Items that may only interest or educate me ….

Canadian economic data, US economic data, The Big 5 market Movers, Relative Strength Index …

Canadian economic data

Statistics Canada’s April Consumer Price Index (CPI) report showed annual inflation in Canada unexpectedly rose 4.4%, following a 4.3% increase in March. That was the first-time inflation grew since June 2022. It was not much, only 0.1%, but it must have caught the Bank of Canada’s (BoC) attention, thereby increasing the chances of another rate hike. On a monthly basis, inflation in April rose 0.7%, after gaining 0.5% in March. As for Core CPI, (CPI, less food and energy) the numbers matched the CPI numbers, up 4.4% on an annual basis, and up 0.5% monthly.

The report said higher mortgages, rent and fuel were the main cause of higher inflation numbers. The higher interest rates would have led to higher mortgages and rent, and I am sure its no coincidence fuel went up the same time the carbon tax was increased.

Canada’s March retail sales fell 1.4% in, after dropping 0.2% in February. On an annual basis, retails sales were up 2.4%. Core retail sales (retail sales less vehicles and vehicle parts, and gasoline) increased to 0.3% in March on a monthly basis and rose 2.5% on a yearly basis.

The slowing in overall retail sales may be enough to offset the increase in inflation and allow the BoC to hold the Canadian benchmark interest rate at 4.5%. However, if the BoC does raise the rate it likely will boost the value of the Canadian dollar.

US economic data

The Commerce Department’s April Advanced Monthly Sales for Retail and Food Services reported retail sales for April rose 0.4%, following a 0.6% decline in March. Analysts had been expecting an increase of 0.8%. On a yearly basis, retail sales were up 1.6%. Core retail sales (retail sales less vehicles, gasoline, building materials and food services) gained 0.7% in April, after falling 0.4% in March. Core retail sales is a value analysts pay attention to because it most closely corresponds with the consumer spending component of gross domestic product.

My takeaway is Americans continue to spend despite the higher interest rates. Analysts suggest consumer spending will provide a moderate amount of economic growth and help the US avoid a recession or at least have a soft landing (slowdown in economic growth that avoids recession).

The Big 5 market Movers

According to a report from DataTrek Research, five companies are responsible for the S&P 500’s year to date return of 9% – Alphabet (NASD: GOOGL), Apple (NASD: AAPL), Meta Platforms (NASD: META), Microsoft (NASD: MSFT), and Nvidia (NASD: NVDA). Of those companies rise in share prices, the report says up to 50% of those gains are from the hot topic of the day – Artificial Intelligence (AI). If not for these big tech companies and their AI appeal, the S&P would be in negative territory for 2023. I am glad I invested in four of those companies well before AI became the latest must have technology. 😊

Relative Strength Index

Just when I thought I was done with indexes, along comes another one – the Relative Strength Index (RSI).

The RSI is a technical indicator used by traders and investors to assess the strength and momentum of a price trend. It is primarily used to identify potential overbought and oversold conditions in a market or a specific security such as stocks.

The RSI is measured on a scale from 0 to 100 and is calculated based on the average gains and losses over a specified period, typically 14 days. The formula considers the ratio of upward price movements to downward price movements during that period.

When the RSI is above 70, it suggests that the market or security is potentially overbought, meaning it may have risen too quickly and could be due for a price correction or reversal. On the other hand, when the RSI is below 30, it indicates potential oversold conditions, suggesting that the market or security may have declined too much and could be poised for a price bounce or recovery.

Investors often use the RSI to help identify potential entry and exit points for trades. For example, if the RSI is above 70 and starts to decline, it may signal a potential sell or short opportunity (where an investor sells shares he does not already own and plans to buy the shares when the share price falls). Conversely, if the RSI is below 30 and starts to rise, it may indicate a potential buy.

The RSI readings can be found on the TD Direct Investing (DI) platform. If you do not use TD DI, it may be available on your trading platform, but if not, you can go to Yahoo! Finance and follow these steps:

- Go to the Yahoo! Finance Canada or the yahoo! finance website.

- In the search bar at the top of the page, enter the name of the company or ticker symbol you are interested in.

- On the stock’s summary page, you will see various tabs such as Summary, Chart, Statistics, etc. Click on the “Chart” tab.

- On the chart page, you should find a toolbar above the chart with several options. Look for an “Indicators” button or a similar feature. Click on it.

- A dropdown menu should appear with various technical indicators. Scroll down until you see “RSI” or “Relative Strength Index.” Click on it.

- The RSI indicator should now be displayed on the chart along with the stock’s price movements. You can adjust the timeframe and other settings as needed.

So, there you have it, another tool to add to your investing toolkit.

Now that you have another tool in your tool bag, let’s see what happened this past week….

Weekly Market Review

Monday: All four major North American indexes started the week on a positive note, ending their respective losing streaks. While the US debt ceiling deadline approaches, many investors believe the debt ceiling will be resolved. However, until the issue is resolved its likely to be a bumpy ride in the stock markets.

In Canada, the Toronto Stock Exchange Composite Index (TSX) was lifted by higher oil prices owing to tightening supplies, due in part to wildfires in Alberta that could lock in crude oil supplies from that province. The Canadian sectors were led upward by Basic Materials (miners and fertilizer manufacturers) and Financials, while Consumer Staples, Healthcare and Telecommunications Services were the only sectors to fall back.

In the US, the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) all edged higher despite the ongoing US debt negotiations and tough talk from the US Federal Reserve (Fed) that they expect interest rates to remain high for a while. It was a broad rally in the American sectors, led higher by Basic Materials and Financials. Defensive sectors Utilities and Consumer Staples were the only two sectors to decline.

Tuesday: In contrast to yesterday when all four indexes finished in the green, today all four ended in the red. Investors continue to monitor the US debt negotiations, hoping the debt ceiling will be raised sooner rather than later.

In Canada, the CPI came in higher than expected at 4.4%, igniting concerns the BoC may decide to raise the interest again to bring down inflation. The TSX dipped to its lowest level in a few months due to interest rate concerns, lower commodity prices dragging down resource companies, and the US bank situation weighing down the Canadian financial sector. It was a day of broad-based declines in the Canadian sectors. Industrial and Telecommunications Services dropped the least while Energy and Basic Materials had the biggest drops.

In the US, lower retail sales caused investors to believe the US economy is slowing down, possibly heading for a recession. Causing more angst for investors, Fed members have indicated they are not ready to lower interest rates any time soon. The Technology sector was the only one of the American sectors to end in the green today. Leading the downward plunge were Energy and Utilities.

Wednesday: Investors’ optimism grew as progress seemed to be made in the US’s debt ceiling negotiations, causing all four indexes to end the day higher. However, concerns persist over the chance of a historic default.

In Canada, after spending the morning in the red, an afternoon rally in energy and financial companies lifted the TSX into the green. On Bay Street, it was a mixed day in the Canadian sector with Healthcare and Consumer Cyclicals pulling the TSX higher, while Utilities and Telecommunications Services were the biggest drag.

In the US of A, US debt negotiators on both sides believe a deal can be done to avoid the US from defaulting on its debt payments, spurring investors to push all three indexes higher. It was a good day on Wall Street, led by the Financials and Consumer Cyclicals sectors. Utilities, Telecommunications Services, and Consumer Staples were the only sectors to end lower.

Thursday: The TSX ended basically flat, while progress in the US debt ceiling negotiations sparked hopes that the US could avoid a recession, pushing the American indexes ending higher. Oil prices fell on economic news that raised the possibility the Fed could increase the cost of borrowing again.

In Canada, the TSX was in negative territory for most of the day on concerns the BoC would raise the Canadian interest rate. Late in the day, a last-minute rally, fueled by optimism from south of the border, nudged the TSX barely into the green. In trading, leading the way in the Canadian sectors were Healthcare and Industrials, while Basic Materials and Utilities had the biggest declines.

In the US, after a rollercoaster ride most of the day, all three indexes ended on a high note thanks to continuing optimism a deal will be done in time to avoid the US default on its debt commitments. Comments from Fed members continue to warn they are not ready to pause or lower interest rates. In trading, Technology and Consumer Cyclicals were the best performers in the American sectors, while Telecommunications Services and Utilities dropped the most.

Friday: A mixed day in the markets with the TSX ending higher, and the American indexes all falling (remember that warning on Monday about a bumpy ride). The big news was once again in the US where US debt ceiling negotiations stalled, after Republicans walked out of negotiations.

In Canada, despite the latest retail sales report showing a drop of 1.4% in March and the pullback of the American indexes, the TSX advanced on stronger commodity prices (such as oil and gold). In trading, the Energy and Consumer Staples sectors were the big winners. Consumer Cyclicals, Financials, and Healthcare were the only sectors to end lower.

In the US, the three indexes started the morning in positive territory before dropping on news of the pause in debt ceiling negotiations. Adding to downward pressure, the Fed said inflation was “far above” their 2% target and indicated it was too soon to tell if another interest rate hike was needed. Of the American sectors, Healthcare, Energy and Consumer Staples were the only sectors to advance. Dropping the most were Consumer Cyclicals and Financials.

Weekly Market and Portfolio Review

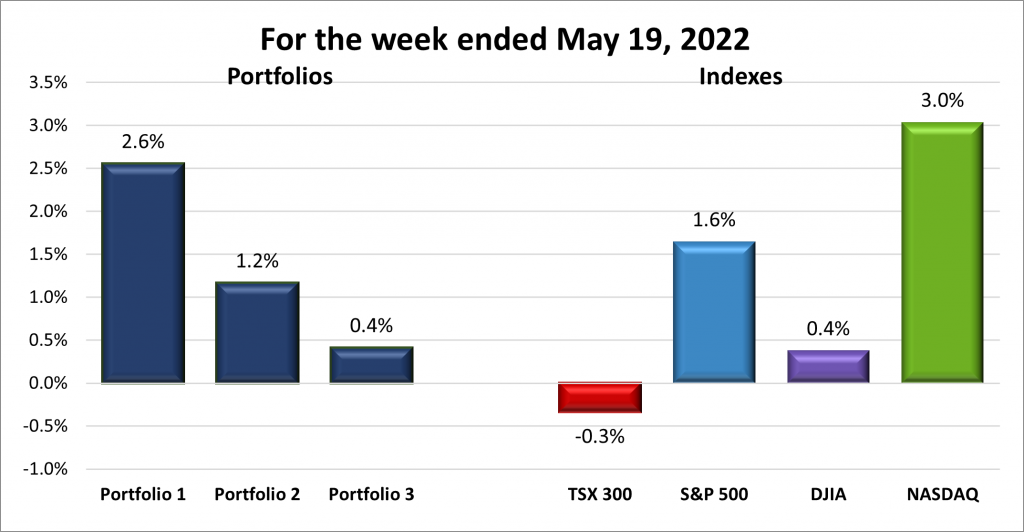

For the week, the TSX (SPTSX) dipped 0.3%, the S&P 500 (SPX) was up 1.6%, the DJIA (INDU) added 0.4% and the Nasdaq (CCMP) surged 3.0%.

![]() The stock market does respond to optimism. It was investor optimism that the US would be able to raise its debt ceiling that pushed the American indexes higher for most of the week, as you can see in the chart above. Investor optimism drove both the S&P and the Nasdaq to their best week since March. It was not until the negotiations hit a snag on Friday morning that the optimism took a hit and caused the three indexes to pullback. The TSX, posted its fourth consecutive weekly decline thanks to the latest Canadian inflation report that came in higher than expected, raising concerns the BoC would raise the Canadian interest rate.

The stock market does respond to optimism. It was investor optimism that the US would be able to raise its debt ceiling that pushed the American indexes higher for most of the week, as you can see in the chart above. Investor optimism drove both the S&P and the Nasdaq to their best week since March. It was not until the negotiations hit a snag on Friday morning that the optimism took a hit and caused the three indexes to pullback. The TSX, posted its fourth consecutive weekly decline thanks to the latest Canadian inflation report that came in higher than expected, raising concerns the BoC would raise the Canadian interest rate.

![]() A good week for the technology heavy Nasdaq usually means another good week for the technology biased Portfolios. And indeed it was, with each posting another positive week. Portfolio 1 was helped by its three mega cap companies – Alphabet, Apple and Nvidia – which continue to outperform. Portfolio 2 was pushed higher by its big mega cap stock Microsoft, but also received lift from its other US technology companies and its Canadian energy companies. Bringing up the rear was Portfolio 3. Along with mega cap Microsoft, Portfolio 3 had good performances from a few of its US technology companies and its lone Canadian energy company. Unfortunately, it had too many companies that drifted lower, limiting the gains this past week.

A good week for the technology heavy Nasdaq usually means another good week for the technology biased Portfolios. And indeed it was, with each posting another positive week. Portfolio 1 was helped by its three mega cap companies – Alphabet, Apple and Nvidia – which continue to outperform. Portfolio 2 was pushed higher by its big mega cap stock Microsoft, but also received lift from its other US technology companies and its Canadian energy companies. Bringing up the rear was Portfolio 3. Along with mega cap Microsoft, Portfolio 3 had good performances from a few of its US technology companies and its lone Canadian energy company. Unfortunately, it had too many companies that drifted lower, limiting the gains this past week.

With the US debt ceiling negotiations gaining urgency next week I expect the markets to be more volatile as investors react to every bit of information and rumour coming out of those meetings. The sooner the deal gets done, the better. Investors will regain confidence in US markets and hopefully the rally that has boosted the mega cap technology companies will spread to the overall market. Until next week, onward and upward! 😊

Companies on the Radar

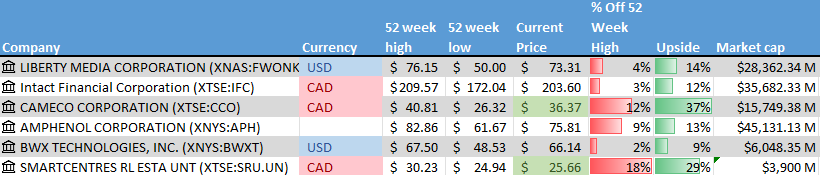

This past week two new companies came on my radar – Cameco (TSX: CCO) and BWX Technologies (NYSE: BWXT). Both are involved in the nuclear energy industry which is seeing a bit more interest lately as countries seek to lower their carbon footprint. Cameco is a Canadian company that mines and sells uranium and builds reactor components for reactors. BWX is an American company that builds and sells nuclear components globally. One of its biggest customers is the US Navy.

There is a bit of a tailwind for nuclear energy as many countries are starting to realize solar and wind power alone cannot supply enough reliable energy to meet their needs. Nuclear energy has zero carbon footprint and can supply reliable energy to a large area. However, nuclear energy faces a significant headwind – fear of a meltdown. Both companies are already successful, but if the world does turn to nuclear energy, these two companies would be in the right place at the right time. I will take a closer look to get a better understanding of both companies to see if they will join the other companies below:

- Liberty Media’s Formula One Group (NASD: FWONK): tracks the performance of their Formula One World Championship unit.

- Intact Financial (TSX: IFC): A Canadian mid size insurance company supplying home, car and business insurance in Canada, the US, and the UK.

- Amphenol: (NYSE: APH) Producer of a high-tech interconnect, sensor, and antenna solutions for the automotive, aerospace, industrial and various technology industries.

- Smartcentres Real Estate Investment Trust (TSX: SRU.UN): Owns and manages a number of income producing malls and retails spaces throughout Canada.

The Radar Check was last updated May 19, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended May 19, 2023: UP ![]()

- Home Depot (NYSE: HD) had a disappointing earnings report and forecast a drop in annual sales and a sharper than expected decline in profit. Management blamed declines on a wet spring season, falling lumber prices and consumers shifting to travel oriented vacations after the past few years of staying at home. The pandemic home improvement boom appears to be over.

- At Tesla’s (NASD: TSLA) annual shareholder meeting, CEO Elon Musk indicated he had no plans to step down from his role at Tesla and assured shareholders the Cybertruck would finally start rolling out to customers later this year. He also said the company would venture into the field of advertising to sell more vehicles.

On a separate note, the company said it is considering building a factory in India to service that market as well as export to other countries. - General Motors (NYSE: GM) said despite the capability to build over 1 million electric vehicles (EVs) by 2025, it would likely be restrained by its ability to produce enough batteries for those EVs. The battery bottleneck could reduce the number of EVs produced to less than 600,000.

- CrowdStrike (NASD: CRWD) announced they have been named a leader in Forrester Research’s The Forrester Wave: Managed Detection and Response (MDR) for the second quarter 2023. As well, CrowdStrike ranked first in market share for the second year in a row in Gartner MDR for Managed Security Services.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX: DIR.UN)

US $

BSR Real Estate Investment Trust (TSX: HOM.U)

Apple Inc. (NASD: AAPL)

Quarterly Reports

Home Depot, Inc.

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their first quarter 2023 financial results on May 16, 2023

- Revenue of $37,257 for the three months ended April 30, compared to $38,908 for the period ended May 1, 2022. A decrease of over 4%.

- Net income of $3,873 for the three months ended April 30, compared to net income of $4,231 for the period ended May 1, 2022.

- Diluted earnings per ordinary share of $3.82 for the three months ended April 30, compared to earnings of $4.11 per share for the period ended May 1, 2022.

SEA Limited

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their first quarter 2023 financial results on May 16, 2023

- Revenue of $3,041,104 for the three months ended March 31, compared to $2,899,571 for the same period in 2022. An increase of almost 5%.

- Net income of $87,292 for the three months ended March 31, compared to a net loss of $580,136 in the same period in 2022.

- Diluted earnings per ordinary share of $0.15 for the three months ended March 31, compared to a loss of $1.04 per share for the same period in 2022.

Lightspeed Commerce Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their fourth quarter 2022 financial results on May 18, 2023

- Revenue of $184,228 for the three months ended March 31, compared to $146,558 for the same period in 2022. An increase of over 25%.

- Net loss of $74,468 for the three months ended March 31, compared to a net loss of $114,517 in the same period in 2022.

- Diluted loss per ordinary share of $0.49 for the three months ended March 31, compared to a loss of $0.77 per share for the same period in 202.

- Revenue of $730,506 for the six months ended March 31, compared to $548,372 for the same period in 2022. An increase of over 33%.

- Net loss of $1,070,009 for the six months ended March 31, compared to a net loss of $288,433 in the same period in 2022.

- Diluted loss per ordinary share of $7.11 for the six months ended March 31, compared to a loss of $2.04 per share for the same period in 2022.

Portfolio 2

Portfolio 2 for the week ended May 19, 2023: UP ![]()

- The Bank of Nova Scotia (TSX: BNS) was handed US$ 35 million in fines because employees used their personal devices and apps for work related communications. BNS notified the US Security Exchange Commission (SEC) of the issues, prompting an investigation by the SEC into the bank’s record keeping practises.

- Guardant Health (NASD: GH) announced it’s Guardant360 CDx/Guardant360 liquid biopsy test is now covered for comprehensive genomic profiling by all major U.S. commercial health insurers. The test is used to detect actionable cancer biomarkers in a patient’s blood that may help determine their course of therapy.

- Walt Disney Company (NYSE: DIS) announced they cancelled plans to build a new US$ 1 billion campus on their Disney World location and relocate 2,000 well paying jobs to the new campus. Disney attributes the decision to “leadership changes” and “changing business conditions.”

Disney also announced they were shutting down their luxury hotel Star Wars: Galactic Starcruiser, also at Disney World.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Take-Two Interactive Software, Inc.

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their fourth quarter 2022 financial results on May 17, 2023

- Revenue of $1,266.3 for the three months ended March 31, compared to $930.0 for the same period in 2022. An increase of over 55%.

- Net loss of $610.3 for the three months ended March 31, compared to net income of $110.9 in the same period in 2022.

- Diluted loss per ordinary share of $3.62 for the three months ended March 31, compared to earnings of $0.95 per share for the same period in 202.

- Revenue of $5,349.9 for the year ended March 31, compared to $3,504.8 for the same period in 2022. An increase of over 52%.

- Net loss of $1,124.7 for the year ended March 31, compared to net earnings of $418.0 in the same period in 2022.

- Diluted loss per ordinary share of $7.03 for the year ended March 31, compared to earnings of $3.58 per share for the same period in 2022.

Portfolio 3

Portfolio 3 for the week ended May 19, 2023: UP ![]()

- The Microsoft acquisition of Activision Blizzard (NASD: ATVI) got interesting when the deal got the go ahead from the European Union (EU). The EU gave their thumbs up to the deal saying the numerous licensing deals Microsoft has made with its competitors makes the deal acceptable. The deal is now knotted 1 approval by the EU, 1 veto by Britain. Microsoft and Activision still need to obtain approval from the US antitrust officials as well as other regulators.

- A few weeks ago, TD Bank (TSX: TD) pulled out of their deal to acquire US regional bank First Horizon (NASD: FHN) after learning US regulators would not sign off on how TD handled suspicious customer transactions. I thought this meant TD would be able to go looking for another US bank to acquire but it turns out TD could be in the penalty box for the next few years. Not only do they have to change the way they handle suspicious transactions, but they must show and prove to the regulators that they have made the required changes that will satisfy the regulators.

- Enghouse Systems Ltd. (TSX: ENGH) announced it has entered into an Agreement with Lifesize Inc., to acquire most of Lifesize’s assets and brands. Lifesize is a global provider of video conferencing and omnichannel contact center solutions.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Fortuna Silver Mines Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their first quarter 2023 financial results on May 15, 2023

- Revenue of $175,653 for the three months ended March 31, compared to $182,239 for the same period in 2022. A decrease of almost 4%.

- Net income of $11,857 for the three months ended March 31, compared to net income of $26,296 in the same period in 2022.

- Diluted earnings per ordinary share of $0.04 for the three months ended March 31, compared to earnings of $0.09 per share for the same period in 2022.