Items that may only interest me ….

Statistics Canada data released this week showed Canada’s Consumer Price Index (CPI) year over year inflation rate for September rose to 6.9%, decelerating from 7% in August (analysts were expecting 6.8%). That is the third successive month that the year over year CPI has dropped. As well, Canada’s core CPI (CPI without gas and food prices) was up slightly from 5.3% in August, year over year, to 5.4% year over year in September.

While a drop in the overall CPI is a good sign inflation is moving in the right direction (down), it is still well above the BoC’s target of 2%. This latest data, combined with the Bank of Canada’s (BoC) commitment to getting inflation under control, leads analysts to believe they will raise the Canadian benchmark interest rate by 0.75% next week, raising the rate to 4.0%, a 14 year high. Anyone with any type of debt that has a variable interest rate is feeling the bite of these increasing rates. To make matters worse, analysts increasingly believe the pace of the rate hikes, with the likelihood there are more to come, will push Canada into a recession (a period of negative economic growth). We do not want a recession as they can cause businesses to fail, fewer job opportunities and lower wages.

On the other hand, some analysts believe the upcoming rate hike will be 0.5% as the BoC attempts to avoid a recession. We shall see next week.

With the global stock markets falling, many investors are getting out of the markets and sitting on their money, waiting for the markets to stop falling and head upward. The preferred currency for many investors is the US dollar, leading to a stronger US dollar. As the US Dollar continues to strengthen it does so at the expense of other currencies, such as the Canadian dollar. The weaker a currency gets, the more of that currency is required to obtain the same items. As inflation remains high, the Canadian dollar does not go as far as it used to. Every time we go to the store or the gas station, we feel it as we pay more for the same product or same amount of fuel. This is the definition of inflation.

However, inflation also impacts our investments and erodes the wealth we have worked hard to build up. The last thing you want is to find out inflation has pushed costs up so much that you must withdraw more cash than you anticipated from your investments. Once you withdraw cash from your nest egg, the cash is no longer working for you, and you have less cash working for you going forward. Being able to keep as much of your money working for you as long as possible is another reason investors want to see inflation quickly return to the 1% – 3% range. Not to mention, inflation in the 2% range would allow the BoC and the US Federal Reserve Bank (Fed) to let interest rates drift back down to previous 2021 levels.

Thanks to a self-inflicted financial wound, Elizabeth Truss resigned as Britian’s Prime Minister this past week. Her 45-day reign was the shortest in Britain’s history. The governing Conservative Party will now select their third leader, and therefore Prime Minister, in three months. Her resignation comes on the heels of replacing her first Chancellor of the Exchequer (finance minister) whose low-tax, high-borrowing policies greatly alarmed British investors, sent British markets tumbling, and greased the skids of his own demise. The new Chancellor of the Exchequer immediately reversed course, cutting most of the planned tax cuts which calmed the British market and restored confidence in the British pound. But that was too little, too late for Ms. Truss, she had lost the confidence of her party and it was only a matter of time before they pushed her out. Hopefully, the Conservative party will choose a more businesslike leader who will provide a steady hand as the United Kingdom attempts to dig itself out of the financial mess.

Why do I spend time on what is happening on the other side of the Atlantic, you ask? To illustrate how globally connected the stock markets of the world are. When the London markets and British pound went into a freefall, it spooked investors in North America, causing the North American markets to sag. I find it useful to be aware of what is happening globally to understand what impacts investor sentiment and moves the markets.

Since the start of 2022, many analysts and investors believed that inflation would be under control by the end of the year and a return to ‘normal’ would begin in 2023. Unfortunately, inflation remains a lot higher than many had expected.

There have been a few rallies, but they have turned out to be ‘bear rallies’ (short lived rallies before resuming the downward trend), with last week’s one day rally being the latest. Investors keep hoping each rally is a market bottom, only to see it become a bear trap as the markets resume their downward slide within few days. Analysts believe the market is unlikely to establish a true bottom until the Fed lowers the size and slows the pace of its rate hikes. And that will not happen until US employment numbers start to soften. This would enable the Fed to slow their rate hikes and eventually start reducing the interest rate. It is the same story in Canada, but the US economy is clearly driving the bus of global economies.

Another thing that could really help the markets is an end to the invasion of Ukraine. The combination of weaker employment numbers and an end to the conflict in Ukraine would be extremely bullish for the North American stock markets.

Rather than holding our breath waiting for the markets to pivot upward, let’s take a look at the past week….

Weekly Market Review

Monday: The week started off with a bang as the four major North American stock indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – all advanced at least 1.5%. Investors on both sides of the border

In Canada, analysts and investors are starting to believe the Bank of Canada (BoC) will raise the benchmark interest rate by 0.5% rather than an additional 0.75%. Given the BoC and the US Federal Reserve Bank (Fed) have been crystal clear on inflation being their #1 enemy, a 0.5% hike seems a bit optimistic. We shall find out next week. Meanwhile, on the Toronto Stock Exchange, all Canadian sectors ended the session higher with the Technology, Utilities, and Industrials sectors leading the way.

In the US, the third quarter earnings report season got underway with US banks posting solid quarterly results, thanks to the higher interest rate charges they are collecting. Investors were hoping that good news in the Financials sector is a good sign for the other sectors, especially the interest rate sensitive, high-growth Consumer Cyclicals, and Technology sectors.

Tuesday: That is a two-day winning streak for all four Indexes. Today’s gain is not as impressive as Monday’s gains but still solidly in the black. Analysts and investors are starting to think that inflation has peaked and the BoC and the Fed will slowdown, if not start reversing recent interest rate hikes.

In Canada, all Canadian sectors ended higher with Industrials and Technology sectors leading the charge.

In the US, another day of strong earnings from US banks helped propel the three American Indexes higher. Helping boost investor sentiment were solid quarterly earnings reported by American companies. The Industrials and Utilities sectors were the best performing S&P sectors. A sign of the time, weapons maker Lockheed Martin (NYSE:LMT) rocketed up nearly 9% thanks to increased demand for weapons systems and ammunition. Hmmm, wonder if the war in Ukraine is a major factor in Lockheed’s increased sales? 😊

Wednesday: The two-day winning streak came to an end for all four major North American Indexes, with each ending within 1% of breaking even. In Canada, the inflation rate slowed to 6.9%, still well above their 2% target, leading analysts to believe the BoC will increase the Canadian interest rate by another 0.75%. I would not be surprised if there was not a bit of profit taking after the rally over the last two days. On the TSX, the Energy sector was the only one of the eleven Canadian sectors to end the day higher.

In the US of A, the American indexes retreated on ongoing fears the Fed will raise interest rates another 0.75%. It did not help that softer earnings reports from companies reporting today took away market momentum generated by solid earnings by the US banks earlier this week. In the market place, higher oil prices helped the S&P Energy sector climb into positive territory, something the other ten sectors were unable to accomplish.

Thursday: Another day of losses for the Indexes has evened up the week with two days of advances and two days of retreats, leaving Friday to decide the best of five contest. Comments from the Fed dashed hopes they would slow down the pace of their interest rate hikes, sending markets lower in both the US and Canada.

In Canada, as an owner of a few Candain technology companies, it was good to see the Technology sector higher and lead the way on the TSX. The Basic Materials (natural resources and fertilizers) and Energy were the only other sectors to advance.

In the US, the day started off on the right foot thanks strong earnings reports, but strong employment data and comments from a member of the Fed threw cold water on investors’ hopes the Fed would pause their planned November rate hike. On the American stock exchanges, the Telecommunications Services, Technology and Energy sectors were the only sectors to end higher.

Friday: Nothing like news the Fed is considering a smaller interest rate hike in December to jump start the markets as all four Indexes ended the day higher. With today’s advances, three out of five days this week saw the markets advance, leaving all four Indexes higher for the week. A fine way to end the week!

In Canada, the TSX had its biggest weekly gain since July as investors seem to have digested upcoming interest rate hikes. All Canadian sectors advanced, with Basic Materials, Utilities and Energy leading the way.

In the US, analysts expect a fourth straight 0.75% interest rates hike in November, before slowing down in December. In the market place, all eleven of the S&P sectors rose today, with the Basic Materials, Industrials and Consumer Cyclicals sectors the top gainers.

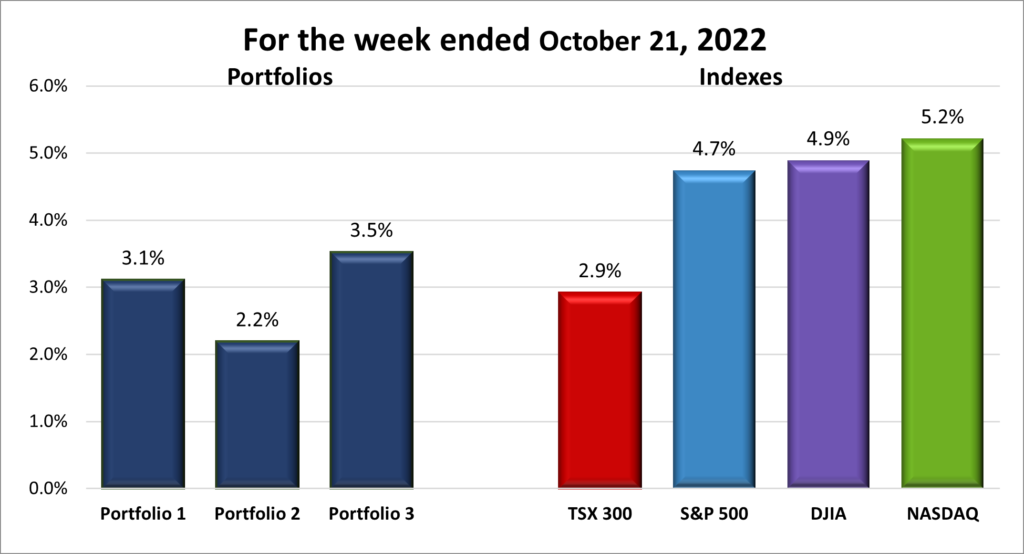

For the week, the TSX advanced 2.9%, the S&P 500 gained 0.36%, the Dow grew 0.13% and the Nasdaq jumped 2.15%.

Weekly Portfolio Review

Despite two negative days in the middle of the week, the three positive days easily pushed the four major North American Indexes higher. While investor sentiment is still bearish, it turned less negative on comments from the Fed they were prepared to discuss lowering the December interest rate hike to avoid sending the US economy into an ‘unforced downturn.’ Canadian analysts were also suggesting the BoC may lower next weeks interest hike. Both bits of positive news were enough to get investors looking for bargains. All three American indexes rose in the 5% range. Canada’s TSX also benefited from the upbeat news, but it does not have the number of beaten down high growth companies that investors flock upon hearing good news, like on the American indexes.

A good week for the Indexes is generally a good week for the Portfolios, and this week was no exception. Portfolios 1 and 3 with their heavier technology and high growth orientation outperformed the TSX, while Portfolio 2 had a solid week as well. I like weeks like this. 😊

Companies on the Radar

These are three companies I am looking at if the right opportunity presents itself. Joining Amazon (NASD:AMZN) and STMicroelectronics N.V. (NYSE:STM) on my radar list is Alphabet (NASD:GOOGL). As with Amazon, Alphabet has seen its share price plunge in 2022 and now could be a good time to add a few more shares.

- Amazon: dominant position in consumer sales; leader in cloud computing through Amazon Web Services (AWS); and a leader in streaming services (Amazon Prime).

- STMicroelectronics N.V.: European manufacturer of semiconductors (chips) for the automotive industry.

- Alphabet: clear leader in online search and online advertising (Google and YouTube); leader in mobile phone operating systems (Android); one of the top cloud computing platforms (Google Cloud); computer hardware and software (Chrome); plus, expanding into other areas, such as health.

Below are my Radar Check on these three companies.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended October 21, 2022: UP ![]()

- If you cannot beat’em, join’em. That is PayPal’s (NASD:PYPL) approach to loyalty programs as they announce their new rewards program. PayPal users earn points towards cash back that can be redeemed when checking out with the PayPal app.

- Docebo (TSX:DCBO) has won TrustRadius’s 2022 Tech Cares Award. The award recognizes companies that have made the most meaningful corporate social responsibility programs for their employees and surrounding environment.

- Tesla (NASD:TSLA) reported they produced and delivered a record number of vehicles in the third quarter. Despite record high revenue, the share price still took a hit when Tesla revised delivery growth expectations.

Chief Executive Officer Elon Musk said a ‘recession of sorts’ in China and Europe was lowering demand for Tesla’s vehicles. He also said Tesla would miss their annual delivery target because of limited transportation capacity to get their cars to market. - Lightspeed Commerce (TSX:LSPD) made a few changes to their executive level, promoting their Chief Revenue Officer, JD St-Martin, to President. He will be responsible for the strategic direction and overall performance of Lightspeed. As well, their Chief Business Officer will be departing at the end of 2022.

- Nvidia (NASD:NVDA) has expanded their collaboration with Oracle (NASD:ORCL) to supply tens of thousands of Nvidia’s high performance A100 and H100 graphics processing chips to help run the artificial intelligence used on Oracle’s cloud platform.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Automotive Properties Real Estate Investment Trust (TSX:APR.UN) DRIP

Andlauer Healthcare Group Inc (TSX:AND)

Algonquin Power & Utilities Corp (TSX:AQN) DRIP

US $

BSR Real Estate Investment Trust (TSX:HOM.U)

Quarterly Reports

Tesla, Inc.

All currency listed in millions of US dollars

Selected highlights from their third quarter 2022 financial results on October 19, 2022

- Revenue of $21,454 for the three months ended September 30, compared to $13,757 for the same period in 2021. An increase of almost 56%%.

- Net income of $3,688 for the three months ended September 30, compared to net income of $2,004 in the same period in 2021.

- Diluted earnings per ordinary share of $0.95 for the three months ended September 30, compared to $0.48 for the same period in 2021.

Portfolio 2

Portfolio 2 for the week ended October 21, 2022: UP ![]()

- Telus (TSX:T) announced a new online platform, ShopWithOwners.ca, to connect businesses and consumers for the upcoming holiday season.

As well, Telus submitted a request to the Canadian telecom regulator to add a 1.5% surcharge for customers who pay their monthly bills with a credit card. I hope this gets squashed as my experience has been it is the telecom companies that want you to pay by credit card to ensure they always get paid on time. Seems a little unethical to tell customers to pay by credit card and then to charge a surcharge to use their preferred method of payment.

- Disney (NYSE:DIS) extended their co-branding agreement with Visa (NYSE:V) and JP Morgan Chase (NYSE:JPM) for various Disney credit and debit cards, including a limited-edition metal Disney Premier Visa card in honour of the Disney Company’s 100th anniversary.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX:DIR.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended October 21, 2022: UP ![]()

- Telus maintained its position as Canada’s fastest mobile network based on Ookla’s Speedtest Global Index rankings that evaluate speed and network performance. Telus posted a median speed of 76 Mbps. Earlier in the year, Telus posted a 91.0 Mbps in Ookla’s Speed Score, giving it the honour of Canada’s Fastest Mobile Network for the tenth straight time.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Brookfield Select Opportunities Income Fund (TSX:BSO.UN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.