Items that may only interest or educate me ….

No Santa rally, January effect …

First, lets start off by saying good riddance to 2022 and a big welcome to 2023!

So much for a Santa Claus rally to end 2022 on a positive note.  Rather than the hoped for year end rally, the Grinch appeared in its place. Concerns about inflation, rising interest rates, and the possibility of a recession squashed hopes for upward momentum as we head into 2023. Instead of a happy ending like in the cartoon where the Grinch’s heart grows in size, the Grinch put an exclamation mark on his handiwork with a down day to end another down week, in a down month in the worst year for the markets since 2008. Let us hope the Grinch’s heart grows three sizes in 2023 and the market triples in the next few years, starting with ….… the January effect.

Rather than the hoped for year end rally, the Grinch appeared in its place. Concerns about inflation, rising interest rates, and the possibility of a recession squashed hopes for upward momentum as we head into 2023. Instead of a happy ending like in the cartoon where the Grinch’s heart grows in size, the Grinch put an exclamation mark on his handiwork with a down day to end another down week, in a down month in the worst year for the markets since 2008. Let us hope the Grinch’s heart grows three sizes in 2023 and the market triples in the next few years, starting with ….… the January effect.

Similar to the Santa Claus rally is the January Effect. Many investors believe the markets perform better in January than the other months, especially the first five trading days.

There are a number of possible explanations for a January Effect including: investors selling their losers in December for tax purposes and are now looking to put their money back into the market; thanks to December selling, share prices have fallen and shares look more attractive; investors have more cash available thanks to corporate bonuses; and people in general tend to be in an upbeat mood coming out of the holiday season. No matter what the reason, they all result in increased buying which pushes share prices higher.

Unfortunately, the January Effect has lost its lustre over the years. As more investors become aware of the supposed January bump, the more people will try to take advantage of it, effectively nullifying whatever dip in share prices there may have been. Add online trading investors to the mix and the January Effect has all but disappeared.

In a sense, the January Effect is a lot like Black Friday, Cyber Monday, and Boxing Day sales. While there are lots of great sales, people tend to get caught up in the buying frenzy, especially if its instore shopping, and feel they must buy something even if what they came for is unavailable.

Since I got back into investing in 2017, the only time I experienced the January Effect was in 2019. Otherwise, I have not experienced another January rally, even in red hot 2021 the markets did not take off until February. Each year I try to keep cash available in the event there is a January Effect. However, I still maintain my strategy of buying great companies with the intent of holding them for the long term.

Now that 2022 year-end has arrived, there will plenty of people claiming how well their portfolio performed in 2022. Take it with a grain of salt. This is especially important in a bearish year like 2022 when the vast majority of investors saw the bottom fall out of their portfolios. Some may be tempted to embellish their results, especially on social media, financial management sites, and elsewhere on the internet. If you are considering paying money for someone to manage your investment or provide advice, try to find out if the results they claim to have achieved have been professionally audited.

Before we call it a wrap for 2023, let’s take a look at how the last week of the year unfolded for the markets and the Portfolios.

Weekly Market Review

Monday: The four major North American indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – were closed for the Christmas holiday.

Tuesday: In Canada, the TSX was closed for the Boxing Day holiday. In the US, it was a mixed bag with the interest sensitive growth technology stocks that dominate the Nasdaq, and to a lesser extent the S&P, ending lower. The lone bright spot was the DJIA, which was held up by the value-oriented companies in the index. In trading, the S&P Energy and Telecommunications Services sectors climbed the most, while the interest sensitive Consumer Cyclicals and Technology sectors had the greatest declines.

Wednesday: I saw a headline from an investing newsletter that said the markets looked set to rise today. Were they wrong! All four indexes plunged in morning trading, followed by a brief lunchtime rally before drifting downward again. Concerns about a surge in Covid-19 cases in China, negative market sentiment, a reluctance to take on risk and lighter trading volumes all contributed to the market’s downward movement.

In Canada, concern over rising Covid cases in China caused oil prices to fall (less work and travel being done mean less need for oil), resulting in many Energy companies ending the day lower. All the Canadian sectors ended lower today. The Consumer Cyclical and Utilities sectors fell the least, while the Energy and Healthcare sectors lost the most.

In the US, slightly over a year ago the Nasdaq hit an all time high. Fast forward to today, the Nasdaq hit a 2022 closing low as investors continued to have concerns about mixed signals after recent economic data, leading to a broad-based decline across all S&P sectors. The Healthcare and Financials sectors dropped the least, while the Energy and Basic Materials (miners and fertilizer manufacturers) fell the most.

Thursday: After Wednesday’s sell off it was good to see all four indexes rebound with solid performances. Each index finished at least 1% higher, with the Nasdaq gaining more than 2%. The main spark for the rally was higher US jobless numbers, indicating the US labour market may finally be cooling off.

In Canada, The Canadian Technology and Healthcare sectors led the way upward. The Consumer Staples sector was the only Canadian sector to slide backward today.

In the US, the growth sectors enjoyed a resurgence. It seems any time there is a hint inflation or interest rates are falling sends investors back into the arms of growth companies, particularly technology companies. It was a complete reversal from Wednesday for the American S&P sectors, with all eleven ending in the black. Leading the way were the Technology and Consumer Cyclical Sectors, with Consumer Staples advancing the least.

Friday: Today pretty much exemplifies 2022 – down. It turns out Thursday was just a one-day speed bump on a downhill road as all four major North American indexes ended the day, week, month, and year lower. The only bright spot was oil ended higher, pushing energy companies’ shares higher.

In Canada, the TSX recorded its first annual drop since 2018 (lets hope drops do not become an annual thing 😊). On the last day of the year for the markets, the TSX had only three Canadian sectors end the day in the black – the Telecommunications Services, Healthcare and Energy sectors. The biggest drops were had by the Utilities and Financials sectors.

In the US, the rapid increase of interest rates has led the S&P, DJIA and Nasdaq to break their three-year winning streak of yearly gains. In trading, only the American S&P Energy and Telecommunications Services sectors ended higher. The biggest losers were the Utilities, and Basic Materials sectors.

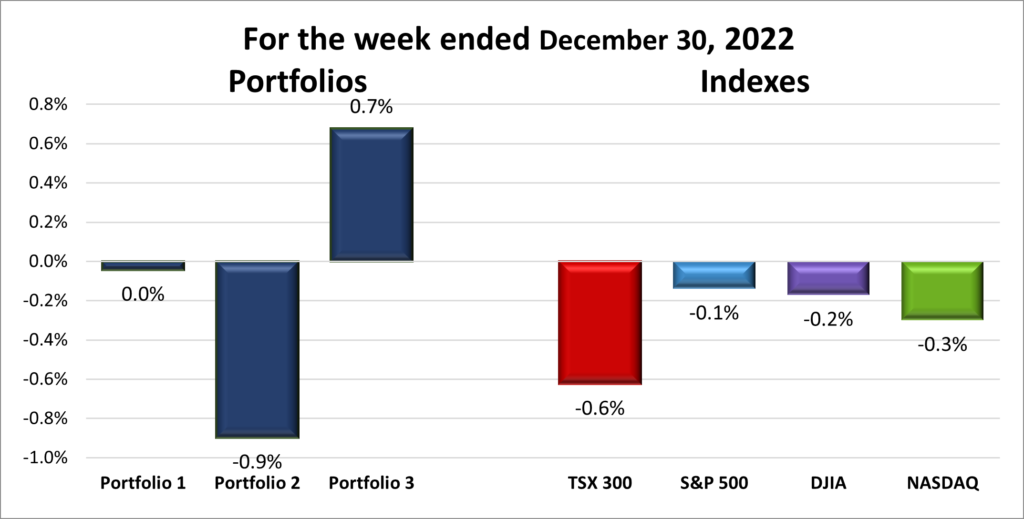

For the week, the TSX dropped 0.37%, the S&P 500 declined 0.1%, the Dow fell 0.2% and the Nasdaq sank 0.3%.

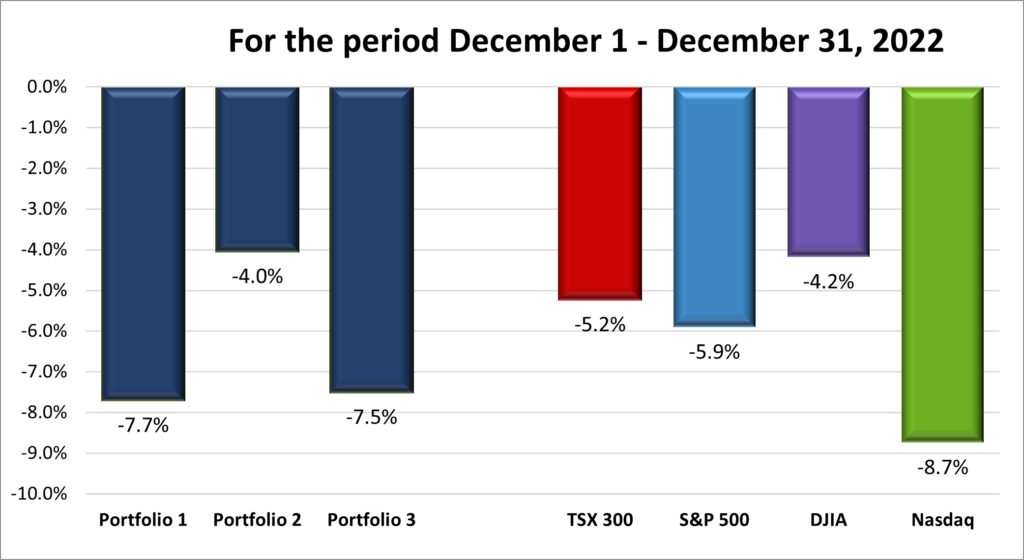

For the month, the TSX sank 5.2%, the S&P 500 dropped 5.9%, the Dow fell 4.2% and the Nasdaq plunged 8.7%.

Weekly Portfolio Review

I had hoped the week would go out on a winning note, but as you can see below, it was not to be. With many of the professional traders and institutional investors enjoying time off before getting back to business in the new year, the field was left to us retail investors. Trading volumes were down and on-going concerns about inflation, interest rates and the possibility of a recession did not give investors any reason to jump into the market this week. All four indexes ended lower, with the TSX dropping the most as the price of oil did not turn upward until the end of the week. Since the Energy sector accounts for 19% of the TSX, falling oil prices weighed on the index. As for the three American indexes, the reasons previously mentioned were probably why they ended lower.

For the portfolios, I was surprised to see Portfolio 3 gained 0.7%. Most of the technology companies in the portfolio ended the week higher which would have lifted the portfolio. The other surprise was Portfolio 2 which fell almost 1%. No big loser but the result of numerous smaller losses added up to Portfolio 2 ending the week lower. Portfolio 1 did not gain any ground but not losing money is the next best thing to gaining money. 😊

There was no Santa Claus rally this year. ☹ The winning streak for monthly returns came to a crashing end in December. After two months of strong monthly gains, all four indexes plunged lower in December. The US interest rate hike and ominous comments from the US Federal Reserve at the start of the month sent the markets in a tailspin and there was not much good news to overcome the downward momentum. The interest sensitive Nasdaq and S&P companies bore the brunt of the pain, with the Nasdaq giving back the gains it had made in the previous two months. Although the TSX and DJIA are not populated with trendy, interest sensitive, growth companies like the Nasdaq and S&P, they were still dragged lower by economic concerns and overall negative market sentiment.

Unfortunately, the three Portfolios tend to mirror the indexes and December was no exception (this past week is the only time I remember a Portfolio advancing when all four indexes declined). The only bright spot (if it can be called a bright spot) was the Portfolios ended like I thought they would. The riskier Portfolios 1 and 3 dropped the most while the more balanced Portfolio 2 fell the least. It seemed for the last few months Portfolio 2 was performing the worst no matter what the markets did so its good see that over time it will not fall as hard as the other two portfolios. I know being the best of a bad lot is not a great achievement, but I am trying to take something positive out of the December results. 😊

That was not how I had hoped December would play out but its over, as is 2022. I hope the bears of 2022 go back into hibernation in 2023, and by the end of the year the bulls once again dominant the stock market field.

Companies on the Radar

A short and quiet week, with no companies coming on the radar to join the four companies listed below.

- Crew Energy (TSX:CR): A Canadian oil and gas company with interests in British Columbia.

- Alvopetro Energy (TSXV:ALV): A Canadian natural gas company developing natural gas projects in Brazil.

- International Petroleum (TSX:IPCO): A Canadian company with oil and gas assets in Canada, Malaysia, and France.

- Alphabet (NASD:GOOGL): The leading online search engine and advertising company, dominant mobile operating system.

The Radar Check was last updated December 30, 2022.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended December 30, 2022: DOWN ![]()

- Tesla (NASD:TSLA) fell out of the S&P’s Top 10 Index this week. Lower output in China, discounts to US consumers, and a CEO who lost his focus.

- Canada’s Competition Tribunal has given the green light to Rogers Communications’ (TSX:RCI.B) to acquire Shaw Communications (TSX:SJR.B). The Commissioner of Competition opposed the merger, arguing the merger would cause “materially higher prices” for consumers in Western Canada. The Commissioner of Competition has appealed this decision, so the process goes on. If/once the merger of Rogers and Shaw goes through there will be one less national telecom provider. If prices were already considered high, I do not see how less competition will improve service and pricing.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Canadian National Railway Co (TSX:CNR)

Shaw Communications Inc (TSX:SJR.B)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended December 30, 2022: DOWN ![]()

- Some good news for Disney (NYSE:DIS). Imax Corporation (NYSE:IMAX) announced Disney’s latest blockbuster ‘Avatar: The Way of Water’ pulled in over US$ 105 million globally from Imax theatres in the first two weeks. The movie became the highest grossing Imax release of all time in several international markets.

- TC Energy (TSX:TRP) put its Keystone pipeline back in operation this week. The company completed repairs, passed the testing of the repaired section, and received the necessary approvals.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX:DIR.UN) DRIP

Brookfield Infrastructure Partners LP (TSX:BIP.UN)

Brookfield Infrastructure Corp (TSX:BIPC)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended December 30, 2022: UP ![]()

- If the Microsoft (NASD:MSFT) deal to acquire Activision Blizzard (NASD:ATVI) goes through, Microsoft will find itself dealing with unions. Employees at Activision’s Proletariat studio in Boston voted to join the Communications Workers of America union. This would be the third Activision studio to unionize, joining studios in Albany, NY, and Wisconsin.

The Federal Trade Commission’s antitrust case against Microsoft over their acquisition of Activision Blizzard is set to begin January 3, 2023, with the first pretrial hearing. The Commission argues the deal would give Microsoft Xbox exclusive access to popular Activision games, to the detriment of rivals. Microsoft is arguing the deal is good for gamers and companies. They have even offered a legally binding agreement to provide their competitors with access to the Activision games.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Brookfield Renewable Corp (TSX:BEPC)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.