Many professional investors took a break for the Christmas holidays, leading to light trading in the Canadian and American markets. I also stepped back from closely tracking daily market moves, but one thing stood out—the absence of a Santa Claus rally this year. As a result, three of the four major indexes, with only the Nasdaq Composite Index (Nasdaq) spared, and all three of my portfolios posted losses for December, though they still managed gains for the year overall.

With December, and 2024, officially behind us, this ‘Weekly Update’ offers a quick visual snapshot of how the indexes and my portfolios fared over the past two weeks, and for December as a whole. I’ve kept this week’s update brief, letting the charts do most of the talking. After all, they say a picture is worth a thousand words, so with four charts, consider this a four-thousand-word recap! 😊

Without further ado ….

Weekly Market and Portfolio Review

Over the last two weeks, the TSX (SPTSX) advanced 1.9%, the S&P (SPX) edged upward 0.2%, the DJIA (INDU) lost 0.3% and the Nasdaq (CCMP) gained 0.3%.

Streaks as of January 3, 2025

Index

Weekly Streak

Portfolio

Weekly Streak

TSX:

2 – week winning streak

Portfolio 1:

1 – week winning streak

S&P:

1 – week losing streak

Portfolio 2:

1 – week winning streak

DJIA:

1 – week losing streak

Portfolio 3:

1 – week winning streak

Nasdaq:

1 – week losing streak

The first week of the Christmas break brought a glimmer of hope as the markets enjoyed the start of a Santa Claus rally. In the second week, the Grinch swooped in, threatening to snatch back those hard-earned gains. But a rally at the start of the new year saved the day, ensuring all three portfolios kicked off the new year with a weekly win. 😊 Here’s hoping it’s a sign of good things to come as we work toward growing the value of our investments in 2025. 😊

Monthly Market and Portfolio Review

For the month, the TSX (SPTSX) lost 3.4%, the S&P 500 (SPX) dropped 2.5%, the DJIA (INDU) plunged 5.3%, while the Nasdaq (CCMP) rose 0.5%.

After a stellar November, I was hopeful the momentum would carry into December—and at first, it seemed promising. All four indexes started the month strong, as shown in the monthly progress chart above. However, the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), and the Dow Jones Industrial Average (DJIA), soon lost steam. The turning point came with the US Federal Reserve’s announcement of only two expected interest rate cuts in 2025. For many, this signaled rates could stay higher for longer, raising borrowing costs and triggering sharp declines across the indexes.

In Canada, the TSX faced additional pressure from political uncertainty following Finance Minister Chrystia Freeland’s unexpected resignation, leaving investors uneasy about the potential impact on economic policies and market stability.

A brief Santa Claus rally offered some hope, lifting markets slightly before a final year-end pullback. Ultimately, the Nasdaq was the only index to finish December in the green, while the others closed out the month in the red.

Hopefully, this pullback is nothing more than the professional money managers cleaning up their portfolios to look good at the end of the year. Once the pros are back in January and trading volume picks up again, the markets will pick up and the indexes will resume their relentless march upward.

Turning to the portfolios, all three struggled to sustain November’s momentum, ending December with declines. Given that three of the four indexes also lost ground, this wasn’t entirely unexpected. However, the biggest surprise came from Portfolio 2, which, as the most balanced and typically least volatile, posted the largest drop of the three.

Ending the year on a brighter note, all three portfolios posted solid quarterly gains, with Portfolios 1 and 3 delivering standout performances, achieving double-digit growth, and easily outperforming the indexes. For the year as a whole, all three portfolios increased in value, with Portfolio 1 more than doubling the return of the top-performing index, the Nasdaq, and Portfolio 3 surpassing every index except the Nasdaq. All in all, it’s been a great year! 😊 Here’s to more wins in 2025—wishing you all the best for the new year!

This marks the final Weekly Update of 2024 – time flies when you’re navigating the markets, doesn’t it? 😊 I’ll be taking the next two weeks off, but don’t worry, the scintillating commentary will return on January 3, 2025.

A heartfelt thank you for sticking with me through the ups and downs of the market this year. Here’s to hoping 2025 keeps the bull run alive that’s been charging ahead since early 2023. 😊 In the meantime, enjoy the Christmas holiday season as 2024 wraps up, and may the new year bring you health, happiness, and, of course, prosperity!

It is the final week before Christmas, and the markets kept us on our toes with a flurry of economic data. But rather than dive straight into the numbers, I thought a little Christmas spirit would set the tone for this Weekly Update. So, without further ado, here is an investing spin on a Christmas classic!

‘Twas the Night Before Christmas

”Twas the week before Christmas, and all through the Street,

The markets were stirring, not ready to retreat.

Investors were watching their tickers with care,

In hopes that a Santa Rally soon would be there.

The bulls were nestled, still dreaming of gains,

While whispers of rate cuts danced in their brains.

And I with my spreadsheets, all set for review,

Had just settled in to assess what I knew.

When out on the floor there arose such a clatter,

I sprang to the charts to see what was the matter.

Away to the data I flew like a flash,

Checking the headlines for signs of a crash.

The candles on charts with their flickering glow,

Gave a glimmer of hope to the bulls down below.

When what to my wondering eyes should appear,

But a strong rebound rally to close out the year.

With a savvy old trader, so sharp and so quick,

I knew in a moment it must be St. Nick.

More rapid than algo trades, upward they came,

And he whistled and shouted and called them by name::

“Now Apple! Now Tesla! Now Microsoft, too!

On Nvidia! On Amazon! On stocks breaking through!

To the top of the charts, to the highs we can see,

Dash away! Cash away! A green close is key!”

As dry powder’s deployed when opportunities call,

When buyers step in to prevent a freefall,

So up to the new highs the tickers they flew,

With portfolios rising and St. Nicholas, too.

And then, in a twinkling, I heard on the news,

The Fed’s steady stance calming Wall Street’s views.

As I refreshed my screen and was spinning around,

Down came St. Nick with a leap and a bound.

He was dressed like a trader from head to his feet,

And his suit was as crisp as the Nasdaq’s last beat.

A bundle of insights he had in his hand,

Ready to share with investors across the land.

His eyes – how they twinkled! His wisdom so cheery!

His forecasts were balanced, not overly dreary.

He spoke of the long game, of patience and care,

Of building portfolios designed to outlast a scare.

“The markets, my friend, can be fickle, it’s true,

But stay in the game, and returns will accrue.

Diversify wisely, avoid chasing the trend,

And remember, each dip can bring gains in the end.”

He finished his speech with a wink of his eye,

And soared from the market with gains flying high.

But I heard him exclaim as he vanished from sight,

“Happy investing to all, and to all a good night!”

While St. Nick and his rallying bulls might be a fun holiday vision, the real markets were not quite as magical this week. Let’s take a look at how the Fed – and Santa – shaped the markets as we head into the final stretch before Christmas.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news,

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Government fiscal update

As many had expected, the fiscal update revealed that the federal government missed one of its key fiscal targets for the 2023/2024 budget, running a fiscal deficit of C$40 billion. However, what caught many off guard was just how badly they overshot their goal, with the deficit coming in at a whopping $61.9 billion—nearly 50% higher than projected.

The news was further shaken up by Finance Minister Chrystia Freeland’s sudden resignation just hours before the Fall Economic Statement. Her departure has left a significant void in the government, raising critical questions about the future direction of Canada’s economic policies. The timing – just before such an important fiscal update – has only deepened the uncertainty about the government’s ability to manage the country’s finances and fueled the political intrigue surrounding her unexpected exit.

Consumer price Index (CPI)

Statistics Canada reported that inflation remained flat in November, slowing from October’s 0.4% increase, and coming in slightly better than the expected 0.1% rise. On an annual basis, inflation stood at 1.9%, just shy of October’s 2.0% and the rate analysts had forecast.

Monthly data showed ‘Food’ prices rising the most with a 0.5% increase, while ‘Household operations, furnishings, and equipment’ saw the steepest drop, declining 0.9%. On a yearly basis, ‘Shelter’ costs, which include mortgages and rent, continued to cool but still posted the largest increase at 4.6%, down from October’s 4.8%. In contrast, prices for ‘Clothing and footwear’ had the sharpest annual decline, falling 3.8%. Inflationary pressures are easing overall but rising costs in key areas like food and shelter still weigh on consumers.

Core CPI, which excludes volatile the food and energy categories, also cooled. It dropped 0.1% month over month and slowed to a yearly growth rate of 1.9%, down from 2.3% in October.

With both the annual headline and core inflation rates dipping below the BoC 2% target, the central bank is likely to return to smaller, more conventional rate cuts of 0.25%, following the last two jumbo sized 0.5% reductions. However, December’s inflation data could shift the narrative – if the numbers come in higher than expected, the BoC might pause its rate-cutting to reassess.

For now, the BoC’s priority seems to be supporting economic growth, but it faces a tricky balancing act. On one hand, letting Canadian interest rates fall too far below US levels could weaken the loonie, driving up the cost of US imports and risking a new bout of inflation. On the other hand, keeping rates too high could stifle domestic growth, which the economy can ill afford.

Retail sales

Statistics Canada reported that retail sales in Canada rose by 0.6% in October, surpassing September’s 0.4% increase but falling short of analysts’ expectations of a 0.7% gain. On a year-over-year basis, sales grew by 1.5%, a stronger performance than the 0.8% increase in September, and ahead of the expected 0.8%.

At the sector level, the ‘Furniture, home furnishings, electronics, and appliances’ category saw the largest monthly gain, jumping 2.5%. On the flip side, ‘Food and beverage retailers’ experienced the biggest decline, down 0.7%. Year-over-year, ‘Motor vehicle and parts dealers’ posted the largest sales increase, up 3.6%, while ‘Gasoline stations and fuel vendors’ reported the biggest annual drop for the second consecutive month, down 5.9%.

Core retail sales, which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers, rose 0.2% in October, a slowdown from September’s 1.4% increase. Annually, core sales were up 1.8%, slightly below the 1.9% growth in September.

This data suggests retail spending is beginning to slow, reflecting the broader trend of a cooling Canadian economy. Since retail sales account for nearly 40% of total consumer spending and are considered an early indicator of GDP growth, this slowdown may signal a slowdown in overall economic momentum. Statistics Canada also provided an early estimate for November, which will be published on January 23, 2025, indicating that the pace of retail sales was largely unchanged.

Canadian market volatility

Canada’s Volatility Index (VIXC) had a relatively calm week, starting at 9.23 before spiking to 11.90 on Wednesday following the US Federal Reserve’s announcement that they only expect to lower US rates twice in 2025. Investor anxiety fluctuated throughout the week, but the VIXC eased back slightly, closing at 11.66—on the lower end of what is considered normal market fluctuations.

Tracked under the ticker VIXI on the Toronto Stock Exchange (TSE), the VIXC measures investor expectations for market volatility. A reading below 10 signals a calm, stable market, while numbers between 10 and 20 indicate typical market fluctuations with moderate volatility. When the index rises above 20, it reflects increased uncertainty and the potential for a bumpier ride ahead.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

FOMC rate decision

At its final Federal Open Market Committee (FOMC) meeting of the year, Fed Chair Jerome Powell announced a widely expected 0.25% cut to the benchmark interest rate, lowering it to a range of 4.25%–4.5%. While the move itself did not surprise analysts or investors, the Fed’s updated forecast – predicting just two rate cuts in 2025, down from four projected in September – caught markets off guard. Investors interpreted this revised outlook as a potential signal of a pause in rate cuts as early as January.

The decision was not unanimous, with one member dissenting in favour of holding rates steady. This marks only the second instance during the Fed’s current rate-cutting cycle where a member did not agree with the majority decision. The latest adjustment is the third cut this year, following a 0.5% reduction in September and a 0.25% cut in November. The updated forecast reflects persistent concerns about stubborn inflation, which the Fed expects could remain elevated into the new year.

Future rate decisions will hinge on whether inflation resumes its downward trajectory after recent resistance. Adding to the uncertainty are the sweeping tax reforms and deregulation efforts promised by the incoming Trump administration, which could further complicate the Fed’s delicate balancing act between fostering economic growth and keeping inflation in check. As 2025 approaches, all eyes will be on the Fed to see how it navigates these competing pressures.

Retail sales

The Commerce Department’s Census Bureau reported a stronger-than-expected November 2024 Advance Monthly Retail Sales report, showing a 0.7% increase in retail and food services sales. This beat analyst expectations of a 0.5% rise and followed an upwardly revised 0.4% gain in October. On an annual basis, retail sales climbed 3.8%, improving on October’s revised growth of 2.9%.

The impact of lower interest rates was evident in the 2.8% surge in sales in the ‘Auto & Other Motor Vehicle Dealers’ category, marking the biggest monthly increase. Meanwhile, ‘Miscellaneous Store Retailers’ experienced the steepest drop, down 3.4% for the month. Year-over-year, ‘Nonstore Retailers’ (online shopping) led the pack with a 9.9% jump, while spending at ‘Gasoline Stations’ declined 3.9%, likely due to lower fuel prices.

Core retail sales – which exclude the volatile categories of motor vehicles, parts, and gasoline—rose modestly by 0.2% in November, following a 0.1% increase in October. Annually, core sales continued their steady climb, rising 3.9%, slightly higher than October’s 3.8% growth.

This latest report underscores the resilience of the American consumer, with lower interest rates, a strong labour market, and rising wages fueling increased retail sales. Car purchases, in particular, surged to their strongest level in three years, while robust Cyber Weekend sales gave online shopping a notable boost. Consumer confidence has also climbed since the presidential election, buoyed by expectations of lower rates and reduced taxes.

This latest data is unlikely to influence the Fed’s rate decision tomorrow, as higher holiday sales are typically expected. However, the stronger-than-anticipated figures are sure to grab their attention as they remain vigilant for signs of rising inflation. When combined with the potential impact of lower taxes, import tariffs, and the pro-growth agenda of the new administration, this retail sales momentum could prompt the Fed to reconsider further rate cuts in January.

Gross Domestic Product (GDP)

The final reading of third-quarter GDP revealed stronger-than-expected growth, with the economy expanding at an annualized rate of 3.1%. This marks an upward revision from the second estimate of 2.8% and exceeds analysts’ forecasts of 2.8%. The revision reflects improved data across key areas: exports, consumer spending, non-residential fixed investment, and federal government spending. These gains were partially offset by a decline in private inventory investment and a steeper drop in residential fixed investment.

With GDP accelerating from 1.6% in the first quarter to 3.0% in the second, and now 3.1% in the third quarter, the data suggests the economy will finish 2024 on a strong note. Analysts now turn to the advance estimate for fourth-quarter GDP, scheduled for release on January 30, 2025, to determine if this momentum carried through the year’s final stretch.

Personal Consumption Expenditures (PCE)

The Commerce Department’s Bureau of Economic Analysis reported that inflation, as measured by the PCE Price Index, slowed to 0.1% in November on a monthly basis, falling short of analysts’ expectations for a 0.2% rise and after two consecutive months of 0.2% increases. On an annual basis, the headline PCE (which includes all items) rose 2.4%, slightly below October’s 2.6% and the forecasted 2.5%.

Core PCE, the Fed’s preferred inflation gauge, which excludes the more volatile food and energy sectors, also came in softer than expected. It rose just 0.1% in November, down from October’s 0.3% increase. Year-over-year, core PCE eased to 2.8%, a noticeable drop from October’s 3.2%, and below the anticipated 2.9%.

After a series of reports showing inflation holding steady or rising slightly, this latest data suggests inflationary pressures are continuing to cool, providing the Fed with some breathing room. While the slowdown in price growth is a positive sign, the Fed remains cautious, as core inflation is still above their 2% target.

The December PCE is scheduled for release on January 31, 2025.

Consumer Sentiment Index (CSI)

The University of Michigan’s final Consumer Sentiment Index (CSI) for December landed at 74, matching expectations and reaching its highest level since April 2024. This marks a 3.1% boost from November’s 71.8 and a solid 6.2% improvement over December 2023, when it stood at 69.7. The December reading also marked the fifth consecutive monthly gain, highlighting a steady climb in consumer confidence.

Digging deeper, the Current Economic Conditions index – which measures how consumers feel about their present financial situation – surged to 75.1. This impressive 17.5% jump from November’s 63.9 contrasts with a more modest 2.5% increase compared to December 2023. Meanwhile, the Index of Consumer Expectations, which gauges optimism about the next six months, slipped 4.7% to 73.3 from November’s 79.9. Still, it remains 8.8% higher than last December’s 67.4.

The rise in overall sentiment appears to be driven by favourable buying conditions for big-ticket items like cars and appliances, supported by lower interest rates and a strong labour market. Many consumers are adopting a “buy now, avoid paying more later” mindset, anticipating the potential for rising interest rates or import tariffs to drive up costs in the future. Interestingly, political affiliation influenced expectations: Republicans were optimistic about improving conditions, while Democrats were more cautious.

American market volatility

The CBOE Volatility Index (VIX), known as the market’s “fear gauge,” started the week at 14.37 and gradually crept higher as investors anticipated the midweek FOMC rate decision. When the Fed announced fewer rate cuts for next year, the VIX spiked to 27.62, a dramatic 74% jump—its largest single-day surge since February 2018. Afterward, the VIX dipped just as sharply, only to rise again above 26 before tumbling back down on Friday, closing the week at 18.37.

For context, the VIX measures expected market volatility over the next 30 days. Readings below 12 signal a calm market, while values between 12 and 20 reflect normal market fluctuations. When the VIX rises into the 20-30 range, it indicates heightened investor anxiety, and anything above 30 typically signals market stress, often foreshadowing major turbulence or even a crisis.

Weekly Market Review

Monday: The week kicked off with a bit of mixed sentiment as the S&P 500 Index (S&P) and the Nasdaq Composite Index (Nasdaq) finished the day in the green, while the Toronto Stock Exchange Composite Index (TSX) and the Dow Jones Industrial Average (DJIA) closed lower. Investors were largely holding their breath ahead of the Fed’s midweek rate update, with most expecting a 0.25% rate cut. Meanwhile, oil prices took a dip, weighed down by weaker-than-expected Chinese retail sales data.

In Canada, the TSX was weighed down by lower oil price and the sudden resignation of the Finance Minister. In trading, Financials was the only sector to advance, while Communication Services had the worst day.

In the US, the Nasdaq soared on the backs of the heavyweight technology companies to another record high in anticipation of a rate cut later this week. On the downside, the DJIA dropped for the eighth straight session, its longest losing streak since June 2018. In trading, the Consumer Cyclicals sector rose the most, while the Energy sector saw the biggest decline.

Tuesday: after a mixed start yesterday, it got worse with all four indexes ending in the red as investors await the Fed’s rate decision tomorrow. Oil prices fell on poor economic reports from the world’s second and third largest economies, China and Germany, respectively.

In Canada, political uncertainty at the federal level, with lower commodity prices, and mixed inflation data combined to knock the TSX to its lowest point in four weeks. In trading, the Healthcare sector posted the biggest gain, while the Communication Services fell the farthest.

In the US, the markets fell after higher-than-expected retail sales data hinted a rate cut tomorrow could be the last cut for a while. The DJIA’s losing streak stretched to nine games, its longest losing streak since February 1978. The DJIA has been weighed down by profit taking in Nvidia (NASD: NVDA) after its recent run up, and UnitedHealth (NYSE: UNH) following the murder of their Chief Executive Officer. In trading, it was a day of wide-ranging losses with only the Consumer Cyclicals able to climb higher, while the Industrials sector dropped the most.

Wednesday: all four indexes were relatively flat prior to the Fed’s rate announcement but they plunged after the Fed announced they expected fewer rate cuts in 2025. Oil prices also fell on the news from the Fed.

In Canada, the TSX was dragged down by the US Fed announcement, sending the index to its lowest level in six weeks. It was a day of across-the-board losses in trading, with the Communication Services sector the best of the lot while the Technology sector fell the farthest.

In the USA, all three indexes reversed earlier gains following the Fed’s announcement. The DJIA extended its losing streak to 10 sessions, its longest since 1974 (50 years). In trading, all sectors lost ground. The Healthcare sector dropped the least while the Consumer Cyclicals sector fell the farthest.

Thursday: the markets started off on the right foot, rebounding from yesterday’s sell off, but at the end of the day only the DJIA remained in the green, making today slightly better than yesterday. Oil prices dropped on concerns that sticky inflation could slow rate cuts and eat into demand.

In Canada, worries over a more aggressive stance from the US Fed weighed heavily on the markets, pushing the Canadian dollar lower and extending the TSX’s losing streak to six straight sessions—its longest slide since October 2023. In trading it was another day of across-the-board losses, with Consumer Staples falling the least and Industrials falling the farthest.

In the USA, the DJIA snaps its longest losing streak in 50 years, barely getting into positive territory. In trading, the Utilities sector increased the most, while the Basic Materials (mining companies and fertilizer manufacturers) gave up the most ground.

Friday: the indexes had a rough start, but all four quickly bounced back after lower-than-expected inflation data from the PCE report, ending the day solidly higher. Oil was down slightly, weighed down by concerns over weaker global demand and an impending supply surplus.

In Canada, the TSX made a strong comeback after six straight losing sessions, boosted by higher commodity prices and lower inflation in the US. The Healthcare sector led the way with impressive gains, while Consumer Staples was the only sector to finish in the red.

In the US, a potential government shutdown was averted at the last minute, bringing relief to investors and employees alike. The three major indexes each posted gains of at least 1%, helped by the inflation data suggesting that price pressures are continuing to ease. It was a day of broad-based gains, with all sectors closing in the green, led by the Technology sector, while Consumer Staples lagged behind.

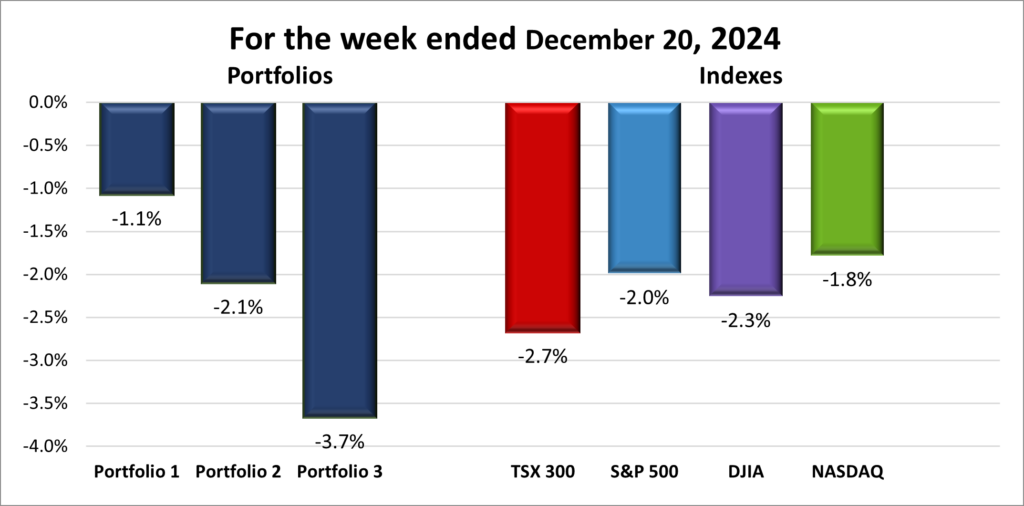

Weekly Market and Portfolio Review

For the week, the TSX (SPTSX) plunged 2.7%, the S&P 500 (SPX) fell 2.0%, the DJIA (INDU) lost 2.3% and the Nasdaq (CCMP) sank 1.8%.

Index

Weekly Streak

TSX:

2 – week losing streak

S&P:

2 – week losing streak

DJIA:

3 – week losing streak

Nasdaq:

1 – week losing streak

The Santa Claus rally seems to be struggling to take off this year. Despite a sharp rebound at the end of the week, all four major indexes still recorded weekly losses, as highlighted in the performance chart above.

The week started on a rocky note, with Nvidia playing an outsized role in dragging down the three American indexes. A sharp 12% drop in Nvidia’s share price – marking a correction from its all-time high in early November – had a significant impact, as the heavyweight is a component of the S&P 500, Nasdaq, and DJIA. This alone set a negative tone, but things went from bad to worse after the Fed’s much-anticipated rate announcement.

While the Fed delivered a widely expected 0.25% rate cut, it was their guidance for 2025 that sent shockwaves through the markets. The Fed indicated it only expects to lower rates twice next year, a sharp contrast to their earlier forecast of four cuts. This cautious stance, driven by concerns over stalled inflation progress, triggered a broad sell-off in both the US and Canadian markets. The DJIA dropped over 1,100 points as investors processed the reality of slower rate relief. However, the American economy remains strong, and the Fed is unlikely to raise rates again anytime soon.

Adding to the mix, the looming threat of a government shutdown added a layer of volatility to the American markets. Political uncertainty of this kind rattles investors, especially as the budget impasse raises concerns about economic disruptions. With the second Trump term looming, markets are bracing for even more political drama.

In Canada, the TSX faced a rough start to the week, and things worsened after the Fed’s announcement of just two rate cuts in 2025. With last week’s cut behind us, it seems the Fed will likely pause further rate reductions for now. If US interest rates hold steady while Canada’s continue to fall, the Canadian dollar could weaken, making US imports more expensive for Canadians. A hawkish Fed typically strengthens the US dollar by attracting foreign capital, putting pressure on other currencies like the loonie. While a weaker loonie could spark inflation by driving up import costs, a stronger US dollar could make Canadian exports more attractive, potentially boosting demand for Canadian goods.

As we move into the final weeks of the year, market volatility is likely to persist as investors digest the latest inflation data and the Fed’s rate cut forecast. Hopefully, Santa’s got his reindeer ready to go, and the Santa rally finally makes an appearance next week! 😊

Portfolio

Weekly Streak

Portfolio 1:

2 – week losing streak

Portfolio 2:

2 – week losing streak

Portfolio 3:

2 – week losing streak

It was a rough week across the board for the three portfolios, mirroring the tough conditions in the markets. Unfortunately, none managed to eke out a gain, with all posting losses of at least 2%.

Portfolio 1 emerged as the “least worst,” limiting its losses to 1.1%. Only 13% of its holdings managed weekly gains, but Mitek Systems (NASD: MITK) stole the spotlight with a 30% surge following a strong earnings report. On the flip side, Innovative Industrial Properties (NYSE: IIPR) plummeted 28% after it was announced that it was being investigated for securities fraud, and Celsius Holdings (NASD: CELH) slid 13%. Alphabet (NASD: GOOGL) hit an all-time high early in the week before reversing to finish lower at the end of the week. Nvidia, the portfolio’s largest holding, chipped in a modest 1% gain, helping soften the blow and keeping the portfolio’s decline the smallest of the portfolios and the four indexes.

Portfolio 2 had the highest percentage of stocks posting gains, with 22% in the green—not exactly a high bar. Still, it wasn’t enough to avoid a weekly loss above 2%.

Portfolio 3 had a tough week all around, posting the largest percentage decline of the three portfolios. Only 13% of its holdings managed to post gains, and there was no standout performer to offset the broader losses. Unlike Portfolio 1, which benefited from Nvidia’s modest gain, Portfolio 3 lacked any significant holding to help limit the damage, resulting in a particularly rough showing.

Tough weeks like this are part of the investing journey. Let’s see what next week brings—hopefully, the Santa Claus rally will finally begin, bringing a brighter outlook for the portfolios! 😊

Weekly Portfolio & Index performance for the week ended December 20, 2024.

Companies on the Radar

This week, I stumbled upon a company that initially did not pass my Radar Check but still piqued my interest—Rubrik, Inc. (NASD: RBRK). Despite presenting a few red flags, including no net income, no operating income, and negative cash flow, I was intrigued by the company’s potential. Rubrik is a large American company in the rapidly growing cybersecurity industry, with over 3,000 employees across 22 global offices and a market cap of over US$13 billion. Founded in 2014 and going public just this past April, the company’s size and the sheer scale of the cybersecurity market have me curious enough to dig deeper.

On the flip side, I’ve decided to part ways with Domino’s Pizza (NYSE: DPZ), the giant pizza chain. While it is a well-established company, its relatively low dividend does not fit the income profile I am after, and its growth potential does not quite align with my goals for more aggressive, growth-oriented stocks.

With one company making its way onto my radar and another exiting, my list remains at four companies, including the ones listed below.

On Holding AG (NYSE: ONON), a medium cap Swiss company, founder-run, sports products company.

Topaz Energy Corp. (TSE: TPZ), a mid-cap Canadian energy investment firm that focuses on strategic investments in premium energy assets operated by top-tier Canadian companies, and currently pays a dividend in the 5% neighbourhood.

Topicus.com Inc. (TSE.V: TOI), a mid-cap spinoff from Constellation in 2020, focusing on delivering vertical software solutions in the European Union market.

As always, these are not buy recommendations – be sure to do your own research and make decisions that align with your personal financial goals!

The Radar Check was last updated December 20, 2024.

Stock on the Radar List. 1 of 2.Stock on the Radar List. 2 of 2.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended December 20, 2024: DOWN

Alphabet’s Waymo autonomous car division announced they will start testing their robotaxis in Japan, starting in 2025. It will be Waymo’s first entrance into a foreign market.

Walmart (NYSE: WMT) has teamed up with Chinese delivery giant Meituan to enhance its delivery services in China. Meituan, the country’s leading platform for quick delivery of everyday household goods, will now feature Walmart on its app. This partnership aims to accelerate Walmart’s e-commerce growth in the Chinese market by tapping into Meituan’s extensive customer base and efficient delivery network.

In other Walmart news, the company was named Yahoo Finance’s Company of the Year. The company has quietly morphed into a leader of utilizing technology, building up their capabilities in artificial intelligence (AI), online advertising through their acquisition of TV maker Visio, same day delivery service, not to mention inexpensive groceries.

Amazon.com (NASD: AMZN) employees at seven US fulfilment centres went on strike during the holiday shopping rush, over the company’s refusal to recognize the Teamsters Union.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Portfolio 2 for the week ended December 20, 2024: DOWN

Guardant Health (NASD: GH) announced they will be working with Boehringer Ingelheim, a German pharmaceutical company. The partnership aims to secure regulatory approval for Guardant’s cutting-edge Guardant360 CDx test as a companion diagnostic to identify non-small cell lung cancer patients who could benefit from one of Boehringer’s advanced cancer treatments.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

SmartCentres Real Estate Investment Trust (TSE: SRU.UN)

Portfolio 3 for the week ended December 20, 2024: DOWN

Enghouse Systems (TSE: ENGH), announced its United Kingdom division had purchased Aculab PLC, for an undisclosed price. Aculab specializes in on-premise and cloud-based communications solutions as well as AI driven answering machine technology.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

SmartCentres Real Estate Investment Trust (TSE: SRU.UN) DRIP

We are not in the era of Skynet – the rogue AI from The Terminator movies – just yet, but Artificial intelligence (AI) has moved from science fiction to everyday life, and tools like ChatGPT have become the poster child of this transformation. Launched just two years ago, ChatGPT isn’t just a tech innovation – it’s a prime example of how AI is reshaping the way we communicate, work, and even invest. For investors keen on spotting trends, understanding ChatGPT’s rise and its impact on industries offers valuable insights into how AI is driving change and creating new opportunities. But first, let’s start with the basics: what exactly is a chatbot?

Chatbots are virtual assistants designed to interact with people through text or voice, helping with everything from answering questions to managing tasks. They come in two flavors: rule-based chatbots that follow scripts for simple tasks, and AI-powered ones like ChatGPT that use innovative technology to understand context and hold dynamic, meaningful conversations. Whether streamlining customer service, powering virtual assistants like Siri, or enhancing online shopping, chatbots are changing how we interact with technology in ways that are fast, efficient, and surprisingly human-like.

Now that we know what a chatbot is, let’s take a look at OpenAI’s ChatGPT.

What is ChatGPT? A Closer Look at OpenAI’s Breakthrough

ChatGPT, developed by OpenAI and introduced in November 2022, is an AI-powered chatbot designed to generate human-like responses. Using GPT (Generative Pre-trained Transformer) technology, it simulates dynamic, meaningful conversations, making it a versatile tool for writing, coding, brainstorming, and more. OpenAI, co-founded in 2015 by visionaries like Elon Musk and Sam Altman, has established itself as an innovator in the AI space, with backing from key supporters like Microsoft (NASD: MSFT).

The chatbot’s versatility, coupled with OpenAI’s commitment to ethical AI development, has helped ChatGPT capture widespread attention. Whether it’s generating content or simplifying complex ideas, ChatGPT showcases how AI is not only reshaping industries but also making technology accessible to millions.

ChatGPT doesn’t learn from your individual chats (your chats are private!), but it’s always improving, meaning it can provide more accurate and useful responses over time. Think of it as your creative assistant, always ready to lend a hand with content creation, strategies, or simply making complex ideas easier to understand. Whether you’re writing a blog post (like me), exploring investment options, or diving into something new, it’s here to help.

How Does ChatGPT Compare to Its Competitors?

While ChatGPT is a standout, it’s part of a rapidly growing field of AI-powered tools. Though it was the first to capture the public’s attention, several other companies have developed their own AI assistants. Here’s a look at some of the major players and what they specialize in:

Microsoft Copilot: A productivity powerhouse, Copilot integrates with Microsoft Office, making tasks like email drafting and report creation seamless. Its strength lies in its focus on workplace efficiency.

Google Gemini: Known for its versatility, Gemini handles text, images, and video. It’s an all-in-one AI tool.

Claude by Anthropic: Prioritizing user safety, Claude emphasizes ethical AI use and excels in coding but lacks real-time web access or image capabilities.

Meta AI’s Llama: An open-source option for developers, Llama offers unmatched flexibility but requires significant resources and expertise to customize effectively.

Amazon’s Alexa: Renowned for voice commands and smart home integration, Alexa shines in task-based assistance but isn’t built for deep, conversational AI like ChatGPT.

Each tool has its own strengths, but ChatGPT’s versatility across industries makes it a great choice – whether for personal projects or business applications. I’ve used Copilot, Gemini, and Claude, but I always find myself coming back to ChatGPT (I even used it to proofread this text! 😊). My experience with Alexa is pretty basic – mostly weather updates and setting timers 😊 – and I haven’t had a chance to try Llama yet. With so many AI options available, it’s interesting to see how these tools continue to evolve.

How is AI Impacting Businesses?

AI’s influence goes far beyond just chatbots. Industries across the board are tapping into its transformative power, customizing its capabilities to address unique challenges and unlock new opportunities. Here’s how some key sectors are embracing AI to innovate and thrive:

Healthcare: AI is revolutionizing patient care and diagnostics. Tools like ChatGPT assist in medical research by analyzing vast datasets to uncover insights quickly, while machine learning models are improving early disease detection, such as identifying cancer through imaging scans. Companies like IBM (NYSE: IBM), through its Watson Health division, use AI to help patients better understand their symptoms and navigate healthcare services more efficiently.

Finance: In the financial sector, AI streamlines processes like fraud detection, algorithmic trading, and personalized financial planning. Financial companies such as the Royal Bank of Canada (TSE: RY), JPMorgan Chase (NYSE: JPM), and Visa (NYSE: V) use AI to analyze transaction patterns and flag suspicious activities, while investment firms leverage machine learning models to predict market trends and optimize portfolios.

Manufacturing: Factories are becoming smarter through AI-driven automation. Predictive maintenance systems analyze machinery data to reduce downtime and extend equipment life. Companies like Tesla (NASD: TSLA) and Rockwell Automation (NYSE: ROK) are utilizing AI to enhancing precision in assembly lines and logistics.

Retail and E-Commerce: AI is reshaping how businesses connect with consumers. Personalized recommendation engines – like those used by Amazon (NASD: AMZN) and Shopify (TSE: SHOP) – analyze user behavior to suggest products, while AI chatbots handle customer inquiries in real-time, improving the shopping experience. Additionally, AI-driven inventory management systems optimize stock levels and reduce waste.

Transportation and Logistics: Autonomous vehicles are taking the spotlight, with companies like Tesla and Alphabet’s (NASD: GOOGL) Waymo leading the charge. AI also optimizes supply chain logistics, enabling companies to predict demand, improve route efficiency, and reduce fuel consumption, ultimately lowering costs and environmental impact.

Energy and Utilities: AI helps utilities manage power grids more efficiently by integrating renewable energy sources while balancing supply and demand. Companies like NextEra Energy (NYSE: NEE) use AI to predict energy production from solar and wind farms, enhancing reliability. In oil and gas, AI driven analytics optimize exploration and production processes.

Entertainment and Media: AI powers personalized content recommendations on platforms like Netflix (NASD: NFLX) and Spotify (NASD: SPOT), creating highly tailored user experiences. It’s also being used in content creation, from generating scripts to designing immersive video game environments.

Agriculture: Companies like Deere & Company (NYSE: DE) are using AI to make farming smarter with technologies like precision agriculture, where drones and sensors gather data to optimize crop planting, irrigation, and pest control. This helps maximize yields and minimize resource use, supporting more sustainable farming practices.

Education: AI-powered tools are reshaping learning experiences. Platforms like Duolingo (NASD: DUOL) use adaptive learning algorithms to tailor lessons to individual students’ needs, while tools like ChatGPT assist with tutoring, helping students grasp complex subjects more effectively.

From improving operational efficiency to driving innovation, AI’s integration across industries demonstrates its potential to create value, solve complex problems, and unlock new growth opportunities. As these technologies mature, their impact on industries – and the investment opportunities they generate – will only continue to grow.

Why Should Investors Pay Attention?

The AI market is projected to skyrocket to US$826 billion by 2030, driven by its integration into industries like healthcare, manufacturing, finance, and beyond. As AI reshapes efficiency and innovation, investors have a unique opportunity to tap into this fast-growing market.

Tech giants such as Nvidia (NASD: NVDA), Microsoft, and Alphabet are at the forefront of this revolution. Nvidia’s cutting-edge GPUs form the backbone of many AI advancements, Microsoft is integrating AI tools like Copilot into its ecosystem, and Alphabet (Google) is driving progress with AI-powered Google Search and its autonomous vehicle division, Waymo.

But the AI ecosystem extends far beyond the headline-grabbing tech giants. Companies like AMD (NASD: AMD) and Intel (NASD: INTC) are fierce competitors in the AI semiconductor race, while data centre operators such as Equinix (NASD: EQIX) and Digital Realty Trust (NYSE: DLR) provide the infrastructure to handle AI’s massive computational demands. Supporting this backbone are companies like Vertiv Holdings (NYSE: VRT), which deliver essential infrastructure and services to keep data centres running efficiently, reliably, and sustainably. Even utilities like NextEra Energy are stepping up to meet AI’s growing energy needs, often leveraging renewable sources to power this tech revolution.

By understanding the relationship between these key industries, investors can uncover opportunities across the entire AI ecosystem—not just in the companies creating AI tools and capturing the headlines, but also in the sectors enabling its widespread adoption.

AI: A Revolution in Progress

ChatGPT burst onto the scene just over two years ago, marking a pivotal moment in the rise of AI. Since then, AI has been reshaping industries, driving technological breakthroughs, and unlocking possibilities that once seemed like science fiction. For investors, the opportunities go far beyond the creators of AI tools. By exploring the broader ecosystem – from chipmakers to the builders and operators of data centres, and even the utilities supplying the immense energy required – you can position yourself to ride this transformative wave.

While the AI market is still in its early stages, its potential to disrupt industries and create value is undeniable. This isn’t just another technology trend; it’s a revolution in progress. For us investors, it’s a chance to gain early exposure to one of the most impactful technological shifts of our time. The future of AI is bright, the opportunities are vast, and its ability to shape the world – and your portfolio – is simply too significant to ignore. AI could be a game-changer for growing your Wealth Through Investing! 😊

How Economic Indicators Influence the Stock Market

Ever wonder how the broader economy ties into your investments? Economic indicators like Gross Domestic Product (GDP), unemployment rates, and inflation serve as the heartbeat of the economy, giving us a window into its health and influencing stock market movements. Understanding these metrics can feel like unlocking a cheat code – helping you spot trends, anticipate changes, and make decisions with confidence. Let us explore these key indicators and their influence on your investments.

Gross Domestic Product (GDP)

Think of GDP as the economy’s report card. It measures the total value of goods and services a country produces within a specific timeframe—usually quarterly or annually. When GDP is climbing, it signals a thriving economy. Businesses are booming, sales are up, and profits are flowing, conditions that often drive stock prices higher.

But it is not always sunshine. A falling GDP can hint at an economic slowdown or recession. With lower consumer spending and shrinking corporate profits, stock prices often take a hit. While Canada has not technically seen a GDP decline, growth has been sluggish, largely fuelled by high immigration rather than increased productivity. Meanwhile, the US continues to benefit from more robust economic expansion.

Unemployment Rate

The unemployment rate is another key barometer of economic health. Low unemployment means more people with jobs, more disposable income, and more spending – music to the ears of companies and their shareholders. This virtuous cycle often supports rising stock prices.

Rising unemployment is often a warning sign for the economy. With fewer people earning paychecks, consumer spending tends to drop, which can lead to weaker corporate earnings and downward pressure on the market. Keeping an eye on unemployment trends provides valuable insights into consumer behaviour and overall market sentiment.

Inflation

Inflation measures how much prices for goods and services are increasing over time, eroding your purchasing power bit by bit. It is often tracked using metrics like the Consumer Price Index (CPI) or the Personal Consumption Expenditures (PCE) Price Index. The CPI highlights how inflation hits your wallet directly, while the PCE offers a broader perspective that is favoured by the US Federal Reserve for shaping policy.

Moderate inflation is a sign of a growing economy – it is like the Goldilocks zone, boosting confidence without overheating the system. But when inflation spirals out of control, it drives up business costs and squeezes profit margins, often dragging stock prices down. Central banks respond by raising interest rates, which can make borrowing more expensive and weigh on corporate earnings, further pressuring markets.

Bringing It All Together

Economic indicators do not operate in isolation—they are all deeply connected. High unemployment can weigh on GDP, while surging inflation often prompts higher interest rates, slowing economic growth and affecting jobs. When the economy strikes the right balance—rising GDP, low unemployment, and moderate inflation—investor confidence grows, and stock prices tend to climb. But when that balance tips, markets can face turbulence.

Conclusion

GDP, unemployment, and inflation are more than just headlines— they are powerful tools for understanding market trends. While they will not make you a market psychic, staying informed about these relationships can sharpen your decisions and strengthen your long-term strategy. With patience and sound judgement, you will be well-equipped to ride out market ups and downs.

Now that we have covered the basics, let’s see how one of these indicators, the latest US inflation data, shaped North American markets this past week.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Bank of Canada makes another super sized cut

For the second consecutive time, the Bank of Canada delivered a super-sized 0.5% rate cut, bringing its benchmark interest rate down to 3.25%. This marks the fifth straight reduction and underscores the central bank’s efforts to support a faltering economy while keeping inflation within its 1% – 3% target range.

The decision follows weaker-than-expected economic growth in the third quarter and a rise in unemployment to 6.8% – a near eight-year high when excluding the pandemic years. BoC Governor Tiff Macklem noted that while further rate cuts remain an option, the Bank plans to take a more measured approach moving forward, potentially opting for smaller 0.25% cuts or even pausing reductions. He also reassured Canadians that a recession is not on the horizon.

However, challenges persist. Canada’s recent economic growth has been heavily reliant on immigration, which is projected to slow in the coming years. Additionally, the looming threat of tariffs from the incoming Trump administration could add uncertainty to trade and economic stability.

On the positive side, the rate cut is expected to provide relief for debt-burdened Canadians, particularly those with variable-rate mortgages. The Bank also highlighted the temporary GST holiday, which could drive consumer spending during the holiday season and provide a short-term boost to the economy. While this may nudge inflation upwards, any effects are expected to fade once the holiday ends.

Overall, it is a solid announcement. Canadians benefit from lower interest rates, with many banks already reflecting this change. That said, some clouds loom on the horizon, hinting at challenges that could shape the road ahead.

Canadian market volatility

Canada’s Volatility Index (CVIX) had a relatively calm week, starting at 9.12 and hovering mostly between 8 and 9. Midweek excitement struck when the Bank of Canada announced a 0.5% rate cut, causing the CVIX to spike sharply to 10.49. However, the excitement was short-lived, as the index gradually descended through the remainder of the week, closing at a serene 7.39.

Tracked under the ticker VIXI on the Toronto Stock Exchange (TSE), the CVIX gauges how much market volatility investors expect. A reading below 10 points to a calm, stable market, while numbers between 10 and 20 signal typical market fluctuations with moderate volatility. But when the index climbs above 20, it is a sign of rising uncertainty and the potential for a bumpy ride ahead.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Consumer price Index (CPI)

The Labor Department’s November CPI report landed right on target, showing inflation ticking up slightly. Monthly inflation rose 0.3%, edging higher than October’s 0.2% increase, while the annual CPI climbed to 2.7%, up from 2.6% the previous month.

In the details, the ‘Used cars and trucks’ category posted the biggest monthly gain, jumping 2.0%, while ‘Electricity’ costs dipped 0.4%. Year over year, the ‘Transportation services’ category continued its sharp ascent, rising 7.1%, while the ‘Fuel oil’ prices category plunged 19.5%. On the housing front – a key area for many households – ‘Shelter’ costs rose 0.3% in November, a slight cooldown from October’s 0.4%. Annually, shelter costs increased 4.7%, easing from 4.9% in the prior month.

Core CPI, which excludes the often-volatile food and energy categories, rose 0.3% monthly for the fourth consecutive month and climbed 3.3% annually for the third month in a row.

This latest data suggests that while inflation has come down from last year’s highs, the pace of improvement has stalled above the Fed’s 2% target. Fortunately, there were no surprises in the report, reinforcing expectations that the Fed will move ahead with its third straight rate cut – likely a 0.25% reduction—at next week’s meeting. We will find out next week!

American market volatility

The CBOE Volatility Index (VIX), often called the market’s “fear gauge,” began the week at 13.37 and mostly traded within a tight 13.0–14.0 range. Midweek, the VIX briefly spiked above 14 on inflation concerns but settled back down as the CPI report met expectations and helped calm investor nerves. By the end of the week, the VIX closed slightly higher than where it started at 13.81.

For some context, the VIX tracks expected market volatility over the next 30 days. When it is below 12, it signals a calm market. Readings between 12 and 20 reflect normal market swings. But once the VIX climbs into the 20-30 range, it indicates increased investor anxiety. Anything above 30 typically means the market is stressed, often a precursor to major turbulence or even a crisis.

Weekly Market Review

Monday: the markets took a breather as all four indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – ended lower. Oil prices rose as China’s interest rate adjustment spurred hopes of increased demand, while the fall of the Syrian government added to supply concerns in the Middle East.

In Canada, despite touching an intraday high and higher commodity prices, the TSX was unable to overcome losses in the majority of sectors. In trading, the Basic Materials (miners and fertilizer manufacturers) sector gained the most, while the Utilities sector had the largest decline.

In the US, the three American indexes were weighed down by news that Nvidia (NASD: NVDA) was being investigated by China on antitrust issues. Many investors saw the investigation as a response to the US restricting semiconductor sales to China. Nvidia’s drop dragged other technology shares lower. In trading, Healthcare was the only sector to end in the green, while the Financials sector was the deepest in the red.

Tuesday: not a great day in the markets as all four indexes ended in the red. Oil prices were little changed despite the potential disruption caused by the overthrow of the Syrian government.

In Canada, investors appear to be taking a breather as investors await the BoC’s latest interest rate announcement. Many analysts are expecting a jumbo sized 0.5% rate cut after the latest labour data showed a sharp increase in unemployment. In trading, it was a day of broad-based declines, with only the Consumer Cyclicals sector able to post a gain. Healthcare saw the biggest decline.

In the US, investors are waiting for tomorrow’s CPI inflation report to provide clues about whether they should expect a rate cut at the Fed’s meeting next week. In trading, the Communications Services sector recorded the biggest increase following Google’s announcement of their new quantum computing chip (see Portfolio Updates, Portfolio 1). On the downside, the Technology sector suffered the biggest decline.

Wednesday: the markets rebounded with all but the DJIA ending in positive territory. Oil prices rose following China’s latest efforts to kickstart their slumping economy caused investors to anticipate greater demand for oil. Also boosting oil prices was news that the European Union agreed to further sanctions of Russia that could impact global oil supplies.

In Canada, the BoC lowered interest rates by 0.5% making it cheaper to borrow money, sending the TSX into the green. In trading, the Basic Materials sector rose the highest, while the Healthcare sector dropped the most.

In the USA, mild inflation data increased investor confidence that the Fed will lower rates at their meeting next week, sparking a run in the heavyweight technology companies that led to the Nasdaq breaking 20,000 for the first time. The mini rally also dragged the S&P into the green, while the DJIA was weighed down by health insurers following the introduction of a bill that is seen as limiting their profits. In trading, Communication Services was the big winner, while Healthcare saw the biggest decline.

Thursday: another down day in the markets following hotter than expected inflation data from the US Producer Price Index (PPI) report raised concerns about the Fed’s upcoming rate decision. Oil prices remained steady as over supply concerns were counterbalanced by expectations of lower interest rates.

In Canada, the TSX was weighed down by lower commodity prices, and concerns about the economy amid looming tariff threats. In trading, Consumer Staples was the only sector to squeak out a gain, while Basic Materials suffered the largest decline.

In the US, doubt creeped into investors’ minds after producer prices came in higher than anticipated, dragging all three indexes into the red. It was a day of broad-based losses, as Consumer Staples was the only sector to rise, while Consumer Cyclicals dropped the farthest.

Friday: a mixed day in the markets to end a tough week, with the TSX, S&P, and DJIA all losing ground, while the Nasdaq gained ground. Oil prices ended higher due to supply concerns following new sanctions on Iran and Russia, coupled with expectations that lower interest rates would boost demand.

In Canada, lower commodity prices dragged the TSX into negative territory. In trading on Bay Street, Technology was the only sector to advance, the Basic Materials sector sank the furthest.

In the US, the DJIA ran its daily losing streak to seven, weighed down by health insurance companies, while a rally in the heavyweight technology companies was enough to lift the Nasdaq into positive territory. In trading on Wall Street, the Technology sector recorded the biggest increase, while the Communication Services sector saw the biggest decrease.

Weekly Market and Portfolio Review

For the week, the TSX (SPTSX) fell 1.6%, the S&P 500 (SPX) dropped 0.6%, the DJIA (INDU) declined 1.8% and the Nasdaq (CCMP) bucked the downward trend and gained 0.3%.

Index

Weekly Streak

TSX:

1 – week losing streak

S&P:

1 – week losing streak

DJIA:

2 – week losing streak

Nasdaq:

4 – week winning streak

The markets struggled to maintain the previous week’s upward momentum, with a downward trend taking over – aside from a brief midweek rally. The spotlight was on US inflation data, sparking both excitement and uncertainty.

Ahead of the CPI report, markets drifted lower, but when the numbers met expectations, investor enthusiasm soared. The Nasdaq celebrated a historic milestone, crossing the 20,000 mark for the first time and reaching another all-time high. This rally was fueled by hopes for another Fed rate cut and continued optimism around AI and the technology heavyweights, even as Nvidia faced potential headwinds from a Chinese antitrust investigation – widely seen as more political than legal.

Later in the week, hotter-than-expected PPI numbers reignited inflation concerns, which tempered some of the optimism. Despite this, many analysts and investors are still betting on a 0.25% rate cut in next week.

In Canada, the TSX saw its winning streak snapped, weighed down by falling commodity prices and looming tariff threats. While the BoC’s rate cut offered some relief for borrowers, many saw it as a sign that the economy could be in rougher shape than previously thought. They might not be wrong. ☹

This week was a clear reminder of how swiftly market sentiment can shift. Don’t get caught up in the short-term noise – it pays to stay focused on the bigger picture: growing your wealth! 😊 And hey, the Santa Claus rally could kick off any time now.

Portfolio

Weekly Streak

Portfolio 1:

1 – week losing streak

Portfolio 2:

1 – week losing streak

Portfolio 3:

1 – week losing streak

As shown in the weekly percentage change chart below, it was a tough week for all three portfolios, with each losing over 1% in value during a challenging week for the markets. Portfolio 1 led the pack with the highest percentage of weekly gainers among the three – but at just 38%, it wasn’t much to celebrate. Winning percentages that low make it hard to make headway.

After last week’s strong performance, Portfolio 1 gave back much of those gains, slipping 2%. Only 38% of its holdings managed to end the week in the green, and unfortunately, Nvidia wasn’t among the winners this time. ☹ While there were not any standout gainers, Cameco (TSE: CCO) took a significant 10% hit.

On a brighter note, members of the Magnificent 7 in the portfolio – Apple (NASD: AAPL), Amazon (NASD: AMZN), and Alphabet (NASD: GOOGL) – reached record highs, offering a silver lining. Celestica (TSE: CLS) also made its mark as the only Canadian company in the portfolio to achieve an all-time high.

Portfolio 2 had the roughest week, with just 18% of its holdings posting gains. A sharp 27% drop in MongoDB (NASD: MDB) – one of the portfolio’s larger holdings – was a key factor in its struggles.

Portfolio 3 held up slightly better than the others, dropping “only” 1.4%. That said, it still underperformed both the Nasdaq and the S&P. Only 38% of the companies in the portfolio posted a weekly gain, making it challenging to offset the losses. Enghouse Systems (TSE: ENGH) was a major drag, tumbling 12% after lower-than-expected revenue in their fourth quarter earnings report.

Overall, it wasn’t a good week for the portfolios, with none seeing more than 38% of their holdings in the green. It’s tough to advance when declines outweigh gains. Here’s hoping for some positive economic news next week, coupled with a rate cut from the Fed, to give markets – and the portfolios – a much-needed boost to get back into the win column. 😊

Weekly Portfolio & Index performance for the week ended December 13, 2024.

Companies on the Radar

No new companies caught my attention this week, but I did whittle my radar list down to four. Dropping off the list was Genuine Parts Company (NYSE: GPC), the American auto and industrial parts distributor. With a dividend yield under 1%, it did not make the cut as an income generator. And while it is a solid, steady-growth company, I am after faster-growing names – preferably with the kind of explosive growth we have seen from Nvidia, which has soared 382% over the past two years. 😊 It is all about finding the right mix of income and growth to match my strategy!

On Holding AG (NYSE: ONON), a medium cap Swiss company, founder-run, sports products company.

Domino’s Pizza (NYSE: DPZ), the well-known American pizza giant.

Topaz Energy Corp. (TSE: TPZ), a mid-cap Canadian energy investment firm that focuses on strategic investments in premium energy assets operated by top-tier Canadian companies, and currently pays a 4.89% dividend.

Topicus.com Inc. (TSE.V: TOI), a mid-cap spinoff from Constellation in 2020, focusing on delivering vertical software solutions in the European Union market.

As always, these are not buy recommendations – be sure to do your own research and make decisions that align with your personal financial goals!

The Radar Check was last updated December 13, 2024.

Stock on the Radar List. 1 of 2.Stock on the Radar List. 2 of 2.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended December 13, 2024: DOWN

In a firm response to US government trade sanctions, China’s antitrust regulator, the State Administration for Market Regulation, announced an investigation into Nvidia. The probe centres on suspicions that Nvidia breached the terms of the conditional approval granted by China in 2020 for its acquisition of Israeli networking firm, Mellanox Technologies.

On a more positive note, Nvidia recently added 200 employees in China to their autonomous vehicle (AV) research unit as the company seeks to integrate itself further into the growing AV industry.

Alphabet’s Google claimed it made a breakthrough in quantum computing. Google claims its new ‘Willow’ quantum chip was able to solve a mathematical equation in five minutes, whereas a supercomputer would take over ten septillion years, which is longer than the entire history of the universe.

General Motors (NYSE: GM) announced they were ‘restructuring’ their Cruise robotaxi unit and focusing their energies on self driving technologies that can be used by everyone. The Cruise unit will be combined with GM’s autonomous driving unit. GM said increasing competitiveness in the robotaxi market led to their decision, leaving Tesla (NASD: TSLA) and Alphabet’s Waymo unit alone in the robotaxi market.

Activity

Sold:Rivian Automotive (NASD: RIVN) After two rounds of investments in Rivian Automotive and a loss of 75% of the total investment, I finally decided it was time to pull the plug. I held on for three years, rooting for the company’s success. Unfortunately, Rivian is still not profitable, continues to burn through cash, and has seen its negative profit margins grow.

The EV market is becoming increasingly competitive, with fierce rivals like Tesla, General Motors, and a slew of new entrants. Adding to the uncertainty, the incoming US administration has threatened to eliminate subsidies, casting doubt on the future of EV sales and the stability of some EV companies.

While it was a tough decision to sell my shares in Rivian, I believe there are better opportunities to grow the portfolio both within the current holdings and beyond. I have to take my lumps on this investment, but by reallocating the funds to more promising companies, I have a better chance at growing my wealth elsewhere.

Sold: Boston Omaha (NASD: BOC) I made my initial investment in Boston Omaha back in May 2020, partly because one of the co-founders is a relative of Warren Buffet – who has not done a bad job with Berkshire Hathaway (NYSE: BRK.B) 😊. I doubled down in October 2021 after the share price had more than doubled. However, since then, the stock price has plummeted and then remained relatively flat, with a slight decline recently. This lack of growth is concerning. While the company might start to grow in the future, I do not want to wait for it to become another Berkshire Hathaway. 😊

Given that Boston Omaha represents a very small portion of the overall portfolio, it was an obvious choice as I continue to trim Portfolio 1’s holdings to a more manageable number. Over the past year, Boston Omaha’s stock has underperformed compared to the broader market. While the S&P saw a return of around 30% (as of December 13), Boston Omaha’s share price dropped by 3.82%. Overall, the investment lost 14%, which, while not as significant as the loss with Rivian, is still a loss. More importantly, I do not see the share price climbing out of that hole any time soon. With that in mind, I decided to move on and look for better opportunities to grow my wealth elsewhere.

Dividends

Dividends Received this week for the following companies:

Portfolio 2 for the week ended December 13, 2024: DOWN

When GM announced it was shutting down its robotaxi ambitions, Microsoft (NASD: MSFT) incurred a US$800 million charge tied to its 2021 investment in the venture.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

December is here, bringing hope that this historically strong month for stocks will close out the year on a high note. 2024 has already seen indexes setting and breaking record highs, leaving investors eager for a festive flourish to finish the year. Historically, December has earned its reputation as a strong performer, thanks in part to the “Santa Claus rally.” This phenomenon often lifts markets during the last week of December and the first few trading days of January. While the rally is not guaranteed, several factors help explain why December tends to shine.

What Fuels December’s Market Optimism?

December’s upbeat reputation stems from a mix of seasonal factors that often work in favour of the markets. For starters, positive sentiment tends to dominate this time of year. Strong holiday spending, year-end bonuses, and the general cheer of the season can boost consumer confidence, creating a ripple effect in the stock market. Investors, buoyed by the festive spirit, are often more optimistic, which can drive prices higher.

Portfolio rebalancing also plays a big role. As the year winds down, fund managers and individual investors adjust their holdings to lock in gains, optimize tax strategies, or prepare for the new year. This activity often creates short-term buying pressure, adding to December’s upward momentum.

Lighter trading volumes during the holiday season are another factor. With many traders and institutional investors taking time off, leaving the field open to us smaller retail investors. 😊 This reduced activity can amplify market moves, often skewing them to the upside. Meanwhile, key economic data – such as retail sales, consumer confidence, and employment reports – can provide an additional boost. Strong holiday shopping figures, in particular, tend to lift retail and consumer stocks.

Finally, the Bank of Canada and US Federal Reserve meetings in December are always worth watching. This year, it is less about whether they will cut interest rates and more about how big those rate cuts will be. Surprises in rate decisions or forward guidance could steer markets in unexpected directions. And let us not overlook the holiday spirit itself – optimism and a reduced focus on negative news often set a positive tone for markets during this season.

What is the Takeaway for Us Investors?

While December’s track record gives us plenty of reasons to feel hopeful, it is a good reminder that the markets do not follow a script. Past performance is never a guarantee of future results – but here is to closing the year with a little holiday cheer! 😊

With December’s market optimism in mind, let’s shift gears and take a look at how the markets performed this past week.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Labour Force Survey (LFS)

Statistics Canada’s Labour Force Survey for November revealed a mixed bag for Canada’s job market. The economy added 51,000 jobs—more than double analysts’ expectations of 25,000 and a sharp increase from the 14,500 jobs added in October. However, most of this growth came from the public sector (funded by taxpayers) rather than the private sector, raising concerns about the long-term sustainability of these gains.

Meanwhile, the unemployment rate climbed to 6.8% in November, up from 6.5% in October and above the expected 6.6%. Monthly unemployment increased by 6.1%, and year-over-year, it is up 22.2%. Excluding the pandemic years, this marks the highest unemployment rate since January 2017. This rise underscores a growing challenge: while jobs are being added, they are not keeping up with population growth, pushing unemployment higher.

For workers, there is a silver lining in wages. Average hourly earnings rose 4.1% year-over-year in November, though this was a slowdown from October’s 4.9% pace. While slower wage growth is not ideal for workers, it helps on the inflation front, as businesses are less likely to pass rising labour costs onto consumers, potentially easing inflationary pressures.

This latest data will undoubtedly weigh on the BoC’s upcoming rate decision. Rising unemployment and cooling wage growth strengthen the case for a more aggressive rate cut, with many expecting the BoC to lower the benchmark interest rate by 0.5% to 3.25% next week. While such a move could offer relief to borrowers, it highlights the ongoing struggles facing Canada’s labour market.

Canadian market volatility

Canada’s Volatility Index (CVIX) had an eventful week, starting at 10.84 before seeing some early-week jitters with spikes to the 11.5 range. However, thoughts of rate cuts in Canada and the US quickly calmed investors, allowing the CVIX to drift lower for the remainder of the week, ending at 9.12.

Tracked under the ticker VIXI on the Toronto Stock Exchange (TSE), the CVIX gauges how much market volatility investors expect. A reading below 10 points to a calm, stable market, while numbers between 10 and 20 signal typical market fluctuations with moderate volatility. But when the index climbs above 20, it is a sign of rising uncertainty and the potential for a bumpy ride ahead.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Labour data

Recent reports from the Labor Department’s Job Openings and Labor Turnover Survey (JOLTS), the Bureau of Labor Statistics’ Employment Situation Summary (ESS), and the ADP Employment Report provide valuable insights into the current state of the US labour market.

JOLTS

The October JOLTS report showed a modest uptick in job openings, rising to 7.7 million, up from a 3.5-year low of 7.4 million in September. This exceeded analysts’ expectations of 7.475 million openings. However, compared to last year, job openings have decreased by 941,000. The job openings-to-unemployed worker ratio held steady at 1.1, meaning there are still more available jobs than there are job seekers. Despite slower hiring, businesses remain confident and continue to seek workers, indicating a tight labour market.

ADP

The ADP National Employment Report for November revealed a gain of 146,000 jobs, falling short of the 150,000 expected and down from 233,000 in October. Of these, 120,000 were created by large companies (500+ employees). While the numbers missed expectations, they still reflect a resilient job market. However, the slowdown suggests that the labour market may be cooling slightly.

ESS

The November Employment Situation Summary came in stronger than expected, with non-farm payrolls increasing by 227,000—well above the forecasted 200,000. This follows a smaller increase of just 12,000 jobs in October, which was impacted by hurricanes and the Boeing (NYSE: BA) strike. The unemployment rate rose slightly to 4.2% from 4.1% in October, in line with expectations. Wages saw a 0.4% rise, matching October’s increase and surpassing the anticipated 0.3%. Year-over-year, wages grew 4.0%, in line with October’s pace and slightly ahead of forecasts.

Summary

Overall, these reports paint a picture of a labour market that remains relatively strong but is showing signs of cooling, with slower job growth and rising unemployment. Hopefully, these trends support the case for a 0.25% rate cut at the Fed’s upcoming meeting, as the central bank works to balance economic growth with inflation control.

Consumer Sentiment Index (CSI)

The University of Michigan’s preliminary CSI for December delivered an upside surprise, climbing to 74.0. This beat analysts’ expectations of 73.0 and marked a 3.1% increase from November’s final reading of 71.8. Year over year, sentiment is up 6.2% from 69.7, reflecting steady gains.

Looking below the surface, the Current Economic Conditions Index, which gauges how consumers feel about their immediate financial situation, soared to 77.7 from November’s 63.9 – a staggering 21.6% jump. Compared to December 2023, the improvement was a more modest 6.0%. Meanwhile, the Index of Consumer Expectations, which looks forward six months, dipped 6.9% from last month to 71.6. Still, it outpaced last year’s 67.4, suggesting cautious optimism for the road ahead despite some lingering concerns.