Bigger Slices of the Pie: Understanding Share Buybacks

While going through the latest batch of quarterly reports, I noticed quite a few companies announcing share buyback programs. If you’re new to investing, that might not sound like much, but buybacks can actually be a very shareholder-friendly move. So this week, let’s talk about what they are and how they can benefit us as investors.

A share buyback happens when a company uses its own money to repurchase some of its stock from the market. Those shares are then cancelled or tucked away in the company’s treasury, leaving fewer shares available for the public to own.

Think of it like a pizza. If you and three friends split one pie, each of you gets a quarter. But if one person leaves and the pizza stays the same size, your slice automatically gets bigger. Owning stock works the same way: when there are fewer shares, each share you own represents a larger slice of the company.

How buybacks benefit shareholders

- Earnings boost – With fewer shares in circulation, the company’s profits are spread across a smaller pool, often lifting earnings per share (EPS) and supporting the stock price.

- Price support – A company buying its own stock signals confidence in its future, and the added demand can help keep prices stable – or push them higher.

- Tax efficiency – Unlike dividends, which are taxed when you receive them, you only pay taxes on buybacks when you eventually sell your shares.

- A show of confidence – Management is essentially saying, “We think our stock is worth more than the market gives it credit for.”

Of course, not all buybacks are created equal. If a company overpays for its shares or borrows heavily to fund them, it can look good in the short term but hurt long-term value. Done wisely, though, buybacks can be a powerful way to return cash to investors without cutting into growth plans.

Good vs. Bad Buybacks: A Quick Checklist

- Financial health: Strong cash flow and low debt ✅ vs. borrowing to fund buybacks ❌

- Share price: Buying when the stock looks undervalued ✅ vs. chasing record highs ❌

- Impact: Reducing the share count meaningfully ✅ vs. buybacks so small they barely matter ❌

- Motives: Disciplined capital allocation ✅ vs. short-term EPS padding ❌

- Priorities: Growth and dividends already funded ✅ vs. cutting corners elsewhere ❌

- Net effect: Share count actually shrinks ✅ vs. just offsetting stock options ❌

Here’s the simple test: if buybacks are funded by healthy profits, reduce the share count, and come after other priorities are taken care of, they’re usually a good sign for shareholders.

The next time you’re skimming through earnings reports (you do read them, right? 😊), take a look at whether the company is planning to buy back shares. You can also check sites like Yahoo! Finance or Fiscal.ai to see if the number of outstanding shares is shrinking (a good sign) or growing (not so good).

Now that you’ve got a clearer picture of how buybacks work and why they matter, let’s shift gears and see how the markets performed this past week – and what drove the moves.

Items that may only interest or educate me ….

What’s the Deal with Jackson Hole?, Canadian Economic news, US Economic news, …

What’s the Deal with Jackson Hole?

Every summer, central bankers, finance ministers, and top economists from around the world gather in Jackson Hole, Wyoming, for one of the most closely watched economic events of the year: the Jackson Hole Economic Policy Symposium. Hosted by the Federal Reserve Bank of Kansas City, the conference has been running since 1978 and has become famous for shaping global market expectations.

The setting may be rustic, surrounded by mountains and wildlife, but the ideas discussed here often ripple through the financial world. Over the years, major policy shifts have been signalled at Jackson Hole, making it a must-watch for anyone trying to understand where interest rates and economic policy might be headed next.

This year, the spotlight was squarely on US Federal Reserve Chair Jerome Powell. His speech is always the headline moment, and 2025 was no exception. Powell noted that inflation has eased closer to the Fed’s 2% target, giving the central bank some flexibility. He signalled that the Fed is prepared to cut rates soon if the progress holds, though he balanced it with caution about moving too quickly. Markets responded positively, sending the markets soaring, as investors interpreted his comments as confirmation that lower rates are just around the corner.

For us investors, Jackson Hole isn’t just a high-level gathering in the Wyoming mountains – it’s a reminder that a few carefully chosen words from central bankers can move trillions of dollars.

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Consumer Price Index (CPI)

Statistic Canada’s latest inflation report showed prices easing a bit more in July. Annual CPI came in at 1.7%, down from 1.9% in June and right in line with expectations. On a month-to-month basis, prices rose 0.3%, also matching forecasts.

The biggest driver of the drop was gasoline, which fell a steep 16.1% over the past year, helped by the removal of the consumer carbon tax, while food prices climbed 3.3% year-over-year. On a monthly basis, the food component also saw the biggest increase, rising 0.6% while clothing and footwear prices fell 1.9%.

Shelter costs – one of the most important parts of the CPI basket since it makes up nearly 30% – inched back up to 3.0% after dipping the previous month. Rising rents (+5.1%) and a slower decline in natural gas costs were the main culprits. Because shelter includes rent and mortgage interest, it has a heavy influence on overall inflation.

Core inflation, which strips out more volatile items like food and gas to give a clearer picture of underlying trends, rose 0.3% in July. That was higher than expected, but the annual pace cooled slightly to 2.5% from 2.6% in June. Even so, that’s still above the BoC’s 2% target.

Big picture: overall inflation is easing, mostly thanks to cheaper gas, and that’s fueling hopes the BoC could cut rates at its September 17 meeting. But with food and shelter costs still running hot, and core inflation proving sticky, the central bank may want to see more evidence before making a move.

Retail Sales

According to Statistics Canada, retail sales bounced back strongly in June, climbing 1.5% as expected and reversing May’s downward revised 1.2% decline. Compared to last year, sales were up 6.6%, showing that consumers are still willing to spend despite economic headwinds.

On the monthly side, convenience retailers and vending machine operators led the way with a 5.3% jump in sales, while furniture, electronics, and appliance stores were essentially flat. Looking at the yearly picture, used car dealers once again topped the leaderboard with a 19.3% surge, while gasoline stations remained the biggest drag, down 5.5%.

Core retail sales – which exclude the more volatile auto and gas categories – were particularly strong, rising 1.9% in June versus analyst expectations of 1.1%. Year over year, they were up 6.8%, an acceleration from May’s 5.3% pace.

All in all, Canadians showed resilience at the checkout, especially in everyday essentials like food and general goods. But it’s not all smooth sailing, Statistics Canada’s early estimate for July points to a 0.8% pullback in retail activity, though that figure is still preliminary and could be revised.

Canadian Market Volatility

Canada’s volatility gauge, the S&P/TSX 60 Volatility Index (VIXC), started the week at 10.59 and held steady in a tight band between 10.5 and 10.0. It wasn’t until Fed Chair Powell’s speech at the global central bankers’ meeting, which was well received by investors, that the index broke lower, finishing the week at 9.14.

Think of the VIXC as a “fear gauge” for the Canadian stock market. When investors feel nervous, often due to uncertainty or sudden news, the index ticks higher. Lower numbers, like where it finished the week, signal calmer sentiment. For anyone new to investing, it’s a useful snapshot of how the market is feeling.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Federal Open Market Committee (FOMC) Minutes

The Fed released minutes this past week from its July 29–30 meeting of the FOMC, giving us a window into how officials are weighing interest rates and the economy. Policymakers voted to keep rates steady at 4.5%, but the minutes revealed that two of the eleven voting members (with one absent) leaned toward cutting sooner rather than later. That hint of division is significant – it’s the first time since 1993 that more than one member has dissented in the same meeting, and it underscores just how divided the committee is on how long rates should stay elevated.

The debate extended beyond rates. Officials wrestled with the impact of President Trump’s tariffs on inflation. Some felt any price increases would be short-lived, while others worried tariffs could fuel more persistent inflation.

The labour market was another dividing line. A few members pointed to continued strength in hiring, but others flagged slower wage growth and signs of cooling demand for workers. That left many participants viewing inflation risks as the bigger concern, though some still saw weakening employment as the greater threat.

For now, the Fed’s decision to hold rates at 4.5% means borrowing costs for mortgages, loans, and credit cards remain where they are. For us investors, the chances of a September rate cut are still high but dipped slightly after the minutes, slipping from about 85% to 83%. Now, attention shifts to Fed Chair Powell’s upcoming speech at the Jackson Hole Symposium, where markets are looking for clearer signals on what comes next.

American Market Volatility

Wall Street’s “fear gauge” – the CBOE Volatility Index (VIX) – opened the week at 15.73 and inched higher as investors waited for Fed Chair Powell’s much-anticipated Jackson Hole speech, which could be his last as head of the Fed. The uncertainty over whether he’d hint at rate cuts or reinforce his inflation-fighting stance nudged market nerves up a notch. However, following favourable comments by Powell, the VIX ended the week at 14.22.

For anyone new to the VIX, think of it as a real-time pulse check on investor anxiety. It tends to jump when markets get rattled – whether by geopolitical flare-ups, inflation surprises, or unexpected shifts in Fed leadership. When fear rises, so does the VIX.

Generally, a reading between 12 and 20 signals calm conditions. Once it breaks above 20, traders start bracing for rougher waters. The higher it climbs, the more uncertainty is being priced into markets.

Weekly Market and Portfolio Review

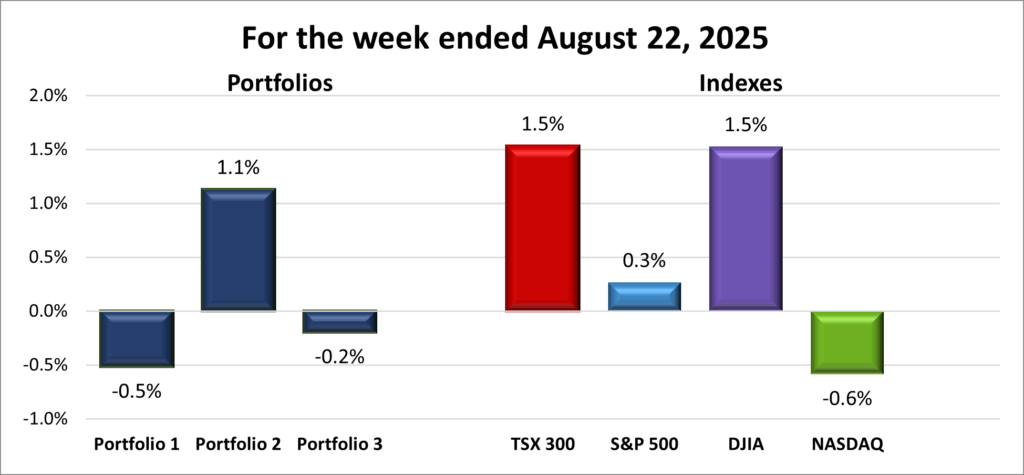

For the week, the TSX (SPTSX) jumped 1.5%, the S&P 500 (SPX) rose 0.3%, the DJIA (INDU) surged 1.5% while the Nasdaq (CCMP) slipped 0.6%.

| Index | Weekly Streak |

| TSX: | 3 – week winning streak |

| S&P: | 3 – week winning streak |

| DJIA: | 3 – week winning streak |

| Nasdaq: | 1 – week losing streak |

![]() Heading into Friday, the US indexes looked like they might end the week in the red, with the exception of Canada’s Toronto Stock Exchange Composite Index (TSX), which held steady. Then Fed Chair Jerome Powell delivered his speech at Jackson Hole, and sentiment flipped, as shown in the weekly progress chart above. His dovish tone sparked a strong relief rally: the S&P 500 Index (S&P) snapped a five-day losing streak, the Dow Jones Industrial Average (DJIA) surged more than 900 points in a single day to set a record high close, and the Nasdaq Composite Index (Nasdaq) recovered most of its earlier losses.

Heading into Friday, the US indexes looked like they might end the week in the red, with the exception of Canada’s Toronto Stock Exchange Composite Index (TSX), which held steady. Then Fed Chair Jerome Powell delivered his speech at Jackson Hole, and sentiment flipped, as shown in the weekly progress chart above. His dovish tone sparked a strong relief rally: the S&P 500 Index (S&P) snapped a five-day losing streak, the Dow Jones Industrial Average (DJIA) surged more than 900 points in a single day to set a record high close, and the Nasdaq Composite Index (Nasdaq) recovered most of its earlier losses.

The Fed stole the spotlight all week. Early on, markets were rattled when President Trump called for Fed Governor Lisa Cook’s resignation over fraud allegations, sparking concerns about Fed independence if another loyalist were appointed, should she resign. Midweek, the July FOMC minutes showed nine of eleven members favoured holding rates steady at 4.25–4.50%. But all eyes were really on Powell’s upcoming Jackson Hole speech, which could be his last as Fed Chair. The question hanging over markets was whether he’d stick to a cautious stance or finally hint at cuts. On Friday, Powell delivered – acknowledging a cooling labour market while warning that tariffs could keep inflation sticky. Investors took his comments as a green light for September rate cuts, sending markets higher to close out the week.

Geopolitical developments also played a role. A White House meeting between Presidents Trump and Zelenskiy and European leaders raised hopes for eventual security guarantees to Ukraine, though little concrete progress emerged. Meanwhile, technology stocks struggled for much of the week amid warnings of an artificial intelligence (AI) bubble from Sam Altman, the CEO of OpenAI (the company behind ChatGPT), combined with an MIT report showing 95% of corporate AI pilot projects failing to deliver returns. Concerns over lofty valuations and increasing government scrutiny added pressure on the sector, even as the broader market recovered late in the week.

In Canada, investors began the week cautiously, keeping an eye on July inflation data, trade developments, and the central bankers’ symposium at Jackson Hole. The inflation report offered a welcome boost, with prices falling more than expected. That eased cost-of-living concerns and opened the door for potential BoC rate cuts, helping the TSX notch back-to-back record highs. On Thursday, it closed above 28,000 for the first time, then followed up with another record on Friday to cap a strong finish to the week.

Trade developments also lifted sentiment. Prime Minister Mark Carney and President Trump reportedly had a productive discussion on trade and broader economic cooperation. Canada then announced it would drop retaliatory tariffs on a wide range of US goods starting September 1. This move aligns with USMCA rules and strengthens bilateral trade momentum, easing long-standing US concerns.

The week ended on a high note with Powell’s dovish Jackson Hole speech, which boosted investor optimism. With US monetary policy signaling possible rate cuts, Canadian markets were pulled along, capping what turned out to be a strong week for both sides of the border.

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week losing streak |

| Portfolio 2: | 3 – week winning streak |

| Portfolio 3: | 2 – week losing streak |

![]()

![]() While Fed Chair Powell’s speech gave markets a late-week lift, the timing wasn’t enough to rescue two of the three portfolios. Even though more than 60% of holdings in each portfolio finished higher, the pullback in technology weighed heavily. The broader rotation out of high-growth tech made gains harder to come by, leaving all three portfolios grinding through ups and downs. The silver lining? On a percentage basis, Portfolio 2’s advance was bigger than the combined losses of the other two, as you can see in the weekly performance chart below. A small win, but I’ll take it. 😊

While Fed Chair Powell’s speech gave markets a late-week lift, the timing wasn’t enough to rescue two of the three portfolios. Even though more than 60% of holdings in each portfolio finished higher, the pullback in technology weighed heavily. The broader rotation out of high-growth tech made gains harder to come by, leaving all three portfolios grinding through ups and downs. The silver lining? On a percentage basis, Portfolio 2’s advance was bigger than the combined losses of the other two, as you can see in the weekly performance chart below. A small win, but I’ll take it. 😊

Portfolio 1 had the toughest stretch, falling 0.5% despite 62% of its companies finishing higher. The drag came from its heavyweight tech names, especially Nvidia (NASD: NVDA), the portfolio’s largest holding.

Portfolio 2 was the lone bright spot, ending the week in the green, edging up 1.1%. More than 74% of its holdings gained ground, though weakness in tech kept the results from being even better. A highlight came from pipeline operator TC Energy (TSE: TRP), which hit an all-time high.

Portfolio 3 slipped 0.2% even though 68% of its stocks moved higher. Steep pullbacks in its two giants, Nvidia and Shopify (NASD: SHOP), were too much to overcome. Together, those two make up over half the portfolio’s value. As they go, so goes the portfolio – and this week, they went down. 😊

The good news is that the overall backdrop looks positive, with markets shaking off interest rate worries and investors finding reasons to stay optimistic. A week like this – drifting lower before rebounding to finish strong – is a good reminder that short-term swings are part of the ride, but the long-term story for these portfolios is still intact. Onward and upward!

Companies on the Radar

This week, a company that had previously caught my eye returned to my radar after delivering a strong second-quarter performance: Arista Networks (NYSE: ANET). Based in the US, Arista designs and sells advanced networking hardware and software, with a focus on high-speed, low-latency switches for its key markets: data centres, AI, cloud computing, and financial trading.

This week, a company that had previously caught my eye returned to my radar after delivering a strong second-quarter performance: Arista Networks (NYSE: ANET). Based in the US, Arista designs and sells advanced networking hardware and software, with a focus on high-speed, low-latency switches for its key markets: data centres, AI, cloud computing, and financial trading.

What really stood out this quarter was solid demand from its core markets, especially in AI and cloud data centres, paired with a hefty share buyback program. On top of that, top institutional investors are increasing their stakes, which signals confidence in the company’s cash position and long-term prospects.

With this addition, Arista now joins the four other companies currently on my radar list:

- Mainstreet Equity Corp. (TSE: MEQ): a Calgary-based real estate company focused on mid-market apartment buildings – typically under 100 units – across Western Canada. It buys underperforming properties at below-market prices, renovates them, and increases rental income through improved operations. With strong demand for rental housing, a repeatable value-add strategy, and a solid balance sheet, Mainstreet offers a compelling mix of income and growth. Shares currently trade below net asset value, giving investors a margin of safety alongside steady cash flow and long-term upside.

- Secure Energy Services (TSE: SES): a Canadian industrial company that focuses on environmental and waste management services for energy and industrial clients. It offers recycling, disposal, and infrastructure support across North America.

- Corning Incorporated (NYSE: GLW): a large cap American company that is a leader in specialty glass, optical fiber, environmental technology, life sciences, and other specialty glasses. They have been the supplier of the glass used in Apples iPhones since 2007, and they are riding the tailwind of an AI-driven fiber optic boom.

- Copart (NASD: CPRT): this American company runs one of the world’s largest online vehicle auction platforms, specializing in salvage cars from accidents and natural disasters. It sells on behalf of insurers, dealerships, rental companies, and individuals. Copart earns revenue through transaction fees, storage, transportation, and listing services. Its digital model, global buyer network, and asset-light approach support strong margins and steady growth. With no long-term debt and rising tailwinds from vehicle values and insurance claims, it’s a steady growth story that’s earned a spot on my radar.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated August 22, 2025.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!