What Falling Interest Rates Mean for Your Portfolio

Last week, we explored how rising interest rates can challenge investors. This week, let us flip the script and talk about something that could actually work in your favour—falling rates. When interest rates drop, it is not just borrowers who feel the relief. If you know where to look, your stock portfolio can benefit too.

Why Do Central Banks Lower Interest Rates?

Central banks, like the Bank of Canada (BoC) or the US Federal Reserve (Fed), lower interest rates to stimulate a sluggish economy. Cheaper borrowing encourages spending and investment, helping businesses expand, creating jobs, and keeping inflation in check. Think of it as their way of giving the economy a boost when growth hits a wall.

How Falling Rates Impact Stocks

When interest rates fall, borrowing becomes cheaper, giving certain sectors a significant advantage. Growth-oriented industries, such as technology, can fund new projects and expand operations more easily, which often lifts their stock prices.

Real estate is another major beneficiary. Real Estate Investment Trusts (REITs), for example, rely on debt to finance property acquisitions and developments. With lower rates, their borrowing costs shrink, improving profitability. It is like snagging a lower mortgage rate—more cash stays available for growth.

Investors also tend to pivot away from bonds and savings accounts, which become less appealing as yields drop. This shift into stocks can give the overall market a broader boost.

On the flip side, financial stocks like banks and insurers may struggle. Lower rates reduce the margins on loans and mortgages, which can impact their profitability.

Consumer Spending and Stocks

Falling rates do not just help businesses – they also benefit consumers. Lower borrowing costs for mortgages, car loans, and other financing encourage spending. This increased confidence often benefits sectors like retail, travel, and luxury goods, as well as housing-related stocks.

How to Navigate Falling Rates as an Investor

- Spot Growth Opportunities: Focus on sectors like technology and real estate, which tend to thrive in low-rate environments.

- Monitor Financial Stocks: Banks and insurers might face challenges, so keep an eye on your financial holdings.

- Follow Consumer Spending Trends: Look to retail, travel, and other consumer-driven industries for potential gains.

Falling interest rates can open up exciting opportunities for your portfolio. By understanding which sectors thrive and which face challenges, you can adjust your strategy and position yourself for growth. Focus on the winners, keep an eye on shifting consumer behaviour, and adapt to these market changes to maximize your returns.

Now that we have covered how falling interest rates can benefit your portfolio, let’s take a closer look at how the markets played out over the past week.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, “Age of AI,” Canadian 2025 TFSA and RRSP limits, .…

Canadian Economic news

This past week’s key economic data that the BoC considers when deciding whether to raise or lower the interest rate.

Consumer price Index (CPI)

Statistics Canada’s latest CPI report revealed a bigger-than-expected jump in inflation. The annual rate rose to 2.0% in October, up from September’s 1.6%, while monthly inflation climbed 0.4% after a 0.4% decline the month prior. Analysts had anticipated smaller increases of 1.9% annually and 0.3% monthly.

Among CPI categories, ‘Clothing and footwear’ led the charge, surging 2.4% month-over-month, while ‘Health and personal care’ and ‘Recreation, education, and reading’ remained flat. On an annual basis, ‘Shelter’ saw the largest rise, up 4.8%, though slightly lower than September’s 5.0%. Meanwhile, gasoline prices provided some relief, dropping 4.0% year-over-year.

Core CPI, which excludes volatile items like food and energy, increased 0.5% monthly and rose 2.3% annually.

The higher-than-expected inflation was partly driven by gas prices, which did not drop as sharply as they did in September. While one month does not make a trend, this latest data may disappoint those hoping for a jumbo-sized 0.5% rate cut from the Bank of Canada (BoC). While inflation remains within the BoC’s target range of 1% to 3%, analysts are now divided on whether the bank will opt for a 0.25% or 0.5% cut in December. The final decision will hinge on other key data, including labour market and Gross Domestic Product figures, as policymakers assess the broader economic picture ahead of their December 11 meeting.

Retail Sales

Canadian retail sales rose 0.4% in September, matching August’s growth, with annual sales up 0.8% – a slight slowdown from the 1.4% gain seen in August. For the third quarter as a whole, sales rose 0.9%. An advance estimate for October indicates sales were up 0.7%, however, that number is likely to be revised as more data is reported.

Taking a closer look at the data, the ‘Building material and garden equipment and supplies dealers’ and the ‘Food and beverage retailers’ categories led the way, each posting a solid 3.0% monthly increase. On the other side, ‘Gasoline stations and fuel vendors’ continued their slump, with sales dropping 2.3% – marking the fifth consecutive month of declines. Year-over-year, ‘Health and personal care retailers’ shone brightest with a 3.5% sales boost, while ‘Gasoline stations and fuel vendors’ faced a sharp 9.8% decline.

Core retail sales, which strip out gas stations, fuel vendors, and motor vehicle and parts dealers, bounced back with a 1.4% monthly increase after a revised 0.5% dip in August. On an annual basis, core sales grew 1.9%, a significant improvement from August’s modest 0.3% growth.

The rebound in core sales hints that lower interest rates are energizing consumer spending, and with October’s strong initial data, the fourth quarter could be shaping up to give a needed boost to Canada’s stagnant economy.

Canadian market volatility

Canada’s Volatility Index (CVIX) began the week at 10.07 and experienced a sharp, brief spike on Tuesday morning, likely triggered by concerns over the Ukraine missile attack on Russia. However, it quickly stabilized around the 11-point level for the rest of the week, closing at 10.72 on Friday.

Tracked under the ticker VIXI on the Toronto Stock Exchange (TSE), the CVIX gauges how much market volatility investors expect. A reading below 10 points to a calm, stable market, while numbers between 10 and 20 signal typical market fluctuations with moderate volatility. But when the index climbs above 20, it is a sign of rising uncertainty and the potential for a bumpy ride ahead.

US Economic news

This past week’s key data points that the Fed considers when deciding whether to raise or lower the interest rate.

Consumer Sentiment Index (CSI)

The University of Michigan’s CSI closed November at 71.8, edging up from October’s 70.5 but falling short of the anticipated 73.7. This marks a modest 1.8% monthly increase and a robust 17.1% jump year-over-year, reflecting a steady recovery in consumer confidence.

Looking closer, the Current Economic Conditions index, which measures how people feel about their immediate financial situation, slipped 1.5% to 63.9 from October. Meanwhile, the forward-looking Index of Consumer Expectations climbed 3.8% to 76.9, a notable 35.4% improvement from the same time last year. This suggests a growing optimism about the months ahead, even as current conditions show slight strain.

November marks the fourth straight month of rising consumer sentiment, supported in part by easing interest rates. Political dynamics also played a notable role. Future expectations surged among Republicans to their highest level since 2021, while slipping for Democrats to a one-year low – highlighting contrasting perspectives on how the incoming administration’s policies could impact the economy. While this rise in optimism is encouraging, uncertainty lingers over the specifics of the new economic agenda.

American market volatility

The CBOE Volatility Index (VIX), often called the market’s ‘fear gauge,’ started the week at 16.58 and edged slightly lower to close at 15.24. With little in the way of major economic or political developments, market activity remained subdued, leaving earnings reports from big-name companies as the primary driver of the modest volatility shifts.

For some context, the VIX tracks expected market volatility over the next 30 days. When it is below 12, it signals a calm market. Readings between 12 and 20 reflect normal market swings. But once the VIX climbs into the 20-30 range, it indicates increased investor anxiety. Anything above 30 typically means the market is stressed, often a precursor to major turbulence or even a crisis.

“Age of AI”

This past week, all eyes turned to Nvidia (NASD: NVDA), the world’s most valuable company with a jaw-dropping US$3.6 trillion market cap (calculated by multiplying the share price by the total number of outstanding shares). Investors were eager to see if the tech behemoth could sustain its meteoric rise, fueled by surging demand from leading technology companies for Nvidia’s artificial intelligence (AI) chips driving their cutting-edge applications and services.

Once again, Nvidia delivered. The company reported third quarter revenues of $35.1 billion, surpassing Wall Street’s $33.2 billion forecast. Even better, Nvidia’s fourth quarter revenue outlook came in strong at $37.5 billion, slightly ahead of analyst expectations. This performance underscores the extraordinary demand for Nvidia’s high-powered, AI-focused chips, which sit at the core of the rapidly expanding AI market.

Looking ahead, the company’s optimism is centered on the launch of its next-generation Blackwell GPUs (Graphics Processing Units), expected to further accelerate revenue growth. Chief Executive Officer Jensen Huang captured the moment, calling it the “Age of AI,” a transformational era Nvidia is not just participating in but actively shaping through its groundbreaking innovations in AI computing.

While analysts praised the report, some raised concerns about potential near-term risks, including supply constraints and possible overheating issues with the Blackwell chips. These challenges could cause shipment delays, but they may also lead to demand outpacing supply – potentially deferring revenues rather than losing them outright. Despite these hurdles, Nvidia remains a favourite among analysts, bolstered by its unrivalled market dominance and remarkable growth in the AI sector.

Investor reactions were more muted, with Nvidia’s stock dipping 1% in after-hours trading. Even with revenues and adjusted earnings per share exceeding estimates, some investors may have been hoping for even bigger surprises to justify the company’s lofty valuation.

If you are not keeping up with technology companies or the AI craze, you might wonder why Nvidia is often considered the world’s most important stock. At the heart of the AI revolution, Nvidia is not just a player – it is a catalyst, providing the hardware and software driving explosive growth, industry advancements, and solutions to global challenges.

Nvidia is the crown jewel of the three portfolios, with its remarkable 291% share price growth since November 22, 2023, being a key driver of Portfolio 1’s performance. Their stellar results and bullish outlook suggest the AI rally has plenty of fuel left. As an owner of this exceptional company, I am pleased with this latest update. While the AI fuelled rally may be slowing, I am hopeful its far from over. 😊

Canadian 2025 TFSA and RRSP limits

The Canada Revenue Agency (CRA) has announced the 2025 contribution limits for Registered Retirement Savings Plans (RRSPs) and Tax-Free Savings Accounts (TFSAs). While I am not a tax expert (or an accountant), I wanted to share the key updates that matter most to Canadian investors like us. For personalized advice, it is always wise to consult a tax professional or certified financial planner.

TFSA Contribution Limit for 2025

The TFSA is a fantastic tool for growing your savings tax-free. Contributions are made with after-tax dollars, so all earnings and withdrawals within the account are tax-free. For 2025, the annual contribution limit remains at C$7,000, unchanged from 2024. Unused contribution room carries forward indefinitely, giving you flexibility to catch up whenever it suits you.

RRSP Contribution Limit for 2025

The RRSP offers immediate tax advantages, making it a powerful tool for building retirement savings. For 2025, the contribution limit is the lesser of 18% of your 2024 earned income (including self-employment and rental income) or C$32,490, plus any unused contribution room carried forward from previous years. Be aware that pension adjustments may reduce your available contribution room.

For more details on contribution rules and limits, check out the CRA’s resources on TFSA and RRSP limits, or consult a tax professional for advice tailored to your situation.

These accounts are some of the best tools to make your money work harder, helping you achieve long-term goals while keeping taxes in check. 😊

Weekly Market Review

Monday: the indexes kicked off the week with a strong start, but the Dow Jones Industrial Average (DJIA) could not keep the momentum going and fell into the red. Now, all eyes are on Nvidia as its Wednesday earnings report promises to shed light on the ever-evolving AI market. Oil prices rose after hostilities between Ukraine and Russia intensified.

In Canada, the Toronto Stock Exchange Composite Index (TSX) rose on higher oil and gold prices. In trading, Basic Materials (mining companies and fertilizer manufacturers) had the best day, while Consumer Staples had the worst day.

In the US, the S&P 500 Index (S&P) and the Nasdaq Composite Index (Nasdaq) both ended in the green thanks to a 5.6% jump in Tesla’s (NASD: TSLA) share price. In trading it was a day of broad-based gains led by the Energy sector. The Industrials sector was the only sector to post a loss.

Tuesday: a Ukraine missile attack into Russian territory leading to fears of nuclear escalation caused investors to rush into safe haven investments such as gold, the US dollar and Swiss francs resulting in an early morning sell off in stocks before spending rest of the session clawing back the losses. The DJIA was the only index that failed to get out of negative territory. Heightened tensions led investors to flock to gold, considered a traditional safe haven investment.

In Canada, a higher-than-expected CPI inflation report caused analysts to speculate that the BoC may cut rates by 0.25%, rather than 0.5%. That and higher gold prices lifted the TSX into positive territory. In trading, the Basic Materials sector advanced the most, while Consumer Staples declined the most.

In the US, excitement over Nvidia’s earnings report, due Wednesday, gave the technology sector a boost and lifted the Nasdaq and S&P into the green. In trading, the Technology sector was the big winner, while the Energy sector recorded the biggest drop.

Wednesday: all four indexes fell into the red in morning trading as investors grew cautious ahead of Nvidia’s highly anticipated earnings release after the end of the session. However, the Nasdaq was the only index unable to get out of the red by the end of the day. The spotlight was firmly on Nvidia to deliver another strong report that could sustain the markets’ upward momentum. With heightened tensions in Ukraine, investors have become more conservative with their investments. Oil prices were down slightly as tensions in the Ukraine – Russia war were offset by rising US crude oil stockpiles.

In Canada, for the third day this week the TSX was lifted by the Energy sector, despite lower oil prices. In trading, the Energy sector posted the largest gain, while Consumer Cyclicals sector suffered the biggest decline.

In the USA, the American indexes were mixed with the DJIA higher, the S&P flat and the Nasdaq lower as concerns about the Nvidia and the broader AI rally weighed on the market. In trading, the Healthcare sector rose the most, the Consumer Cyclicals sector dropped the most.

Thursday: all four indexes ended in the green, as investors digested Nvidia’s earnings report, and its implications for the AI rally. Oil prices were higher as the Ukraine – Russia conflict intensified.

In Canada, the TSX hit a record close thanks to government measures meant to stimulate the economy and higher commodity prices. In trading, it was a day of broad-based gains led by the Technology sector. The Communication Services sector was the only sector to close lower.

In the US, the Nasdaq and S&P were weighed down by the Department of Justice asking a federal judge to break up Alphabet’s (NASD: GOOGL) empire, and Amazon (NASD: AMZN) announced they were likely to be investigated by the European Union’s (EU) anti trust regulator, the European Commission (EC). In trading, the Utilities sector led all sectors while Consumer Cyclicals and Communication Services were the only sectors to end in the red.

Friday: positive economic news from both Canada and the US gave markets a strong finish to the week, with all four major indexes closing in the green. Oil prices moved higher amid growing tensions in the Middle East and Ukraine.

In Canada, stronger-than-expected retail sales lifted investor sentiment, propelling the TSX to another record high – topping yesterday’s milestone. On Bay Street, Industrials led the charge, while the Healthcare sector lagged.

South of the border, lower interest rates and optimism about possible upcoming business-friendly policies propelled the DJIA to a new record close. Investors seemed to rotate out of heavyweight tech stocks, shifting their focus to small-cap companies and a broader range of sectors. On Wall Street, Industrials led the charge as the top-performing sector, while Communication Services saw the steepest decline.

Weekly Market and Portfolio Review

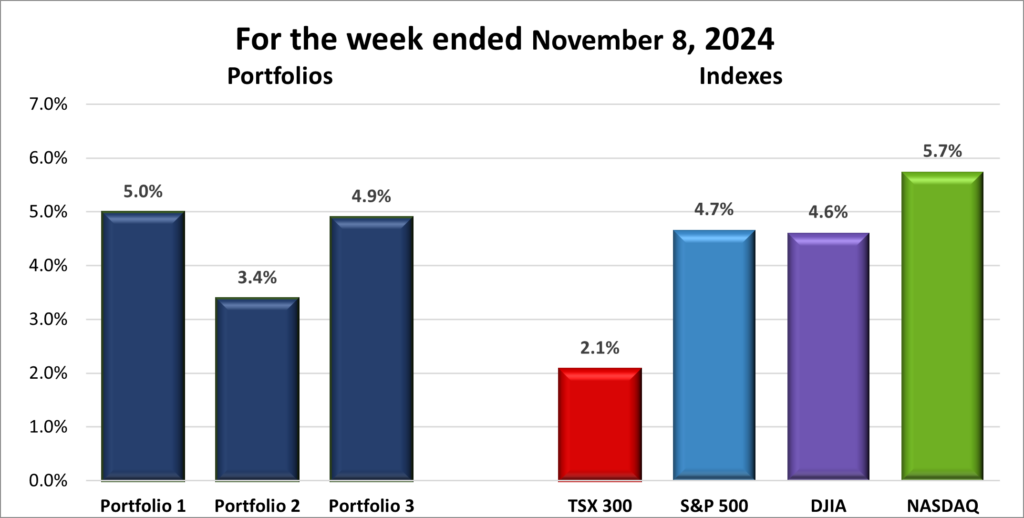

For the week, the TSX (SPTSX) surged 2.2%, the S&P 500 (SPX) rose 1.7%, the DJIA (INDU) jumped 2.0% and the Nasdaq (CCMP) rose 1.7%.

| Index | Weekly Streak |

| TSX: | 3 – week winning streak |

| S&P: | 1 – week winning streak |

| DJIA: | 1 – week winning streak |

| Nasdaq: | 1 – week winning streak |

![]() The markets had a strong week, with all four major indexes posting weekly gains, as shown in the weekly progress chart above. Leading the charge was Canada’s TSX, lifted by surging energy and gold prices as investors flocked to safe-haven assets amid escalating tensions between Ukraine and Russia. Federal stimulus measures aimed at reviving Canada’s sluggish economy and a better-than-expected retail sales report also gave the index a boost, propelling it to a record high. The only stumbling block was a hotter-than-expected inflation report, which dimmed hopes for a larger rate cut in December. Many now expect the BoC to opt for a modest 0.25% reduction instead of the more aggressive 0.5% “jumbo” cut.

The markets had a strong week, with all four major indexes posting weekly gains, as shown in the weekly progress chart above. Leading the charge was Canada’s TSX, lifted by surging energy and gold prices as investors flocked to safe-haven assets amid escalating tensions between Ukraine and Russia. Federal stimulus measures aimed at reviving Canada’s sluggish economy and a better-than-expected retail sales report also gave the index a boost, propelling it to a record high. The only stumbling block was a hotter-than-expected inflation report, which dimmed hopes for a larger rate cut in December. Many now expect the BoC to opt for a modest 0.25% reduction instead of the more aggressive 0.5% “jumbo” cut.

In the US, the week began with investor speculation about how the recent presidential election might influence the Fed’s upcoming rate decison. However, earnings season quickly stole the spotlight, with Nvidia – the AI poster child – a highly anticipated report. While its results impressed, they fell short of the lofty expectations of some investors, triggering a pullback after the midweek announcement. Even so, Nvidia’s earnings signaled that the AI rally isn’t over, even if its pace has cooled. Encouragingly, this week also showed signs of the rally broadening beyond heavyweight tech companies, with gains spreading across multiple sectors.

On the economic front, it was a relatively quiet week, though geopolitical tensions remained in sharp focus. Ukraine’s conflict regained the spotlight after both sides exchanged missile fire, briefly overshadowing tensions in the Middle East.

All in all, it was a solid week for the markets, bolstered by optimism around potential lower taxes and lighter regulations, the resilience of energy and gold, and signs that the AI rally still has room to grow. Looking ahead, next week’s economic data could set the tone, with US inflation numbers and Canada’s productivity report in the spotlight. If inflation surprises to the downside and productivity surprises to the upside, the markets could extend their rally. Let’s keep our fingers crossed for more good news! 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week winning streak |

| Portfolio 2: | 3 – week winning streak |

| Portfolio 3: | 3 – week winning streak |

![]() Another solid week for the portfolios, with all three gaining value. Portfolio 2 even outpaced the TSX, this week’s top-performing index, while Portfolio 3 barely made it into the green. Still, a win’s a win—progress is progress! 😊

Another solid week for the portfolios, with all three gaining value. Portfolio 2 even outpaced the TSX, this week’s top-performing index, while Portfolio 3 barely made it into the green. Still, a win’s a win—progress is progress! 😊

Portfolio 1 bounced back in style, with 82% of its holdings posting weekly gains. The stars of the show were Navitas Semiconductor (NASD: NVTS), which soared 36%, and Datadog (NASD: DDOG), up 21%. Other notable performers included Cloudflare (NYSE: NET) up 15%, Celsius Holdings (NASD: CELH) and indie Semiconductor (NASD: INDI), each up 14%, and Hammond Power Solutions (TSE: HPS.A) and Trade Desk (NASD: TTD), both climbing 10%. Walmart (NYSE: WMT) also hit an all-time high, though its weekly gain fell short of the double digits. The only downside was Nvidia gained just over 1% for the week.

Portfolio 2 was the top performer of the indexes and the portfolios, extending its winning streak to two weeks. A remarkable 81% of its holdings gained ground, led by MongoDB (NASD: MDB), which jumped 17%, and Hammond Power Solutions’ 10% gain. iA Financial Group (TSE: IAG) also reached an all-time high, adding to the portfolio’s strong showing.

Portfolio 3 lagged this week, but even a narrow win is still a win. About 63% of its holdings moved higher, with standout performances from Cloudflare, up 15%, and Vertiv Holdings (NYSE: VRT), which hit an all-time high with a 13% weekly gain.

By week’s end, all three portfolios were worth more than they started, with over 60% of each portfolio’s holdings in the green and no single company suffering a drop greater than 10%. Like I said at the start, whether it’s a big leap or a small step forward, I’ll take weekly wins any day. 😊

Companies on the Radar

This past week, two new companies caught my attention. The first is Global Dividend Growth Split Corp. (TSE: GDV), a Canadian investment company offering exposure to a diverse portfolio of global dividend-paying equities. With a current dividend yield of 9.87%, GDV aims to provide both income and capital appreciation.

This past week, two new companies caught my attention. The first is Global Dividend Growth Split Corp. (TSE: GDV), a Canadian investment company offering exposure to a diverse portfolio of global dividend-paying equities. With a current dividend yield of 9.87%, GDV aims to provide both income and capital appreciation.

The second is Cardinal Energy (TSE: CJ), a mid-cap Canadian oil and natural gas company. Cardinal stands out with its impressive 11.16% dividend yield, displaying its focus on rewarding shareholders.

Despite the eye-catching dividends, neither company will be staying on my radar list next week. While those yields are tempting, I have my doubts about their ability to maintain such generous payouts. With plenty of other opportunities out there – like the two companies listed below – I am happy to move on.

Once again, the Radar Check has done exactly what it is meant to do: save time and help me focus on the most promising prospects.

- On Holding AG (NYSE: ONON), a medium cap Swiss company, founder-run, sports products company.

- Topaz Energy Corp. (TSE: TPZ), a mid-cap Canadian energy investment firm that focuses on strategic investments in premium energy assets operated by top-tier Canadian companies, and currently pays a 4.69% dividend.

As always, these are not buy recommendations – be sure to do your own research and make decisions that align with your personal financial goals!

The Radar Check was last updated November 22, 2024.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended November 22, 2024: UP ![]()

- Nvidia is running into delays for their newest Blackwell chips which are used for AI applications. The chips reportedly overheat when joined together in server racks that can hold up to 72 of the chips. Nvidia, its suppliers and customers are working together to resolve the problem. In the short term this is not good news, but the company will need to resolve the problem otherwise they could open the door to their competitors.

- The Department of Justice has argued that Alphabet’s Google should be required to sell its Chrome browser, share data and search results with competitors, and potentially take other measures to break its alleged monopoly in online search. Obviously, Google opposes these recommendations, claiming they are “wildly overboard.” The final decision on whether to implement these remedies now rests with a federal judge.

- Amazon said they were likely to be investigated by the EU’s anti trust regulator, the EC. Amazon has been charged with favouring their own products brands in their e-commerce marketplace at the expense of other merchants.

In other Amazon news, the company invested an additional US$4 billion in AI startup Anthropic, bringing their total investment to $8 billion.

Activity

Remember the covered call I wrote for Nvidia a few weeks ago? Well, as trading wrapped up on November 22, the stock price remained below the agreed strike price, which means the option expired worthless (that is a win for me 😊). In simple terms, I get to keep both my Nvidia shares and the premium the buyer paid me upfront for the option. Think of it like getting paid a nonrefundable downpayment for agreeing to sell your house at a certain price, but the potential buyer never followed through – you keep the house AND the downpayment!

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Decisive Dividend Corp (TSEV: DE) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

Walmart Inc.

Third quarter 2024 financial results on November 19, 2024

Nvidia Corporation

Third quarter 2025 financial results on November 20, 2024

Portfolio 2

Portfolio 2 for the week ended November 22, 2024: UP ![]()

- TC Energy (TSE: TRP) announced plans to move forward with four projects totalling C$1.5 billion, including the conversion of two existing power plants from coal to cleaner, natural gas-powered operations.

- Microsoft (NASD: MSFT) announced they were building two new semiconductors for their own data centres. These custom designed chips will reduce Microsoft’s reliance on the higher end, expensive Nvidia chips.

Activity

After adding a new company and boosting shares in existing holdings the previous week, I still had enough cash left to do a bit more shopping. This week, I decided to increase my stake in Brookfield Infrastructure Partners L.P. (TSE: BIP.UN), doubling down on my confidence in their long-term potential. 😊

Bought: Brookfield Infrastructure Partners L.P. I first invested in Brookfield Infrastructure Partners L.P. back in 2018, and while the journey has had its ups and downs, one thing has remained consistent: its reliable dividend, which has never dipped below 3%. Today, the stock offers an attractive 4.75% yield, and with its current upward trajectory, I decided to increase my position (still exceedingly small 😊).

What makes BIP.UN stand out is its focus on high-demand, high-growth sectors like cell towers and data centres – key infrastructure for generative AI and emerging technologies. Its strong financial performance over the years, with consistent growth in revenue, income, cash flow, and EPS, reflects its solid execution. Margins are robust too, with a 25.4% gross margin and 23.8% operating income margin for the last twelve months and in line with the margins over the last five years, showcasing profitability despite a modest free cash flow margin of 0.33%.

Since spinning off from Brookfield Corporation in 2007, BIP.UN has built a diversified portfolio spanning utilities, transport, energy, and data infrastructure. This provides both stability and growth opportunities, backed by a reputation for operational excellence.

Of course, no investment is without risks. Rising interest rates could increase debt servicing costs, while economic downturns or regulatory changes may impact operations. Global exposure brings currency fluctuations into play, and its focus on capital-intensive sectors like cell towers and data centres could face delays or cost overruns. Additionally, the modest free cash flow margin might limit flexibility.

Ultimately, success hinges on Brookfield’s ability to execute its ambitious investments effectively. With its strong reputation and history of delivering results, I feel confident increasing my investment in BIP.UN, expecting steady, reliable dividends with some growth potential thrown in. Not a bad combination! 😊

Dividends

Dividends Received this week for the following companies:

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended November 22, 2024: UP ![]()

- Brookfield Corporation (TSE: BN) is reportedly preparing to acquire Spanish drugmaker Grifols (OTCM: GIKLY) for €7 billion. Brookfield is looking to take advantage of a 30% drop in Grifols’s market value due to being accused of overstating earnings and understating debt, which Grifols denied.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

No dividends this past week.

Quarterly Reports

Real Matters Inc.

Fourth quarter 2024 financial results on November 21, 2024