Hawk or Dove? The Fed’s Next Chapter

For many investors, the US Federal Reserve – better known simply as “the Fed” – can feel like this mysterious force that “moves markets,” and somehow influences everything from stock markets and mortgages to inflation and the broader economy. In reality, it does. Because Canada’s economy and markets are tightly linked to the US, Fed decisions often ripple north of the border through the Canadian dollar, borrowing costs, commodities, and investor sentiment. As the central bank of the world’s largest economy and reserve currency, the Fed plays a major role in shaping global financial conditions.

Created in 1913 after a series of banking panics, the Fed’s role evolved into a dual mandate: keeping inflation under control while supporting maximum employment. In simple terms, it’s constantly trying to balance price stability with economic growth – a difficult line to walk in any cycle.

Over time, Fed Chairs have become closely tied to defining entire economic eras. Paul Volcker crushed runaway inflation in the early 1980s, when US inflation peaked above 14% (and over 20% in Canada), but at the cost of a deep recession. Alan Greenspan oversaw the long 1990s expansion and the buildup to “irrational exuberance,” while Ben Bernanke guided the Fed through the 2008 financial crisis with unprecedented emergency support.

Now, another era has ended. Jerome Powell’s term has ended after one of the most difficult stretches in modern Fed history. He inherited a stable, low-inflation economy and was quickly hit with COVID, massive stimulus, supply chain shocks, regional bank stress, and the highest inflation in roughly 40 years. The result was one of the fastest interest-rate hiking cycles in decades as the Fed tried to restore price stability without triggering a deep recession.

His tenure also came under repeated political pressure from Donald Trump, who publicly pushed for lower interest rates to support growth and markets – a reminder of how important Fed independence is, even under intense scrutiny.

With Powell’s term ending on May 15, Kevin Warsh has now taken over as Fed Chair. He’s not new to central banking, having served during the 2008 financial crisis and worked closely with policymakers through one of the most volatile periods in modern finance. He also brings Wall Street experience, giving him a mix of market and policy perspective.

Earlier in his career, Warsh was seen as strongly focused on inflation control. More recently, however, he has been more critical of keeping rates high for too long – a stance that aligns with broader concerns about slowing growth and echoes Trump’s long-standing calls for lower rates. That shift is part of why his appointment has drawn attention, as investors try to figure out where his real priority will sit: inflation discipline or economic support.

For us investors, the stakes are simple. Interest rates shape everything – from mortgages and consumer spending to corporate profits and equity valuations. A more growth-friendly Fed could support markets, while a more cautious, inflation-first approach could keep financial conditions tighter for longer. Much will depend on the economic backdrop Warsh inherits over the coming quarters.

Every Fed Chair is ultimately defined by their era. Volcker fought inflation. Bernanke fought a financial crisis. Powell fought a pandemic, inflation shock, and tremendous political pressure. The question now is will Kevin Warsh be a hawk or a dove – and what defining challenge will shape his time at the helm of the world’s most influential central bank.

With that in mind, let’s take a step back and look at how markets – and my three portfolios – reacted in Warsh’s first week, along with Nvidia’s (NASDAQ: NVDA) much-anticipated earnings.

Items that may only interest or educate me ….

Canadian Economic News, US Economic News, ….

Canadian Economic News

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Consumer Price Index (CPI)

Statistics Canada’s April inflation report showed prices rising 0.4% month-over-month, a slowdown from March’s 0.9% increase. On an annual basis, inflation rose to 2.8% from 2.4%, marking the highest reading since May 2024, though still below the 3.1% expected.

The main driver was energy. Oil prices jumped following geopolitical tensions in the Middle East, pushing gasoline up 8.9% in April alone – the largest monthly gain across all categories – and nearly 29% higher than a year ago. That surge fed directly into transportation costs and lifted the headline number.

Outside of energy, inflation pressures stayed fairly contained. Recreation, education, and reading costs fell 1.7%, while household operations, furnishings, and equipment had the mildest price gains of any category, up just 0.4%. Shelter costs continued their slow grind higher, up 0.1% in April and 1.8% year-over-year.

Core inflation, which strips out food and energy and is closely watched by the BoC, remained subdued. It rose 0.1% month-over-month, matching March, while the annual rate eased to 1.5% from 1.9%. That suggests underlying price pressures continue to cool even as headline inflation picks up.

For us investors, that distinction matters. With core inflation softening, expectations for additional BoC tightening eased slightly after the report.

Overall, the data still points to an oil-driven inflation bump rather than a broad-based reacceleration. That gives the BoC room to remain patient rather than rushing into further rate hikes.

Retail Sales

Canada’s latest retail sales report from Statistics Canada showed that consumer spending is still holding up, even if the momentum is a bit uneven month to month.

In March, retail sales rose 0.9%, ahead of expectations for a 0.6% gain and slightly stronger than February’s 0.7% increase. On a year-over-year basis, sales were up 3.4%, a touch softer than the 3.8% pace the month before. Overall, the picture remains one of steady growth rather than a clear acceleration or slowdown.

Looking deeper, the gains weren’t evenly distributed. Sales rose in four out of nine subsectors, suggesting spending is still active but concentrated in a few key areas. The biggest driver was gas stations and fuel vendors, where sales jumped 12.4% on higher fuel prices. In contrast, building material and garden supply stores fell 2.9%, pointing to softer demand in parts of the housing-related space.

Over a longer horizon, the same divide stands out. Energy-related spending has been a major contributor, with gas station sales up 15.8% year-over-year, while categories like furniture, electronics, and home furnishings are down about 8%. That gap highlights how uneven consumer spending has become across the economy.

A big part of this comes down to fuel prices. Higher energy costs, driven by the Iran war and global supply disruptions, have lifted spending at the pump. While that boosts headline retail sales, it doesn’t necessarily reflect stronger consumer strength – it mainly means more of the household budget is being directed toward essentials like gasoline.

That shift matters because every extra dollar spent on fuel is a dollar not going elsewhere. It helps explain why some categories are still growing while discretionary areas are still under pressure.

To smooth out that noise, economists often look at core retail sales, which exclude gasoline, motor vehicles, and parts. On that measure, sales slipped 0.1% in March after a 0.6% gain in February, suggesting underlying demand is softer than the headline figure implies.

Overall, the Canadian consumer is still active, but more selective. Spending on essentials is holding up, while higher prices and borrowing costs are shaping where money gets spent. Growth is still intact but increasingly concentrated in a smaller number of categories.

Canadian Market Volatility

Canada’s version of the market “fear gauge” is the S&P/TSX 60 VIX Index (VIXC), often shown on trading platforms as VIXI.TO. Like the better-known CBOE Volatility Index in the US, it measures expected volatility in the Canadian stock market over the next 30 days.

The VIXC opened the week at 15.72, slightly above the previous week’s close of 15.50 as inflation concerns created some early caution. However, with few major surprises during the week, volatility steadily faded and the index eventually closed at 15.52.

Overall, the decline suggests investors became more comfortable with the broader market backdrop as geopolitical tensions appear to cool and oil prices hold steady. It also highlights one of the key differences between Canadian and US markets. Canada’s market is more heavily weighted toward sectors like financials, energy, and mining, which tend to produce steadier market movements than the more technology-heavy US indexes, where volatility can swing much more sharply.

US Economic News

This past week’s key data points that the Fed considers when deciding whether to raise or lower the interest rate.

Consumer Sentiment Index (CSI)

The University of Michigan’s final reading of consumer sentiment fell to 44.8 in May, down sharply from April’s 49.8 and well below expectations for 48.2. That marked the third straight monthly decline and pushed consumer confidence to its lowest level since the survey began in the 1950s.

Looking beneath the surface, the weakness was widespread. The Current Economic Conditions Index – which reflects how consumers feel about their finances and job security today – fell to 45.8, down 12.8% from April and more than 22% lower than a year ago. Meanwhile, the Expectations Index, which measures how consumers feel about the economy over the next six months, dropped to 44.1, down 8.3% month over month and 7.9% from May 2025.

The biggest issue weighing on sentiment was inflation, particularly rising gasoline and energy prices tied to ongoing tensions in the Middle East and disruptions around the Strait of Hormuz. Lower-income households appeared especially concerned, as higher fuel and food costs tend to hit those consumers the hardest.

For us investors, the report sent mixed signals. Weak consumer sentiment can point to slower economic growth ahead, since consumers often cut back spending when confidence falls. At the same time, softer economic sentiment can sometimes reduce pressure on the Fed to keep interest rates elevated if the economy begins cooling. For now, the key is whether this weakness remains mostly tied to energy prices and geopolitics, or if it starts spreading more broadly across the economy.

American Market Volatility

The VIX, often called the market’s “fear gauge,” measures how much volatility investors expect in the S&P 500 over the next 30 days. In simple terms, it reflects how much uncertainty traders are pricing into the market. The VIX typically rises when fear increases and falls when investors become more confident. Readings above 20 are often associated with elevated market stress, and throughout this past week the index remained below that level, suggesting investors stayed relatively calm despite ongoing geopolitical tensions.

The VIX opened the week at 18.01 as investors reacted to inflation concerns and uncertainty surrounding interest rates. However, the index gradually drifted lower throughout the week, eventually closing at 16.70. Cooling tensions in the Middle East helped ease some market anxiety, but strong corporate earnings – particularly from major technology companies – also reassured investors that the broader economy and profit outlook remained resilient. Hopes that oil prices and inflation may continue easing over the coming months further supported investor sentiment and reduced fears of a larger market pullback.

Weekly Market and Portfolio Review

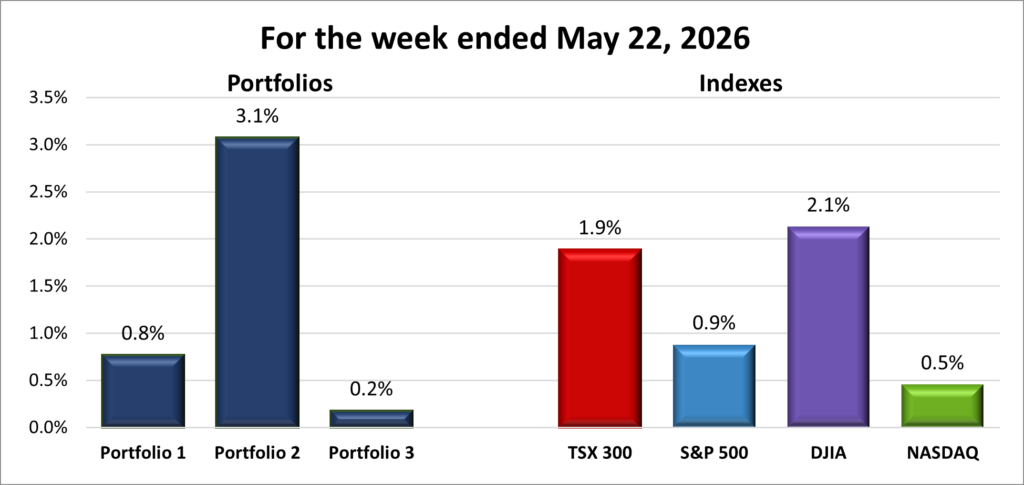

For the week, the TSX (SPTSX) advanced 1.9%, the S&P 500 (SPX) rose 0.9%, the DJIA (INDU) jumped 2.1% and the Nasdaq (CCMP) added 0.5%.

| Index | Weekly Streak |

| TSX: | 1 – week winning streak |

| S&P: | 8 – week winning streak |

| DJIA: | 1 – week winning streak |

| Nasdaq: | 1 – week winning streak |

![]() The week started on a softer note, with mixed performance across the major indexes. The Dow Jones Industrial Average (DJIA) was the only index to post a gain on the opening day, but by the following session it had joined the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), and the Nasdaq Composite Index (Nasdaq) in negative territory.

The week started on a softer note, with mixed performance across the major indexes. The Dow Jones Industrial Average (DJIA) was the only index to post a gain on the opening day, but by the following session it had joined the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), and the Nasdaq Composite Index (Nasdaq) in negative territory.

Sentiment then improved steadily, helped in part by reports of progress in US-Iran peace talks, which eased concerns around energy supply risks. Markets went on to post three straight days of gains, with the DJIA setting back-to-back record highs to close the week. The S&P 500 extended its winning streak to eight weeks, its longest stretch since 2023, while the other major indexes also returned to positive territory.

Behind the scenes, markets were driven by a mix of inflation concerns, geopolitical developments, and another major round of AI-driven earnings.

Early in the week, rising oil prices and hotter-than-expected inflation data pushed US Treasury yields higher, reviving concerns that interest rates may need to stay elevated for longer. Higher yields tend to weigh most heavily on technology and other growth sectors because their valuations are more dependent on future earnings. As a result, the Nasdaq came under the most pressure early in the week, while the more defensive DJIA held up relatively better.

Geopolitical tensions added another layer of volatility. Concerns around Middle East supply disruptions initially pushed crude prices higher, reinforcing inflation fears. However, as tensions eased later in the week, oil prices pulled back, helping calm markets.

Even if the conflict were to end, it would likely take several weeks for shipping backlogs in the Strait of Hormuz to clear and for oil production across parts of the Middle East to fully ramp back up. In other words, supply does not return to normal overnight, which helps explain why oil markets can remain volatile even as headlines improve.

As pressure from inflation and interest rates eased into the back half of the week, investor attention shifted back toward earnings and whether corporate profits were still holding up.

All eyes were on Nvidia’s results as investors looked for confirmation that the AI-driven growth story is still intact. The company once again delivered strong results, yet expectations were so high they failed to move investors. Even so, enthusiasm around artificial intelligence (AI) remained strong, with continued momentum across the technology sector. Outside of technology, earnings were also generally solid, with several companies across different sectors beating expectations, helping support broader market sentiment.

At the same time, not all signals were encouraging. Consumer sentiment data released at the end of the week showed Americans are feeling even worse about the economy, highlighting how many households are still struggling with higher prices and borrowing costs despite continued strength in parts of the market and economy.

And if investors didn’t already have enough to process, Kevin Warsh was sworn in as Federal Reserve Chair on Friday, adding another layer of uncertainty around the future direction of interest rates.

In Canada, the shortened trading week followed a similar path, shaped largely by the same global forces rather than anything uniquely domestic. With its heavier weighting toward energy, the TSX largely tracked the same swings in oil prices, although inflation expectations, and US earnings sentiment played a role.

Energy was a key driver throughout the week. Rising oil prices initially supported Canadian energy stocks, but as Middle East tensions eased and crude prices pulled back, some of that strength faded.

Interest rates also played an important role. Stronger inflation signals in the US weighed on Canadian markets early in the week, particularly rate-sensitive areas like technology and consumer cyclicals. When oil prices pulled back, sentiment improved and helped support a broader rebound.

Finally, optimism around American AI companies also helped support Canadian technology names. Even though the TSX is less tech-heavy than the Nasdaq, strength in global technology companies, particularly those tied to AI infrastructure, still tends to spill over into Canada through improved investor confidence.

Overall, both markets followed a similar pattern this week, moving lower early on amid inflation and interest rate concerns before recovering as oil prices eased, earnings remained resilient, and optimism around AI and US-Iran peace talks improved sentiment.

| Portfolio | Weekly Streak |

| Portfolio 1: | 3 – week winning streak |

| Portfolio 2: | 8 – week winning streak |

| Portfolio 3: | 3 – week winning streak |

![]() The way the week started, I thought fears around inflation and rising oil prices might finally bring an end to my portfolios’ winning streaks. Instead, reports of progress in US-Iran peace talks lifted investor optimism and pushed oil prices lower, easing some inflation concerns. At the same time, Nvidia’s earnings reinforced that the AI gold rush still has legs, helping investors move back into AI stocks and the broader markets. Higher oil prices supported my portfolios early in the week, but improving sentiment and renewed AI enthusiasm ultimately carried all three portfolios higher into the close, extending each winning streak. 😊

The way the week started, I thought fears around inflation and rising oil prices might finally bring an end to my portfolios’ winning streaks. Instead, reports of progress in US-Iran peace talks lifted investor optimism and pushed oil prices lower, easing some inflation concerns. At the same time, Nvidia’s earnings reinforced that the AI gold rush still has legs, helping investors move back into AI stocks and the broader markets. Higher oil prices supported my portfolios early in the week, but improving sentiment and renewed AI enthusiasm ultimately carried all three portfolios higher into the close, extending each winning streak. 😊

Despite beating revenue and earnings expectations, forecasting stronger-than-expected revenue next quarter, and announcing an $80 billion share buyback, investors still seemed underwhelmed by Nvidia’s results, with the stock finishing down 2% for the week. At this point, I’m starting to wonder if investors will ever truly be satisfied with Nvidia’s earnings reports and forecasts. 😊

Portfolio 1 gained 0.8% this week, supported by broad strength across the portfolio, with 70% of holdings finishing higher. One of the biggest contributors was Navitas Semiconductor (NASDAQ: NVTS), which surged 35% as investors continued piling into companies tied to higher-voltage, energy-efficient chips that are part of the AI power infrastructures. Also posting strong gains were Lattice Semiconductor (NASDAQ: LSCC), which climbed 17% while setting multiple record highs, CrowdStrike (NASDAQ: CRWD), which gained 12% and also reached a new high, and Cloudflare (NYSE: NET), which advanced 11%. Other companies hitting record highs during the week included Datadog (NASDAQ: DDOG), Alphabet (NASDAQ: GOOGL), and Bank of Nova Scotia (TSE: BNS).

Portfolio 2 was the surprise performer this week, gaining 3.1% and outperforming both my other portfolios and all four major indexes. Since it is typically the more balanced and conservative of the three portfolios, it does not usually lead during strong market rallies, which made this week’s performance stand out even more. Gains were widespread, with 79% of holdings advancing as the portfolio extended its winning streak to eight straight weeks. Leading the way were Birkenstock (NYSE: BIRK), which jumped 31%, Guardant Health (NASDAQ: GH), up 23%, and Mitek Systems (NASDAQ: MITK), which gained 13%. South Bow (TSE: SOBO), Bank of Nova Scotia, and TC Energy (TSE: TRP) also reached record highs during the week.

Portfolio 3 lagged behind the other two portfolios but still posted a 0.2% gain this week (even a small gain is better than a loss 😊). It also had the fewest weekly winners, with 62% of holdings advancing. Helping extend the portfolio’s winning streak were 5N Plus (TSE: VNP), which climbed 11% while setting another record high, along with Cloudflare’s 11% gain. 😊

This week was a good example of how quickly investor sentiment can change. Early fears around oil prices and inflation gave way to renewed optimism as tensions in the Middle East eased, earnings remained strong, and enthusiasm around AI picked back up. Weeks like this are a good reminder that markets rarely move in a straight line, which is why I focus on investing in high-quality companies and playing the long game. Of course, picking the right themes like AI always helps, but even a blind squirrel gets lucky now and then. 😊

Companies on the Radar

This week, with six companies all tied to AI’s “optical ecosystem,” it was harder than expected to identify a clear frontrunner. Of the group, I’d only consider investing in one or two at most. Based on my Radar Test results (below), I decided to remove GlobalFoundries (NASDAQ: GFS) and Ciena (NYSE: CIEN), as they finished at the bottom of the group. While they may still be solid businesses, they ranked lowest in my overall scoring.

This week, with six companies all tied to AI’s “optical ecosystem,” it was harder than expected to identify a clear frontrunner. Of the group, I’d only consider investing in one or two at most. Based on my Radar Test results (below), I decided to remove GlobalFoundries (NASDAQ: GFS) and Ciena (NYSE: CIEN), as they finished at the bottom of the group. While they may still be solid businesses, they ranked lowest in my overall scoring.

That leaves four names, each playing a different role in the broader AI infrastructure stack:

- Corning (NYSE: GLW): The “Glass Giant” supplying the fibre backbone that connects massive clusters of GPUs.

- Lumentum Holdings (NASDAQ: LITE): A key supplier of high-performance photonics, including advanced lasers used in AI data centres, where certain components are still in tight supply.

- Coherent Corp. (NYSE: COHR): The “Laser Powerhouse,” producing lasers and materials that convert electrical signals into light.

- Fabrinet (NYSE: FN): The “Master Builder,” providing high-end contract manufacturing for complex optical and electronic components.

Alongside these names, Amphenol Corporation (NYSE: APH) and TerraVest Industries (TSE: TVK) also moved back onto my radar.

With those changes, the six companies currently on my radar are:

- Amphenol Corporation: A large-cap US interconnect company that designs and manufactures connectors, cables, and fibre systems used across AI data centres, telecom networks, automotive, and industrial applications. It focuses on the physical connectivity layer that links everything together and enables high-speed data and power transfer.

- Fabrinet: A US large-cap precision manufacturing company that builds complex optical and electronic components for leading networking and photonics firms. It focuses on contract manufacturing rather than design, producing high-end optical modules and subsystems used in AI and telecom infrastructure.

- TerraVest Industries: A mid-cap Canadian industrial company that produces equipment for energy, storage, and transportation markets, including propane tanks, pressure vessels, and heating systems. It grows through a mix of organic expansion and acquisitions, serving steady, asset-heavy industrial niches across North America.

- Lumentum Holdings: A US large-cap optical networking company that designs and sells photonics components such as lasers and transceivers used in AI data centres and telecom networks. It sits in the middle of the value chain, turning optical technology into finished components that move data between systems.

- Coherent Corp.: A US large-cap technology company operating at the component and materials level, producing lasers, optical chips, and advanced materials used in AI infrastructure, telecom, and industrial applications. It supplies foundational building blocks for high-speed data transmission.

- Corning: A large-cap US company best known for specialty glass and fibre-optic products used in data centres, telecom networks, smartphones, and vehicles. It benefits from long-term demand for AI and cloud infrastructure, driven by massive fibre buildouts needed to move data efficiently.

To make the three optical companies easier to distinguish, here’s a simple mental model:

• Coherent = builds the core components (lasers, materials, chip-level photonics)

• Lumentum = designs and sells finished optical components/modules

• Fabrinet = manufactures those components for other companies

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated May 22, 2026.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!