Let’s take a moment this November 11th to honour and remember those who served. Lest we forget.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, Covered calls, …

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Bank of Canada minutes

The Bank of Canada’s Governing Council cut the benchmark interest rate by 0.5% on October 23, bringing it down to 3.75%. This marks the fourth consecutive cut, aimed at reviving the sluggish economy. The decision came after a thorough discussion of key factors, as outlined in the minutes of their latest meeting.

Internationally, the American economy continues to outperform expectations, driven by strong consumer spending and cooling inflation. However, the robust US labour market could delay reaching the 2% inflation target, which may slow future rate cuts there. In China, despite government efforts to revive its struggling economy, uncertainty persists, potentially reducing demand for raw materials—a concern for resource rich Canada. Overall, global conditions are improving as inflation falls and rates ease.

Domestically, Canada’s GDP remains weak, with rising unemployment and slowing population growth adding to concerns. Higher interest rates have led consumers to save more and spend less, while mortgage holders feel the pinch of rising payments. Business investment has also slowed. However, energy exports have increased thanks to the Trans Mountain Expansion, offering a bright spot. Inflation has dropped, with the Consumer Price Index at 1.6% and core inflation at 2.5%, largely due to lower oil prices.

In the end, the Council agreed that with inflation likely to keep cooling, a 0.5% rate cut was appropriate given the weak labour market and economy. Some members worried that such a large cut could be seen as a sign of trouble, “leading to expectations of more moves of this size.” While more cuts may be needed, they emphasized that future decisions will be data-driven, cautioning against expecting more large cuts ahead.

Labour Force Survey (LFS)

Statistics Canada’s latest Labour Force Survey revealed that the economy added 15,000 jobs in October – well below the expected 25,000 and a sharp decline from September’s impressive 46,700. The unemployment rate held steady at 6.5%, slightly better than the forecasted 6.6%, but still 0.8% higher than this time last year. Meanwhile, the employment rate edged down by 0.1%, from 60.7% to 60.6%, as job growth could not quite keep pace with the growing population.

On a positive note, wage growth showed solid momentum, rising 0.4% month-over-month and 4.9% year-over-year, up from 4.6% in September. This suggests that while the overall job market remains soft, those who are employed are seeing healthy pay increases.

After September’s unexpected surge in jobs, October’s results appear to reflect the ongoing cooling of the labour market. For now, the outlook remains mixed—job growth is slowing, but wage growth provides a silver lining for workers. This combination of data could lead to more cautious decision-making by the Bank of Canada, likely resulting in a 0.25% rate cut rather than the hoped-for 0.5% reduction. Investors should keep a close eye on these developments, as they could have a big impact on future monetary policy and overall economic growth.

Canadian market volatility

Canada’s Volatility Index (CVIX) kicked off the week at 12.59 and steadily dropped, finishing at 11.57 by Friday’s close. This dip suggests that the market was feeling more confident, likely due to the clarity following the US presidential election.

Tracked under the ticker VIXI on the Toronto Stock Exchange (TSE), the CVIX gauges how much market volatility investors expect. A reading below 10 points to a calm, stable market, while numbers between 10 and 20 signal typical market fluctuations with moderate volatility. But when the index climbs above 20, it is a sign of rising uncertainty and the potential for a bumpy ride ahead.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Fed rate decision

Following the latest FOMC meeting, Fed Chair Jerome Powell announced a 0.25% cut to the benchmark interest rate, bringing it down to 4.75%—the second reduction in seven weeks. This move comes as inflation continues to cool but remains slightly above the Fed’s 2% target.

The Fed also noted that while economic activity is expanding at a solid pace, the labour market has eased, with unemployment ticking up but still staying relatively low. Powell emphasized that the recent US election results will not impact near-term monetary policy (interest rates), though the Fed will monitor potential tax and regulatory changes from the new administration for any effects on inflation and employment.

While Powell did not provide clues about future rate changes, he struck an optimistic tone, saying, “We think the economy, and our policies, are both in a very good place.”

For us investors, a lower rate combined with a strong economy is a win-win. Lower interest rates make it cheaper for businesses to borrow, which can lead to more growth and potentially higher profits. This often gives the stock market a boost, as investors shift towards stocks when bonds and savings accounts offer lower returns.

For Canadian investors with exposure to US markets, rising prices in American stocks could lead to gains, and since our markets often follow the US, we might see some positive movement here in Canada too.

So, for long-term investors, rate cuts can create some exciting opportunities for growth – something I am always happy to see. 😊

Consumer Sentiment Index (CSI)

The University of Michigan’s preliminary consumer sentiment reading came in higher than expected, climbing to 73.0—the highest reading since April—up 3.5% from October’s 70.5. Analysts had predicted a reading of 71, so this improvement was a welcome surprise. Year-over-year, sentiment has surged by over 19% from last November’s 61.3, marking the fourth consecutive month of rising optimism among consumers.

Looking at the details, the Current Economic Conditions index, which measures how consumers feel about their current financial situation, dipped slightly by 0.8% from October’s 64.9 to 64.4, and is down 5.7% from a year ago when it stood at 68.3. On the other hand, the Index of Consumer Expectations, which reflects how people feel about the future, jumped from 74.1 to 78.5—its highest point since the summer of 2021, reflecting a solid 5.9% increase. Year-over-year, this component has surged by 38.2% from 56.8, signaling growing confidence in job prospects, a stable economy, and easing inflation.

This positive trend in consumer sentiment suggests that optimism is building, which could help support ongoing economic growth in the months ahead.

American market volatility

The CBOE Volatility Index (VIX), also known as the market’s “fear gauge,” started the week at 21.84 but took a sharp dive following the US election, dropping into the 15-16 range, and finally closing the week at 14.94. This post-election plunge marked the biggest drop since August. Adding to the calm, the Fed’s recent rate cut helped ease investor concerns and further smoothed the market’s nerves.

For some context, the VIX tracks expected market volatility over the next 30 days. When it is below 12, it signals a calm market. Readings between 12 and 20 reflect normal market swings. But once the VIX climbs into the 20-30 range, it signals growing uncertainty. Anything above 30 typically means the market is stressed, often a precursor to major turbulence or even a crisis.

New sheriff in town: What Long-Term Investors Need to Know Post-US Election

Technically, this is political news rather than economic news, but it will undoubtedly impact the American economy, and as the world’s largest economy, that effect will ripple through global markets.

As you have probably heard, Donald Trump is heading back to the White House. This time, the Republicans are not just in control of the presidency – they have secured both the Senate and the House of Representatives. When one party controls the White House and both chambers of Congress, like the Republicans do now, it often leads to a more predictable policy environment. With less gridlock, it becomes easier to pass laws and policies – something markets tend to appreciate.

That said, market reactions will depend on the specifics of the policies Republicans put forward. Changes to trade agreements, government spending, or social programs could create shifts that impact different sectors in varying ways. For example, traditional energy might benefit, while sectors like green energy or healthcare could face more challenges, depending on the agenda.

For us long-term investors, it is crucial to focus on the bigger picture rather than getting swept up by short-term political waves. While power shifts, like Republicans winning the White House and both chambers of Congress, may cause market reactions, long-term growth is driven by fundamentals – company earnings, economic trends, and overall market performance.

Here are a few key points long-term investors should keep in mind:

- Stick to Your Strategy: If you have a well-diversified portfolio, there is no need to make drastic changes just because of political outcomes. A disciplined, long-term approach helps you avoid emotional, reactionary moves in the market.

- Monitor Policy Changes: While you should not overhaul your portfolio based solely on elections, it is wise to keep an eye on major policy shifts, especially around taxes, regulations, and trade. These can create both opportunities and risks in specific industries.

- Diversify Across Sectors: If you are worried about how new policies might impact certain sectors, ensure your portfolio is spread across a range of industries. This way, you are not overly exposed to one area that could be affected by political changes.

- Focus on Fundamentals: In the long run, a company’s performance, earnings growth, and broader economic trends will matter more than short-term political shifts. Keeping your focus on these key indicators will help you make informed, long-term decisions.

- Stay Patient: Political cycles will come and go, but long-term investors benefit the most from riding out short-term volatility. Stick with investments that have strong growth potential over time.

In short, while political changes can shake up certain sectors and cause short-term market movements, the best strategy is to stay steady, diversified, and focused on the long-term horizon.

With the political landscape in the US shifting, it is important to remember that market movements are influenced by many factors beyond politics, including this week’s announcements from the Fed.

Covered Calls

This past week, I placed my first ‘covered call’ in over five years. I had almost forgotten about this strategy, but it is a smart way to generate extra income from stocks you already own.

If you are new to investing, covered calls might not be the best fit just yet. Your focus should be on buying great companies that you would be proud to own long term. Once you have a handle on that, options trading – like covered calls – could be worth exploring. That said, many investors do not use options at all, so sticking with solid stock picks and letting them grow in value is perfectly fine. Personally, the only type of options trading I do is covered calls. If you are curious, here is my take on how they work:

What is a Covered Call?

A covered call is when you own shares of a stock and sell a call option on them. The “covered” part means you already own the shares, so if the option buyer decides to buy the stock at the agreed price (the strike price), you are prepared to sell.

In simple terms, you are giving someone the right to buy your stock at a set price by a certain date, and in return, you get paid a premium—like rent for your shares. If the stock does not reach that price, you keep both the shares and the premium.

How Does it Help Grow Wealth?

The idea behind a covered call is to create extra income from stocks you already own. You still benefit from any dividends or stock price growth, but you also get the premium from selling the call option. It is a way to boost your returns, especially in flat or mildly rising markets where the stock price is not moving dramatically.

Pros of Covered Calls:

- Extra Income: You collect a premium, adding some cash flow to your portfolio.

- Reduced Risk: The premium helps offset potential losses if the stock price drops.

- Control Over Selling: You choose the strike price, meaning you only sell if the stock reaches a price you are prepared to sell at.

Cons of Covered Calls:

- Capped Upside: If the stock soars past your strike price, you miss out on those gains since you are obligated to sell at the lower price.

- Stock Ownership Risk: You still own the stock, so if the price falls significantly, the premium may not fully cover your loss.

- Limited Growth: In fast-growing markets, covered calls can limit your profits if the stock takes off.

When to Use a Covered Call

Covered calls are a solid strategy if you expect the stock to stay flat or rise gradually. They are not ideal for high-growth situations, but they can help generate extra income while you hold onto your shares in calmer markets. In my case, I was looking to trim my position in a company and the share price was already close to the price I was prepared to sell at. By writing a covered call, I am not only giving someone the option to buy at my price, but I also get paid a premium for giving them that right. So, if the stock hits my target, I will get the price I want plus the extra cash from the premium. Not a bad deal at all. 😊

In summary, covered calls can be a smart strategy for boosting your income, but they do come with trade-offs, especially when it comes to limiting your upside potential if the stock price jumps.

Weekly Market Review

Monday: the markets led off what looks to be a volatile week with a mixed bag, the Toronto Stock Exchange Composite Index (TSX) ended in the green while the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) all ended in the red. An uncertain presidential election and a rate announcement by the Fed has investors on edge and happy to remain on the sidelines. Oil prices surged after OPEC+, the Organization of the Petroleum Exporting Countries plus Russia and other allies, announced they would delay increasing monthly output by 180,000 barrels per day.

In Canada, higher oil prices was the main reason the TSX was able to avoid a loss. In trading, the Energy sector advanced the most, while Communications Services dropped the most.

In the US, investors were feeling the jitters ahead of tomorrow’s election, with its widespread consequences likely to shake up the markets. In trading, the Energy sector posted the biggest gain, while the Utilities sector recorded the biggest loss.

Tuesday: the markets rallied on election day, pushing all four indexes into positive territory, as investors wait for today’s election results. Oil prices also got a slight boost on news that storms in the Gulf of Mexico could lower US oil output.

In Canada, the TSX extended its winning streak to three days, despite the country reporting a higher-than-expected trade deficit of C$1.26 billion. The deficit was driven by falling prices, despite a rise in export volumes for September. In trading, the Utilities sector posted the largest increase, while Consumer Cyclicals recorded the largest loss.

In the US, all three indexes each gained at least 1% on positive economic data. In trading, Consumer Cyclicals was the big winner for the day, while Basic Materials (miners and fertilizer manufacturers) suffered the biggest decline.

Wednesday: it seems the markets approve of the US elections, as all four major indexes surged over 1%, sparking a global rally. Oil prices rose slightly as investors feel the new administration could lead to tighter supplies.

In Canada, the TSX also rode the tailwinds of the Republican victory, as investors caught the positive sentiment coming from the US. In trading, the Technology sector advanced the farthest, while Healthcare suffered the largest loss.

In the US, the three major indexes each surged over 2%, with each hitting new all-time highs as investors reacted positively to the prospect of a Republican-led government. The Dow and S&P 500 posted their largest one-day percentage gains since November 2022, while the Nasdaq saw its biggest daily jump since February. In trading, the Financials sector gained the most, while Consumer Staples declined the furthest.

Thursday: the post-election rally continued, boosted by a 0.25% rate cut from the Fed, pushing three of the four major indexes higher. The only exception was the DJIA, which ended the day right at the same level as it began.

In Canada, with the uncertainty of the US elections removed, and an interest rate reduction in the US, the TSX was lifted to a new all time high. In trading, Basic Materials rose the farthest, while Communication Services sank the furthest.

In the USA, investor optimism that the incoming government will be better for business, combined with the interest rate cut, propelled the S&P and Nasdaq to new record highs. In trading, Communication Services advanced the most, while Financials dropped the farthest.

Friday: investor optimism continued to push US indexes to new heights, while protectionist worries weighed on the TSX. Oil prices slipped after disruptions from Gulf of Mexico hurricanes, adding to market concerns.

In Canada, the TSX snapped its five-day winning streak amid concerns over potential tariffs from the Trump administration, which could hit Canada’s economy hard. The latest labour report also fell short of expectations, adding to the downside. On Bay Street, Utilities led the charge with the biggest gains, while Basic Materials took the hardest hit.

In the USA, election momentum lifted all three major indexes, with the S&P and Nasdaq stretching their daily win streaks to four. The DJIA soared above 44,000 for the first time, and the S&P briefly passed 6,000 before both pulled back toward the day’s end. In trading, Utilities had the strongest performance, while Basic Materials lagged behind.

Weekly Market and Portfolio Review

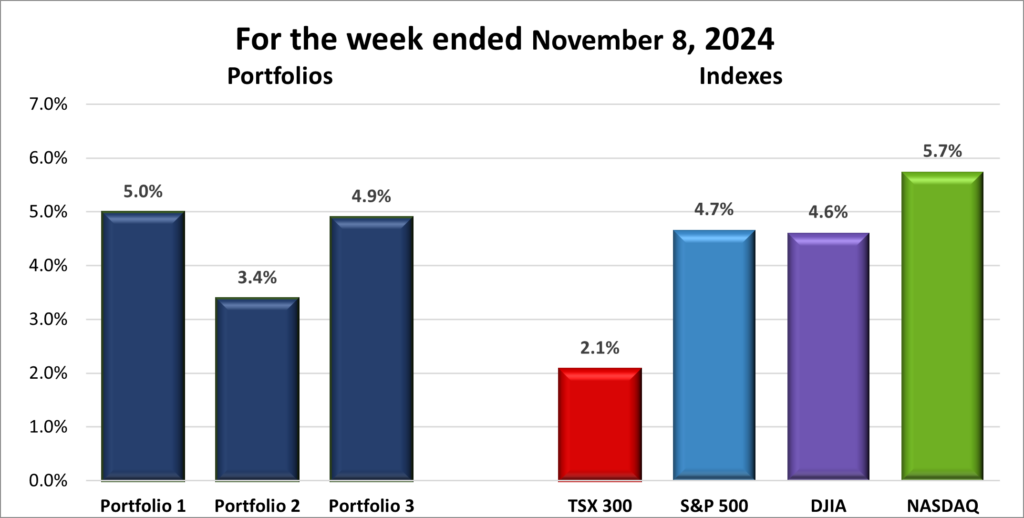

For the week, the TSX (SPTSX) gained 2.1%, the S&P 500 (SPX) rose 4.7%, the DJIA (INDU) advanced 4.6% and the Nasdaq (CCMP) surged 5.7%.

| Index | Weekly Streak |

| TSX: | 1 – week winning streak |

| S&P: | 1 – week winning streak |

| DJIA: | 1 – week winning streak |

| Nasdaq: | 1 – week winning streak |

![]() It was an eventful week in the markets, with the US election and a second rate cut in the US fueling a strong rally, as illustrated in the chart above. It’s not often a Fed decision takes a back seat, but election buzz stole the spotlight, even prompting the Fed to delay its meeting by a day.

It was an eventful week in the markets, with the US election and a second rate cut in the US fueling a strong rally, as illustrated in the chart above. It’s not often a Fed decision takes a back seat, but election buzz stole the spotlight, even prompting the Fed to delay its meeting by a day.

The US election emerged as the main catalyst behind the market’s best week of the year. As the potential for a Republican sweep came into focus (with the House still undecided, as of this writing), optimism surged. Investors started pricing in expectations for tax cuts and deregulation, while a late-week rate cut from the Fed added more fuel to the rally. The Fed also highlighted that although the labour market had slowed, the economy remained stable, with steady progress being made toward its 2% inflation goal. As uncertainty around a divided government faded (and markets love clarity 😊), investor confidence soared.

The prospect of pro-business policies pushed major indexes to new highs. The DJIA briefly touched 44,000 before closing just shy at 43,988.99, while the S&P crossed 6,000 before pulling back, still able to log its 50th record close this year. Both indexes saw their best performance since a year ago. Not to be left out, the Nasdaq set record highs for three straight days.

In Canada, optimism from the American markets spilled over, lifting the TSX to a record high. However, the rally cooled as concerns about potential US tariffs surfaced. Given America is Canada’s largest trading partner, such tariffs could hit the commodities-heavy economy hard. Analysts warn these measures, if enacted, could reduce Canada’s GDP by 1.7% by 2028.

Currently, the markets are riding the post-election and rate cut tailwinds to new heights. However, it’s important to remember that they can’t rise every day, and volatility is always a possibility. But for now, the optimism around potential pro-business policies and the Fed’s actions provides a solid foundation for growth. I’m definitely happy to ride these tailwinds and see the markets rally to new heights. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week winning streak |

| Portfolio 2: | 1 – week winning streak |

| Portfolio 3: | 1 – week winning streak |

![]() This past week’s rally, gave all three portfolios a solid boost, as seen in the chart below. At least 72% of the holdings in each portfolio recorded gains for the week.

This past week’s rally, gave all three portfolios a solid boost, as seen in the chart below. At least 72% of the holdings in each portfolio recorded gains for the week.

Portfolio 1 stole the show, with 75% of its companies in the green, including a gain by Nvidia (NASD: NVDA), the portfolios biggest holding. Several heavyweights hit all-time highs, including Amazon (NASD: AMZN), Liberty Media’s Formula 1 (NASD: FWONK), Visa (NYSE: V), and Walmart (NYSE: WMT). Despite a 16% drop from Innovative Industrial Properties Inc. (NYSE: IIPR), the portfolio easily shook it off with indie Semiconductor Inc. (NASD: INDI) skyrocketing 57% and Celestica Inc. (TSE: CLS) jumping 21%. Shopify (TSE: SHOP) and Carnival Corp. (NYSE: CCL) both gained 11%, with CrowdStrike (NASD: CRWD) and Magnite Inc. (NASD: MGNI) each adding 10%.

Portfolio 2 had what would typically be a standout week, but it lagged behind the others with a ‘measly’ 3.4% gain. 😊 Still, 77% of its holdings posted gains, with Guardant Health (NASD: GH) up 28% and iAG Financial (TSE: IAG) climbing 13%. Both iAG Financial and Dollarama (TSE: DOL) hit all-time highs, adding some strong momentum.

Portfolio 3 had a strong week as well, though it was bested by Portfolio 1’s performance. With 72% of its holdings advancing, Vertiv Holdings (NYSE: VRT) surged 18% to hit an all-time high, Shopify gained 11%, and Magnite added 10%. While Adyen (OTCM: ADYEY) slipped 10%, the overall gains easily kept the portfolio in comfortable positive territory.

A fantastic week across the board! I will happily take these kinds of gains week after week.

Companies on the Radar

Still no new additions to my radar list this past week. That said, I am debating whether it is better to invest in a new company or add to one of the existing positions in my portfolios. For now, my radar list remains focused on the three companies below:

Still no new additions to my radar list this past week. That said, I am debating whether it is better to invest in a new company or add to one of the existing positions in my portfolios. For now, my radar list remains focused on the three companies below:

- On Holding AG (NYSE: ONON), a medium cap Swiss company, founder-run, sports products company.

- Topaz Energy Corp. (TSE: TPZ), a mid-cap Canadian energy investment firm that focuses on strategic investments in premium energy assets operated by top-tier Canadian companies, and currently pays a 4.95% dividend.

- Zoetis Inc. (NYSE: ZTS), a leading animal health company that discovers, develops, manufactures, and commercializes vaccines, medicines, diagnostics, and other technologies for both companion animals and livestock.

As always, these are not buy recommendations – be sure to do your own research and make decisions that align with your personal financial goals!

The Radar Check was last updated November 8, 2024.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended November 8, 2024: UP ![]()

- BCE (TSE: BCE) announced they planned to purchase private American internet services provider Ziply Fiber for C$5 billion. BCE plans to use the acquisition as a means of increasing their presence in the US market.

Activity

Sold: Nvidia If you’ve been following my ‘Weekly Updates,’ you know Nvidia has been the star player in this portfolio, often determining whether it ends the week in the green or red. Riding Nvidia’s artificial intelligence tailwind has been amazing so far, but with its stock becoming such a dominant part of the portfolio, it was time to take some risk off the table. You have probably heard me mention that I need to trim my Nvidia position to avoid having the portfolio’s performance hinge on just one stock. Well, this week, I finally took action—or rather, I set the wheels in motion. Let me explain.

At first, I was planning to place a simple ‘Sell’ order for X shares at $150, good until the end of November. But then I had a better idea—why not write a covered call? With a covered call, instead of just selling the shares, I get paid a premium upfront for the option. Essentially, I am agreeing to sell those shares if Nvidia hits $150, but in the meantime, I get paid for waiting.

Since I was already comfortable selling at $150, getting that extra premium felt like a win-win. Now, if Nvidia reaches that price, I will sell as planned, but with a little bonus on top. If it does not, I keep the premium and the shares. Either way, it is a smart way to trim my position while putting some extra cash in my pocket. 😊

Sold: Lightspeed Commerce (TSE: LSPD) I first invested in Lightspeed Commerce back in September 2019, and I added more to my position when the stock started to soar in January 2020. Like many technology stocks, Lightspeed took off during the pandemic, rallying through 2021 and hitting a high of $150. Unfortunately, I did not lock in those gains when I had the chance. Instead, I held on and watched the stock slide all the way down to its current level in the low $20s. ☹

As part of my ongoing effort to streamline this portfolio, Lightspeed became an obvious choice to sell. The company continues to face profitability challenges and has a long road ahead to turn things around. Given these factors, I do not see the stock returning to its 2021 highs anytime soon. With better opportunities out there, I decided it was time to cut my losses—admittedly, much later than I should have.

Dividends

Dividends Received this week for the following companies:

No dividends this past week.

Quarterly Reports

Berkshire Hathaway Inc.

Third quarter 2024 financial results on November 2, 2024

Navitas Semiconductor Corporation

Third quarter 2024 financial results on November 4, 2024

Lattice Semiconductor Corporation

Third quarter 2024 financial results on November 4, 2024

Decisive Dividend Corporation

Third quarter 2024 financial results on November 5, 2024

Andlauer Healthcare Group Inc.

Third quarter 2024 financial results on November 5, 2024

Ferrari N.V.

Third quarter 2024 financial results on November 5, 2024

Celsius Holdings, Inc.

Third quarter 2024 financial results on November 6, 2024

Atlanta Braves Holdings, Inc.

Third quarter 2024 financial results on November 6, 2024

Innovative Industrial Properties, Inc.

Third quarter 2024 financial results on November 6, 2024

Tourmaline Oil Corp

Third quarter 2024 financial results on November 6, 2024

Supremex Inc.

Third quarter 2024 financial results on November 6, 2024

Cameco Corporation

Third quarter 2024 financial results on November 7, 2024

Pinterest, Inc.

Third quarter 2024 financial results on November 7, 2024

BCE Inc.

Third quarter 2024 financial results on November 7, 2024

indie Semiconductor, Inc.

Third quarter 2024 financial results on November 7, 2024

Cloudflare, Inc.

Third quarter 2024 financial results on November 7, 2024

Datadog, Inc.

Third quarter 2024 financial results on November 7, 2024

Rivian Automotive, Inc.

Third quarter 2024 financial results on November 7, 2024

Magnite, Inc.

Third quarter 2024 financial results on November 7, 2024

The Trade Desk, Inc.

Third quarter 2024 financial results on November 7, 2024

Telus Corporation

Third quarter 2024 financial results on November 7, 2024

Trisura Group Ltd.

Third quarter 2024 financial results on November 7, 2024

Docebo Inc.

Third quarter 2024 financial results on November 8, 2024

Portfolio 2

Portfolio 2 for the week ended November 8, 2024: UP ![]()

- The Walt Disney Company (NYSE: DIS) is being sued by technology company Adeia (NASD: ADEA) for infringing on six of its streaming technology patents. Adeia claims Disney’s Hulu, ESPN+ and Disney+ business units used their technology to improve their streaming services.

Activity

Sold: Bank of Nova Scotia (TSE: BNS) This investment had grown to almost 45% of my portfolio—putting way too many eggs in one basket. 😊 That single stock had become too dominant, making the portfolio vulnerable to its ups and downs. By selling some shares, I now have cash to invest in new opportunities or to add to my existing holdings. Rebalancing not only lowers my risk but also helps protect against overall portfolio volatility caused by one company.

Dividends

Dividends Received this week for the following companies:

No dividends this past week.

Quarterly Reports

iA Financial Corporation Inc.

Third quarter 2024 financial results on November 5, 2024

Fortis Inc.

Third quarter 2024 financial results on November 5, 2024

Tourmaline Oil Corp.

See report under Portfolio 1.

Take-Two Interactive Software, Inc.

Third quarter 2024 financial results on November 6, 2024

Guardant Health, Inc.

Third quarter 2024 financial results on November 6, 2024

Brookfield Infrastructure Partners L.P.

Third quarter 2024 financial results on November 6, 2024

TC Energy Corporation

Third quarter 2024 financial results on November 7, 2024

Airbnb, Inc.

Third quarter 2024 financial results on November 7, 2024

Telus Corporation

See report under Portfolio 1.

Brookfield Renewable Partners L.P.

Third quarter 2024 financial results on November 8, 2024

Portfolio 3

Portfolio 3 for the week ended November 8, 2024: UP ![]()

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

No dividends this past week.

Quarterly Reports

Brookfield Asset Management Ltd.

Third quarter 2024 financial results on November 4, 2024

Lithium Americas (Argentina) Corp.

Third quarter 2024 financial results on November 5, 2024

Alvopetro Energy Ltd.

Third quarter 2024 financial results on November 6, 2024

Magnite, Inc.

See report under Portfolio 1.

goeasy Ltd.

Third quarter 2024 financial results on November 7, 2024

Lithium Americas Corp.

Third quarter 2024 financial results on November 7, 2024

Cloudflare, Inc.

See report under Portfolio 1.

TELUS Digital Experience

Third quarter 2024 financial results on November 8, 2024

Brookfield Renewable Partners L.P.

See report under Portfolio 2.