Buffett Goes to Japan: Why Berkshire Bought Into 5 Giant Trading Companies

A few years back, Warren Buffett made headlines – not by adding more Apple (NASD: AAPL) or Coca-Cola (NYSE: KO) to Berkshire Hathaway’s (NYSE: BRK.B) portfolio, but by putting billions into five Japanese companies most people outside Japan had barely heard of. These weren’t flashy tech stocks or hot new startups. They were century-old industrial titans known in Japan as sōgō shōsha – general trading companies that do a little bit of everything.

From metals and energy to food, finance, and even convenience stores, these trading houses are quietly woven into the fabric of the global economy. And Buffett, always a fan of strong cash flow and solid management, saw something special in them.

Let’s take a closer look at the five companies Berkshire invested in – and what made them attractive to Buffet.

Heads up: When you see TSE in this article, we’re talking about the Tokyo Stock Exchange, not the Toronto Stock Exchange. Same abbreviation, different continent. Since this article is all about Japanese companies, TSE = Tokyo here.

The second ticker listed for each company, the ones starting with the OTCM prefix, refers to their American Depositary Receipts (ADRs). These are traded over-the-counter in the US, making them accessible to North American investors without having to buy directly on the Tokyo Stock Exchange. While ADRs often represent a fraction of a share and may have lower trading volume than local listings, they’re still a practical way to gain exposure to these Japanese conglomerates.

The Big Five: Japan’s Trading Giants

Itochu Corporation (TSE: 8001 | OTCM: ITOCY)

Itochu is the most consumer-focused of the bunch, with business lines in food, fashion, tech, and finance. It also owns a major stake in FamilyMart, one of Japan’s largest convenience store chains.

Why Itochu: Highly efficient, well-managed, and super friendly to shareholders. A steady cash generator with global reach.

Marubeni Corporation (TSE: 8002 | OTCM: MARUY)

Marubeni is involved in everything from power plants and food trading to infrastructure and chemicals. It’s less of a household name, but its global reach is impressive.

Why Marubeni: It was undervalued and improving its profitability – an under-the-radar value play.

Mitsubishi Corporation (TSE: 8058 | OTCM: MSBHF)

The biggest and best-known of the five. Mitsubishi handles liquid natural gas (LNG), metals, finance, real estate, and much more. Think of it as Japan’s mega-conglomerate.

Why Mitsubishi: Diversified, stable, and built for the long haul. A blue-chip within a blue-chip.

Mitsui & Co., Ltd. (TSE: 8031 | OTCM: MITSY)

Mitsui has a global footprint in energy, mining, and chemicals, with projects ranging from Australian LNG terminals to US healthcare services.

Why Mitsui: Consistent long-term growth, strong cash flow, and a firm grip on global operations.

Sumitomo Corporation (TSE: 8053 | OTCM: SSUMY)

Rooted in steel and machinery, Sumitomo has been expanding into renewables and real estate. It’s evolving while staying true to its industrial roots.

Why Sumitomo: Conservative, reliable, and positioned to deliver long-term returns.

Why Buffett Looked Beyond North America

Buffett usually sticks close to home, so this move to Japan raised eyebrows. But it followed his timeless strategy: find great businesses at fair prices, no matter where they are. Here’s what made these companies so appealing:

- Low valuations + solid dividends: These firms were trading at low price-to-earnings ratios and offering healthy dividend yields – classic Buffett bait.

- Global diversification: Each company operates worldwide, giving Berkshire exposure to commodities, infrastructure, and emerging markets.

- Strong leadership: Buffett praised their management teams for being smart with capital and running tight ships.

- Currency edge: Berkshire financed the purchases in yen, providing a natural hedge against the US dollar – and likely benefiting from Japan’s low interest rates.

- Shareholder-friendly reforms: Japanese companies have been shifting toward better returns for investors, including buybacks – something Buffett loves.

- Long-term play: Buffett has said he plans to hold these positions indefinitely and may even boost his stake.

The Big Picture

This wasn’t a pivot – it was Buffett doing what he’s always done: buying great businesses with solid fundamentals at reasonable prices. Only this time, he found them in Japan, not America.

For us everyday investors, it’s a great reminder that opportunity isn’t limited to North America. There’s a whole world of potential out there—and sometimes, the most dependable businesses are quietly thriving halfway around the globe.

Now that we’ve looked at potential investments halfway across the globe, let’s turn our attention back home to what moved the markets this past week.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Gross Domestic Product (GDP)

Canada’s economy returned to modest growth in March, expanding by 0.1% after slipping 0.2% in February, according to Statistics Canada. The bounce was supported by gains across both goods-producing and services-producing industries – an encouraging sign of broad-based resilience.

The biggest lift came from the mining, quarrying, and oil and gas sector, which jumped 2.2% on the month. On the flip side, the management of companies and enterprises category saw the steepest drop, falling 4.4%.

Over the past year, GDP grew 1.7% – a touch higher than the 1.6% year-over-year growth seen in February. The energy sector once again led the pack with a 4.4% annual increase, while the management sector plunged 30.3% compared to a year ago.

Looking ahead, early estimates suggest GDP grew another 0.1% in April, pointing to a slow but steady economic expansion heading into the second quarter.

On a quarterly basis, Canada’s economy grew at an annualized rate of 2.2% in the first quarter of 2025, beating expectations of 1.7%. Quarterly GDP rose 0.5%, matching the previous quarter’s pace.

Much of that growth came from a 1.6% jump in goods exports – especially in passenger vehicles and industrial machinery – as businesses rushed to ship products ahead of expected US tariffs. That urgency also drove up imports, creating a temporary surge in trade activity.

This “rush to ship” dynamic helped inflate GDP, but it wasn’t driven by long-term demand. Instead, it reflected timing shifts and inventory stockpiling that are unlikely to repeat in the second quarter.

With the tariff-related boost now fading, many analysts expect growth to cool, with forecasts for second-quarter GDP hovering around 0.5% annualized.

Canadian market volatility

Canada’s market mood ring – the S&P/TSX 60 Volatility Index (VIXC) – started the week at 14.73 and drifted lower as optimism grew. By week’s end, it had settled at 10.41. Hopes that key trade deals would come through, along with strong earnings from Canada’s big six banks, helped cool investor nerves and bring the VIXC down.

For those unfamiliar with the VIXC, it’s essentially Canada’s version of a fear gauge. Readings under 10 show strong investor confidence, 10–20 is business as usual, and anything above 20 suggests investors are getting uneasy.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Federal Open Market Committee (FOMC) minutes

This week, the Fed released minutes from its May 6–7 FOMC meeting, providing a clearer look at how officials were thinking about interest rates and the broader economy.

As expected, the Fed held its key rate steady at 4.25%–4.50% while it continues to monitor inflation. What stood out, though, was the decision to slow the pace of balance sheet reduction. In simple terms, the Fed is easing up on how much money it’s pulling out of the financial system – something that could help stabilize markets and reduce the risk of sudden shocks. (Mind you, some of those shocks do present “buying the dip” opportunities. 😊)

The overall tone from Fed Chair Jerome Powell and others was cautious. Officials acknowledged they could face “difficult trade-offs” ahead if inflation stays high while unemployment rises. For now, they’re sticking to a “wait-and-see” strategy, holding off on any major policy changes. But with inflation still running above the Fed’s 2% target – and trade tariffs adding extra pressure – markets are already speculating about a potential rate cut later this year.

For us investors, the key takeaway is that Fed decisions ripple through the economy. If rates stay elevated, borrowing remains expensive and growth could slow. But if the Fed signals future cuts, it could encourage more investment and spending – potentially giving markets a lift. A cut sooner rather than later wouldn’t hurt. 😊

Consumer Confidence Index (CCI)

American consumers are feeling a lot better about where the economy is headed, and that positive vibe should give markets a lift. The Conference Board’s CCI bounced back in May, rising to 98.0 from 85.7 in April. That was more than a simple rebound, it’s the first increase in five months and the biggest monthly jump in four years. Analysts were expecting a more modest 86.5, so this beat was a pleasant surprise.

The Present Situation Index, which reflects how people feel about current business and job conditions, inched up to 135.9 from 131.1, a sign that many still see the economy as holding steady. But the biggest increase was in the Expectations Index, which measures how people feel about the next six months. It surged to 72.8 from 54.4, a massive 17.4-point leap, and the biggest monthly gain since 2011. While it’s still below the key 80 level that typically signals recession risk, it’s a big step in the right direction.

The increase in optimism was sparked by relief over easing trade tensions. The May 12 pause on the US-China trade dispute paused many of the tariffs each side had levied on the other, reducing global uncertainty and boosting confidence that a trade deal could get done. Encouragingly, this lift in confidence was broad-based – cutting across age groups and political lines.

Good news for us investors: 44% of consumers now expect stock prices to rise over the next 12 months. That growing confidence could lead to stronger spending and investing ahead – positive signs for both the economy and the markets.

Gross Domestic Product (GDP)

The Commerce Department’s Bureau of Economic Analysis released its second estimate of first-quarter GDP. The US economy shrank by 0.2% in the first quarter, and tariffs played a big role in that decline. Businesses rushed to import goods ahead of impending tariffs, causing a massive surge in imports – the biggest trade-related drag on GDP in history. Because imports are subtracted from growth, this made the economy look weaker than it actually was.

At the same time, companies stockpiled inventory to prepare for higher costs and possible supply chain disruptions, which boosted inventory accumulation in the GDP report. While that helped offset some of the decline, it also means future demand might slow as businesses work through excess inventory.

The White House has since delayed or canceled some of the planned tariffs, easing fears of an immediate recession. But economists are watching closely to see how these trade policies will affect inflation, consumer spending, and overall economic growth in the coming months.

Compared to the previous quarter, the drop in GDP in the first quarter primarily reflected an increase in imports, a deceleration in consumer spending, and a downturn in government spending that were partly offset by upturns in investment and exports.

Personal Consumption Expenditures (PCE)

Inflation showed more signs of cooling in April, offering some relief to both consumers and policymakers. According to the Commerce Department, headline PCE ticked up just 0.1% for the month, matching expectations after remaining flat in March. On a year-over-year basis, prices rose 2.1%, down from March’s 2.3% increase and marking the slowest annual pace since September 2021. Analysts had forecast a 2.2% rise, so this undershoot adds weight to the idea that price pressures are gradually easing.

Core PCE – which strips out food and energy and is considered the Fed’s preferred inflation gauge – also rose 0.1% in April. On an annual basis, core prices were up 2.5%, a slight step down from 2.6% in March and right in line with forecasts. The steady cooling in core inflation helps support the broader disinflation narrative the Fed has been watching closely.

With inflation still above the Fed’s 2% target but moving in the right direction, this report strengthens the case for interest rate cuts later this year. That said, the full impact of President Trump’s new tariffs has yet to show up in the data. Some analysts warn that these trade measures could reverse recent gains, potentially pushing inflation closer to 3% in the months ahead. For now, the Fed is likely to stay cautious, waiting for more evidence that inflation is sustainably on its way down before making any moves.

Consumer Sentiment Index (CSI)

Consumer sentiment showed signs of stabilizing in May. The University of Michigan’s final reading of the CSI came in at 52.2 – matching April’s figure and marking the first time in four months that sentiment hasn’t declined. That’s up from the mid-month preliminary reading of 50.8 and ahead of the expected 51.0. While the bounce is encouraging, sentiment is still far from strong – the current reading is well below the 69.1 recorded in May 2024 and remains one of the lowest levels on record since the index began in 1952.

Looking closer, the Current Conditions Index, which gauges how consumers feel about their personal finances today, slipped slightly to 58.9 from 59.8 – a 1.5% drop from last month and 15.4% lower than a year ago. Rising prices and stagnant wages continue to weigh on household confidence. On the flip side, the Expectations Index – which reflects how consumers view the economic outlook over the next six months – ticked up to 47.9 from 47.3, a modest 1.3% gain. Still, that’s 30.4% lower year over year.

Inflation worries remain top of mind. Year-ahead inflation expectations edged up from 6.5% to 6.6%, while long-run expectations eased to 4.2% from April’s 4.4%, breaking a four-month streak of increases.

The late-month pickup in sentiment likely reflects some relief over the pause in tariffs with China. While that helped lift spirits a bit, the overall reading remains historically low, and when consumer sentiment stays this weak, it often points to softer spending ahead. That’s a key concern, given how much the US economy relies on consumer activity.

American market volatility

Wall Street’s “fear gauge,” the CBOE Volatility Index (VIX), started the week at an elevated 20.63 – just above its usual 12–20 range and down slightly from last week’s close of 22.35. By midweek, the VIX had slipped back under 20, hovering around 19 before ending the week at 18.57.

The pullback was helped by President Trump walking back his threat of a 50% tariff on the European Union, along with signs of improving consumer confidence – both of which helped calm investor nerves. Still, concerns about his proposed spending bill, which could add trillions to the already ballooning US debt, kept the VIX near the top of its typical range.

For anyone new to the VIX: it’s basically Wall Street’s stress meter. When investors grow uneasy, they tend to pull back from riskier assets, such as technology stocks, which can lead to sharper price swings and more unpredictable markets. That’s when the VIX tends to rise – capturing the surge in volatility and fear. A reading between 12 and 20 signals business as usual, while anything above 20 suggests growing anxiety. The higher it climbs, the more turbulence investors are expecting.

Weekly Market and Portfolio Review

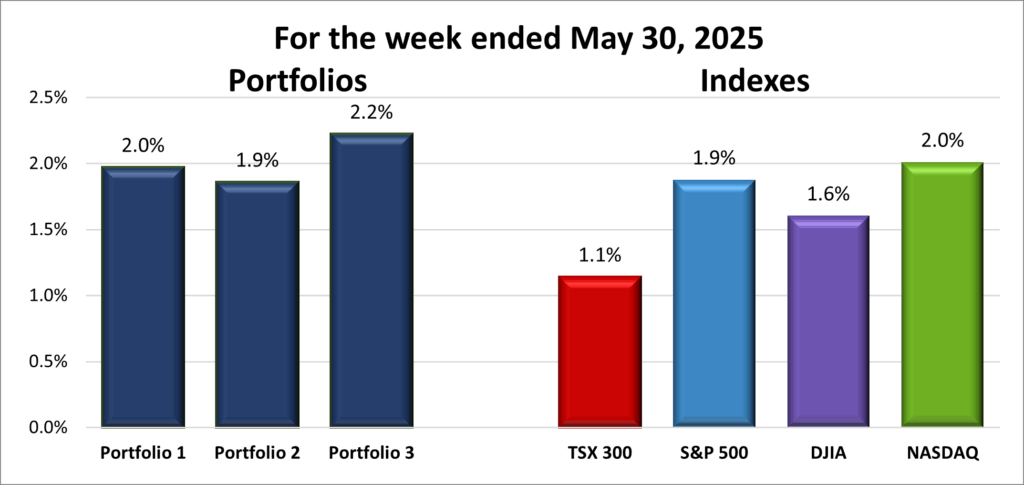

For the week, the TSX (SPTSX) advanced 1.1%, the S&P 500 (SPX) rose 1.9%, the DJIA (INDU) added 1.6% and the Nasdaq (CCMP) climbed 2.0%.

| Index | Weekly Streak |

| TSX: | 1 – week winning streak |

| S&P: | 1 – week winning streak |

| DJIA: | 1 – week winning streak |

| Nasdaq: | 1 – week winning streak |

![]() It’s always nice to see the indexes bounce back into the green. After the previous week’s slump, markets shook it off and rallied, with all four major indexes gaining at least 1%. The momentum came from a mix of factors: ongoing US tariff drama, Nvidia’s (NASD: NVDA) much-anticipated earnings release, and a wave of end-of-month economic data – including encouraging US inflation numbers.

It’s always nice to see the indexes bounce back into the green. After the previous week’s slump, markets shook it off and rallied, with all four major indexes gaining at least 1%. The momentum came from a mix of factors: ongoing US tariff drama, Nvidia’s (NASD: NVDA) much-anticipated earnings release, and a wave of end-of-month economic data – including encouraging US inflation numbers.

With US markets closed for Memorial Day on Monday, the Toronto Stock Exchange Composite Index (TSX), got a head start. Before the long weekend, President Trump made headlines by threatening the European Union (EU) with 50% tariffs, only to hit pause during the break. That rollback helped the TSX open the week on a strong note. Once American traders returned on Tuesday, they joined the rally, pushing the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) higher as hopes grew for a US – EU trade deal. If you’ve been following along, you’ll recognize the familiar playbook: Trump ramps up the tariff talk late in the week, then eases off by Monday. Markets are getting used to it – and this week, they responded accordingly.

Midweek, attention shifted to Nvidia. As the poster child of the artificial intelligence (AI) boom, Nvidia’s results are seen as a temperature check for the entire sector. The company didn’t disappoint – surpassing revenue expectations and showing that the AI spending spree is still going strong. That said, its guidance for next quarter was more cautious, with export restrictions to China expected to trim as much as US$8 billion from future revenue. CEO Jensen Huang struck an upbeat tone, highlighting strong demand for its new Blackwell AI chips and the long runway for AI infrastructure. Investors liked what they heard – Nvidia’s stock got a nice post-earnings boost.

While the spotlight was on Nvidia, trade tensions re-emerged that same day. The US Court of International Trade ruled that many of Trump’s global tariffs were illegal and must be halted within 10 days. Markets got a brief lift – until a federal appeals court allowed the tariffs to remain in place (for now), keeping trade tensions alive. The back-and-forth weighed on sentiment and reminded investors that tariff risks aren’t going away any time soon.

Heading into the weekend, Trump threw another wrench into the mix – this time accusing China of breaking its temporary trade truce with the US While he didn’t specify how China had violated the agreement, it’s believed to be related to delays in resuming exports of rare earth minerals – critical components for everything from semiconductors to electric vehicles. That rattled markets briefly, before he said he would speak directly with China’s President Xi to work out a deal – calming nerves a bit as the week wrapped up.

In Canada, the TSX got a boost from strong earnings by the Big Six banks. While results were solid, the banks are setting aside more cash for potential loan losses – a cautious signal about the economic outlook and the uncertainty surrounding US tariffs. Investors also welcomed signs of easing global trade tensions earlier in the week. Then on Friday, stronger-than-expected GDP data added a final touch of optimism. The Canadian economy grew at a 2.2% annualized pace in Q1, beating forecasts. But much of that came from a temporary surge in exports as companies rushed to beat new tariff deadlines – making it unlikely to be repeated in the second quarter

All in all, markets got the rebound they were hoping for, even if trade tensions continue to hover in the background.

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week winning streak |

| Portfolio 2: | 1 – week winning streak |

| Portfolio 3: | 1 – week winning streak |

![]() While it was nice to see the indexes back in the green, it was even better watching all three of my portfolios bounce back with solid gains across the board. Two of them outpaced the major benchmarks, and the third kept pace with the week’s top performer – as shown in the weekly performance chart below.

While it was nice to see the indexes back in the green, it was even better watching all three of my portfolios bounce back with solid gains across the board. Two of them outpaced the major benchmarks, and the third kept pace with the week’s top performer – as shown in the weekly performance chart below.

Portfolio 1 had a strong week, posting a 2.0% gain with 79% of its holdings finishing higher. Outside of Navitas Semiconductor (NASD: NVTS), which popped 11%, there weren’t any standout surges – but the broad-based gains helped push the portfolio ahead of all the indexes. The largest holding, Nvidia, also chipped in with a decent move. 😊

Portfolio 2 came in third, with a 1.9% gain and 74% of holdings finishing the week higher. Highlights included Dollarama (TSE: DOL) hitting an all-time high and Guardant Health (NASD: GH) climbing 11%. Energy companies were the main drag here, as all of the oil and gas holdings ended in the red due to lower global oil prices.

Portfolio 3 had the best weekly performance of all the portfolios and all the indexes, posting a 2.2% gain, also with 74% of holdings in the green. No major standouts this week – just steady strength across the board.

All in all, a strong rebound week for my portfolios, and a great way to close out the month. 😊

Companies on the Radar

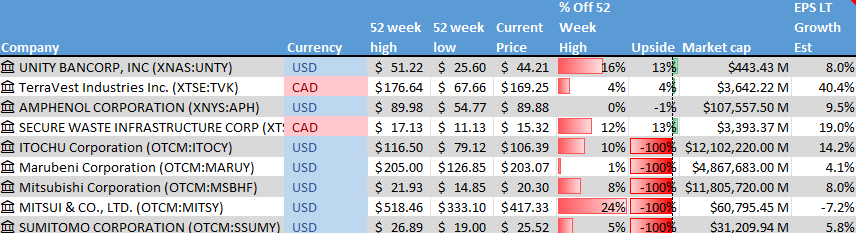

This week’s radar list got a bit of a shake-up. I dropped WisdomTree (NYSE: WT) from the list, and no new North American companies made the cut. Instead, I added the five Japanese trading giants Berkshire Hathaway invested in – mentioned earlier in this Weekly Update.

This week’s radar list got a bit of a shake-up. I dropped WisdomTree (NYSE: WT) from the list, and no new North American companies made the cut. Instead, I added the five Japanese trading giants Berkshire Hathaway invested in – mentioned earlier in this Weekly Update.

- Itochu Corporation

- Marubeni Corporation

- Mitsubishi Corporation

- Mitsui & Co., Ltd.

- Sumitomo Corporation

On the surface, these companies look like solid long-term bets: diversified, global reach, and Buffett-approved. But once I dug deeper, things got more complicated. Currency fluctuations can eat into returns, and Japan’s economy has its own challenges, including periods of slow growth. The ADRs make these stocks accessible in North America, but they can come with tax quirks and lower liquidity, which isn’t ideal for efficient trading. Plus, governance standards and disclosure norms in Japan differ from what we’re used to here, which adds another layer of complexity.

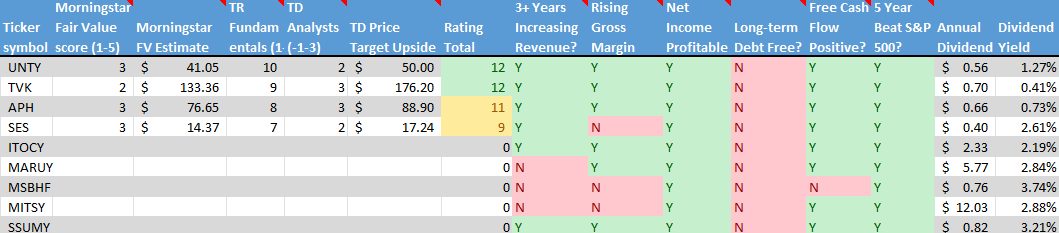

None of these are dealbreakers, but they are real risks that investors should consider. For me, the biggest challenge was the lack of reliable research. I used Finchat.io and Yahoo! Finance to dig up the basics, but I couldn’t access key metrics like Morningstar’s Fair Market Value or analysts’ ratings through TD Direct Investing, as you can see in the second part of the chart below. Without those tools, I couldn’t get a solid enough read to feel confident. So for now, these companies are a pass for me, not because they aren’t promising, but because they fall into my personal ‘too hard’ pile.

Joining the five Japanese companies on the list this week are these four holdover from last week:

- Unity Bancorp (NASD: UNTY) is a small-cap regional bank based in the US, serving parts of New Jersey and Pennsylvania. It’s showing strong fundamentals, including solid revenue growth, efficient capital use, and double-digit earnings expansion. Earnings per share is expected to climb nearly 13% this year – matching industry averages – and it has a steady history of dividend increases.

- TerraVest Industries (TSE: TVK) is a Canadian mid-cap industrial company that manufactures equipment for the energy, agriculture, and transportation sectors across North America. Its product lineup includes propane tanks, specialized tanks used to store and transport ammonia gas commonly used as fertilizer (anhydrous ammonia vessels), natural gas liquids transport vehicles, and a range of energy processing equipment.

- Amphenol Corporation (NYSE: APH), a global giant in the connector and cable business, supporting a wide range of industries with electrical, electronic, and fiber optic solutions.

- Secure Energy Services (TSE: SES) is a Canadian mid-cap industrial company focused on waste management and energy infrastructure. They serve clients across North America with recycling, disposal, and environmental solutions – a solid pick in the sustainability and infrastructure space.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals. That goes double when it comes to foreign-listed companies. 😊

The Radar Check was last updated May 30, 2025.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!