Fractional shares….

Just when supply chain problems were slowly being eliminated, rail workers in the US threatened to go on strike. Fortunately, a deal between the major U.S. railroads and the railroad unions was reached to avert a work stoppage. This was such a crucial deal for the US economy that even President Biden took part in the negotiations, though I would guess it was more a signal of the importance of this deal.

According to an Association of American Railroads report, if the railroad system in the US was to grind to a halt, the US economy would lose $2 billion every day the trains were idle. The US railroad system accounts for almost 30% of cargo by weight shipped across America. It would take approximately 467,000 additional freight trucks each day to make up the loss. In other words, a national rail strike would be painful for everyone.

USA: The stock markets ran red, deep red, when this week’s US Consumer Price Index (CPI) data for August was announced. Investors dropped stocks like a hot potato this week as investors braced for the U.S. Federal Reserve (Fed) to come out swinging next week in its battle with inflation.

The US CPI increased by 0.1% over July and 8.3% over the previous year. Analysts were expecting 8.1% over the prior year so a higher-than-expected increase was a surprise. Core CPI, which strips out volatile food and energy prices, increased more than expected, rising to 6.3% from 5.9% in July. As I have said before, the markets do not like surprises, especially negative surprises, and the American markets reacted accordingly with the S&P having its worst days since June 2020 and falling 4.8%. If that was not bad enough, the tech heavy Nasdaq fell 5.5%. The DJIA did not escape unscathed, its week was just not as bad as it ‘only’ fell 4.1%. Ouch!

Analysts now expect a 0.75% rate hike by the Fed during their meeting next week to fight inflation. However, the possibility of a full 1% hike lurks in the shadows as the Fed may now feel justified in taking even bigger steps to get a handle on inflation. Going forward, investors are now wondering what the Fed’s plans are for future rate hikes scheduled for November and December.

This does not bode well for the Portfolios.

Canada: There is a saying that when the US sneezes, Canada gets a cold. Well, this week the US sneezed, sending stock markets in Canada and around the tumbling.

Fortunately, energy prices continue to cushion the fall in the Canadian market. On the Toronto Stock Exchange Composite Index (TSX), the Energy sector accounts for 18% of the market capitalization. This heavy weighting of energy companies has helped the TSX avoid the dramatic declines seen in other markets. While higher oil and natural gas prices is good news for those invested in oil and natural gas companies, its not great news for consumers as those higher prices are reflected at the gas pump.

The good news is gas prices continue to drop which should eventually lead to lower transportation costs to bring products to market, resulting in lower prices.

Next week, several key Canadian economic data are due to be released, including the Producer Prices data for August, the Consumer Price Index report for August, and the Retail Sales data for July.

Ethereum merged the two Ethereum blockchains into one, which Ethereum claims will not only reduce its energy use by 99.95%, but it will also enable cheaper cryptocurrency transactions, as well as help the second biggest cryptocurrency network to expand into other areas and opportunities. For here more information on “The Merge.”

With all that foreshadowing about the stock markets falling, lets take a look at what happened in the stock market and to the Portfolios….

Weekly Market Review

Monday: This week picked up where last week left off with all four major North American stock exchanges ending solidly higher. In Canada, higher oil prices lifted the Toronto Stock Exchange Composite Index (TSX) to hits highest close in three weeks, as all Canadian sectors ended the day higher.

In the US, all three American Indexes – the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – rose on the day before the release of the key Consumer Price Index (CPI) data. Analysts and investors are waiting for Tuesday’s inflation report and how it will impact the US Federal Reserve’s (Fed) upcoming interest rate hike. In the markets, all S&P sectors closed higher, led by the Energy, Consumer Cyclical and Technology sectors.

Tuesday: So ends the four-day rally. Thanks to a higher-than-expected US CPI report, the stock markets took a drubbing today. In Canada, the TSX posted its largest loss in almost three months. All Canadian sectors lost ground with the Utilities and Energy sectors being the only sectors to limit losses to under 1%. Interest sensitive sectors such as Technology and Consumer Cyclical had a tough day.

In the US it was even worse than in Canada. All three American Indexes saw their four day winning streaks broken and all eleven S&P sectors ended deeply in the red. Every single stock in the Nasdaq 100 ended lower – that has not happened since March 2020. The CPI report indicated inflation remained high which crushed any chance of the Fed easing off on their upcoming interest rate hike. Analysts are now considering a full 1% interest rate hike by the Fed later this month.

Leading the way lower were the interest sensitive sectors such as Technology which fell over 5%, and Consumer Cyclical which dropped almost 5%. Not a good day for the growth companies.

Wednesday: I was not sure if today would bring more stock market declines or a bounce. It looks like the markets had a wee bounce with all four Indexes ending the day slightly higher. In Canada, higher oil prices were the main reason the TSX was able to end higher. Other sectors helping the TSX higher include the Technology sector, with a slight bounce back after yesterday’s sharp drop, and the Basic Materials sector (natural resources & fertilizers).

In the US, investors took a deep breath to recover from yesterday’s sell off. It was the largest percentage drop for the S&P, DJIA and Nasdaq since the start of the pandemic. Data from today’s Producers Price Index (PPI) report came in as expected (dropped 0.1%) suggesting inflation has not become entrenched as feared. Although the news helped halt yesterday’s rout, the three American Indexes did not exactly inspire confidence with today’s performance. Nonetheless, a gain is a gain, and better than a loss. 😊

As was the case in Canada, higher oil prices lifted the S&P Energy sector, while rebounds in yesterday’s whipping boys – the Technology and Consumer Cyclical sectors – help push all three Indexes into the black.

Thursday: The markets gave back the wee bounce they took Wednesday with all four major North American Indexes ending lower. Investors are worried about the size of the Fed’s upcoming US interest rate hike and continued to sell their shares, with the high growth technology companies bearing the brunt of the sell-off. In Canada, a drop in the price of oil did not do the TSX any favours as the Energy and Basic Materials sectors had the largest fall. The Telecommunications Services and Financials sectors were the only two to make headway today.

In the US, analysts are confident the Fed will raise the US benchmark rate by 0.75%, with an outside chance at a 1.0% increase, but they are also trying to figure out what the Fed will do for the rest of the year. In the stock markets, the Healthcare sector was the only S&P sector to post a gain today, while Utilities and Energy fell the farthest.

Friday: Fears of inflation and another aggressive interest rate hike by the Fed, and to a lesser extent, another hike by the Bank of Canada, dragged all four Indexes lower. In Canada, the Telecommunications Services and Consumer Staples were the only sectors on the TSX that were able to inch into positive territory.

In the US, the Nasdaq and S&P fell to lows last seen in July 2022 thanks to investors’ concerns about future interest rate increases. Analysts expect another 0.75% increase to come out of the Fed’s meeting next week, but there is an outside chance the Fed will go for a full 1% increase. Now that would send the markets into a tizzy, and not in a good way. Meanwhile, in the markets today all eleven S&P sectors ended in the red.

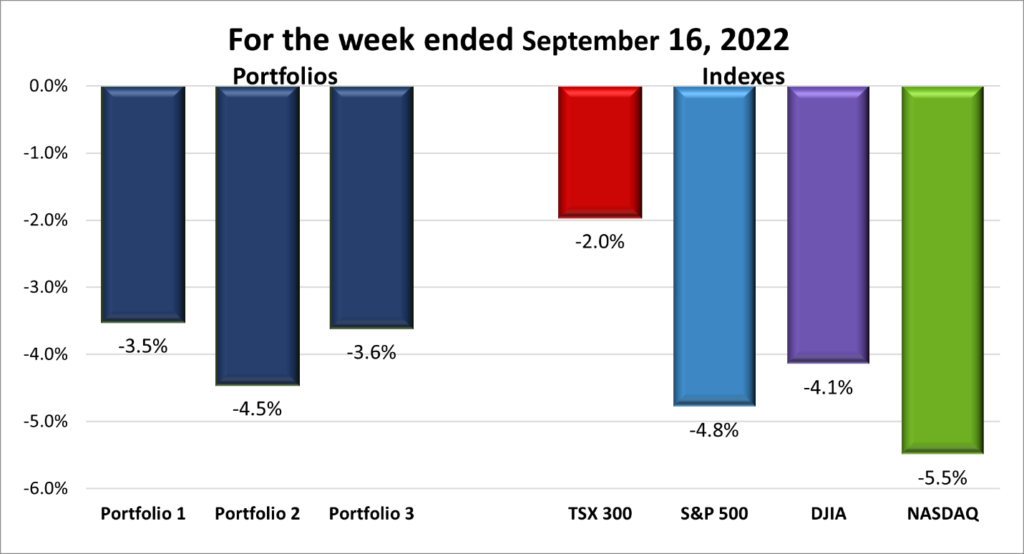

For the week, the TSX fell 2.0%, the S&P 500 tumbled down 4.8%, the Dow lost 4.1% and the Nasdaq plunged 5.5%.

Weekly Portfolio Review

If last week was a pleasant surprise, this week was an unpleasant surprise thanks to the higher-than-expected US CPI numbers. The chart below shows the Nasdaq and the S&P fell the most. Since both Indexes are heavily weight towards interest sensitive, high growth-oriented companies (primarily technology and consumer cyclical companies), this is hardly surprising since the high growth companies tend to have a lot of debt. The more debt a company has the more of its cash is required to pay the interest on that debt, cash that could have been used to grow the company. The TSX, which is more heavily weighted with energy, mining, and financial companies, fell but no where near as badly as the American Indexes.

If the Indexes drop, the Portfolios must drop (or be lucky). And drop they did, with each falling more than 3%. Ouch! As the week wore on, I fully expected the Portfolios to decline so it was not a surprise to see all three lower. What was a surprise was Portfolio 2 fell the farthest. Given its less risky collection of companies, Portfolio 2 usually falls the least. However, MongoDB (NASD:MDB) had a bad week, dropping over 25%. Add in a bad week by the other technology companies in the portfolio and I can see Portfolio 2 dropping 4.5%. Maybe I should be more surprised that Portfolios 1 and 3 did not fall farther. 😊

I want to think next week will be better for the Indexes and the Portfolios but with the Fed set to announce the latest US interest rate hike, I am not holding my breath.

Companies on the Radar

I recently read that copper is essential to the electric revolution. Electric vehicles, wind turbines, solar power, and the infrastructure required to harness renewable energy, all require copper. Demand for copper is expected to double by 2035. With this growing demand for copper and copper companies appearing to be down from early 2022 highs, I have been looking for a few of the better copper mining companies. So far, I am only at the name gathering stage, but here are a few that I have seen mentioned when searching for “top copper miners 2022.”

- Copper Mountain Mining Corporation (TSX:CMMC)

- Capstone Copper Corp. (TSX:CS)

- Hudbay Minerals Inc. (TSX:HBM)

- First Quantum Minerals Ltd. (TSX:FM)

- Lundin Mining Corporation (TSX:LUN)

These are all small cap companies so are likely very volatile, but they could also have more potential than some of the bigger copper miners. I know nothing about mining companies, so I plan to take a high-level look at these companies in the next little while before deciding to dig deeper (get it, mining companies dig deeper 😊). When it comes to copper prices moving higher. I think it’s more a question of when rather than if.

Still on my radar are Amazon (NASD:AMZN), Ferrari (NYSE:RACE) and Brookfield Select Opportunities (TSX:BSO.UN) as well as last week’s additions XPEL, Inc. (NASD:XPEL) and WESCO International (NYSE:WCC).

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended September 16, 2022: DOWN ![]()

- Nvidia (NASD:NVDA) anticipates losing as much as US$ 400 million in revenue thanks to US government regulations limiting the shipment of their top semiconductor chips, the A100 and H100, to China. Going forward, Nvidia and other leading US based chip manufacturers will require permission from the US government to sell specific products to Chinese companies.

- Unity Software (NYSE:U) saw their share price plunge when AppLovin withdrew its buyout offer. With AppLovin’s unsolicited bid out of the way, the path is now clear for Unity to complete their purchase of ironSource. The acquisition of ironSource should help Unity developers grow and monetize their apps and thereby help Unity grow and prosper.

- Alphabet’s Google (NASD:GOOGL) was hit with a record €4.1 billion (euros) by Europe’s General Court when it ruled Google broke European Union anti-trust rules, specifically the Digital Markets Act. As big as the fine is, Google is more concerned that the decision will embolden other regulators to go after Google.

- Regulatory oversight is coming to “buy-now, pay-later” (BNPL) companies, such as PayPal (NASD:PYPL). The US Consumer Financial Protection Bureau (CFPB) announced they plan to start regulating the emerging industry over concerns the products of BNPL companies could harm consumers. The CFBP would like to standardize disclosures for all members of the BNPL industry, provide data to credit reporting agencies to provide a better overall picture of the potential borrower, and identify appropriate data collection and surveillance practises.

- Apple (NASD:AAPL) unveiled a new feature as part of their iPhone 14 release called ‘Emergency SOS via satellite’. This feature would allow the high-end versions of iPhone 14 to make satellite calls. To further iPhone satellite capabilities, Apple is investing US$ 450 million toward building out this satellite capabilities with satellite operator partner Globalstar (NYSE:GSAT). Apple will put up 95% of the costs and in return Apple will receive exclusive access to 85% of Globalstar’s current and future network capacity to support Apple’s satellite features.

- Cargojet (TSX:CJT) was selected the Shipper’s Carrier of Choice Award by the Canadian Shipper magazine.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Yellow Pages Ltd (TSX:Y)

Automotive Properties Real Estate Investment Trust (TSX:APR.UN)

US $

BSR Real Estate Investment Trust (TSX:HOM.U)

Skyworks Solutions Inc (NASD:SWKS)

ZIM Integrated Shipping Services Ltd (NYSE:ZIM)

Home Depot Inc (NYSE:HD)

General Motors Co (NYSE:GM)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended September 16, 2022: DOWN ![]()

- Microsoft’s (NASD:MSFT) acquisition of game maker Activision Blizzard (NASD:ATVI) is going to be put under the microscope by Britain’s Competition and Markets Authority (CMA). The CMA contends the purchase of Activision could harm competition in the gaming industry if competitors were denied access to Activision’s games.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

iA Financial Corporation Inc (TSX:IAG)

Summit Industrial Income REIT (TSX:SMU.UN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended September 16, 2022: DOWN ![]()

- Shopify (TSX:SHOP) is rolling out a new compensation structure that will allow employees to structure their awards to better suit their individual needs. Employees who enroll in the new compensation system will be able to choose the mix of cash and equities that works best for them.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.