Items that may only interest or educate me ….

Welcome to December, TSX prospects for 2023, a fourth quarter comeback for the S&P, lower interest rate hikes, an inflation speed bump, Canadian banks’ earnings, and the next increase to the Canadian interest rate

November is over and ended with a bang thanks to the optimism created when the Chair of the US Federal Reserve (Fed) suggested it was time to slow the pace of increases to the US benchmark interest rate to see how the US economy was responding. Investors responded positively to this news, ensuring all four indexes each recorded their second consecutive monthly advance.

As we head into December, investors are hoping the traditionally strong month will end the year on an upbeat note. December has typically been a great one for stocks, with the S&P rising 71% of the time since 1950 (by my calculations, the Toronto Stock Exchange Composite Index (TSX) has risen in December four of the last five years). Of course, lower corporate profits and the Fed’s rate hikes might play the Grinch this year. Given how 2022 has gone, I am cautiously optimistic December will end higher. One can hope.

A bit of good news to start, analysts are predicting the TSX to gain 8% during 2023 and end 2023 slightly higher than it ended 2021 (21,222.80). They are also predicting the TSX to beat its all time high of 22,087.22 sometime in the late summer before moving higher going into 2024. However, analysts and economists say it depends on Canada experiencing nothing more than a mild recession. As with all predictions, it is just that – an educated guess. Who knows what other national or global events will occur between now and then to blow up those predictions. Afterall, no one predicted a global pandemic in 2020, and most people did not anticipate Russia invading Ukraine in 2021.

Since closing at a two-year low on October 10, the S&P 500 Index (S&P) has rebounded almost 14%. Not a bad gain in six weeks considering the headwinds the markets are experiencing. Higher interest rates, the increasing chances of a recession, lower corporate earnings and negative investor sentiment are all doing their best to buffet the S&P. However, investors seem determined to finish the year clawing back as much of their 2022 losses as possible. Starting with American Thanksgiving (also known as Cyber Weekend), online shoppers did their part with online sales of over US$ 35 billion, over the 5-day period. On Cyber Monday alone, sales hit US$ 11.3 billion, making it the biggest American online shopping day on record. Before rushing out and loading up on shares of retail companies, keep in mind 8% inflation artificially boosted prices.

Investors started December off rather gingerly, but it has only been two days. 😊

During a speech on Wednesday, the Fed’s Chair Jerome Powell said, “It makes sense to moderate the pace of our rate increases …. moderating the pace of rate increases may come as soon as the December meeting.” He indicated it would be a good time to evaluate how the rate hikes are impacting the American economy, given it takes time for the changes to kick in. He cautioned the fight with inflation had a long way to go. The Fed still needed to determine how high rates would go and how long they would remain at that level there before they could start lowering the interest rates. These comments gave investors more confidence of a 0.5% increase at the Fed’s December 13-14 meetings.

Investors should not get too excited about a potential change in direction by the Fed because a decline in earnings is imminent thanks to the cutbacks in spending by consumers and businesses alike. The potential downside to the markets from a significant decline in earnings would probably outweigh the possible upside from the Fed taking their foot off the interest rate gas pedal. It is almost a no-win scenario for share prices. If the Fed does not lower interest rates, share prices are likely headed lower. On the other hand, if the Fed does lower interest rates, expect a strong rally. However, before thinking higher interest rates are a thing of the past, keep in mind that the next earnings season will reflect profits while the interest rates were high. Those earnings reports are likely to be disappointing and the market (analysts and investors) does not like bad news. If companies announce disappointing earnings, the market will likely return to the funk it was in for most of 2022.

On Friday, a speed bump appeared in investors’ road to lower inflation. A report from the US Department of Labor showed the US labour market remains strong. This week’s non-farm payroll report showed US jobs grew more than expected, wages continued to rise, and unemployment remained unchanged. This data supports the Fed’s claim that there is still more work to be done in their battle to get inflation under control and back to their 2% target. The Fed has been saying interest rates will need to go higher and last longer and this data backs their statements. Do not fight the Fed.

Last week I mentioned the possibility of a rail strike in the US. Well, the US government was not going to let that happen because it could cost the US economy up to US$ 2 billion per day. President Biden and Congress intervened in the impasse between rail workers and rail owners to avoid what would have been the first nationwide strike in 30 years. The government imposed the deal originally worked out in September that provided a pay raise, one personal day (in lieu of paid sick days) and other benefits. The deal avoids bringing 30% of American cargo shipments by weight to a grinding halt and stranding millions who rely on rail lines to commute and travel throughout the US.

Canada’s big five banks reported fourth quarter earning this past week. Like other businesses, the banks have been impacted by the highest inflation in decades, and the Bank of Canada’s (BoC) increases to Canada’s benchmark interest rate to get inflation back down to their target 1% – 3% range.

The banks saw declines in revenues from their wealth management services as investors were concerned about preserving capital in the falling markets. The banks also saw a drop in fees from investment banking as businesses shied away from taking on debt due to the higher interest costs. The higher interest rates also caused a decline in the housing market as the higher rates discouraged potential buyers.

Not all has been bad for the banks as they saw increased revenues from their lending services thanks to the higher interest rates that effect mortgages, lines of credit, and business loans. While higher interest rates benefit banks’ lending units, the higher rates are also forcing the banks to set aside more cash in anticipation of a higher number of loan defaults caused by inflation and higher interest rates.

While the banks may not generate as much revenue and profit as previous years, I am confident they will be alright. Banks do not lose money. 😊

The items of interest section started with a bit of good news so let us end with a piece of good news. The latest report from Statistics Canada showed job growth continued to grow but was inline with analysts’ predictions. Wage growth remained the same from October and unemployment dropped to 5.1%. That data appears to indicate the multiple boosts to the benchmark interest rate has not ruined the Canadian economy, and there is room for further increases should they be required. With that in mind, investors are expecting a 0.25% – 0.5% interest rate increase at next week’s BoC interest rate announcement. This would bring the Canadian benchmark rate to 4.25%.

With that mixed bag of information out of the way, let us see how that information impacted the markets and the portfolios during the week of November 28 – December 2. Let’s begin.

Weekly Market Review

Monday: Another week, another Monday the markets took a step backwards. The impetus this time was an old friend that had been relegated to the back bench for most of 2022. Tighter Covid-19 restrictions in China led to numerous protests in China. These Covid-19 lockdowns are causing lower productivity in Chinese factories, and lower demand for raw materials. Many companies rely on China’s manufacturing capabilities so a slowdown in Chinese productivity would impact domestic and global economies.

In Canada, the Toronto Stock Exchange Composite Index (TSX) ended lower thanks to falling oil and natural resources prices. All was not lost on the TSX, as the Canadian Technology and Consumer Staples sectors were the best performers, while the Basic Materials (Natural resource miners and fertilizer manufacturers) and Financials sectors weighed down the TSX.

In the US, the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) all ended sharply lower on concerns how the Covid-19 restrictions in China will impact the growth of the Chinese economy (the second largest after the US). In the American markets, it was a full-blown retreat with all eleven sectors ending lower, with the S&P Energy and Basic Materials having the worst day.

Tuesday: A volatile day in the markets with the more growth-oriented Nasdaq and S&P ending slightly lower and the more value oriented TSX and DJIA ended slightly higher. Investors are watching for signs China could ease some of the restrictions of their zero covid policy that led to protests throughout China.

In Canada, higher prices for metals and natural resources tilted the TSX into positive territory for the day. In the Canadian sectors, the Basic Materials, Healthcare sectors were the best performers while Technology and Utilities fell the most.

In America, trading was relatively subdued ahead of Wednesday’s speech from the head of the US Federal Reserve (Fed). Analysts and investors will be looking for signs about the direction of the upcoming interest rate hike. In the US’s S&P sectors, strong days from the Energy, Basic Materials, Financials, and Industrials could not overcome losses in the remaining sectors.

Wednesday: All four indexes ended the day higher thanks to a speech from the Fed’s Chair, Jerome Powell. The indexes had been in the red until 1:30 when news got out that Mr. Powell had said, “It makes sense to moderate the pace of our rate increases …. moderating the pace of rate increases may come as soon as the December meeting.” Another data point suggesting a lower interest rate hike was the US jobs report showed job openings fell in October, reversing September’s surprising increase. Investors are now anticipating the Fed will raise the US benchmark interest rate by 0.5%, rather than the 0.75% in previous increases.

In Canada, despite poor earnings report from two of Canada’s biggest banks, the TSX rallied on the news the Fed is likely to lower the size of the next US interest rate hike. Canadian banks must increase their loan loss provisions in anticipation of people being unable to meet their loan, mortgage, and credit card requirements in 2023. This means cash they could normally use to grow their businesses or increase dividends is no longer available. On the TSX, the odd combination of Technology (high growth) and Utilities (defensive) sectors led all Canadian sectors. The only Canadian sector not to finish higher was the Energy sector.

In the US, many of the big-name technology stocks surged on Mr. Powell’s comments (which is good news for my three portfolios). Investors now turn to the Friday’s non-farm jobs report for signs job openings continue to fall. In the markets, the interest rate sensitive Technology and Consumer Cyclical S&P sectors were the best of a broad-based rally that saw all eleven sectors end in the black.

Thursday: Wednesday’s rally became a one hit wonder as the odd combination of the TSX and Nasdaq ended slightly higher while the S&P and DJIA were down slightly. An odd mix of a growth companies index paired with a more traditional companies index. Dual odd couples if you will.

In Canada, on the TSX ten of eleven of the Canadian sectors ended higher, with Energy the only sector to lose ground. The top performers on the day were the Technology and Basic Materials sectors.

In the US of A, investors were absorbing Wednesday’s news from the Fed about the likelihood of a 0.5% interest rate hike in mid-December, resulting in the mixed bag of American indexes. The S&P sectors were divided evenly between sectors that ended higher and those that slid back. Among the gainers were the Healthcare and Technology sectors. Dropping the most were the Energy and Financials sector.

Friday: Jobs reports in Canada and the US were the main market movers today. A stronger than expected US jobs report caused all four North American indexes to plunge in early morning trading. However, all four indexes clawed their way upward, with only the DJIA able to end in positive territory.

In Canada, the TSX ended the day down slightly thanks to the mixed bank earnings this week and anticipation of next week’s Canadian interest rate hike. This was reflected on the TSX where the Canadian Technology and Financials sectors had the biggest drop, overwhelming the day’s best performing sectors Healthcare and Consumer Cyclicals.

In the US, the US jobs report put an end to the upward momentum earlier in the week, causing the S&P and Nasdaq to end the day slightly lower while the DJIA barely made it into the black. In the American marketplace, Basic Materials and ad Consumer Staples were the best performers of the S&P sectors, while Energy and Utilities brought up the rear.

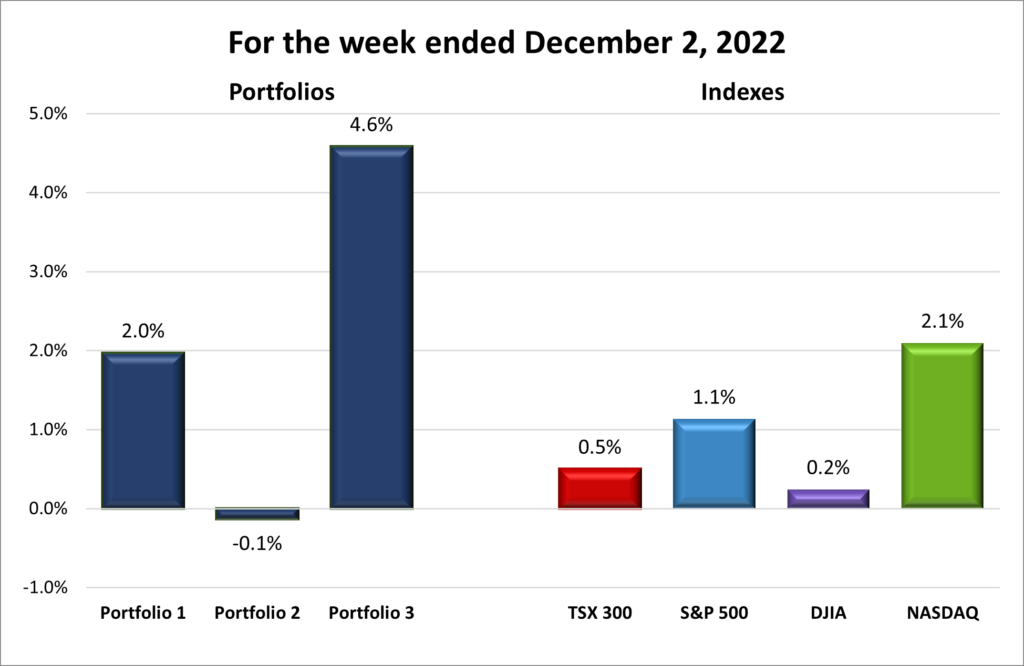

For the week, the TSX (SPTSX) increased 0.5%, the S&P (SPX) rose 1.1%, the DJIA (INDU) inched up 0.24% and the Nasdaq (CCMP) gained 2.1%.

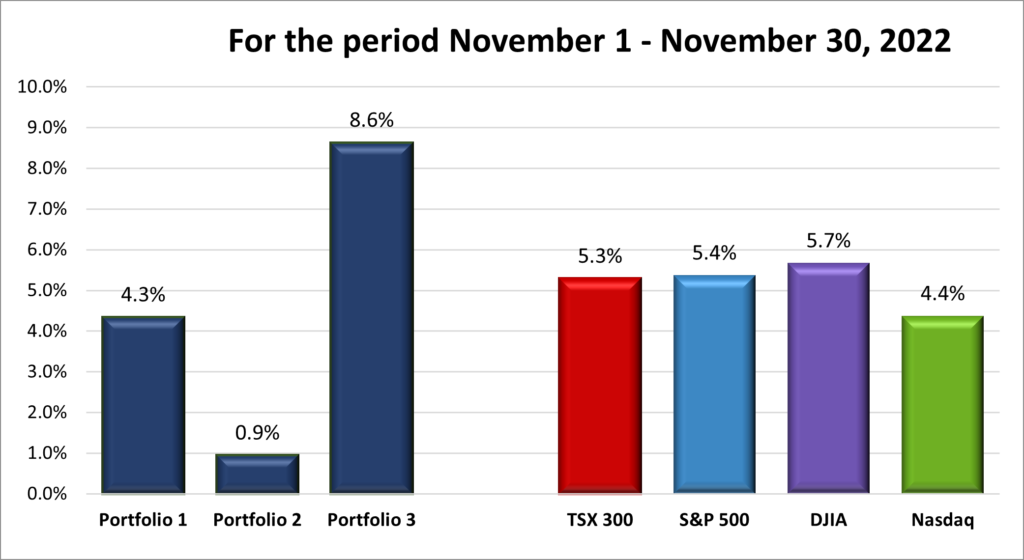

For the second consecutive month all four indexes ended higher. In November, the TSX (SPTSX) rose 4.8%, the S&P (SPX) increased 5.4%, the DJIA (INDU) gained 5.7% and the Nasdaq (CCMP) advanced 4.4%.

Weekly Portfolio Review

For the second week in a row all four indexes ended the week higher. The gains are decreasing but they are gains none the less. Many investors took this past week’s comments by the Chair of the Fed as a green light to move back into the more growth-oriented companies that reside on the Nasdaq and S&P.

A mixed week for the portfolios. Portfolios 1 and 3 benefitted from investors taking on more risk by moving into the growthier sectors, such as Technology. The biggest beneficiary was Portfolio 3 which has the heaviest weighting in Technology companies. Portfolio 1 is also biased to the Technology sector, but it also contains a number of non-technology companies. Unfortunately, Portfolio 2 just missed making it three for three for the Portfolios.

That is two months of gains in a row for the four indexes! Not as good as October’s gains, especially for the DJIA but it was unreasonable to expect another month of 15% growth. A lot of the gains can be attributed to the Fed, and the BoC to a lesser extent, hinting at lower future interest rate hikes. This in turn led to improved investor sentiment, opening the door for investors to cautiously re-enter the markets. Again, the DJIA, home of thirty blue chip companies, was the main beneficiary.

All three portfolios also advanced for the second consecutive month. As investor sentiment improved, investors moved back into the riskier Technology sectors in Canada and the USA. As with October, Portfolios 1 and 3 had the best improvement thanks to their heavier exposure to technology companies. Meanwhile, Portfolio 2, which had often been the best of a bad lot earlier in the year thanks to its more balanced, dividend-oriented portfolio, trailed the pack. As long as they each keep going up, I am happy. 😊

Companies on the Radar

My Radar list is currently comprised of Crew Energy (TSX:CR), International Petroleum (TSX:IPCO), Alvopetro Energy (TSXV:ALV) and Alphabet (NASD:GOOGL).

- International Petroleum: a Canadian company with oil and gas assets in Canada, Malaysia, and France.

- Alvopetro Energy: a Canadian natural gas company developing natural gas projects in Brazil.

- Crew Energy: a Canadian oil and gas company with interests in British Columbia.

- Alphabet: leading online search engine and advertising company, dominant mobile operating system.

Below are my Radar Checks on these companies, updated December 2, 2022.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended December 2, 2022: UP ![]()

- Thanks to production problems due to social unrest in China, many shoppers were unable to purchase Apple (NASD:AAPL) iPhones over the Black Friday – Cyber Monday weekend. Analysts are predicting ongoing unrest in China could lead to a shortfall of up to six million iPhones this holiday season. One of Apple’s primary suppliers, Foxconn, is already experiencing lower productivity and additional restrictions in China could only lead to a further shortage of Apple products.

- Amazon (NASD:AMZN) used its expertise from the retail side of Amazon to rollout a new cloud based service for its Amazon Web Services division. AWS Supply Chain will allow businesses to monitor their inventories and alert them when they run low.

- Tesla (NASD:TSLA) finally unveiled its long awaited Semi, an all electric semi trailer truck. The 18-wheeler is reported to have an 800 km/500 mile range but there was no information on how fast it took to re-charge nor how much cargo it can haul. The price was originally listed as US$ 180,000, but that was back in 2017. I am guessing the Semi is considerably more than it was in 2017. After waiting three years, PepsiCo (NYSE:PEPS) finally received their first Semis. If Tesla can deliver an electric semitruck that can replace traditional diesel semitrucks, Tesla will have a big win which should provide a nice boost to the share price.

Activity

Sold: Automotive Properties Real Estate Investment Trust (TSX:APR.UN). As I mentioned in the Weekly Update for November 18, APR is an automotive dealership property REIT, with properties located throughout Canada. I do not see an end to dealership lots, but I do see it as a finite market. Many of the new electric vehicle companies are not selling their vehicles on traditional car lots so I do not see huge demand for more car lots in Canada.

APR’s share price has been trending downward since December 2021. The REIT share price has not grown a much as the other REITS across the other the three portfolios, so I decided to sell this stock and replace it with another defensive, income generating REIT….

Bought: Dream Industrial Real Estate Investment Trust (TSX:DIR-UN). Dream has a broad portfolio of industrial properties across North America and they are expanding into Europe. With the growth of online shopping and the accompanying growth of distribution centres, I feel industrial REITs are a reliable source of income (6% monthly dividend) and provide balance and diversification to the portfolio. Finally, Dream has done well in Portfolio 2, and I want to add to this winner. In short, I have replaced APR with DIR.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Shaw Communications Inc (TSX:SJR.B)

US $

Visa Inc. (NYSE:V)

Quarterly Reports

Scotiabank

All currency listed in millions of Canadian dollars

Selected highlights from their fourth quarter 2022 financial results on November 29, 2022

- Revenue of $7,626 for the three months ended October 31, compared to $7,687 for the same period in 2021. A decrease of 1%.

- Net income of $2,093 for the three months ended October 31, compared to net income of $2,559 in the same period in 2021.

- Diluted earnings per ordinary share of $1.63 for the three months ended October 31, compared to $1.97 for the same period in 2021.

- Revenue of $31,416 for the twelve months ended October 31, compared to $31,252 for the same period in 2021. An increase of 0.5%.

- Net earnings of $10,174 for the twelve months ended October 31, compared to net earnings of $9,955 in the same period in 2021.

- Diluted earnings per ordinary share of $8.02 for the twelve months ended October 31, compared to $7.70 for the same period in 2021.

Shaw Communications Inc.

All currency listed in millions of Canadian dollars

Selected highlights from their fourth quarter 2022 financial results on November 29, 2022

- Revenue of $1,356 for the three months ended August 31, compared to $1,377 for the same period in 2021. A decrease of 1.5%.

- Net income of $169 for the three months ended August 31, compared to net income of $252 in the same period in 2021.

- Diluted earnings per ordinary share of $0.34 for the three months ended August 31, compared to $1.97 for the same period in 2021.

- Revenue of $5,448 for the twelve months ended August 31, compared to $5,509 for the same period in 2021. A decrease of 1.1%.

- Net earnings of $764 for the twelve months ended August 31, compared to net earnings of $986 in the same period in 2021.

- Diluted earnings per ordinary share of $1.52 for the twelve months ended August 31, compared to $1.94 for the same period in 2021.

CrowdStrike Holdings, Inc.

All currency listed in thousands of US dollars

Selected highlights from their third quarter 2022 financial results on November 29, 2022

- Revenue of $580,882 for the three months ended October 31, compared to $380,051 for the same period in 2021. An increase of almost 53%.

- Net loss of $54,631 for the three months ended October 31, compared to a net loss of $50,450 in the same period in 2021.

- Diluted loss per ordinary share of $0.24 for the three months ended October 31, compared to a loss of $0.22 for the same period in 2021.

- Revenue of $1,603,869 for the nine months ended October 31, compared to $1,020,584 for the same period in 2021. An increase of 57%.

- Net loss of $133,353 for the nine months ended October 31, compared to a net loss of $190,639 in the same period in 2021.

- Diluted loss per ordinary share of $0.58 for the nine months ended October 31, compared to a loss of $0.85 for the same period in 2021.

TD Bank Group

All currency listed in millions of Canadian dollars

Selected highlights from their fourth quarter 2022 financial results on December 1, 2022

- Revenue of $15,563 for the three months ended October 31, compared to $10,941 for the same period in 2021. An increase of over 42%.

- Net income of $6,564 for the three months ended October 31, compared to net income of $3,718 in the same period in 2021.

- Diluted earnings per ordinary share of $3.62 for the three months ended October 31, compared to $2.04 for the same period in 2021.

- Revenue of $49,032 for the twelve months ended October 31, compared to $42,693 for the same period in 2021. An increase of over 44%.

- Net earnings of $17,170 for the twelve months ended October 31, compared to net earnings of $14,049 in the same period in 2021.

- Diluted earnings per ordinary share of $9.48 for the twelve months ended October 31, compared to $7.73 for the same period in 2021.

Portfolio 2

Portfolio 2 for the week ended December 2, 2022: DOWN ![]()

- The Walt Disney Corporation’s (NYSE:DIS) new CEO Bob Iger said one of his first priorities is for the company to stop chasing subscribers for their streaming services, instead Disney will focus on turning their streaming unit into a profitable business unit.

- TC Energy (TSX:TRP) anticipates additional cost increases as they complete the Coastal GasLink pipeline in British Columbia. The company is experiencing higher costs due to the mountainous terrain as well as growing wages to attract and maintain workers to lay the pipeline.

The Canadian government approved the expansion of TC Energy’s pipeline system in Alberta. This expansion will improve market access for Canadian natural gas. - The Bank of Nova Scotia (TSX:BNS) had a less than stellar fourth quarter earnings report. Worse, it expects earnings for next year to be lower thanks to higher funding costs, expenses, and taxes.

Despite the fourth quarter report, Scotiabank was named Bank of the Year in Canada by The Banker magazine for the fourth consecutive year. It also received The Bankers global award for Banking in the Community. Well done!

- Canadian natural Resources (TSX:CNQ) said it would increase production by 4% in 2023 to capitalize on the higher prices for oil and natural gas. They plan to use increased cash to pay down debt, continue its share buyback program and increase dividends. All three are shareholder friendly. 😊

- iAFinancial Group (TSX:IAG) announced the launch of iA Private Wealth (USA), a registered investment advisor firms that offers cross border wealth management services. Located in Toronto, their Investment Advisors will be dual licensed in Canada and the US to provide solutions that include Canadian registered accounts (RRSP, RIF, TFSA), US non-registered accounts, and US retirement accounts (401k).

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Fortis Inc (TSX:FTS)

US $

No US$ dividends this past week.

Quarterly Reports

Scotiabank

All currency listed in millions of Canadian dollars

Selected highlights from their fourth quarter 2022 financial results on November 29, 2022

- Revenue of $7,626 for the three months ended October 31, compared to $7,687 for the same period in 2021. A decrease of 1%.

- Net income of $2,093 for the three months ended October 31, compared to net income of $2,559 in the same period in 2021.

- Diluted earnings per ordinary share of $1.63 for the three months ended October 31, compared to $1.97 for the same period in 2021.

- Revenue of $31,416 for the twelve months ended October 31, compared to $31,252 for the same period in 2021. An increase of 0.5%.

- Net earnings of $10,174 for the twelve months ended October 31, compared to net earnings of $9,955 in the same period in 2021.

- Diluted earnings per ordinary share of $8.02 for the twelve months ended October 31, compared to $7.70 for the same period in 2021.

Portfolio 3

Portfolio 3 for the week ended December 2, 2022: UP ![]()

- Shopify (TSX:SHOP) reported a record US$ 3.36 billion in global sales by Shopify merchants, a 17% increase in Black Friday sales in 2021. The sales began in New Zealand and ended at the close of Black Friday in California. Sales volume peaked at US$ 3.5 million per minute at 9:01 Pacific Time. That gave a nice little bump to Shopify’s revenues. 😊

- The Royal Bank (TSX:RY) acquired HSBC of Canada, the Canadian arm of Britain’s HSBC Bank, for C$ 13.5 billion in cash. The deal will see the Royal Bank (RBC) add C$ 134 billion of assets to its existing assets, and it will increase the Royal’s client base, both commercial, wealthy clients and newcomers. The deal is expected to close in late 2023, after clearing regulatory hurdles.

RBC raised their quarterly dividend by C$ 0.04 to C$ 1.32. They also announced starting with the February 24, 2023, dividend, investors who are utilizing a Dividend ReInvestment Program (DRIP) to purchase additional Royal Bank shares, rather than taking the cash, will have the option of receiving those shares from RBC’s treasury at a 2% discount from the market price. In the past, shares bought as part of a DRIP were purchased at market price. Investors can opt out of this plan but why would you not take the 2% discount? This is very investor friendly. 😊

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Enghouse Systems Ltd (TSX:ENGH)

Royal Bank of Canada (TSX:RY)

US $

No US$ dividends this past week.

Quarterly Reports

Royal Bank of Canada

All currency listed in millions of Canadian dollars

Selected highlights from their fourth quarter 2022 financial results on November 30, 2022

- Revenue of $12,567 for the three months ended October 31, compared to $12,376 for the same period in 2021. An increase of almost 1.5%.

- Net income of $3,882 for the three months ended October 31, compared to net income of $3,892 in the same period in 2021.

- Diluted earnings per ordinary share of $2.74 for the three months ended October 31, compared to $2.68 for the same period in 2021.

- Revenue of $48,985 for the twelve months ended October 31, compared to $49,693 for the same period in 2021. An increase of almost 1%.

- Net earnings of $15,807 for the twelve months ended October 31, compared to net earnings of $16,050 in the same period in 2021.

- Diluted earnings per ordinary share of $11.06 for the twelve months ended October 31, compared to $11.06 for the same period in 2021.

TD Bank Group

All currency listed in millions of Canadian dollars

Selected highlights from their fourth quarter 2022 financial results on December 1, 2022

- Revenue of $15,563 for the three months ended October 31, compared to $10,941 for the same period in 2021. An increase of over 42%.

- Net income of $6,564 for the three months ended October 31, compared to net income of $3,718 in the same period in 2021.

- Diluted earnings per ordinary share of $3.62 for the three months ended October 31, compared to $2.04 for the same period in 2021.

- Revenue of $49,032 for the twelve months ended October 31, compared to $42,693 for the same period in 2021. An increase of over 44%.

- Net earnings of $17,170 for the twelve months ended October 31, compared to net earnings of $14,049 in the same period in 2021.

- Diluted earnings per ordinary share of $9.48 for the twelve months ended October 31, compared to $7.73 for the same period in 2021.