Under Pressure: Fed Independence Under Fire

With apologies to Queen and David Bowie, the US government has turned up the pressure on the US Federal Reserve, and on Chair Jerome Powell in particular, to fall in line with President Trump’s push for lower interest rates. For investors, the question isn’t politics – it’s how this could rattle markets and shake confidence in US interest rates.

In November 2025, US Department of Justice (DOJ) prosecutors in Washington, D.C. approved a criminal investigation into Federal Reserve Chair Jerome Powell, centred on his testimony to Congress about a roughly US$2.5 billion renovation of the Fed’s Washington headquarters and whether lawmakers were misled about the project’s scope and costs. The inquiry, approved by US Attorney Jeanine Pirro, a Trump appointee, included document requests from Powell’s team.

The issue stayed under the radar through the fall but burst into headlines in early January 2026 when grand jury subpoenas were served, raising the possibility of indictments tied to Powell’s testimony. Powell responded with a rare public video, calling the move “unprecedented” and describing it as a pretext for political pressure, coming shortly after he resisted White House calls for deeper and faster interest-rate cuts.

This escalation fits into a broader pattern of sustained pressure from President Trump on Powell to lower rates, rather than a simple policy disagreement. While Trump nominated Powell during his first term, tensions escalated after Trump returned to office in 2025. Since then, the president has repeatedly criticized Powell for keeping rates “too high,” publicly attacked him, and even floated the idea of firing him – actions that break with long-standing norms around central bank independence. Powell, for his part, has avoided political engagement and consistently stressed that Fed decisions are driven by economic data, not politics.

President Trump has denied any involvement in the DOJ investigation. Still, many observers believe the broader effort reflects an attempt to assert greater control over the Fed and push for lower rates that align with the administration’s agenda. That perception has triggered significant pushback, including public statements from three former Fed chairs, senior economic officials, and even Republican senators, all warning that political interference risks undermining confidence in US monetary policy.

While the DOJ’s focus on renovation testimony may sound technical, the real issue for investors – including those in Canada – is confidence in the Fed’s independence. Central banks, like the Bank of Canada, operate independently from government, setting interest rates to keep inflation near their 2% target. The Fed’s dual mandate is similar: maintaining price stability while promoting maximum employment in the US economy. To do this effectively, they need the freedom to set policy based on economic data, not political pressure.

If investors start doubting the Fed’s independence, they may demand higher interest rates on government debt to compensate for the risk of politically influenced policy. That can ripple through the financial system, putting pressure on rate-sensitive stocks like technology and housing and increasing overall market volatility. Confidence in the dollar could also waver, and businesses and consumers may hesitate to invest or spend amid greater uncertainty. When political pressure appears aimed at the Fed’s leadership, it raises concerns about future monetary policy and market stability – which is why former Fed chairs, economists, and lawmakers from both parties have pushed back strongly.

In practical terms, nothing about how rates are set has changed. Powell and the Fed are still calling the shots, and inflation, jobs, and growth remain the key drivers of future decisions. But the bigger picture matters – political pressure on the Fed is a reminder that markets can feel under pressure, with swings in stocks, bonds, and the dollar. For now, let’s see what else moved markets this past week.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Canadian Market Volatility

Canada’s VIXC, essentially the TSX’s own “fear gauge,” opened the week a bit higher at 13.47 after news of the DOJ investigation involving the Fed stirred fresh concerns about Fed independence. Once investors absorbed that development, the VIXC settled into a calm 12–13 range, signaling mild caution rather than outright stress.

The index briefly spiked above 15 midweek and again toward the end of the week as uncertainty crept in, but in both cases it quickly eased, before ending the week at 13.02.

Think of the VIXC as Canada’s market mood ring. Readings in the low teens suggest cautious confidence – investors are alert and paying attention, but there’s no panic in the cabin.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Consumer Price Index (CPI)

The Department of Labor’s latest CPI report showed inflation holding steady, not heating back up – which is exactly what investors were hoping to see. Headline inflation came in at 2.7% year over year in December, unchanged from November and right in line with expectations. In plain terms, prices are still rising faster than the Fed’s 2% target, but they’re no longer accelerating. On a monthly basis, prices rose 0.3%, matching both last month and forecasts.

Under the hood, energy prices were mixed. Utility gas prices – natural gas delivered to homes – are up 10.8% over the past year, a reminder of how winter heating costs can bite. Gasoline prices, on the other hand, are 3.4% lower than a year ago, even though they jumped 1.9% in December, the biggest monthly increase in the report. Fuel oil (heating oil) moved the opposite way, falling 1.5% on the month. These swings highlight why energy inflation can feel unpredictable from month to month.

Shelter costs – which include rent, homeowner expenses, and other housing-related costs – rose 0.4% in December and remain one of the biggest pressure points for households. The good news is that the annual pace continues to cool, easing to 3.2%, suggesting housing inflation is slowly moving in the right direction.

The most encouraging part of the report was core inflation, which strips out food and energy to give a cleaner view of underlying price trends. Core CPI rose 2.6% year over year, slightly better than the expected 2.7% increase and unchanged from November. On a monthly basis, it increased just 0.2%, below forecasts of a 0.3% gain. For the Fed, this points to inflation pressures beneath the surface gradually easing.

This is the first clean look at inflation since September, and the message is reassuring. Inflation isn’t back to the Fed’s 2.0% target yet, but it’s behaving. Prices are rising more slowly, core inflation is cooling, and the data supports the idea that the Fed can afford to be patient rather than rush into earlier or deeper rate cuts.

Retail Sales

In the first major retail sales report since last year’s federal government shutdown, the Commerce Department showed that US consumer spending picked up meaningfully. Retail sales rose 0.6% in November, beating expectations for a 0.4% increase and improving sharply from October’s flat reading. On a year-over-year basis, sales were up 3.3%, pointing to steady consumer demand.

Spending gains were broad but uneven. Sporting goods, hobbies, music, and bookstores saw a strong 1.9% jump, suggesting discretionary spending held up well heading into the holiday season. Furniture and home furnishings slipped 0.1%, while over the past year, miscellaneous retailers posted a sizable 16.3% increase. On the weaker side, building materials and garden supplies were down 2.8%, reflecting slower housing-related activity.

Looking at core retail sales – which strip out autos and gasoline to give a clearer picture of everyday spending – sales rose 0.4% in November, double October’s 0.2% gain, though slightly below expectations for a 0.7% increase. The annual pace held steady at 4.4%, matching October and reinforcing the idea that consumer spending is still resilient.

Overall, the report points to a consumer that’s still willing to spend, supporting a solid holiday shopping season and continued economic growth. That matters because consumer spending makes up roughly two-thirds of the US economy, so healthy retail sales help underpin economic growth into year-end.

For us investors, retail sales offer an important signal about where the economy is headed. Strong spending can support earnings for companies tied to both discretionary and everyday purchases, while also influencing how the Fed views the economy. As long as consumers continue to spend, Fed officials may feel less urgency to rush into interest-rate cuts, keeping the focus on incoming inflation and jobs data.

American Market Volatility

The CBOE Volatility Index (VIX), often called the market’s “fear gauge,” opened the week around 15.75 after Fed Chair Jerome Powell disclosed that the DOJ had served subpoenas to the Fed, raising questions about the central bank’s independence. While the headline grabbed attention, volatility remained fairly contained, with the VIX generally hovering between 15 and 16.

Midweek, the index pushed closer to 18 as US–Iran tensions flared and a handful of large US banks delivered mixed earnings, giving markets a brief jolt. That unease faded quickly as geopolitical concerns cooled and solid results from additional big US banks helped steady sentiment. By week’s end, the VIX had eased back to 15.86.

Think of the VIX as the market’s pulse. This week, it settled into a steadier, healthier rhythm. Investors aren’t exactly carefree, but they do appear more comfortable as inflation continues to cool and interest rates edge closer to a turning point.

Weekly Market and Portfolio Review

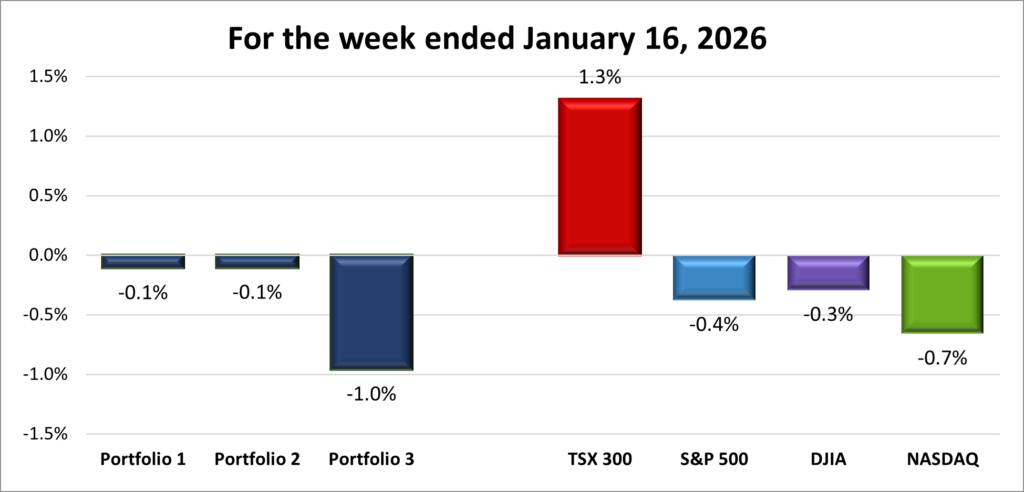

For the week, the TSX (SPTSX) was up 1.3%, the S&P 500 (SPX) lost 0.4%, the DJIA (INDU) dipped 0.3% and the Nasdaq (CCMP) fell 0.7%.

| Index | Weekly Streak |

| TSX: | 2 – week winning streak |

| S&P: | 1 – week losing streak |

| DJIA: | 1 – week losing streak |

| Nasdaq: | 1 – week losing streak |

![]()

![]() The second full week of trading in 2026 got off to a strong start, with all four major indexes ending the opening day higher, including record highs for the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), and the Dow Jones Industrial Average (DJIA). That optimism faded midweek in the US, as the S&P, DJIA, and Nasdaq Composite Index (Nasdaq) slipped into the red and spent the rest of the week trying, but failing, to recover. Canada’s TSX, meanwhile, paused briefly on Tuesday before resuming its climb and finishing the week with two more record-high closes.

The second full week of trading in 2026 got off to a strong start, with all four major indexes ending the opening day higher, including record highs for the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), and the Dow Jones Industrial Average (DJIA). That optimism faded midweek in the US, as the S&P, DJIA, and Nasdaq Composite Index (Nasdaq) slipped into the red and spent the rest of the week trying, but failing, to recover. Canada’s TSX, meanwhile, paused briefly on Tuesday before resuming its climb and finishing the week with two more record-high closes.

Markets opened under a cloud after Fed Chair Jerome Powell revealed he is under investigation by the DOJ, raising concerns about the Fed’s independence and future interest-rate decisions. While the headline rattled investors initially, attention quickly shifted to fourth-quarter earnings and a busy slate of economic data.

Early bank earnings were mixed, dragging US indexes lower. Sentiment improved after strong results from Goldman Sachs (NYSE: GS) and Morgan Stanley (NYSE: MS) reversed the sell-off in financials and steadied the market. Later in the week, technology took the lead when Taiwan Semiconductor (NYSE: TSM) reported strong earnings and issued an upbeat growth outlook. That reassured investors that demand for artificial intelligence (AI) chips remains robust, lifting the S&P and Nasdaq, while the DJIA also benefited from stronger banks and defensive sectors.

Economic data added support. The latest CPI inflation report, the first full reading since last fall’s government shutdown, showed inflation coming in as expected, with core inflation holding steady. Retail sales also surprised to the upside, confirming consumers continued spending through the holiday season. Together, the data pointed to a resilient American economy with easing price pressures and reinforced expectations for two Fed rate cuts in 2026.

Late in the week, uncertainty resurfaced after President Trump suggested he was reluctant to appoint his economic advisor, Kevin Hassett, as Fed Chair due to their strong working relationship. The comments raised fresh questions about who will eventually lead the central bank and whether future interest-rate policy could be less inclined to lower rates than many investors currently expect.

In Canada, the TSX extended its strong start to the year, setting record highs on each of the final three trading days. The main driver was a powerful rally in gold, silver, and other commodities, fueled by concerns over Fed independence and geopolitical tensions. Safe-haven demand pushed gold past US$4,600 per ounce for the first time, setting a positive tone for the week.

Other sectors helped as well. Energy stocks rose with higher oil prices, financials recovered after early weakness tied to US banks, and technology shares got a lift midweek as optimism around AI spilled into the Canadian market.

Overall, it was a noisy but busy week. Political headlines and geopolitical tensions created short-term swings, yet markets largely took it in stride. Beneath the surface, money continued rotating out of some of the larger technology names and into more overlooked areas, suggesting investors remain selective but engaged rather than heading for the exits.

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week losing streak |

| Portfolio 2: | 1 – week losing streak |

| Portfolio 3: | 1 – week losing streak |

![]() Well, those winning streaks didn’t last long. A mixed week for the major indexes translated into a disappointing week for my portfolios as well ☹️. One important update this week came from the quarterly review of the S&P/TSX 60 Index, which tracks 60 of the largest and most liquid companies on the Toronto Stock Exchange. While the index changes themselves were finalized in December, their impact became clear this week. Because many ETFs and index funds are designed to mirror the index, any additions or removals force those funds to buy or sell shares. That rebalancing can create short-term price moves, and this reshuffle directly affected both Portfolio 1 and Portfolio 3.

Well, those winning streaks didn’t last long. A mixed week for the major indexes translated into a disappointing week for my portfolios as well ☹️. One important update this week came from the quarterly review of the S&P/TSX 60 Index, which tracks 60 of the largest and most liquid companies on the Toronto Stock Exchange. While the index changes themselves were finalized in December, their impact became clear this week. Because many ETFs and index funds are designed to mirror the index, any additions or removals force those funds to buy or sell shares. That rebalancing can create short-term price moves, and this reshuffle directly affected both Portfolio 1 and Portfolio 3.

Portfolio 1 slipped just 0.1% on the week, despite 54% of its holdings finishing higher. That was a bit surprising given that Nvidia (NASD: NVDA) also posted a weekly gain. Helping limit the downside, Walmart (NASD: WMT) and Cameco (TSE: CCO) both hit record highs on their way to solid weekly gains. One company that benefitted from the shuffling of the S&P/TSX 60 was Celestica (TSE: CLS). Even with that tailwind, the stock still finished the week lower, a reminder that index additions don’t guarantee immediate gains.

There were also a few notable company-specific developments in Portfolio 1. Alphabet (NASD: GOOGL) crossed the US$4 trillion market cap mark, driven by its renewed push in AI. A major validation of their AI strategy came when Apple (NASD: AAPL) announced its AI offerings will be built on Google’s Gemini platform through a multi-year partnership. Meanwhile, Nvidia received approval to sell its China-specific H200 AI chips into the Chinese market, helping ease some concerns around export restrictions.

Technically, Portfolio 2 also finished the week down 0.1%, but on a closer look it actually held up marginally better than Portfolio 1, although only 46% of its holdings posted weekly gains. There weren’t many standout movers, although Aritzia (TSE: ATZ) briefly hit a record high before slipping into a small loss by week’s end.

Portfolio 3 had the toughest week, falling 1.0%. That was another mild surprise, since 60% of its holdings finished higher and Nvidia, the largest position, was also in the green. Unfortunately, Nvidia’s modest gain wasn’t enough to offset a sharper drop in Shopify (TSE: SHOP), the second-largest holding. On the index shuffling front, Lithium Americas (TSX: LAC) was added to the TSX Composite, while Canada Packers (TSX: CPKR) was removed in the same rebalance.

It wasn’t a great week for the portfolios, but there was a silver lining: both Portfolio 1 and Portfolio 3 saw the majority of their holdings post weekly gains. It’s not much of a victory, but in choppy markets, those underlying positives are worth noting. 😊

Next week, fourth-quarter earnings season ramps up, which should give a clearer picture of how companies are really doing. Strong results and companies meeting or beating forecasts could help stabilize the markets and regain upward momentum after a choppy start to the year. And lift my portfolios with them. 😊

Companies on the Radar

It was a busy week for my radar list, with one company coming off and three new names being added. I decided to drop Build-A-Bear Workshop, Inc. (NYSE: BBW), as it increasingly feels more like a fad than a durable long-term business. The company doesn’t appear to have a strong competitive moat, which leaves it vulnerable to copycats. That said, I wouldn’t rule out the possibility of BBW eventually being acquired by a larger toy company.

It was a busy week for my radar list, with one company coming off and three new names being added. I decided to drop Build-A-Bear Workshop, Inc. (NYSE: BBW), as it increasingly feels more like a fad than a durable long-term business. The company doesn’t appear to have a strong competitive moat, which leaves it vulnerable to copycats. That said, I wouldn’t rule out the possibility of BBW eventually being acquired by a larger toy company.

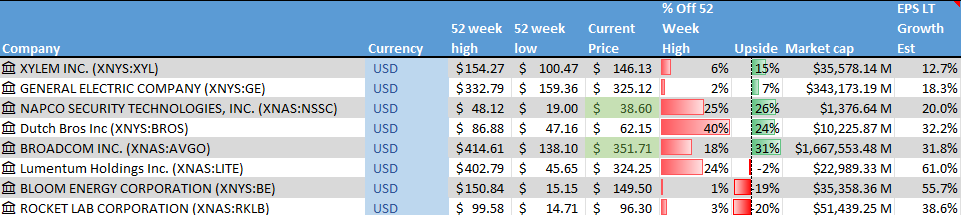

Replacing it are three companies benefiting – directly or indirectly – from the ongoing build-out of AI and data-centre infrastructure: Broadcom (NASD: AVGO), Lumentum Holdings (NASD: LITE), and Bloom Energy (NYSE: BE).

Broadcom is a large cap American company that sells semiconductors and software globally. It designs critical chips used in data centres, networking equipment, and broadband infrastructure, playing a behind-the-scenes role in cloud computing and AI. Broadcom also owns a growing enterprise software business following its acquisition of VMware, giving it exposure to both hardware and software spending tied to AI and cloud growth.

Lumentum is a large cap US-based optical technology company that makes key components used to move data at extremely high speeds across cloud and data-centre networks. Products like electro-absorption modulated lasers (EMLs) are seeing rising demand as AI workloads require faster and more efficient connections between servers. As large cloud providers continue ramping up AI infrastructure spending, Lumentum has emerged as a key beneficiary of this next wave of data and connectivity growth.

Bloom Energy is another large cap American company but approaches the AI trend from a different angle. Rather than supplying chips or networking gear, it provides clean, on-site power through fuel-cell systems designed for customers that need reliable electricity and can’t afford outages. As AI drives rapid growth in data-centre capacity – and with it, soaring energy demand – interest in resilient, lower-emission power solutions has increased. Bloom offers exposure to the rising power needs created by AI alongside broader trends in energy reliability and decarbonization.

After these changes, my radar list now stands at eight companies.

- Xylem Inc. (NYSE: XYL): This is a large American company that develops water technology focused on moving, treating, and managing water. Its products and services are used by utilities, industrial customers, and municipalities for everything from clean drinking water and wastewater treatment to flood control and leak detection. With aging water infrastructure and more frequent climate challenges like droughts and flooding, demand for Xylem’s solutions remains strong. The business offers exposure to long-term, essential infrastructure spending tied to water scarcity, sustainability, and smarter cities.

- GE Aerospace (NYSE: GE): This is the large American aviation and defence business that remained after General Electric split into three separate companies in 2024. It has been on a strong run thanks to high demand for commercial jet engines as global air travel continues to recover. The company focuses on aircraft propulsion systems and services for both commercial and military customers, and it’s also moving into drones. As a global leader in jet engines and aircraft systems, GE Aerospace offers exposure to long-term trends in travel, defence spending, and emerging aviation technology.

- Napco Security Technologies, Inc. (NASD: NSSC): A small US company that provides security hardware and systems like smart locks, intrusion alarms, fire alarms, and access control solutions. It sells through a network of distributors and installers, and has been increasing its recurring service revenue – something investors usually like to see. As demand for security and smart home products grows, Napco has multiple avenues for expansion.

- Dutch Bros Inc. (NYSE: BROS): A rapidly expanding drive-thru coffee chain in the US, known for its energetic customer service and customizable drinks. The company is aiming to open at least 160 new locations by the end of 2025 and has long-term goals of surpassing 2,000 stores. Strong brand loyalty, especially in the Western US, makes this an interesting high-growth story – though still in an aggressive build-out phase.

- Rocket Lab (NASD: RKLB): They are an aerospace company helping make space more accessible. It launches rockets that carry small satellites into orbit – the kind used for communications, Earth observation, and research – and also builds the space hardware that makes those missions possible. Over time, Rocket Lab has grown beyond just launching rockets, evolving into a more complete space company that designs spacecraft, manages missions, and supports customers from launch all the way through operations in space.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated January 16, 2026.

Portfolio Update

Portfolio 1

Bought: Visa (NYSE: V) This week, I made my fourth investment in Visa since my original purchase in 2020, taking advantage of a recent pullback tied to President Trump’s proposed 10% cap on credit card interest rates. In my view, the selloff reflects short-term fear around the headlines rather than any real change in how Visa’s business operates. While the proposal unsettled investors, Visa doesn’t set interest rates or earn interest income – banks do. Visa makes its money from transaction volume, and that core part of the business remains firmly intact.

Visa’s competitive moat is still massive. Its global payments network is deeply embedded with consumers, merchants, banks, and governments, making it extremely difficult to replace. Even when spending slows, transactions don’t disappear – they shift – and Visa continues to collect a small fee almost every time money moves electronically.

Long-term trends also are still firmly in Visa’s favour. The global move away from cash, growth in digital payments, e-commerce, and cross-border travel all support steady transaction growth over time. With strong cash flow, high margins, and ongoing share buybacks and dividends, Visa remains a high-quality compounder. Adding shares during a bout of uncertainty felt like an opportunity to increase ownership in a durable business at a more attractive price.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!