Since the start of the first quarter, all four of the major North American indexes – Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – finished the quarter higher than they started, as were the three portfolios. Let’s take a look at what happened over the first three months of 2023 ….

Contents

Portfolio 1 for the first quarter

Portfolio 2 for the first quarter

Portfolio 3 for the first quarter

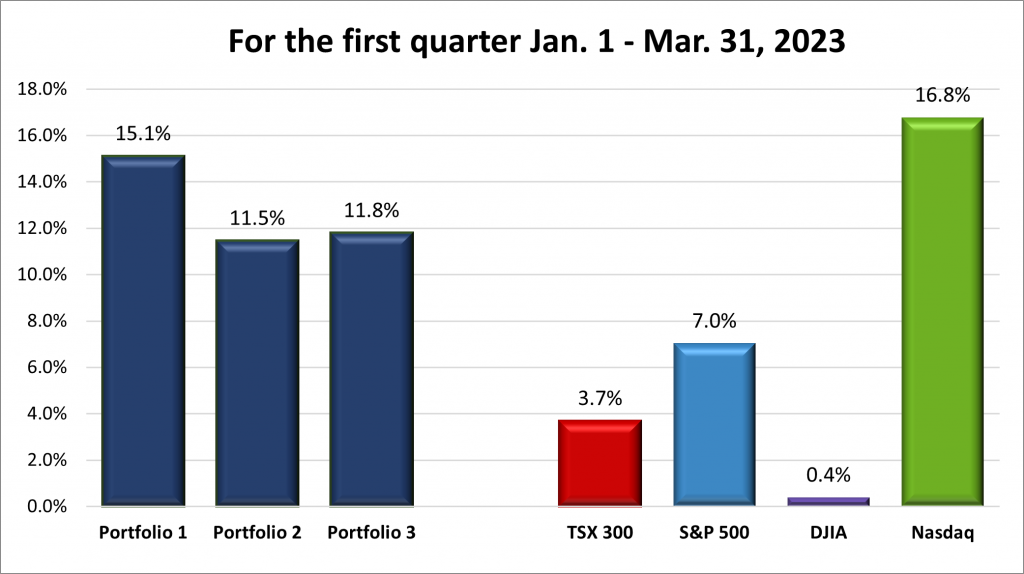

First Quarter Review

For the first quarter, the TSX (SPTSX) climbed 3.7%, the S&P (SPX) gained 7.0%, the DJIA (INDU) gained 0.4% while the Nasdaq (CCMP) surged 16.8%.

![]()

As seen in the chart above, the indexes started the year off on the right foot in January thanks to increased demand from China’s reopening after the Covid-19 pandemic shutdown most of China. In February, the indexes gave back some of January’s gain as fears of US interest rates reaching 6% became investors’ predominant concern and cooled the markets. While higher interest rates were paramount in investors’ minds, by the end of the February the focus turned to a liquidity crisis which claimed two regional US banks as well as one of the thirty large, global systemic banks – Credit Suisse. By the end of March, the markets rallied as investors gained confidence that the banking crisis had been contained and interest rates returned to the forefront.

In January, the Bank of Canada (BoC) raised the Canadian benchmark interest rate by 0.25% to 4.5%, then held it there through the remainder of the quarter. The number of consecutive interest increases by the US Federal Reserve (Fed) reached nine, including two hikes of 0.25% in the first quarter, sending the rate up to 5%, the highest its been since 2007. As well, the regional banking crisis led to tighter credit conditions, acting as an additional brake on the US economy. On the corporate side, many of the big technology companies reversed their pandemic hiring sprees by laying off up tp 10% of their workforce during the first quarter.

Despite all this, the Nasdaq notched its biggest quarterly percentage gain since June 2020, benefiting from a shift away from financial stocks to the mega cap technology stocks as a safe haven during the banking crisis. The S&P 500 posted a second straight quarter of gains, led by the technology sector’s more than 20% advance. As shown in the chart below, the Nasdaq and S&P enjoyed gains of 16.8% and 7%, respectively, as investors moved back into beaten down technology companies. In general, growth stocks enjoyed a sizable rebound after falling for most of 2022. The TSX had a decent quarter, up 3.7%. It was a reversal from the first quarter of 2022, as the Technology and Consumer Cyclicals (last year’s first quarter deadwights) did the heavy lifting this year, while the Energy sector (last year’s first quarter winner) was the deadwight in 2023. Finally, the DJIA, home of the blue chips, trailed with a gain of 0.4%.

Despite the strong start to 2023, all four indexes are still lower than they were on April 1, 2022. Going back to January 1, 2022, The S&P is still in a market correction (down more than 10%) and the Nasdaq remains in a bear market (down 20% or more). We are not out of the woods yet.

First Quarter Portfolio Update

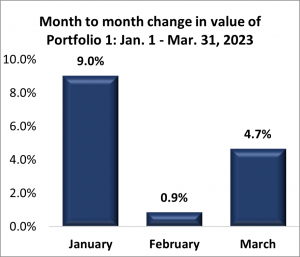

Portfolio 1 for the first quarter: UP

Portfolio 1 benefitted from the surge in Nasdaq, especially the surge in the big US technology companies – Alphabet up 18%, Apple gained 27% and Nvidia had a great quarter growing 90%. It was the only portfolio not to post a monthly loss. If it was not for the smaller technology companies that remain beaten down from 2022, the portfolio might have grown by 20%. However, 15.1% is great.

Activity: Sold Brookfield Select Opportunities; sold Viemed Healthcare; sold and bought back Trisura Group.

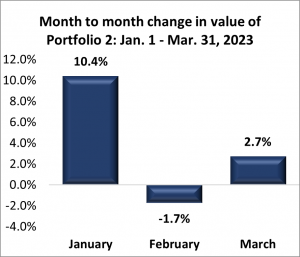

Portfolio 2 for the first quarter UP

The first quarter saw Portfolio 2 bookend a monthly loss in February with gains in January and March. The surge in the Technology sector boosted the portfolio in January, then the banking crisis dragged it down in February. Once the banking crisis started to fade, the technology companies in the portfolio pushed the portfolio back into the winning side, lifting it up 11.5% for the quarter.

Activity: Bought Crew Energy; sold Brookfield Select Opportunities; Summit Industrial Income REIT taken private, cash received for shares.

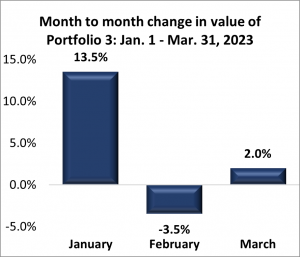

Portfolio 3 for the first quarter UP

The first quarter was much better for Portfolio 3, as it rode the surge in technology companies, despite a February swoon highlighted by a 20% drop in Shopify’s share price. The portfolio gained 11.8% for the quarter.

Activity: Bought more Alvopetro; sold Brookfield Select Opportunities; sold Viemed Healthcare.

Looking forward

A year ago, the concerns were the Russian invasion of Ukraine and rising inflation. As the second quarter of 2023 begins, the Russian invasion continues, a banking crisis came and seems to have gone (but not completely out of the picture). The BoC paused its interest rate hike campaign it began a year ago and plans to hold it there unless data dictates otherwise. Investors have once again focused on the Fed to see what they will do at their upcoming meeting in early May. Will they raise the interest rate and possibly send the US into a recession, or will they pause the rate hikes? Even if the Fed pauses the rate hikes, investors still need to keep in mind:

- The banking crisis has caused banks to tighten their lending standards making cash harder to obtain.

- As the economy cools there will be higher unemployment, leading to lower demand.

- With slowing demand, corporate earnings could falter.

Despite the almost singular focus on the US benchmark interest rate and whether another increase will tip the world’s largest economy into a recession, the outlook for the markets remains cloudy. The Nasdaq is currently in a bull market (up 20% since its October low). Hopefully, that bull market is contagious and will spread to the other three indexes. 😊 At this point I am cautiously optimistic that the markets and portfolios will continue their upward trends. One bull is back, may the other three return!