SK hynix: The Memory Powering the AI Revolution

When investors think about artificial intelligence (AI), companies like Nvidia (NASDAQ: NVDA) and Microsoft (NASDAQ: MSFT) are often the first names that come to mind. However, AI requires much more than powerful processors and software. Behind the scenes, an entire ecosystem of companies provides the infrastructure needed to make AI possible.

One of those companies is SK hynix (NASDAQ: SKHY). Nvidia may be the face of AI, but SK hynix – yes, the lowercase “h” is intentional – provides one of the critical components that allows AI chips to reach their full potential: advanced memory.

What does SK hynix do?

Unlike companies such as Nvidia, which design advanced processors, SK hynix specializes in developing and manufacturing memory semiconductors.

Its two main product categories are:

- DRAM (Dynamic Random-Access Memory): High-speed memory that allows devices and servers to quickly access data while they are running.

- NAND flash memory: Storage memory used in products such as smartphones, solid-state drives (SSDs), and data centres.

A simple way to think about it: the processor is the brain of a computer, while memory is the workspace that allows the brain to quickly access the information it needs. The faster and larger that workspace becomes, the more efficiently the system can operate.

Why is demand for SK hynix’s products so strong?

The biggest reason investors are paying attention to SK hynix today is High Bandwidth Memory (HBM).

Traditional memory wasn’t designed to handle the enormous data demands of modern AI models. HBM addresses this challenge by stacking multiple memory chips together and placing them closer to AI processors, allowing data to move far more quickly while using less power.

This makes HBM a critical component in advanced AI servers.

As companies around the world invest billions of dollars building AI infrastructure, demand for specialized memory has surged. SK hynix has become a leader in HBM technology and is one of the key suppliers helping power the growth of AI computing.

Why is SK hynix listing in the US?

Although SK hynix already trades on South Korea’s main stock exchange (Korea Exchange), the company expanded access to its shares by launching an American Depositary Receipt (ADR) on the Nasdaq under the ticker SKHY.

An ADR allows investors in other countries to invest in a foreign company without needing to buy shares directly on the company’s home exchange. In SK hynix’s case, each ADR represents one-tenth of an ordinary share, meaning investors need to own 10 ADRs to equal one share of the underlying company. This structure allows the US-listed shares to trade at a more accessible price while still providing exposure to the same underlying business.

For investors in Canada and the US, the Nasdaq listing provides easier access through regular brokerage accounts, greater visibility among global investors, and a closer connection to the broader AI investment theme.

The US share offering also generated significant investor interest. Priced at US$149.00 per ADR, the offering raised US$26.5 billion, making it the largest US listing by a foreign company. The shares opened at US$170.00 and finished their first trading day at US$168.01, reflecting strong demand from investors eager to gain exposure to one of the key suppliers behind the AI boom.

For SK hynix, the listing provides access to a deeper pool of global capital that can help fund continued investment in semiconductor manufacturing capacity and future technology development.

What should investors keep in mind?

While SK hynix has benefited from the AI boom, the memory chip industry has historically been cyclical. Strong demand often encourages manufacturers to increase production, which can eventually create excess supply and pressure prices.

The company is also closely tied to AI infrastructure spending. If companies reduce their investment in AI data centres or if new technologies emerge, growth expectations could change.

Final thoughts

As AI infrastructure continues to expand, fast, specialized memory will remain a critical part of the AI ecosystem. While Nvidia may be the face of AI, companies like SK hynix serve as a reminder that every AI breakthrough relies on an entire ecosystem working behind the scenes. It’s another example of why understanding an entire industry – not just the headline-grabbing names – can help uncover businesses that might otherwise be overlooked.

Now that we’ve looked at one of the companies helping power the AI revolution, let’s see what drove the markets this week, whether the AI rollercoaster continued, and how it impacted the three portfolios.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Labour Force Survey (LFS)

Statistics Canada’s June employment report showed the economy added 18,200 jobs, beating economists’ expectations of 10,000. While the gain was much smaller than May’s surge of 87,800 jobs, it suggests the labour market continues to stabilize after a softer start to the year. Most of the new jobs were part-time positions, with hiring concentrated in accommodation and food services, along with wholesale and retail trade. Manufacturing, however, continued to face headwinds amid ongoing trade uncertainty.

Meanwhile, the unemployment rate fell for a second consecutive month to a six-month low of 6.5%, edging down from 6.6% in May and coming in slightly better than expected.

Wage growth also edged higher. Average hourly wages rose 3.3% year over year, up from 3.0% in May. While encouraging for workers, stronger wage growth is something the BoC will monitor closely because rising labour costs can contribute to inflation.

Overall, the report painted a picture of a labour market that remains resilient despite ongoing economic uncertainty. For investors, that reinforces expectations the Bank of Canada will leave its benchmark interest rate unchanged at 2.25% next week as it continues to balance inflation risks with economic growth.

Canadian Market Volatility

Canada’s version of the market “fear gauge” is the S&P/TSX 60 VIX Index (VIXC). Like the US VIX, it measures how much volatility investors expect in the Canadian stock market over the next 30 days. Higher readings signal greater uncertainty, while lower readings suggest investors are feeling more confident.

The VIXC generally runs lower than its US counterpart because the Canadian market has less exposure to high-growth technology companies and greater weightings in sectors such as financials, energy, and materials. These industries tend to experience fewer sharp swings in investor sentiment, resulting in lower expected volatility.

The VIXC opened the week at 14.71, slightly above the previous week’s close of 14.19, and remained relatively steady around the 14.50 level for most of the week. Midweek, the index briefly climbed above 15.5 after the US and Iran exchanged missile strikes, raising concerns that their fragile ceasefire could unravel. However, investors quickly regained confidence as tensions eased, pushing the VIXC lower before it finished the week at 12.89.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Federal Open Market Committee (FOMC) minutes

This week, the Fed released the minutes from its June 16-17 FOMC meeting, the first under new Chair Kevin Warsh. Officials kept the benchmark interest rate unchanged at the 3.50%-3.75% range, but the minutes revealed a deeper divide over what comes next.

Some officials believed inflation would continue to ease as temporary pressures, such as higher energy prices and other supply-related factors, faded, allowing rates to remain steady or eventually move lower. Others worried inflation could prove more stubborn, potentially requiring another rate increase later this year. A few even felt there was already a case for raising rates at the June meeting.

One thing remains clear: as long as inflation stays above the Fed’s 2% target, Fed officials are likely to remain cautious. Higher rates increase borrowing costs for consumers and businesses, which can slow economic growth. Growth-oriented sectors, particularly technology, often feel this pressure because higher rates reduce the value investors place on future earnings.

The minutes also highlighted the impact of AI infrastructure spending. Several officials noted that the massive investment in AI data centres, semiconductors, electricity, and related infrastructure could keep inflation elevated in the near term. However, they also acknowledged that AI could eventually improve productivity and help lower costs over the longer term.

For investors, the message was clear: the Fed is in no rush to declare victory over inflation, meaning interest rate expectations will likely remain one of the key drivers of markets in the months ahead.

American Market Volatility

The VIX – often called the market’s “fear gauge” – measures expected volatility in the S&P over the next 30 days. In simple terms, it reflects how much uncertainty investors are pricing into the market, rising when anxiety picks up and easing when conditions feel more stable. Readings above 20 are generally associated with heightened volatility, while lower levels tend to signal calmer markets.

The index opened the week at 16.40, little changed from the previous week’s close of 16.16, and remained relatively steady around the 16 level through the first half of the week. Midweek, the VIX briefly surged to 18.90 after President Trump declared the memorandum of understanding (MOU) and ceasefire between the US and Iran “over” following overnight missile exchanges between the two countries. Although those concerns quickly eased, the VIX received another short-lived spike after the Fed released the minutes from its June meeting, revealing officials were divided over the outlook for inflation and the future path of interest rates. By Thursday, investor confidence had returned, pushing the VIX back toward 16, where it finished the week at 15.04. Despite the week’s headlines, investors ultimately finished the week feeling a less anxious than when it began.

Weekly Market and Portfolio Review

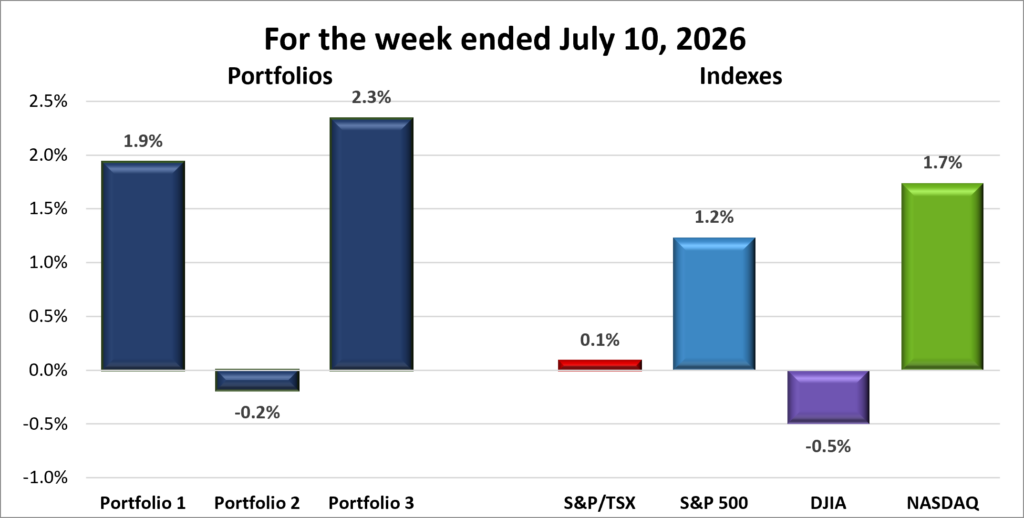

For the week, the TSX (SPTSX) gained 0.1%, the S&P 500 (SPX) advanced 1.2%, the DJIA (INDU) slipped 0.5% and the Nasdaq (CCMP) climbed 1.7%.

| Index | Weekly Streak |

| TSX: | 2 – week winning streak |

| S&P: | 2 – week winning streak |

| DJIA: | 1 – week losing streak |

| Nasdaq: | 2 – week winning streak |

![]() The market roller coaster continued this past week. The Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) all experienced plenty of volatility, although only the TSX, the S&P and the Nasdaq were able to finish the week in positive territory. Along the way, the DJIA closed above 53,000 for the first time, setting a record high, but gave back those gains to snap its weekly winning streak at four. The TSX did the opposite, suffering its worst one-day decline in over a month but bounced back to extend its winning streak another week.

The market roller coaster continued this past week. The Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) all experienced plenty of volatility, although only the TSX, the S&P and the Nasdaq were able to finish the week in positive territory. Along the way, the DJIA closed above 53,000 for the first time, setting a record high, but gave back those gains to snap its weekly winning streak at four. The TSX did the opposite, suffering its worst one-day decline in over a month but bounced back to extend its winning streak another week.

With a relatively light week for economic data, investors once again focused on two familiar themes: geopolitical tensions in the Middle East and the ongoing tug-of-war in AI stocks.

Early in the week, OPEC+ countries agreed to raise production for a fifth straight month, adding to expectations that the oil market could shift from tight supply just a few months ago to a potential surplus. Falling oil prices eased concerns that higher energy costs could reignite inflation, helping technology stocks regain their footing after the previous week’s sell-off. Renewed enthusiasm for AI-related companies, led by semiconductor stocks, then gave US markets a solid start.

Midweek, investor attention shifted to the latest minutes from the Fed’s FOMC meeting, which reinforced the view that Fed officials remain cautious about inflation. While the minutes did little to change expectations for interest rates, they reminded investors that the path toward lower borrowing costs may not be as smooth as many had hoped. Adding to the cautious tone, renewed tensions in the US-Iran war pushed oil prices higher after each side exchanged missile strikes. The US also revoked a licence that had allowed Iranian oil exports under an interim agreement, raising concerns that higher energy costs could slow progress on inflation and potentially keep interest rates higher for longer.

In Canada, the impact of the oil moves was felt most directly through the energy sector. As oil prices declined early in the week, Canadian energy stocks came under pressure, weighing on the TSX due to the sector’s significant influence on the index. However, losses were partially offset by strength in basic materials (gold and other metals), where elevated gold prices supported mining stocks as investors continued to seek stability amid ongoing uncertainty.

Financial stocks also provided some support, with Canada’s major banks remaining relatively resilient. Despite those offsets, the combination of weakness in energy stocks and a midweek market pullback kept the TSX under pressure for much of the week, before rebounding with a broader market rally to end the week in positive territory.

By the end of the week, sentiment improved as oil prices retreated and fears of a broader disruption to global energy supplies eased. Investors also returned to AI-related technology stocks, with the successful Nasdaq debut of South Korea’s SK hynix ADRs reinforcing optimism surrounding semiconductor companies and the broader AI trade. That combination helped the US market recover much of its midweek losses and finish the week on a positive note. The recovery, however, was not felt equally across markets. The divergence between the Canadian and US markets once again highlighted the TSX’s unique composition, where commodities and financials play a much larger role than technology stocks.

| Portfolio | Weekly Streak |

| Portfolio 1: | 2 – week winning streak |

| Portfolio 2: | 1 – week losing streak |

| Portfolio 3: | 2 – week winning streak |

![]()

![]() Despite another volatile week in the markets, my portfolios held up well. The renewed AI rally helped Portfolios 1 and 3 outperform Nasdaq, the top performing index, and extend their winning streaks another week. Only Portfolio 2 failed to extend its winning streak, although it narrowly missed joining them.

Despite another volatile week in the markets, my portfolios held up well. The renewed AI rally helped Portfolios 1 and 3 outperform Nasdaq, the top performing index, and extend their winning streaks another week. Only Portfolio 2 failed to extend its winning streak, although it narrowly missed joining them.

Anticipation ahead of the Nasdaq debut of South Korea’s SK hynix ADRs added to the positive sentiment surrounding AI stocks, helping lift many of the AI-related companies across the three portfolios, including an 8% gain by Nvidia. Because Nvidia is the largest holding in Portfolios 1 and 3, its strong week had an outsized impact on their overall performance.

Portfolio 1 gained 1.9% for the week, outperforming the Nasdaq Composite’s 1.7% gain. Normally that would have been enough to claim top honours, but not this week. Nvidia’s strong performance provided a solid foundation for the portfolio, but the gains were broad-based as well. More than half of the portfolio’s holdings finished the week higher, led by Cloudflare (NYSE: NET), up 11%, and Arista Networks (NYSE: ANET), which climbed 15% while setting a record high.

Portfolio 2 was the only portfolio to finish lower, slipping 0.2%. While Bank of Nova Scotia (TSE: BNS), the portfolio’s largest holding, posted a gain, declines in Microsoft and MongoDB (NASDAQ: MDB), the second and third largest holdings, were enough to outweigh it. It’s another reminder that even a diversified portfolio can have an off week when several of its largest holdings move in the same direction.

Portfolio 3 claimed top honours with a 2.3% gain, despite fewer than half of its holdings finishing the week higher. Strength across several AI-related holdings, particularly cybersecurity company Cloudflare, which gained 11%, more than offset a 20% decline in Rocket Lab (NASDAQ: RKLB) and a 16% drop in MDA Space (TSE: MDA). So much for getting a lift from my space companies. 😊

One piece of news that didn’t have a major impact this week – but could be important over the long term – was Broadcom’s (NASDAQ: AVGO) announcement of a new multi-year chip supply agreement with Apple (NASDAQ: AAPL) worth more than US$30 billion. Because Apple accounts for roughly 20% of Broadcom’s annual revenue, the deal provides greater certainty for one of the company’s most important customer relationships. As a Broadcom shareholder, I’m pleased to see one of the company’s most important customer relationships secured for years to come.

This week’s results were another reminder that it’s not just the market that matters, but what you own within it. Even when markets move in the same direction, portfolios can produce very different results depending on their largest holdings and sector exposure.

Next week promises to be another busy one, with the latest US inflation data, the start of second-quarter earnings season, the Bank of Canada’s latest interest rate decision, and ongoing developments in the Middle East. It should make for another interesting week in the markets.

Companies on the Radar

This week, a company quietly helping power the AI boom came onto my radar. SK hynix is a large cap South Korean semiconductor company that currently trades on South Korea’s main stock exchange but began trading in the US as an ADR [link to ADR] under the ticker SKHY, making it much easier for North American investors to own.

This week, a company quietly helping power the AI boom came onto my radar. SK hynix is a large cap South Korean semiconductor company that currently trades on South Korea’s main stock exchange but began trading in the US as an ADR [link to ADR] under the ticker SKHY, making it much easier for North American investors to own.

As discussed earlier, SK hynix is one of the world’s leading memory chip manufacturers and a leader in High Bandwidth Memory (HBM), the specialized memory powering today’s AI systems. As companies continue investing heavily in AI infrastructure, demand for HBM has surged, making SK hynix a key supplier in one of technology’s fastest-growing markets.

With SK hynix joining the four companies carried over from last week (listed below), my radar list now stands at five companies.

- S&P Global (NYSE: SPGI): A large cap American company and one of the world’s most important financial information companies. Most investors know it for the S&P 500 Index, but the business also provides credit ratings, market data, analytics, and research used by banks, corporations, governments, and investors worldwide. Think of it as one of the key information providers that helps global financial markets function, generating revenue through subscriptions, licensing fees, and rating services.

- Perimeter Solutions (NYSE: PRM): An American mid-cap company that produces specialty chemicals. Its best-known products are the fire retardants used to fight wildfires. If you’ve seen aircraft dropping bright red retardant over a wildfire, there’s a good chance it came from Perimeter. The company operates in a niche but essential market, supplying products and services that help protect communities, infrastructure, and natural resources during increasingly active wildfire seasons.

- TerraVest Industries (TSE: TVK): A mid-cap Canadian industrial company that produces equipment for energy, storage, and transportation markets, including propane tanks, pressure vessels, and heating systems. It grows through a mix of organic expansion and acquisitions, serving steady, asset-heavy industrial niches across North America.

- Forgent Power Solutions (NYSE: FPS): An American large-cap industrial company that builds the electrical infrastructure needed to power data centres, factories, and other large facilities. In simple terms, it makes the equipment that helps move electricity from the grid to where it is needed. It’s not the company building AI models, but rather one of the companies supplying the critical infrastructure that helps keep the AI boom running.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated July 10, 2026.

Note: Because SK hynix only began trading on Nasdaq on July 10, 2026, analyst coverage, Morningstar ratings, and other third-party research are not yet available for the new listing. As coverage develops, this information will provide additional insight into how the market is evaluating the company.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!