of potash, a key ingredient of fertilizer. The loss of fertilizer products will lead to higher prices in almost all food products as producers pass along the higher costs to consumers. As well, if the cost of fertilizer gets too high, producers will not be able to afford enough fertilizer required for their crops. This in turn will lead to lower supplies to meet the demand. In the case of food products, we will get a double dip of inflation with higher fertilizer to produce the crops and higher fuel costs to get the produce to market.

The next time you go grocery shopping, note the prices of the products you buy. It may take a month or so for the higher costs to kick in so keep your receipts and compare them to your latest receipt each time you go grocery shopping. That is inflation in action and a knock-on effect of the Russian invasion of Ukraine.

Inflation is not good for businesses as it increases costs which are passed down the line to the eventual consumer. Talk of inflation makes investors skittish due to fear of higher interest rates. Its these rumours that cause the stock market to act like a rollercoaster.

Let us see if the Indexes and portfolios enjoyed the rollercoaster ride this past week….

Weekly Market Review

The impressive performance by the S&P 500 Index (S&P) last week cut its loss for the year to date in half. On March 14, the S&P was down 11.8%, today the S&P starts at -5.6%. I hope that trend continues.

Monday: News the European Union is considering a Russian oil embargo sent the Toronto Stock Exchange Composite Index (TSX) up for the fifth straight session thanks to gains in Energy (oil) and Materials (mining and fertilizers) stocks.

In the US, the Energy and Materials sectors were up, however, after the US Federal Reserve suggested a .5%, or 50 basis point, raise in interest rates might happen sooner rather than later caused the S&P, the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) break their 4 day winning streaks.

Tuesday: The four major North American markets each finished in the green (or is it black) today. In both countries, the respective Technology and Consumer Cyclical sectors led the advance. The Financial sectors in both countries also had a good day as bank revenues are likely to increase now that interest rates have gone up and further hikes are anticipated. The TSX closed at another record high, while all the sectors S&P ended higher, except for the Energy sector which dropped when the European Union pulled back from talks about a Russian oil embargo.

The Nasdaq rose 2% on the strength of a few of its biggest growth companies such as Apple (NASD:AAPL), Alphabet (NASD:GOOGL), Microsoft (NASD:MSFT) and Tesla (NASD:TSLA). In Canada, Shopify (TSX:SHOP) had a good day dragging the Canadian Technology sector higher.

Wednesday: The TSX had its first decline in almost two weeks despite gains in the Energy and Materials sectors which had had been the main catalysts for the TSX’s string of positive days. Despite the a down day for the TSX, it was still better than the three American Indexes today which each fell more than 1%. In Canada and the US, the respective Technology and Financials sectors were the worst performers on the day.

The heads of Western countries will meet in Brussels later Thursday to discuss additional sanctions against Russia for its invasion of Ukraine. Other than an oil embargo I do not know what other economic measures are available. As well, Russia announced it planned to sell natural gas in roubles to ‘unfriendly’ countries. Disruptions in shipments of Kazakhstan and Russian oil further tightened an already tight supply of oil, causing a spike in oil prices. The disruption was a result of a major storm at a terminal on the coast of the Black Sea.

Thursday: The stock market continued its up and down like a yoyo routine. The Indexes fell on Wednesday and rebounded today to each close the day in positive territory. In Canada, the Healthcare sector rose on news the US government is preparing to vote to legalize marijuana at the federal level. The Canadian Energy sector was a drag on the TSX as the price of oil fell 2.25%.

In the US, today’s rally was led by the Technology sector, especially the semiconductor industry. The Basic Materials (mining and fertilizers) and Healthcare sectors round out the top three US sectors for the day.

Friday: The TSX started a new winning streak ending higher for the second consecutive day. Once again rising oil prices propelled energy stocks higher, overcoming the drag of the technology sector. The TSX recorded it fifth straight week of gains.

In the US, both the S&P and DJIA finished higher while Nasdaq was unable to crawl out of the hole it dug itself earlier in the day. The Energy sector, riding the coattails of higher oil prices, led the way upward. The Financial sector, benefiting from higher interest rates, and, surprisingly, the Utilities sector helped boost the S&P and DJIA. Utilities are typically considered defensive stocks because of their low growth rates and dependable dividends. Not sure what would cause investors to move into Utilities other than the ongoing war in Ukraine. Finally, if the Nasdaq ends the day down you know it was not a great day for the Technology sector. Technology stocks were down on concerns of more aggressive interest rate hikes by the US Federal Reserve.

Weekly Portfolio Review

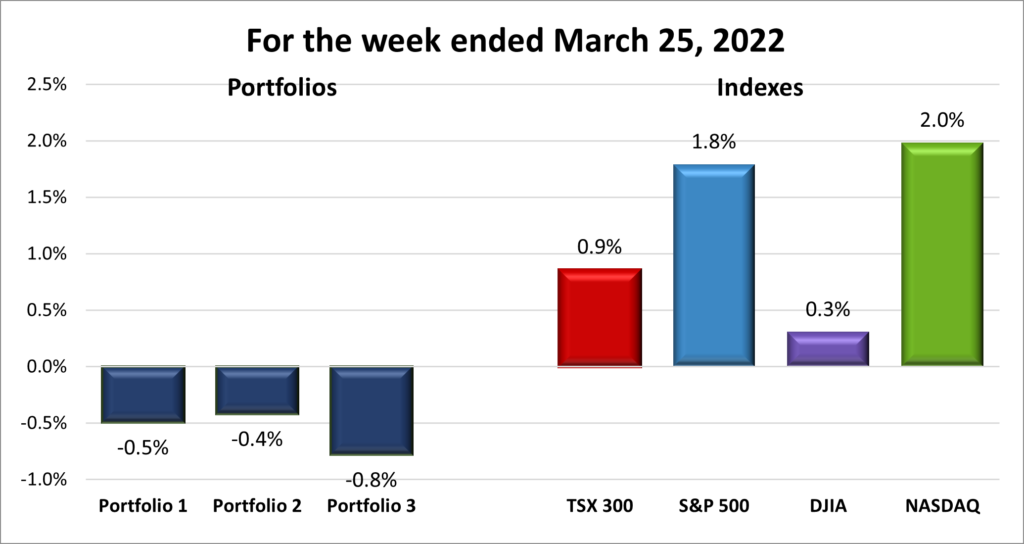

All four Indexes ended the week in the black, led for the second week in a row by the Nasdaq. As seen in the chart above, the three American Indexes seemed to follow a similar yo-yo pattern while the TSX was more like a rolling wave with smoother ups and downs.

I was hoping the Portfolios would have another great week like last week, but it was not to be. Going into Friday all three Portfolios were in the black but a decline in the Technology sector on Friday caused all three Portfolios to fall into the red. ☹ This week was one of the few times when all four Indexes, led by the Nasdaq, advanced for the week while all three Portfolios declined. Usually, the Portfolios ride the coattails of the Nasdaq. Even though each portfolio was down it was not by much and its much less stressful looking at the Portfolios now than it was several weeks ago, when they were constantly falling. That being said, I would rather they just be in the black than just a little in the red. Hopefully that will be the case next week.

Weekly Portfolio & Index performance for the week ended Mar. 25, 2022.

Companies on the Radar

With limited cash, I’ve removed Amazon (NASD:AMZN) from my radar. I would lose approximately CAD$ 800 to foreign exchange and I can think of better ways to spend that money, such as another investment in the Energy sector, either another investment in International Petroleum (TSX:IPCO) or Transocean (NYSE:RIG). I am also thinking about adding to shares in Marqeta (NASD:MQ) or Unity Software (NYSE:U). Still on the radar are:

Portfolio 1 for the week ended March 28, 2022: DOWN

Despite ongoing supply chain issues plaguing the automotive industry, GM (NYSE:GM) announced plans to accelerate the rollout of its Cadillac electric vehicle.

Nvidia announced several new chips and technologies that will boost the speed of chips used in artificial intelligence (AI), and data centres (used by customers such as Alphabet and Microsoft). They estimated the total addressable market for gaming, AI, the metaverse, and automotive applications will grow to $1 trillion over the next decade. Hence Nvidia is on my radar.

Nvidia is also talking with Intel (NASD:INTC) about Intel producing Nvidia’s chips. Sounds like a win for both parties. Nvidia gets another supplier of its in-demand semiconductors and Intel gets business for its new factories.

Apple is acquiring British financial technology company Credit Kudos for USD $150 million. As part of a trend known as ‘open banking,’ Credit Kudos develops software to provide better and faster credit checks on consumer loan applications using the consumer’s own banking information. From here, I am not sure how this acquisition fits with other Apple financial services Apple Pay and Apple Card. Perhaps Apple is looking to setup its own financial eco system to help consumers finance the rumoured Apple car. 😊

Rogers Communications (TSX:RCI.B) proposed acquisition of Shaw Communications (TSX:SJR.B) passed its first hurdle with the conditional approval of Canada’s telecommunications regulator.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Revenue increased 33% YoY to $21.8 million, driven by the increase in new clients and the expansion of existing clients.

Gross profit of $17.3 million, a 29% increase from $13.4 million in Q4 2020, representing a Gross Margin of 79%.

Strong balance sheet with cash and cash equivalents of $161.4 million as of December 31, 2021, compared to $15.9 million on December 31, 2020.

Full Year 2021 highlights

Record revenue of $69.3 million, an increase of 56% over the prior year.

Annual Recurring Revenue grows 39% YoY to $36.8 million and Net Revenue Retention Rate was 116%.

Gross profit of $54.9 million, a 69% increase from $32.4 million in the prior year, representing a Gross Margin of 79% as compared to a Gross Margin of 73% as of December 31, 2020. The growth reflects an increase in revenue, successful remote delivery resulting in less travel, as well as an improvement in utilization.

Net loss of $6.5 million, compared to net loss of $9.1 million in the prior year

Portfolio 2

Portfolio 2 for the week ended March 28, 2022: DOWN

The governing Liberal Party of Canada reached an agreement with the New Democratic Party that should keep the Liberals in power until 2025. Political thoughts aside, the government is now likely to impose some form of tax on bank profits greater than CAD $1 billion. Since banks never lose money (IMHO), this means that tax will be passed on to us consumers in some form of a fee hike. It also sets a bad precedent for future taxes on profits in any industry. ☹☹

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX:DIR.UN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended March 28, 2022: DOWN

Hackers claimed to access Cloudflare (NYSE:NET) systems and reset a few employee passwords. Cloudflare announced there was no evidence its systems were compromised, but nevertheless was resetting employee login credentials as a precaution. Later this week police in London, England arrested the suspected hackers. It is believed these same people had previously hacked Nvidia, Microsoft and Okta.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

It was an ominous start to the week when the Nasdaq 100 Index closed in bear market territory (down more than 20% from its peak in November). It was the first time in three years that any of the US Indexes had fallen into a bear market. Heck, even the Dow Jones Industrial Average (DJIA) and the S&P 500 Index (S&P) have been in ‘corrections’ (down 10% – 20%) this year. It seems all my portfolios are sinking lower each week.

The Toronto Stock Exchange Composite Index (TSX) is the only Index up in 2022 thanks to its heavy weighting in financial and resource companies. The Canadian Financials sector (banks and other money lenders which tend to benefit from higher interest rates), accounts for nearly 30% of the TSX. The resource companies listed on the TSX in the Energy and Basic Materials sectors benefit from higher commodity prices and accounts for over 25% of the TSX’s weighting. Together these three sectors make up over 50% of the TSX.

Unlike the TSX, the S&P sectors are much more heavily weighted towards Technology at nearly 30% (on the TSX, the Canadian Technology sector accounts for almost 10%). The Financials, Energy and Basic materials sectors together make up 17% of the S&P Index.

(In the US, most people refer to the S&P sectors rather than the DJIA or Nasdaq sectors because the S&P represents more of a cross section of all of the US exchange listed companies. In the DJIA there are only 30 companies while the Nasdaq has more than 55% of its weighting in the Technology sector and an additional 20% weighting in Consumer Cyclical.)

The current environment caused by inflation and war in Ukraine (pushing inflation even higher) is almost the perfect storm for the TSX. The fight against inflation is likely to last for the rest of 2022. Who knows how long the Russian invasion will last but its impact on the economy will last much longer than the war itself. It should be a good year for the TSX but its too early to tell if it will outperform any of the US Indexes this year as the US indexes seemed to find their footing this week.

The US Federal Reserve removed the uncertainty of a possible rate hike to fight inflation and announced a .25% rate increase, with additional increases to follow throughout the year. Investors were relieved to put fears of a more aggressive increase behind them and jumped back into the stock markets, most notably the Technology sector (where I like to invest). I know I’ve been waiting for the market to bottom out and I suspect there are a lot of other investors in the same boat. Hopefully this is the bottom we’ve been waiting for, and the US Indexes will get back and surpass their November 2021 highs. In a perfect world, the TSX continues its winning ways and the US Indexes rebound strongly but we probably haven’t seen the last of Covid-19 and who knows what else lies ahead in 2022.

For now, lets see what happened in the markets this past week….

Weekly Market Review

Monday: Energy stocks, especially oil companies, and the Materials sector fell today, causing the Toronto Stock Exchange Composite Index (TSX) to drop. Energy and Materials had been nudging the TSX higher the last few weeks so the pullback in these sectors led to a drop for the TSX. The Canadian technology sector also weighed down the TSX.

In the US, lower oil prices and the expected interest rate hike by the Federal Reserve weighed on investors’ minds. The Dow Jones Industrial Average (DJIA) was the only Index to finish the day in positive territory. The S&P 500 Index (S&P) and the Nasdaq Composite Index (Nasdaq) were dragged down by the negative impact of higher interest rates on the Technology sector and Consumer Discretionary sectors.

Tuesday: Investors must be feeling confident ahead of the US Federal Reserve interest rate hike announcement as all four major North American Indexes finished in the black today. The TSX rebounded from a sharp drop at the start of the day to eke over the bar by the end of the trading day. In the US, a weaker than anticipated Producers Price Index caused investors to think the Federal Reserve will limit the interest rate hike to .25%, or 25 basis points. The only thing now is to wait for Wednesday’s announcement. If the interest rate increase is higher, I expect the market to drop. If it is .25%, as is now fully anticipated, or lower I expect a nice back in black moment for the stock market.

On both sides of the border, Technology and Consumer Cyclical sectors led the charge upward while the Energy sector retreated (thanks to oil falling below USD $100 a barrel).

Wednesday: As expected, the US Federal Reserve announced an interest rate hike of .25%, the first rate hike in three years and indicated there will be additional hikes throughout the year. More good news for the day was another round of peace talks between Ukraine and Russia. All this good news caused all four Indexes to each finish the day in positive terror.

In Canada and the US, the Indexes were lifted by strong gains in their respective Technology and Consumer Cyclical sectors.

The only downer for the day was the annual inflation rate in Canada rose in February to hit a 30-year high of 5.7%, hinting at additional interest rate increases in Canada.

Thursday: All four Indexes finished in the black for the third consecutive day, with the TSX hitting a record close. Given all the mayhem in the markets since the start of the year I was surprised to discover the TSX had a record close today.

The interest hike is now in the rear-view mirror, combined with ongoing peace talks between Russia and Ukraine, the two issues that have been haunting the markets lately may have been put to rest for the time being. With three straight days of gains, investors appear to have turned the corner from pessimistic to cautiously optimistic as they hunt for bargains amongst the many beaten down stocks.

Oil ended the day over USD $100 a barrel, pushing the Energy sectors in both countries higher. In Canada, the top performing sectors were Technology, Materials and Energy, while in the US the top performers were the Energy, Basic Materials, and Healthcare sectors.

Friday: For the fourth time this week all four Indexes closed the day in in positive territory. The TSX finished the day at another record high, led by the Technology, Consumer Cyclical, and Industrials sectors.

In the US, it was another broad-based rally, with the Technology, Consumer Cyclical, and Healthcare sectors leading the way. Not only did this week’s rally push the returns for March into the black but it was also the best week for the three Indexes since November 2020.

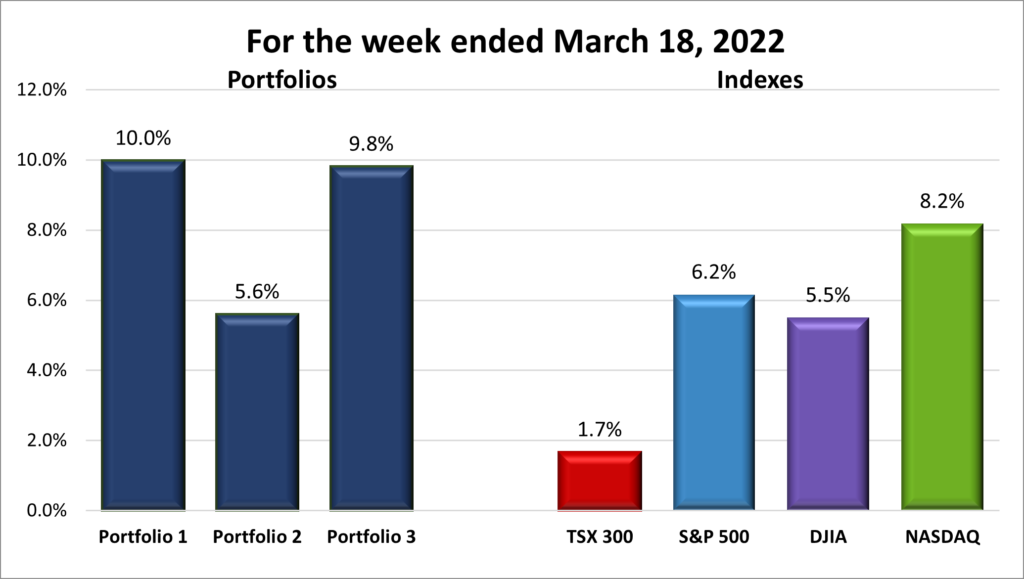

Weekly Portfolio Review

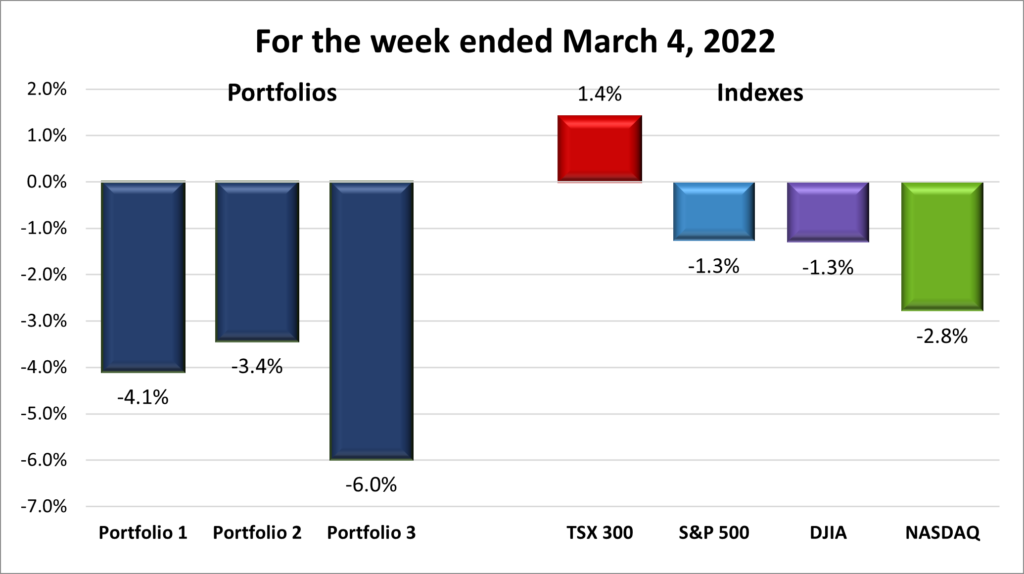

Its nice to see all the Indexes up, especially the technology heavy Nasdaq Index because when it does well, the Portfolios do well. And that was the case again this week as the Portfolios had an outstanding week. Portfolio 1 had a double-digit gain of 10%, Portfolio 3 almost hit double digits coming in at 9.8%, and Portfolio 2 had a respectable 5.6% gain for the week. While Portfolio 2 trailed the other two Portfolios, I would be very happy if each Portfolio went up 5.6% every week for the rest of the year. 😊

Unfortunately, weeks like this haven’t happened enough in 2022. And it will take many more similar weeks before the Portfolios get back to their November highs. Nonetheless, after a bleak start for the markets in 2022 I’ll celebrate this week but won’t get fooled into thinking the rollercoaster ride is over. But I do hope the investing gods will provide more weeks like this.

Weekly Portfolio & Index performance for the week ended Mar. 18, 2022.

Companies on the Radar

With the stock market continuing its month long decline I haven’t been following the market as closely as in previous weeks. Now that the market has picked up, it may be time to start looking for bargains. For now, the same companies from last week remain on my radar:

I was very pleased to see for the last four days this week that all companies that appeared in the daily Top Movers section of this TD Direct Investing account were going up. For the past few weeks, the Top Movers always seemed to be headed down. The technology companies that had been causing Portfolio 1 to drift downward the last three months finally had good week, lifting it 10% for the week (and Monday was a down day).

In other news…

General Motors (NYSE:GM) announced it will increase its stake in its self-driving car subsidiary Cruise to 80% by acquiring SoftBank Vision Fund’s equity stake. GM plans to spin off Cruise with an IPO some time in the future.

One of Portfolio 1’s best performing companies, Innovative Industrial properties (NASD:IIPR) announced a quarterly dividend of USD $1.75 per share, an increase of 17%. The company has done very well the last few years and the share price has gone up nearly 5X since the initial purchase in 2018. The decent and increasing dividend is a nice bonus on top of the high growth.

Sea Limited (NYSE:SE) jumped 30% this past week when China announced it would end its crackdown on local technology companies. Sea is a Singapore based company, not a Chinese company so I was wondering why its share price was so beaten down. I guess it got caught in a regional downdraft. Glad to see it also rode the updraft. I am still very reluctant to invest in China, or other autocratic nations where financial reporting is less transparent and government policies can change on a whim.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Automotive Properties Real Estate Investment Trust (TSX:APR.UN) DRIP

Yellow Pages Ltd (TSX:Y)

US $

BSR Real Estate Investment Trust (TSX:HOM.U)

Skyworks Solutions Inc (NASD:SWKS)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended March 18, 2022: UP

MongoDB (NASD:MDB) gained nearly 33% this past week to boost Portfolio 2 higher. Otherwise, it was a mixed bag for this Portfolio with only 60% of the stocks finishing the week in the black. This would be the downside to a ‘balanced’ portfolio – it doesn’t go up as much as the other more aggressive Portfolios. However, so far in 2022 it is the best performing of the three Portfolios. Nothing to complain about. 😊

MongoDB announced an expanded partnership with Amazon’s Amazon Web Services (AWS) division. The six-year deal is aimed to advance cloud adoption of MongoDB’s products on AWS.

Microsoft and Rogers Communications (TSX:RCI.B) signed a five-year deal to help companies with their digital transformation. Together they will assist companies upgrade and replace their existing landline and existing voice services with 5G enabled mobile solutions from Microsoft.

Guardant health (NASD:GH) received regulatory approval in Japan for their liquid biopsy test – Guardant360® CDx. This test helps identify patients with advanced cancer who may benefit from specific advanced treatments.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

iA Financial Corporation Inc (TSX:IAG)

Summit Industrial Income REIT (TSX:SMU.UN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended March 18, 2022: UP

Finally, a good week for Portfolio 3, up almost 10% this past week. Shopify (TSX:SHOP), Microsoft and Cloudflare (NYSE:NET) led the way but all the companies were up except for the two Brookfield Renewable Energy stocks (TSX:BEP.UN & TSX:BEPC). A solid week all around.

Microsoft is once again being sued, this time in Europe. An antitrust complaint was filed by three European competitors alleging Microsoft is undermining competition in the lucrative cloud computing business. I’ve no idea how this will turn out, but similar lawsuits do not seem to have hampered Microsoft in the past.

A bit of good news in Europe for Microsoft. Heat waste from Microsoft’s two new data centres in Finland will be recycled to heat homes and businesses in the Helsinki area. The switch from fossil fuel sources to recycled heat will also cut carbon emissions.

Kneat.com (TSX:KSI) announced it had signed an agreement for its laboratory equipment validation lifecycle management solution with a European country’s national health service. Kneat.com did not name the country or provide any details of the agreement.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

The week got off to a great start …. if you’re heavily invested in oil and energy companies as oil jumped to USD $130 a barrel. Sadly, I am not ☹, so it was another in a trend of blue Mondays. The markets went on a bit of a rollercoaster ride for the rest of the week. At the start of the week the Dow Jones Industrial Average was the last of the three major American Indexes to enter correction territory (a drop of 10% – 20%). Wednesday was a bright spot for us technology investors, but the rally was short lived as the Technology sectors in Canada and the US resumed their respective declines on Thursday and Friday.

While I am not heavily invested in oil, I have invested in a few oil and energy companies but not enough to offset the declines in the high growth sectors like Technology and Consumer Cyclicals (nonessential products people want rather than need) that I tend to favour. I hate to think what the losses would be like without these oil stocks and other defensive stocks like Utility companies and Real Estate Investment Trusts that have continuously paid dividends and distributions, respectively, throughout this market correction.

Throughout this market downturn I have been constantly reminding myself that with my investment philosophy and the way I have built the three Portfolios, the inevitable market downturns will be uncomfortable, but not forever. Since I do not need any cash in the immediate future, I can ride out this storm either by doing nothing or buying shares of my best companies while they are on sale. One of the few advantages I have as an individual investor is I can play the long game and not worry about short term share price fluctuations or try to meet short term targets. I have always believed you should play to your strengths, so I intend to make the most of this advantage.

Since I have developed my investment philosophy and strategy, I find I do not worry about market declines (that much). I have no control over what the stock market does or when it does it. My strategy helps me stay focused when the inevitable market downturns occur. When a decline occurs, rather than stress about it (ok, maybe a bit of stress), I look at it as an opportunity to purchase good companies while they are on sale. I know, easier said then done, but consider the sudden market crash in 2020 at the start of the pandemic. It felt awful. But once I got my head around the fact that there was nothing I could do but lock in losses, I started to see opportunities everywhere. I was fortunate to have cash in one of the Portfolios and I took advantage of the sale.

This 2022 market correction is not nearly as much fun because the decline is painfully slower than in 2020, the recovery is taking longer to kick in and I do not have much cash available to take advantage of these sale prices. This time, I am doing nothing but that does not mean I am not looking. 😊

Now, lets take a closer look at what happened in the market this past week and how it impacted the Portfolios (hint: the blue Monday led to a week of red). ☹

Weekly Market Review

Monday: Another rough day in the stock market as oil spiked to USD$ 130.50 a barrel, its highest price since 2008. On Canada’s Toronto Stock Exchange (TSX), higher oil prices led to higher share prices for Energy sector stocks which minimized today’s broader decline. The Utilities, Materials, Consumer Defensive were the other sectors to finish with more than a 1% gain today, not enough to compensate for larger losses in the Consumer Cyclical, Technology and Financials sectors.

In the US, the S&P 500 Index (S&P), Nasdaq Composite Index (Nasdaq) and the Dow Jones Industrial Average (DJIA) all fell more than 2% on fears a ban on Russian oil imports would lead to increasing energy costs, rising inflation and could halt economic growth. Todays decline by the DJIA means it has fallen over 10% since its early January record high and, by definition, is now in a correction. Worse, the Nasdaq’s ended today down over 20% since its November record high, putting it in a bear market. The Energy and Utilities sectors were the only US sectors to end the day higher.

Tuesday: For the second day in a row, all four Indexes fell. On the bright side, they didn’t fall as much as on Monday. Investors in both Canada and the USA are concerned about the Ukraine invasion and its impact on the global economy and inflation. On the TSX, the Materials and Consumer Defensive sectors were the best performing sectors today, while the Technology sector was the worst performer.

In the US, President Biden banned Russian oil and other energy imports from the US. The Energy sector continues to lead the charge, but it was not enough to offset losses in the Consumer Defensive, Healthcare, and Utilities sectors. Some positive news for me was some of the mega cap growth stocks inched upward. Not much, but at least it was in the right direction.

Wednesday: A great day for the North American stock market today, with the TSX the only one of the four major Indexes not up 2% or more. All four Indexes were led by the Technology, Consumer Cyclical and Financials sectors. The Energy sectors in both countries fell when it was announced OPEC would support increasing oil exports to compensate for the loss of oil caused by the sanctions on Russia.

In Canada, Shopify (TSX:SHOP) jumped 13% to lead the Canadian Technology sector rebound. In America, The S&P had its best one-day gain since June 2020 and the Nasdaq had its biggest gain since March 2021.

Thursday: The US Labour Department reported over the last 12 months that the US inflation rate jumped 7.9%, the highest point since 1982. In Canada, the inflation sits at 5.1%, the highest since 1991. And that doesn’t include the latest surge in fuel prices in both countries. If those numbers aren’t bad enough, Russia’s invasion of Ukraine could land another nasty shock by driving energy prices higher.

In Canada, the TSX rose on the strength of the Energy and Materials sectors, again. In the US, all three Indexes resumed their decline after Wednesday’s technology driven rally. The four-decade high inflation rate all but confirmed the US Federal Reserve will be raising interest rates next week. The ongoing conflict in Ukraine is only adding to fears of inflation. Rising energy prices can’t help but drive up the cost of heating, food and just about everything else.

Friday: The week started on a down note Monday and ended with a down day on Friday with all four Indexes posting a loss for the day. In Canada, the economy added twice as many jobs as forecasted, causing the unemployment rate to fall below its pre-pandemic level for the first time. Not only have more people returned to work, but the average hourly wage is also slightly higher. This will likely lead to another interest rate hike in the future. The expectant interest hike, the Ukraine situation and taking some profit after a 1 month high likely led to today’s drop. Despite today’s decline, the TSX still inched into positive territory for the week the third consecutive week.

In the US, once again the Indexes took a tumble. The broad-based decline (all the S&P sectors fell) was fueled by the Ukraine invasion, anticipation of an interest rate hike at next week’s US Federal Reserve meeting, and probably investors taking some money off the table going into the weekend and given the volatile Ukraine situation.

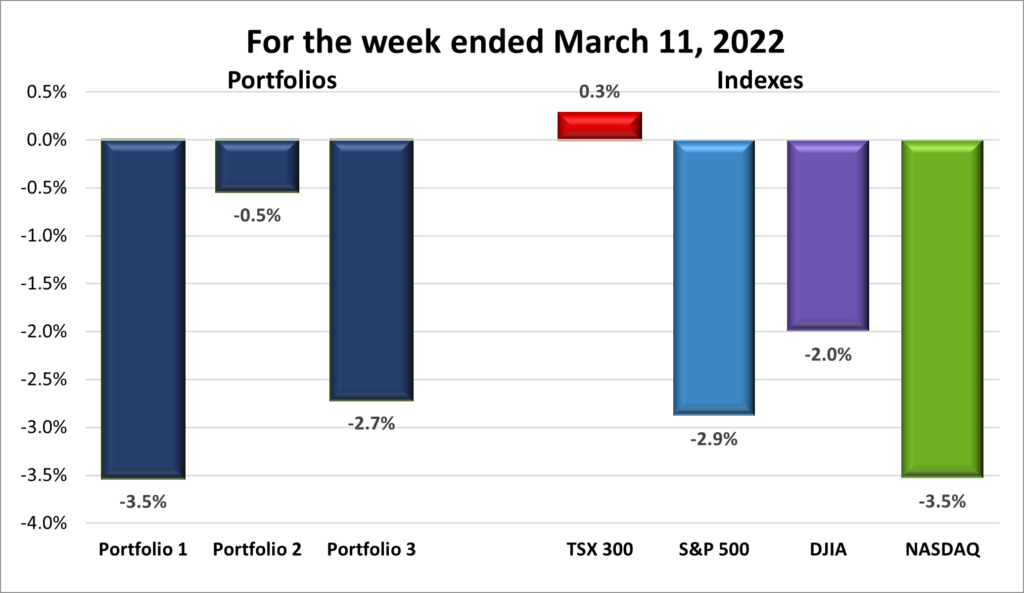

For the week, the TSX gained .3%, the S&P 500 fell 2.88%, the DJIA dropped 2%, and the Nasdaq shed 3.53%.

Weekly Portfolio Review

If you’re primarily invested in commodities on the TSX, you had another good week. If you’re like me with a slight majority of your investments in the US market, with a high growth technology bias, it was not a great week, again. Despite a strong surge on Wednesday, the three American Indexes still had a weekly decline of 2% or greater. For the DJIA, it was the fifth week in a row.

As all three Portfolios have a strong technology component, it was another poor week for the Portfolios. Once again, the more balanced Portfolio 2 declined the least There might be something to this balanced approach. 😊

Weekly Portfolio & Index performance for the week ended Mar. 11, 2022.

Companies on the Radar

With the news that Amazon (NASD:AMZN) will be splitting 20 for 1 in late May, the company has piqued my interest, even if I only buy 1 or 2 shares now so I’ll have 20 or 40 post split. Not much, but Amazon is dominant in a few high growth areas such as cloud services and e-commerce. They also plan a shareholder friendly $10 billion buyback of shares, meaning my shares would be worth a tiny bit more. Joining Amazon on my watch list are:

Portfolio 1 for the week ended March 11, 2022: DOWN

Google (NASD:GOOGL) is buying cybersecurity firm Mandiant (NASD:MNDT) for $5.4 billion, their second largest ever. This acquisition provides another diverse revenue stream in the fast-growing cybersecurity field to go along with their core digital advertising business. It also allows Google to more effectively compete against cloud rivals Microsoft and Amazon in the cloud infrastructure industry. The shift to working remotely during the pandemic, as well as the Russia – Ukraine conflict, has fueled a spike in cyberattacks and bolstered demand for security software, a market expected to more than double to $352.25 billion by 2026

On the electric vehicle front, Rivian (NASD:RIVN) committed a PR blunder when they announced a price increase on pre-ordered vehicles. They had to throw it into reverse after customer pushback (surprise). Anyone who had pre-ordered a Rivian vehicle will get the price they were quoted while new orders will get the higher price. Rivian blamed the price increase on supply chain issues. They should’ve foreseen the negative publicity that announcement would generate and the potential loss of goodwill and feel-good vibe around the company. A simple announcement of a price increase on all new sales as a result of supply chain issues would have done the job, which is exactly what they have now. An unforced error in my book.

Adding to Rivian’s troubles, Rivian sliced its production forecast in half due to thanks to the Ukraine invasion. Surging prices for raw materials have led to ongoing supply chain disruptions.

It was a busy week for GM (NYSE:GM) as they made several announcements this past week. First, they will launch a new independently owned, premium brand in China that will import GM vehicles currently unavailable in China. Next, they will partner with a South Korean company build a facility in Quebec that will produce cathode active material (CAM) for their Ultium batteries which will be used in electric vehicles. Finally, GM will work with Pacific gas and Electric in California to determine how electric vehicles can be used to power home during brownouts and blackouts. GM is certainly putting their money where their mouth is when it comes to electric vehicles.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Revenues for the quarter were $235.9 million compared to fourth quarter 2020 Revenues of $187.1 million.

Net income for the quarter was $102.0 million (net income of $33.4 million excluding warrant valuation gain) compared to net loss of $20.5 million in 2020 (net income of $27.4 million excluding warrant valuation loss).

Total revenue growth of 26.1% for the quarter compared to prior year reflected the results of our previously announced diversification strategy that is helping deliver a balanced portfolio growth where each line of business is a strong contributor.

Fiscal 2021 highlights

Revenues for the year were $757.8 million compared to 2020 Revenues of $668.5 million.

Net income for the year was $167.4 million (net income of $88.4 million excluding warrant valuation gain) compared to net loss of $87.8 million in 2020 (net income of $90.1 million excluding warrant valuation loss).

Total net revenues for the current quarter were $32.0 million.

Net revenues attributable to the Company’s core business for the quarter ended December 31, 2021, were $29.0 million, a new Company record and an increase of 11% over the quarter ended December 31, 2020.

Net income for the quarter ended December 31, 2021, totaled approximately $4.1 million, compared to $5.1 million for the quarter ended December 31, 2020.

Fiscal 2021 highlights

Net revenues for the year ended December 31, 2021, were $117.1 million for the Company, including $8.6 million of COVID-19 related sales and services.

Net income for the year ended December 31, 2021, totaled approximately $9.1 million, compared to $31.5 million for the year ended December 31, 2020. In the prior year, net income included an income tax benefit of $5.2 million and $34.4 million of COVID-19 response sales and services during the height of the COVID-19 pandemic.

The Company had a cash balance of $28.4 million on December 31, 2021. Total long-term debt as of December 31, 2021, was $4.3 million.

Revenue increased 83% to $211.9 million from $115.9 million.

Net income decreased to $12.3 million from $22.6 million, primarily due to a $29.7 million increase in share-based payments to employees who joined the Company as part of acquisitions completed during the third quarter and other employee incentive grants.

Total volume increased 127% to $31.5 billion from $13.9 billion

Fiscal 2021 highlights

Revenue increased 93% to $724.5 million from $376.2 million.

Net income increased by $210.7 million to $107.0 million compared to a net loss of $103.7 million.

Free cash flow increased by 100% to $290.1 million from $145.1 million.

Cash balance of $748.6 million on December 31, 2021, compared to $180.7 million on December 31, 2020.

The fourth quarter 2021 petroleum and natural gas sales increased 142% as compared to the same period in 2020.

Light crude oil price increased 90% over the fourth quarter of 2020, which was higher than the Company’s WTI benchmark increase of 75%.

Average realized ngl (natural gas liquids) price increased 161% in the fourth quarter as compared to the same period in 2020.

Fiscal 2021 highlights

Petroleum and natural gas sales increased 141% as compared to the prior year as a result of a 101% increase in the average realized commodity price combined with an increase in production.

Light crude oil price increased 90%, which was higher compared to the 62% increase in the WTI benchmark.

Average realized ngl price increased 130% over the same period in 2020, due to increases in product pricing for butane and pentane across North America.

Total revenue was $431.0 million, a 63% increase, compared to $264.9 million in the fourth quarter of fiscal 2021.

Annual Recurring Revenue (ARR) increased 65% year-over-year and grew to $1.73 billion as of January 31, 2022, of which $216.9 million was net new ARR added in the quarter.

GAAP net loss was $42.0 million, compared to $19.0 million in the fourth quarter of fiscal 2021.

Free cash flow was $127.3 million, compared to $97.4 million in the fourth quarter of fiscal 2021.

Fiscal 2021 highlights

Total revenue was $1.45 billion, a 66% increase, compared to $874.4 million in fiscal 2021.

GAAP net loss was $234.8 million, compared to $92.6 million in fiscal 2021.

Free cash flow was $441.8 million, compared to $292.9 million in fiscal 2021.

Added 1,638 net new subscription customers in the quarter for a total of 16,325 subscription customers as of January 31, 2022, representing 65% growth year-over-year.

subscription customers that have adopted four or more modules, five or more modules and six or more modules increased to 69%, 57%, and 34%, respectively, as of January 31, 2022.

Total revenue was $580.8 million, an increase of 35% year-over-year. Subscription revenue was $564.0 million, an increase of 37% year-over-year.

Gross margin was 77%, compared to 76% in the same period last year.

Net loss per basic and diluted share was $0.15 on 199 million shares outstanding compared to $0.38 on 189 million shares outstanding in the same period last year.

Fiscal 2021 highlights

Total revenue was $2.1 billion, an increase of 45% year-over-year. Subscription revenue was $2.0 billion, an increase of 47% year-over-year.

Gross margin was 78%, compared to 75% in fiscal 2021.

Net loss per basic and diluted share was $0.36 on 197 million shares outstanding compared to $1.31 on 186 million shares outstanding in fiscal 2021.

Authorized a stock repurchase program of up to $200 million of DocuSign’s outstanding common stock.

Revenue of $29.8 million, an increase of 59% from the same period in the prior year.

Gross profit of $23.7 million, an increase of 50% from the comparative period in the prior year, or 80% of revenue compared to 84% of revenue for the comparative period in the prior year

Net loss of $1.4 million, compared to net loss of $4.1 million from the same period in the prior year.

Fiscal 2021 highlights

Revenue of $104.2 million, an increase of 66% from the prior year.

Gross profit of $83.5 million, or 80% of revenue.

Net loss of $13.6 million, compared to net loss of $8.0 million for the prior year.

Total revenue was $36.8 million, a 33.9% sequential increase from the third quarter of 2021, a 5% year over year increase.

Net income was $2.5 million, compared to net income of $4.2 million for the three months ended December 31, 2020.

Cash and cash equivalents of $102.2 million, compared to $22.6 million as of December 31, 2020.

Fiscal 2021 highlights

Total revenue was $122.0 million, an increase of 16.3% compared to the same period in 2020.

Net income increased 186% to $10.6 million for the year ended December 31, 2021, compared to net income of $3.7 million for the year ended December 31, 2020.

Revenue of $21.4 million, an increase of 37% compared to $15.6 million.

Total Recurring Revenue(1) was $17.6 million, representing 82% of total revenue.

Gross Margin was 93%, compared to 96%. The change is primarily due to an increase in professional services, which offers lower margin revenue than licence or maintenance and support revenue.

Net Income was $0.8 million, a decrease of $3.7 million compared to $4.5 million. The change is primarily due to increased investments in Research & Development and Sales & Marketing, including restricted share unit expenses for 2021 awards in the period.

Fiscal 2021 highlights

Revenue of $70.3 million in FY 2021, an increase of 37%.

Gross Margin of 93% in FY 2021.

Net income of $7.3 million in FY 2021, a decrease of 31%

Portfolio 2

Portfolio 2 for the week ended March 11, 2022: DOWN