Items that may only interest or educate me ….

Increased TFSA contribution limit, probability of smaller interest rate increases in Canada and the USA, potential rail system gridlock (again)

Let us start with some good news. The annual contribution limit for Canada’s tax-free savings account (TFSA) is set to rise from C$6,000 to C$6,500 for 2023, the first increase since 2019. This gives each investor an extra C$500 to invest tax free. If you are not already, and are able to, you should maximize your TFSA contributions and invest that money in assets such as stocks, mutual funds, electronically traded funds (ETFs) and other investment opportunities. Ideally you want an asset that will grow faster than the rate of inflation, and just as importantly, also will not cause you to lose any sleep.

More good news for Canadians, the Bank of Canada (BoC) believes the higher interest rate is starting to take hold, slowing the Canadian economy. The benchmark rate (what the BoC lends to banks) is currently 3.75%, its highest since the financial crisis in 2008. Analysts anticipate another 0.25% increase at the BoC meeting on Dec. 7, although a 0.5% is possible. Hopefully, we are at the height of the interest rate hikes in Canada and the question becomes how long the higher rates will stay in place.

Potentially good news as Canada posted a C$1.72 billion budget surplus in the first half of the 2022/23 fiscal year. Since government only has one source of revenue, that means the higher revenues came from all the taxes the government collects from individuals and businesses. This will be good news if the extra money goes to pay down the debt but all governments, especially the current government, likes to spend money our money, so I will not hold my breath.

It was a short week in the US markets as they were closed for American Thanksgiving on Thursday and took the afternoon off on Friday. However, that did not mean there was not good news from south of the border as minutes from the US Federal Reserve Bank’s (Fed) November meeting showed a majority of members agreed it would “likely soon be appropriate” for a smaller interest rate increase. The Fed does not believe their fight with inflation is over but slowing the pace from the past interest rate hikes would allow them to gauge the impact the higher rates are having on the American economy.

The minutes also indicated the members were considering how high the interest rate would have to go and how long it would have to remain at that rate. Some members believed a slower rate of increases could reduce the risk of a recession, while others argued they should keep their foot on the gas until they have concrete data that inflation had significantly receded.

The prospect of a lower rate increase opened the door to the possibility of 0.50% or lower rate hike at their next session in mid December. Naturally, investors seized on this news and pushed the markets modestly higher (and higher is always better 😊).

This rally could backfire as it reflects a belief by investors that the US benchmark interest rate has hit its high point. However, the Fed is still planning to raise rates to slow demand, though maybe not as aggressively as in the past. This rally provides ammunition for those Fed members wanting to maintain their aggressive pace since the Fed wants to see demand and spending going down, and a rising market does not reflect lower demand or spending. While the rally is good for investors, in the long run it may lead to more pain from another aggressive interest hike.

In any event, we will find out which way the Fed is going in a few weeks. In the meantime, analysts and investors will be watching for any data that suggests which way the Fed will go regarding the size of the interest rate hike at their upcoming December meeting. Equally important will be the Fed’s projections for inflation and the likely course of interest rate adjustments in 2023.

Analysts are predicting 2023 will be composed of two phases. The first half of the year will be quite volatile for stock prices as companies adjust their earnings guidance lower to account for falling profit expectations. In the last half of 2023, interest rates should be at their peak, if not drifting downward, and companies will have adjusted their earnings guidance, accordingly, setting the table for a moderate rally to end the year and take us into 2024. We shall see.

One exception to these predictions is Goldman Sachs. They point out that the average cyclical bear market, which we are in, typically lasts 26 months, and stock prices generally take 50 months to return to the previous peak. The current bear market is approaching twelve months so there is still room for the market to fall. While riding out this storm, try to be patient and remember the markets will turn upwards again, hopefully much sooner than later.

If you thought supply chains issues were a thing of the past, think again. Back in September [link to September 16] I mentioned how the US avoided a railroad strike with a last-minute contract between the railway unions and the railway owners. Well, not so fast. That screeching you are hearing is the contract coming to grinding halt, just in time for the Christmas season. So far, four national rail unions have rejected the deal. If a deal does not get done it will cost the US economy up to $2 billion a day because so many businesses and people rely on the rail system for transportation of food, raw materials, components, and end products, not to mention moving people around the USA.

It sounds like both sides are dug in, so it could come down to the US Congress stepping in. If that is the case, the field will tip to the rail system owners’ advantage when the Republicans take control of the House of Representatives in January. Historically, Republicans tend to favour businesses over unions. Let’s hope a deal can be reached to keep this vital piece in the supply chain moving.

Now, with that mostly good news out of the way, lets see how it impacted the week of November 21 – 25. In the words of Daenerys Targaryen, “Let’s begin.”

Weekly Market Review

Monday: I had hoped the week would pick up on the same positive note last week ended on, but it was not to be. Instead, all four major North American Indexes started the same way as the previous Monday – drifting downward.

In Canada, the Toronto Stock Exchange Composite Index (TSX) suffered an early downdraft but was able to battle almost all the way back, ending just in the red. The Energy and Basic Materials sectors that had carried the TSX for most of the year has started to soften in recent weeks, causing the TSX to drift lower. The best performing companies were in the Canadian Consumer Staples and Industrials sectors, while the Technology, Energy and Basic Materials sectors dragged the index down.

In the US, investors were concerned that China may once again implement their strict Covid-19 restrictions to fight a recent breakout. A locked down China could create supply chain problems as China is the home to many manufactured products and components. It would also limit the demand of Chinese consumer market. As with the TSX, the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) all dropped in morning trading but were able to recover some of those losses in the afternoon session. The best performing S&P sectors were the Consumer Staples and Utilities sectors, while Energy and Technology had the worst performance today.

Tuesday: All four indexes rode the rising tide of investor optimism to post solid gains. Investors appear to have turned from high growth companies to companies that provide value and will be able to weather the expected economic downturn in 2023. The price of oil reversed the course of the last few days and ended higher after Saudi Arabia announced OPEC would stick to planned output cuts.

In Canada, higher oil and commodity (natural resources) prices lifted the TSX to its best day in three months. On the TSX, the Canadian Basic Materials (natural resource miners and fertilizer companies), and Energy sectors led the way. Healthcare and Telecommunications Services were the only Canadian sectors that ended slightly lower.

In the US, investors believe the Fed’s upcoming interest rate hike will be smaller than the previous four 0.75% hikes. This optimism has investors wading back into the market, looking for companies well poised for 2023. Higher oil prices also provided a lift to the S&P and DJIA. In the market, it was a broad-based rally for the S&P with the Energy and Basic Materials sectors leading the way.

Wednesday: The markets rejoiced with the release of the Fed’s November meeting minutes, showing the Fed was likely to lower the size of the December rate increase. Investors now believe the December interest rate hike will be 0.5%. The minutes also revealed that November was the first time in 2022 that the Fed the spoke about recession in the US, putting the chances at 50/50.

In Canada, the TSX was buoyed by the good news coming from the Fed’s November minutes. It was a strange mix of Canadian sectors, with the growth-oriented Technology being the best performing sector, followed by the defensive Utilities sector. Energy and Healthcare were the only two Canadian sectors to end lower.

As the Americans prepared for the US Thanksgiving holiday, news from the Fed’s minutes gave investors reason to be optimistic, which in turn spurred the three American indexes higher. The best performing S&P sectors were the growth-oriented Consumer Cyclicals and Technology sectors, while the Energy and Telecommunication Services sectors were the only sectors to slide backward.

Thursday: It was a slow day in the North American stock markets as America was closed for business as they celebrated US Thanksgiving. The only major North American market open for business was the Toronto Stock Exchange. Yesterday’s positive news from the Fed led to investor optimism, pushing the TSX to its highest point since June. The Canadian Technology and Basic Materials sectors were the top performers.

Friday: The American markets half heartedly returned to work, but only for the morning before taking the afternoon off. The day was mixed with the growth-oriented S&P and Nasdaq ending slightly lower, while the more traditional TSX and NYSE both ended slightly higher. The good news from the Fed earlier this week, combined with the good feelings of the season has led to positive sentiment in the market.

For Canada’s TSX, it was another regular day at the office. Expectations of a smaller interest hikes by both the BoC and the Fed helped push the TSX to its fourth consecutive day of gains and its highest close since June. Leading the way were the Canadian defensive sectors Utilities and Telecommunication Services. The only two Canadian sectors to end lower were Basic Materials and Technology.

In the US, if investors were not participating Black Friday sales, they were probably waiting to see how inflation and higher interest rates impacted retailers on the biggest shopping day of the year in America. Those numbers should come out next week. On the trading floor, volume was light with the S&P defensive sectors Utilities and Telecommunication Services performing the best, while the Technology and Basic Materials sectors were the only two sectors to end in the red.

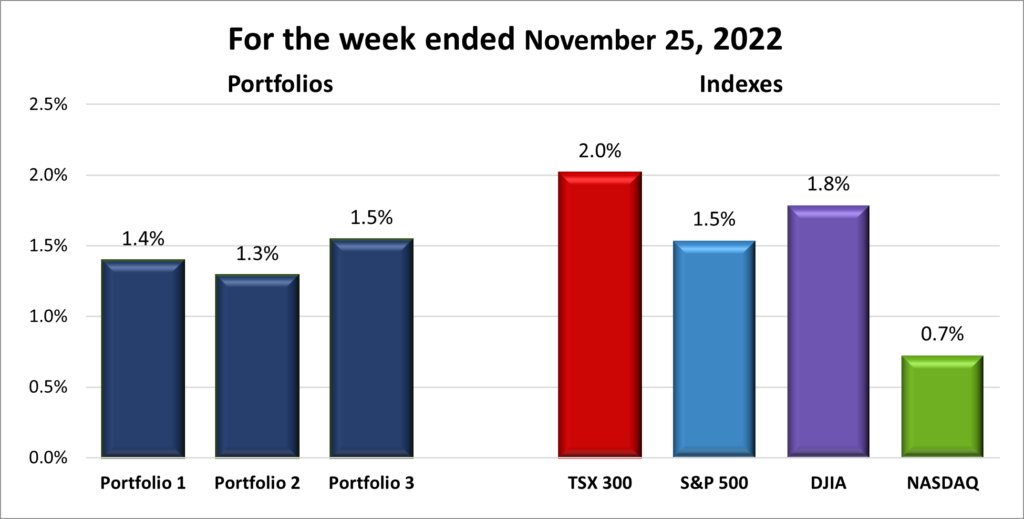

For the week, the TSX (SPTSX) was up 2.0%, the S&P 500 (SPX) gained 1.5%, the DJIA (INDU) rose 1.8% and the Nasdaq (CCMP) climbed 0.7%.

Weekly Portfolio Review

All four indexes – the TSX, S&P, DJIA and Nasdaq – ended higher this week. Mind you, the three American indexes had a week many of us would like to have on a regular basis, a short 3.5-day work week. Perhaps if they had put in the extra time, they could have outperformed the TSX. 😊 One can see that the more traditional blue chip, dividend paying companies found on the TSX and the DJIA are currently in favour with investors. When interest rates are high, the TSX and DJIA tend to perform the best since their share prices tend not to get beaten down as much thanks to their strong Balance Sheets (lots of cash, little debt), and paying dividends doesn’t hurt. 😊

After last week’s losses, I was simply glad to see all three portfolios were back on the positive side for the week. Nothing noticeable stood out other than being lifted by the rising tide of the overall marketplace.

Companies on the Radar

After doing a quick check last week on Restaurant Brands (TSX:QSR) and the Dream REIT (TSX:DIR.UN) to the radar, I determined QSR was priced higher than Morningstar’s Fair Market Value and the current price was higher than analysts’ twelve month price target. With it being considered overpriced with no upside, I will pass on this for now.

As for Dream, you can see it scored a 12 out of 13 on my Radar Check, below. It is considered under priced with almost a projected 25% upside, so it goes to the top of my list.

I’ve added Alphabet (NASD:GOOGL) back to the list because I believe this will continue to be the dominant search company for the next few years at least. Five years from now I think buying additional shares while it is on sale will have been a very good move. 😊

My Radar list is now comprised of Crew Energy (TSX:CR), Dream REIT, International Petroleum (TSX:IPCO) Alvopetro Energy (TSXV:ALV) and Alphabet.

- Dream REIT: income generating Canadian industrial property operator, with properties across North America and Europe.

- Crew Energy: a Canadian oil and gas company with interests in British Columbia.

- International Petroleum: a Canadian company with oil and gas assets in Canada, Malaysia, and France.

- Alvopetro Energy: a Canadian natural gas company developing natural gas projects in Brazil.

- Alphabet: leading online search engine and advertising company, dominant mobile operating system.

Below are my Radar Checks on these companies, updated November 25, 2022.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended November 25, 2022: UP ![]()

- GM’s (NYSE:GM) Cruise unit expanded its autonomous ride-hail service to daytime hours in most of San Francisco. the company has eighty cars in San Francisco, with plans to scale to a fleet of one million vehicles by 2030

- Britain’s Competition and Markets Authority (CMA) announced they would perform an in depth investigation of both Apple (NASD:AAPL) and Alphabet’s Google dominant mobile operating systems (iOS and Android). The CMA said they hoped to improve competition and innovation in the mobile platform industry.

- Amazon (NASD:AMZN) plans to spend more than $1 billion a year to produce movies for release in actual theaters. This could be a huge blackhole for revenue generated by Amazon’s e-commerce business and their AWS cloud services units.

- Poland’s government regulator is looking into PayPal’s (NASD:PYPL) self proclaimed rights to impose penalties, ranging from blocking accounts to imposing financial penalties to terminating accounts, if a user violated certain provisions of their contract. The regulator said the description of the prohibited activities are unclear and could cause users to go astray unknowingly.

- Tesla’s (NASD:TSLA) existing ‘Autopilot’ feature allows their vehicles to autonomously steer, accelerate and brake. This past week Tesla released the latest Beta version of its Full Self-Driving software to the public. The US$ 15,000 software add-on provides their cars with the ability to change lanes and park. For those not familiar with the Beta designation, it refers to software that is still being tested to eliminate any problems with the software. Tesla is still waiting regulatory approval to be able to designate their vehicles as self driving. If I were a regulator, I would be very reluctant to approve anything that was in Beta mode.

Tesla is recalling over 80,000 of their electric vehicles In China. Chinese regulators identified problems with the seatbelts and the battery management system. The battery system is a software upgrade while Tesla will have to check the seatbelts of all recalled cars and reinstall them if necessary. The recall cover vehicles made in China as well as imports, dating back as far as 2013.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Pulse Seismic Inc (TSX:PSD)

TMX Group Ltd (TSX:X)

Quinsam Capital Corp (TSX:QCA)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended November 25, 2022: UP ![]()

- On Sunday November 20, Disney (NYSE:DIS) brought former CEO Bob Iger out of retirement to replace his successor Bob Chapek, who had been CEO since 2020. Mr. Iger had been with Disney for over 40 years, including the last fifteen as CEO before stepping down. During his tenure as CEO, Disney acquired Pixar Animation Studios, Marvel Entertainment and 21st Century Fox, to name a few. He will lead Disney for the next two year and has been charged with setting “the strategic direction for renewed growth and to work closely with the Board in developing a successor to lead the Company at the completion of his term.”

Disney shares were down over 40% in 2022 so I can see why the Disney Board of Directors were not happy with Disney’s performance under Mr. Chapek. Apparently, investors approved of this move as Disney shares jumped almost 10% Monday morning from their Friday closing price.

After shutting down on October 31 due to China’s strict Covid-19 restrictions, Disney’s Shanghai Resort theme park re-opened November 25. - Microsoft’s (NASD:MSFT) deal to acquire Activision Blizzard sounds like it will be opposed by the US Federal Trade Commission.

- Alimentation Couche-Tard Inc. (TSX:ATD) reported a strong second quarter, mostly thanks to higher fuel prices. With the extra money the company bought back shares during the last quarter and raised its quarterly dividend by 27% to $0.14 per share. Both are good for investors.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX:DIR.UN)

US $

No US$ dividends this past week.

Quarterly Reports

Alimentation Couche-Tard Inc

All currency listed in millions of US dollars

Selected highlights from their second quarter 2023 financial results on November 22, 2023

- Revenue of $16,879.5 for the 12 weeks ended October 9, 2022, compared to $14,219.7 for 12 weeks ended October 10, 2021. An increase of almost 19%.

- Net income of $810.4 for the 12 weeks ended October 9, 2022, compared to net income of $694.8 for 12 weeks ended October 10, 2021.

- Diluted earnings per ordinary share of $0.79 for the 12 weeks ended October 9, 2022, compared to $0.65 for 12 weeks ended October 10, 2021.

- Revenue of $35,537.2 for the 24 weeks ended October 9, compared to $4,126.3 for the 24 weeks ended October 10, 2021. An increase of almost 28%.

- Net earnings of $1,682.8 for the 24 weeks ended October 9, compared to net earnings of $1,459.2 for the 24 weeks ended October 10, 2021.

- Diluted earnings per ordinary share of $1.64 for the 24 weeks ended October 9, compared to $1.36 for the 24 weeks ended October 10, 2021.

Portfolio 3

Portfolio 3 for the week ended November 25, 2022: UP ![]()

- Brookfield Asset Management (TSX:BAM.A) and its Australian partner State Super (one of Australia’s largest pension funds) are selling Geelongport to US investment group Stonepeak and Australia’s Spirit Super (a money management company) for an estimated A$1.1 billion. Geelongport is the second largest port in the state of Victoria, Australia, handling two million tonnes of cargo and 600 vessel visits per year.

Brookfield announced all material approvals for the spin-off of their asset management unit (the ‘Manager’) have been received and the shares are expected to be distributed to shareholders of Brookfield on December 9. - The Royal Bank (TSX:RY) and TD Bank (TSX:TD) are the only Canadian banks among the 30 globally systemically important banks (G-SIBs). I never knew such a thing existed. Turns out being designated a G-SIB has higher capital requirements, additional compliance costs and regulatory scrutiny. I do not see any benefit for the Royal or TD to be on the list other than to show they are big banks, but it is good to know they are among the biggest, most stable banks in the world.

- Cloudflare (NYSE:NET) was recently recognized as number 55 in the Top 100 Most Loved Workplaces in 2022. Cloudflare’s mission is to build a better Internet appears to have rubbed off on its work environment.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.