Back at the start of the year, in January 2022, financial analysts were warning, if not screaming, that inflation and higher interest rates were coming. Prices were rising and it was going to cost more to pay off debt, be it loans, mortgages, or corporate debt. That we knew should have planned accordingly (I did not ☹). What most of the world did not expect was for Russia to invade Ukraine.

With the onset of the invasion and the subsequent sanctions against Russia by the US and other western countries, the global supply of natural gas, oil, wheat, and other natural resources from this region were severely disrupted. Shortages of these essential materials that were just beginning to rebound from the pandemic were further squeezed. Manufacturers that had previously sourced materials (oil, metals, etc.) from traditional sources in Russia were suddenly having to secure new suppliers in other parts of the world. These supply constraints, combined high demand caused by a world emerging from a global shutdown, has conspired to send prices surging in many industries. As a result, prices that had been slowly creeping higher suddenly jumped higher. For consumers in North America, that was most noticeably felt at the gas pump. For Europeans, not only were higher prices reflected at the pump but also in their heating bills, with higher prices expected this winter.

For us investors, this was a double-edged sword. On the positive side, if you had the foresight to know the invasion would occur and therefore cause the price of oil to skyrocket or were simply invested in the right sector at the right time (most likely), you would being doing OK in 2022, or not as bad as most investors in 2022.

On the negative side, the conflict accelerated higher prices which negatively impacted all of us, not just investors. As well, the conflict accelerated inflation which has led to higher interest rates as central banks (think Bank of Canada or the US Federal Reserve) attempt to get inflation back to the traditional 2% – 3% target range. As interest rates climbed, the cost of borrowing climbed and sent the shares prices of many non-energy companies plummeting. No where is this more noticeable than for high growth companies like those typically found in the Technology and Consumer Cyclical sectors, where share prices have plunged in 2022. These high-growth companies need to use their cash to build their respective businesses rather than putting more cash towards paying off interest.

I have found one of the keys to investing is to look ahead rather than focus on the present. To paraphrase Wayne Gretzky, “look to where the world is going, not where it has been.” In 2019 – 2020, I was investing in renewable energy companies, figuring that is where the world was going, and various governments were strongly encouraging the move away from traditional energy sources. In 2021, a friend told me he had been investing in oil companies. I wondered why when renewables were the ‘thing,’ and oil and natural gas companies were out of favour. He showed me how the earnings and share prices of the various companies had been moving steadily upward. The light bulb went on.

To make a long story short, after doing due diligence on the oil industry and a few oil and natural gas companies, I did what I never thought I would do – bought my first two oil companies, International Petroleum Corporation (TSX:IPCO) and Crew Energy (TSX:CR) in 2021. (OK, I invested in the oil companies, but I like to think of myself as an owner, albeit an exceedingly small owner). Both companies were doing well prior to the Russian invasion and continue to do well. They have done so well that I bought a third energy company this year – Alvopetro Energy Ltd. (TSV:ALV). As you can see by the chart, these three energy companies have done well since the start of 2022. I do not see buying additional oil and gas companies in the future, but I did not see buy any to begin with. Instead, I am already looking for opportunities where demand could exceed supply.

Do I wish I had been looking farther ahead in 2019? Yes! But I did learn that Mr. Gretzky’s, “look to where the puck is going, not where it has been” can be applied to investing. While I missed the early stages of the oil rush, I like to think I am well positioned in the event hostilities between China and Taiwan breakout.

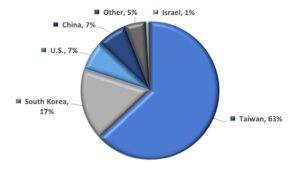

Considering recent events in the waters between China and Taiwan, it is not hard to imagine conflict over Taiwan independence breaking out. Besides the pain and suffering caused by wars, from an investing perspective, the cost of semiconductors (or chips) will skyrocket as most (over 60%) of advanced semiconductors are made in Taiwan (see chart). Smart phones to military weapons utilize chips, chips are important both from an economic standpoint as well as security standpoint.

Labour shortages were the issue during the pandemic. In the case of conflict, buildings would be destroyed, and it would take billions of dollars to rebuild the foundries, not to mention a significant number of years. If chip foundries were to get damaged or destroyed during a conflict, it could cause a global shortage of semiconductors far worse than shortages caused by the recent Covid-19 pandemic. Imagine paying exorbitant prices for a new iPhone (OK, even more exorbitant prices), assuming you could even get one. The same would be for any smart device, appliance, or vehicle. If you think there were supply issues the last few years, imagine the problems if 60% of the world’s chip makers go offline or are unable to ship their products to their customers. If any existing smart device, appliance, vehicle, or other component that requires chips were to break down, it would be a lengthy wait to get the item repaired. It was hard enough getting parts during the pandemic; this would be much worse.

I had no way of knowing Russia would invade Ukraine and spark an energy shortage. However, my investing takeaway from the energy shortage is to make a semi educated guess where the world is going and try to invest accordingly. While I hope conflict does not break out over Taiwan, with three chip companies (Nvidia (NASD:NVDA), Lattice Semiconductor (NASD:LSCC) and Skyworks Solutions (NASD:SWKS), I am well positioned if a shortage does occur.