This is another in the series of ‘Tips for Those New to Investing.’ This week we take a look at Dollar cost averaging.

The Power of Dollar-Cost Averaging: A Beginner’s Best Friend

When markets get unpredictable, it is easy to feel unsure about when to invest. Should you wait for prices to drop further, or jump in now? One simple strategy that can remove some of the guesswork is Dollar-Cost Averaging (DCA).

What Is Dollar-Cost Averaging?

Dollar-cost averaging means investing a fixed amount of money at regular intervals, no matter what is happening in the market. Whether stocks are rising, falling, or going sideways, you are consistently buying in, which helps average out the price over time.

Let us say you invest $100 every month into a company or an index fund. Some months, the price will be higher, meaning you will buy fewer shares. Other months, when prices are lower, you will scoop up more shares for the same amount of money. Over time, this strategy helps smooth out the market’s highs and lows.

Benefits of Dollar-Cost Averaging

- Reduces the Impact of Market Volatility Trying to time the market perfectly often leads to missed opportunities or overpaying for stocks. With DCA, you do not have to worry about timing – you are consistently investing, helping you stay steady during market swings.

- Builds Discipline DCA encourages a consistent investing habit, which is especially important when you are just starting out. You are regularly growing your portfolio without second-guessing every market move.

- Lowers Emotional Investing Market volatility can lead to emotional decisions, like panic selling or buying into a rally out of fear of missing out (commonly referred to as FOMO). DCA takes emotions out of the equation by keeping you focused on a long-term plan, no matter what is happening in the market today.

- Accessible for New Investors With DCA, you do not need a large sum to start investing. Even small, regular contributions can help grow your portfolio over time. This makes it perfect for those just starting out who might not have a lump sum to invest upfront.

Why It Works in Volatile Markets

During volatile periods – like October, when markets can get particularly unpredictable – DCA really shines. Instead of stressing over market drops, you can view them as opportunities to buy more shares at lower prices, setting yourself up for potential gains when the market rebounds.

How to Get Started with Dollar-Cost Averaging

- Set a Budget: Decide how much you can comfortably invest each month. It does not have to be a lot – the key is consistency.

- Choose Your Investments: DCA works well with both index funds and individual stocks. For beginners, broad market index funds can help diversify your portfolio.

- Stay Committed: Stick to your plan, especially when the market is down. Remember, this strategy is for the long term.

Conclusion

Dollar-cost averaging is one of the easiest and most effective strategies for new investors to start building wealth without worrying about market timing. By investing regularly, you will benefit from market dips, stay disciplined, and avoid the emotional rollercoaster that comes with volatility. If you are new to investing, this strategy is a steady friend in both calm and stormy markets!

Now that we have covered the benefits of dollar-cost averaging, let us shift gears and look at what has been happening in the markets this past week. Let’s look into the latest developments and see how the markets have been reacting.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Bank of Canada makes super sized cut

The BoC delivered a widely anticipated 0.5% cut to its benchmark interest rate on Wednesday, lowering it to 3.75%. This marks the fourth consecutive rate cut and the first “super-sized” reduction in over 15 years, excluding the pandemic period.

With inflation seemingly under control, BoC officials have shifted their focus to reviving the economy. Third-quarter growth came in well below expectations, and unemployment remains high. The economy has underperformed, with per capita GDP shrinking for five consecutive quarters. Officials voiced concerns that inflation could dip too low and hope this rate reduction – and potential future cuts – will stimulate demand and foster stronger growth, keeping inflation near their 2% target.

The BoC attributed the easing inflation to lower shelter costs (mortgages and rents), a cooling demand-supply imbalance, and falling global oil prices. Although the sluggish economic growth is concerning – third-quarter GDP is projected to grow by just 1% annually, well below the bank’s forecast – officials remain optimistic about a rebound over the next two years.

Governor Tiff Macklem explained the larger cut, stating, “We took a bigger step today because inflation is back at the 2% target, and we want to keep it there.” The BoC expects inflation to remain stable at 2% through 2025, signaling that more rate cuts could be on the horizon, assuming the economy evolves as expected.

In the short term, the rate cut will lower the cost of variable-rate mortgages and loans, as well as new loans, giving consumers and businesses more disposable income. Over time, this extra cash is expected to fuel consumer spending and business investment, helping to jumpstart the economy.

The next interest rate announcement is scheduled for Dec. 11.

Retail prices

Statistics Canada’s retail sales report for August showed a 0.4% increase, down from a stronger-than-expected 0.9% gain in July. On an annual basis, retail sales grew by 1.4%, surpassing analysts’ prediction of a 0.9% rise for the year. Monthly gains came in slightly below the forecast of 0.5%, but the overall trend remains positive.

Digging deeper into the numbers, ‘Shoe retailers’ led the monthly growth with a 6.5% surge, while the ‘Jewellery, luggage, and leather goods’ sector saw the largest drop, falling by 2.9%. Over the year, ‘New car dealers’ posted the biggest gain, jumping 7.5%, while ‘Convenience retailers and vending machine operators’ struggled, down 5.7%.

Core retail sales, which exclude gas stations, fuel vendors, and motor vehicle and parts dealers, took a slight hit, falling 0.4% in August after two consecutive monthly gains. Year-over-year, core retail sales edged up by 0.3%, slowing from July’s 0.9% growth.

This mixed picture suggests that while some sectors are thriving, others are struggling as consumer spending shifts. Consumers have yet to fully benefit from easing inflation and the BoC’s recent rate cuts, which lowered the benchmark rate by a total of 0.75%. However, further reductions may be necessary to drive sustained growth in spending and boost the broader economy.

Canadian market volatility

Canada’s Volatility Index (CVIX) began the week at 10.57, climbing to a midweek high of 12.99 before settling at 11.04 by Friday’s close. The early rise was likely driven by anticipation of the BoC’s interest rate decision, with a brief spike coinciding with the announcement. Afterward, Canadian markets remained relatively calm, gradually drifting to lower levels as the week went on.

Tracked under the ticker VIXI on the Toronto Stock Exchange (TSE), the CVIX gauges anticipated market volatility. A reading below 10 suggests calm and stable market conditions, while values between 10 and 20 indicate moderate volatility with typical market fluctuations. When the index climbs above 20, it signals heightened uncertainty and the likelihood of more turbulent market conditions.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Consumer Sentiment Index (CSI)

The University of Michigan’s CSI for October came in at 70.5, slightly up from September’s 70.1 and 10.5% higher than last year’s 63.8 reading. This is the highest level since April 2024, though still well below the 88.3 peak recorded in 2021, post-pandemic.

Looking closer, the Current Economic Conditions index rose to 64.9, a 2.5% increase from September. However, it remains 8.1% lower than the 70.6 recorded in October 2023, showing that short-term confidence still lags. On the flip side, the Index of Consumer Expectations dipped slightly to 74.1 from 74.4 in September, but it is up 25% from 59.3 a year ago, reflecting growing optimism about future economic prospects.

The Current Economic Conditions index reflects how consumers feel about their immediate financial situation, while the Consumer Expectations index captures their outlook for the months ahead.

This marks the third consecutive month of rising consumer sentiment, largely driven by easing interest rates. However, political uncertainty surrounding the upcoming presidential election is also influencing consumers. As the gap between Democrats and Republicans narrows, many are adopting a “wait-and-see” approach to their economic outlook, with political outcomes likely weighing heavily on future expectations.

American market volatility

The CBOE Volatility Index (VIX), often referred to as the market’s “fear gauge,” started the week at 18.02, fluctuating between 18.0 and 19.5 before spiking above 20 on Wednesday. It continued to bounce between 20 and 18.3 for the rest of the week, ultimately closing at 20.33. A VIX above 20 tends to grab Wall Street’s attention, as it signals heightened market volatility.

The midweek spike coincided with Tesla’s stronger-than-expected earnings report, while growing concerns over the Fed’s upcoming interest rate decision likely added to the market jitters.

For context, the VIX measures expected market volatility over the next 30 days. Readings below 12 suggest calm conditions, while levels between 12 and 20 reflect typical market fluctuations. When the index moves into the 20-30 range, it indicates increasing uncertainty, and anything above 30 points to elevated market stress, often signaling a looming crisis or major market disruption.

Weekly Market Review

Monday: the week got off to a slow start with three of the four major North American indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA) – ending the day lower. Investors are preparing for a week of big-name earnings reports. A week of solid earnings should keep the bull market running, whereas weak reports will act as a drag on the indexes. Oil prices were up slightly as a result of ongoing tensions in the Middle East.

In Canada, investors are waiting third quarter earnings results and this week’s upcoming rate decision by the BoC. In trading, Energy was the only sector to end in the green, while Healthcare fell the farthest.

In the US, the Nasdaq Composite Index (Nasdaq) was the only index to post a gain, largely on the strength of a surging Nvidia (NASD: NVDA). In trading, Technology was the only sector to close in the green, while Healthcare ended the deepest in the red.

Tuesday: the indexes started the day lower but steadily climbed throughout the session, with the Nasdaq being the only one to break into positive territory, while the others hovered just below the flatline. Oil prices ended higher on tightening supplies and the conflict in the Middle East.

In Canada, most analysts expect the BoC to cut the benchmark interest rate by 0.5% in a bid to jumpstart the sluggish economy. Higher commodity prices limited the declines caused by a drop in the Financials sector. In trading, the Healthcare sector recoded the largest gain while Consumer Cyclicals suffered the biggest fall.

In the US, investors are starting to worry that the recent strong economic data might prompt the Fed to hold off on any rate cuts at their next meeting, stirring some unease in the markets. In trading, Consumer Staples advanced the farthest, while the Industrials declined the most.

Wednesday: the indexes all closed lower as investors reassessed the odds that the Fed will lower the interest rate at their next meeting. Oil prices returned to their downward trajectory following a report of a large build up in American inventories.

In Canada, the BoC lowered their lending rate by 0.5% to 3.75% but that was not enough to prevent the TSX from falling for a third straight day, dragged lower by falling commodity prices. In trading, Consumer Cyclicals and Communications Services were the only sectors to advance, the Technology sector incurred the biggest decline.

In the USA, investors were taking some profits after the previous week’s rally. In trading it was day of broad-based losses, with only the Utilities sector managing to post a gain. Leading the sectors down was Consumer Cyclicals.

Thursday: the markets saw mixed results today, with the TSX and DJIA closing in the red, while the Nasdaq and S&P finished higher. The S&P snapped a three-day losing streak, buoyed by a strong earnings report from Tesla (NASD: TSLA) which caused its share price to jump 21%, giving investors hope that the rest of the “Magnificent 7” will deliver similarly upbeat earnings. Oil prices fell on news of peace talks in the Middle East.

In Canada, the TSX lost ground for the fourth straight day, weighed down by lower commodity prices. It appears investors are waiting for earnings from some of the bigger companies. In trading, the technology sector was the biggest gainer, while Communications Services had the biggest fall.

In the USA, high yields on US Treasury bonds and profit taking continued to put downward pressure on the markets. In trading, the Consumer Cyclicals led all sectors thanks to the surge in Tesla shares. On the downside, Basic Materials (mining companies and fertilizer manufacturers) declined the most.

Friday: after a strong start in the morning that saw all four indexes in the green, the markets cooled off in afternoon trading, leaving only the Nasdaq in the green at the end of the day. Uncertainty over the next move by the Fed regarding the US interest rate continues to weigh on the markets. Oil prices surged nearly 1.5%, driven by growing doubts over the success of Middle East peace talks.

In Canada, the TSX extended its longest losing streak since April, marking five consecutive days of decline. Investors grew increasingly risk-averse ahead of the upcoming US election and a series of earnings reports from major bellwether companies, both of which could impact market sentiment in the near term. In trading, rising oil prices propelled the Energy sector to the biggest daily gains, while Consumer Cyclicals suffered the largest decline.

In the US, optimism surrounding strong earnings reports expected from five of the “Magnificent 7” companies next week helped the Nasdaq buck the trend and avoid the declines seen in the other indexes. In trading, Communication Services posted the biggest gain, while Utilities suffered the biggest loss.

Weekly Market and Portfolio Review

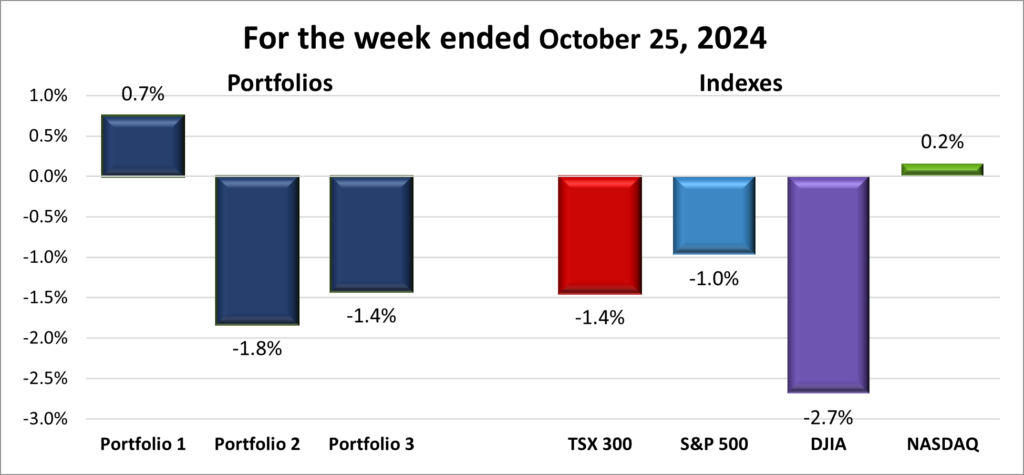

For the week, the TSX (SPTSX) slipped 1.4%, the S&P (SPX) fell 1.0%, the DJIA (INDU) declined 2.7% and the Nasdaq (CCMP) gained 0.2%.

| Index | Weekly Streak |

| TSX: | 1 – week losing streak |

| S&P: | 1 – week losing streak |

| DJIA: | 1 – week losing streak |

| Nasdaq: | 7 – week winning streak |

![]() As we move through the historically volatile months of September and October, I’ve had my fingers crossed to avoid any downside surprises. After the previous week’s strong upward trend that saw several of the major North American indexes hit fresh highs, this past week felt like the markets were hitting the pause button. Let’s hope it’s just a breather! 😊

As we move through the historically volatile months of September and October, I’ve had my fingers crossed to avoid any downside surprises. After the previous week’s strong upward trend that saw several of the major North American indexes hit fresh highs, this past week felt like the markets were hitting the pause button. Let’s hope it’s just a breather! 😊

In the US, with limited economic data to guide the way, third-quarter earnings and speculation around the Fed’s next moves took the spotlight. Add in rising US Treasury yields, tensions in the Middle East, and the increasingly tight US election race, and it’s no surprise that American indexes pulled back from their recent highs.

So far, earnings have been solid, with Tesla delivering a surprise boost that sparked optimism ahead of next week’s tech-heavy lineup. Many of the tech giants – including members of the Magnificent 7 – are set to report. Strong corporate earnings are key to keeping this bull market alive.

The Fed also remains in focus – not so much for what it’s done, but for what it might do next. Investors are growing uneasy about the possibility of the Fed slowing down or even pausing their rate cuts at their upcoming meeting.

Here in Canada, the TSX hit an all-time high the previous Friday but spent most of this past week giving back some of those gains. Despite the Bank of Canada’s hefty 0.5% rate cut, lower commodity prices and similar challenges affecting US markets weighed on the index.

Overall, it wasn’t a great week, but there were no major drops – just more of a breather. Looking ahead, next week brings a wave of economic news and a flurry of earnings reports, including from Magnificent 7 members Alphabet (NASD: GOOGL), Microsoft (NASD: MSFT), Amazon (NASD: AMZN), and Apple (NASD: AAPL). Strong results from these companies, along with positive earnings overall, could keep the bulls running – otherwise we might see a major stumble. We’ll find out soon enough. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 7 – week winning streak |

| Portfolio 2: | 1 – week losing streak |

| Portfolio 3: | 1 – week losing streak |

![]() After two strong weeks of gains in October, a market pullback felt almost inevitable, as the weekly performance chart below shows. I was expecting the portfolios to take a hit as well, but to my surprise, Portfolio 1 managed to extend its weekly winning streak to seven, despite the dip.

After two strong weeks of gains in October, a market pullback felt almost inevitable, as the weekly performance chart below shows. I was expecting the portfolios to take a hit as well, but to my surprise, Portfolio 1 managed to extend its weekly winning streak to seven, despite the dip.

Portfolio 1 was the only one to increase in value, as well as outperform all four indexes. Despite only 46% of its holdings posting a gain, a stellar 22% rise in Celestica (TSE: CLS) and a small bump from Nvidia, the portfolio’s most valuable stock, pushed it into positive territory. During the week, both Nvidia and Apple hit record highs, and after a slight pullback from Apple, Nvidia claimed the crown as the world’s most valuable company by market cap.

Portfolio 2 had a rough week, showing the weakest performance of the bunch. Only 30% of the companies in the portfolio increased in value, and none were significant enough to offset the losses. On the bright side, there were no major drops, but that’s a small consolation.

Portfolio 3 didn’t fare much better, with just 31% of its holdings posting gains. Fortunately, Lithium Americas (TSE: LAC) had a strong week, jumping 18%, which helped cushion the overall loss.

With three of the four indexes in the red, it wasn’t surprising to see the portfolios have an off week. To paraphrase the band Trooper, “the markets can’t shine every day.” 😊 Here’s hoping the markets shine once again next week!

Companies on the Radar

Once again, no new companies have caught my eye. To be fair, I am not actively hunting for them, as I am content with the ones already in any of the three portfolios. In fact, I am more inclined to trim a few positions rather than add more. That said, if a great company popped up at the right price, it would definitely grab my attention. For now, though, the radar stays focused on the four companies listed below.

Once again, no new companies have caught my eye. To be fair, I am not actively hunting for them, as I am content with the ones already in any of the three portfolios. In fact, I am more inclined to trim a few positions rather than add more. That said, if a great company popped up at the right price, it would definitely grab my attention. For now, though, the radar stays focused on the four companies listed below.

- On Holding AG (NYSE: ONON), a medium cap Swiss company, founder-run, sports products company.

- Topaz Energy Corp. (TSE: TPZ), a mid-cap Canadian energy investment firm that focuses on strategic investments in premium energy assets operated by top-tier Canadian companies

- Zoetis Inc. (NYSE: ZTS), a leading animal health company that discovers, develops, manufactures, and commercializes vaccines, medicines, diagnostics, and other technologies for both companion animals and livestock.

- Coca-Cola (NYSE: KO), a global beverage giant, best known for its flagship soft drink, Coca-Cola. They offer a wide range of non-alcoholic drinks, including sodas, juices, teas, and bottled water, catering to consumers worldwide.

As always, these are not buy recommendations – be sure to do your own research and make decisions that align with your personal financial goals!

The Radar Check was last updated October 25, 2024.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended October 25, 2024: UP ![]()

- Walmart (NYSE: WMT) announced plans to begin delivering prescription medicines and refills alongside groceries and other items, all in a single order delivered that day, if not within 30 minutes of being placed. This new service, however, will only be available in the US, adding another level of convenience for their American customers.

- Nvidia announced that, in collaboration with their manufacturing partner Taiwan Semiconductor (NYSE: TSMC), they have resolved a design flaw in their latest Blackwell chips. These artificial intelligence (AI) – specific chips are set to begin shipping later this year.

In other Nvidia news, the company expanded its relationship with India’s Reliance Industries (NSE: RELIANCE) to launch an AI model for the Hindi language. This new model would be used to help other businesses develop their own Hindi language AI models.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Decisive Dividend Corp (TSEV: DE) DRIP

BCE Inc (TSE: BCE) DRIP

Dream Industrial Real Estate Investment Trust (TSE: DIR.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

General Motors Company

Third quarter 2024 financial results on October 22, 2024

Canadian National Railway Company

Third quarter 2024 financial results on October 22, 2024

Celestica Inc.

Third quarter 2024 financial results on October 23, 2024

Portfolio 2

Portfolio 2 for the week ended October 25, 2024: DOWN ![]()

- Walt Disney (NYSE: DIS) named Morgan Stanley (NYSE: MS) executive chair James Gorman as the board of governors’ chair and announced they plan to have a replacement for current Chief Executive Officer (CEO) Bob Iger in 2026. Mr. Gorman brings valuable succession planning experience, having successfully appointed his own successor as CEO at Morgan Stanley while retaining the other two internal CEO candidates within the company.

- Canadian Natural Resources (TSE: CNQ) is set to boost its use of the newly completed Trans Mountain pipeline after acquiring Athabasca oil sands assets from Chevron (NYSE: CVX) earlier this year. With the added capacity, CNQ will be able to ramp up its oil shipments by 75%, bringing its total to 164,000 barrels per day (bpd). Considering the pipeline’s overall capacity of 890,000 bpd, CNQ will command around 18% of the total – not a small amount!

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSE: DIR.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

Whitecap Resources Inc.

Third quarter 2024 financial results on October 23, 2024

Portfolio 3

Portfolio 3 for the week ended October 25, 2024: DOWN ![]()

- Microsoft launched the latest installment in the Call of Duty series, Call of Duty: Black Ops 6 – one of the most successful video game franchises in history. This is the first major release from Microsoft since they acquired the gaming giant Activision Blizzard last year, underscoring the company’s big bet on the video game industry. Microsoft is betting that gamers will prefer a streaming version enough to pay a more lucrative monthly subscription fee rather make a one-time purchase.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Canadian $

goeasy Ltd. (TSE: GSY)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.