During the May 31 Weekly Update post, I mentioned my preference for direct ownership of stock in a company rather than indirect ownership through Depositary Receipts. When I got back into investing in 2016, I was not familiar with depository receipts. My guess is that if you are new to investing you are not familiar with them. So, let’s take a closer look at them.

What are Depositary Receipts?

Depository receipts (DRs) are a popular way for investors to gain exposure to foreign companies without dealing with the complexities of international markets. These financial instruments represent shares in a foreign company and trade on domestic stock exchanges, making them accessible to domestic investors.

Here’s how they work: A depository bank purchases shares of a foreign company and holds them in custody. In return, the bank issues depository receipts, which are traded on local exchanges like any other stock. This allows investors to buy shares in international companies through familiar domestic channels.

One of the key benefits of depository receipts is convenience. Investors can diversify their portfolios internationally without needing to open foreign brokerage accounts or navigate foreign regulations. Additionally, depository receipts are often denominated in the investor’s local currency, reducing the complexities of currency conversion.

However, it’s important to be aware of the potential downsides. While DRs simplify international investing, they still carry risks. These include political and economic instability in the foreign company’s home country, currency fluctuations, and potential differences in accounting and regulatory standards. Furthermore, depository banks may charge fees for their services, which can impact overall returns.

In summary, depository receipts offer a practical and accessible way for investors to gain international exposure, providing the benefits of global diversification while trading in familiar local markets. As always, it’s crucial to understand the specific risks and costs involved, and consulting with a financial advisor can help ensure that depository receipts align with your investment goals.

What types of DR are available to purchase?

There are two main types of depository receipts: American Depository Receipts (ADRs) and Global Depository Receipts (GDRs). ADRs are issued by US banks and traded on US exchanges, such as the NYSE or NASDAQ, while GDRs are typically listed on European exchanges and can be traded in multiple markets.

American Depository Receipts

ADRs are issued by banks in the United States and represent ownership in a foreign company’s shares that are traded on a US stock exchange. The first American Depositary Receipt (ADR) was created in 1927 by the predecessor of JPMorgan Chase & Co. (NYSE: JPM), Guaranty Trust. This innovation allowed American investors to buy shares of a British retailer, Selfridges, on the New York Curb Exchange (an earlier version of the American Stock Exchange), opening up easier access to foreign companies for American investors.

The concept of Global Depositary Receipts (GDRs) emerged as a broader term encompassing depositary receipts used globally, following the success of ADRs. While a specific date for the first GDR is not available, it was after 1927 and likely coincided with the rise of depositary receipts in other financial centers around the world.

GDRs are issued by banks outside the United States and represent ownership in a foreign company’s shares that are traded on a stock exchange outside the US.

Examples of global depositary receipts (GDRs):

Tata Motors Limited (NYSE: TTM): A prominent Indian multinational automotive manufacturing company.

Petrobras (NYSE: PBR) is a Brazilian multinational corporation in the petroleum industry

When an investor buys a DR, they are effectively purchasing a certificate that represents a certain number of shares in the foreign company. The bank or financial institution that issues the DR holds the actual shares in custody and pays any dividends or other payments to the DR holders. DRs are typically denominated in US dollars or Euros, making it easier for investors to track their investments and receive payments without worrying about currency exchange rates.

While ADRs and GDRs sound the same, there are some key differences:

Geography: ADRs are issued in the United States, while GDRs are issued outside of the United States. ADRs represent ownership of foreign company shares that are held in US banks, while GDRs represent ownership of foreign company shares that are held in banks outside the United States.

Regulation: ADRs are regulated by the US Securities and Exchange Commission (SEC), while GDRs are typically regulated by the financial regulators in the country where they are issued.

Denomination: ADRs are denominated in US dollars, while GDRs are denominated in a variety of currencies, such as Euros or British pounds.

Trading: ADRs are listed on US stock exchanges, while GDRs are typically listed on foreign stock exchanges.

Liquidity: ADRs generally offer more liquidity due to their listing on US exchanges and compliance with US market regulations.

Cost: ADRs tend to be less expensive than GDRs due to their larger market size and greater liquidity.

It is worth noting that not all foreign companies have ADRs or GDRs, and even those that do may not have them available on all stock exchanges. Additionally, ADRs and GDRs may not necessarily trade at the same price as the underlying shares in the foreign company, influenced by factors such as currency fluctuations and demand for the DRs themselves.

Not all ADRs are created equal

There are different types of ADRs, such as sponsored and unsponsored. In a nutshell, a sponsored ADR is created with the foreign company’s involvement and a single depositary bank to issue the ADRs, subject to stricter regulations and disclosure, can be listed on major US exchanges. On the other hand, an unsponsored ADR is issued without the foreign company’s involvement, is subject to less stringent regulations, and typically traded on the Over-the-Counter Market (OTCM). Sponsored ADRs are typically more liquid and have lower trading costs than unsponsored ADRs.

How to identify an ADR

While some ADRs are not obvious, such as Toyota Motor Corporation, a Japanese company, which is traded as an American ADR on the New York Stock Exchange (NYSE). This makes it easier for Canadian and American investors to purchase shares without having to deal with foreign stock exchanges.

Other ADRs are easier to spot due to a ‘Y’ or an ‘F’ at the end of a ticker. For instance, China’s BYD Company Limited, a manufacturer of automobiles and rechargeable batteries, trades on the OTCM under the tickers OTCM: BYDDY and OTCM: BYDDF.

BYDDY: This represents the ADRs that trade on the OTCM. Each BYDDY ADR typically represents 10 underlying BYD shares.

BYDDF: This also trades on the OTC market, but each ADR represents 1 underlying share of BYD.

Both BYDDY and BYDDF allow North American investors to invest in the BYD Company without having to directly invest in the Chinese market.

What does the letter ‘Y’ or ‘F’ at the end of the ticker indicate?

When comparing ADRs (tickers ending with ‘Y’) and foreign ordinary shares trading on the OTCM (tickers ending with ‘F’), it’s important to consider several factors that affect the risk level of each. The letters ‘Y’ and ‘F’ at the end of a ticker symbol reveal crucial information about the type of security and its listing:

‘Y’ at the end of the ticker (e.g., BYDDY):

Indicates that the security is an American Depositary Receipt (ADR).

ADRs simplify international investing by allowing trades in US dollars, avoiding the complexities of direct international trading and currency conversion.

Generally, have higher liquidity since they are traded on major US exchanges. Higher liquidity means it is easier to buy and sell shares without significantly affecting the price.

Companies issuing ADRs typically provide more comprehensive financial information and disclosures in English, making it easier for North American investors to access and understand relevant information.

These securities are subject to stringent regulatory oversight from US exchanges (e.g., NYSE, NASDAQ) and the Securities and Exchange Commission (SEC), ensuring transparency and reduced fraud risk.

Are more widely recognized and accessible to Canadian and American investors, which can contribute to a perception of lower risk.

‘F’ at the end of the ticker (e.g., BYDDF):

Indicates that the security is a Foreign Ordinary Share, traded on the OTCM.

Tend to have lower liquidity because they are not traded on major exchanges. Lower liquidity can lead to larger bid-ask spreads and more price volatility.

Information may be less readily available, and what is available might not be as thorough or in English, making it harder for investors to make informed decisions.

Unlike ADRs, Foreign Ordinary Shares are not registered with the SEC. They trade on the OTCM, which generally has less regulatory oversight compared to major US exchanges.

Generally less accessible and less well-known, which can contribute to a perception of higher risk

In summary:

BYDDY is an ADR of BYD Company Ltd, allowing Canadian and American investors to trade it on US exchanges.

BYDDF represents the foreign ordinary shares of BYD Company Ltd, trading on the OTCM.

While both types of securities involve risks associated with investing in foreign companies, OTCM foreign ordinary shares (tickers ending with ‘F’) are generally considered riskier than ADRs (tickers ending with ‘Y’) due to lower regulatory oversight, lower liquidity, less information availability, and less market accessibility.

Canadian DRs

Let’s get more specific and explore a type of DR specifically designed for Canadian investors: The Canadian Depositary Receipt (CDR). While ADRs and GDRs have long been familiar, CDRs represent a newer option for investors. Managed by the Canadian Imperial Bank of Commerce (TSE: CM) and exclusively traded on the Cboe Canada Exchange (formerly Neo Exchange, now part of Cboe Global Markets since 2022), CDRs open up access to international companies listed on major US exchanges like the NYSE and Nasdaq for Canadian investors. You can trade CDRs through brokerage accounts that provide access to the Cboe Canada Exchange platform. Introduced in the summer of 2021, CDRs provide Canadian investors with a straightforward path to international investments, minus the complexities of currency conversions. Here’s how they work:

Investing in Global Companies: CDRs mirror shares of foreign companies typically listed on major US exchanges such as the NYSE or Nasdaq. By purchasing CDRs, investors gain exposure to foreign companies while trading in Canadian dollars on a Canadian exchange.

Convenience of trading in Canadian dollars: A major perk of CDRs is the ability to trade them in Canadian dollars. This eliminates the need for currency conversions, saving on foreign exchange fees and simplifying the investment process.

Built-in Currency Hedge: CDRs come with a built-in currency hedge, minimizing the impact of fluctuations between the Canadian dollar and the foreign currency (often US Dollars). This safeguard helps shield investments from currency volatility.

Fractional Shares: CDRs often represent fractions of a share of the foreign company, making it easier and more affordable for Canadian investors to buy into large-cap companies.

Trading Like Regular Stocks: CDRs are traded on Canadian exchanges just like conventional stocks and ETFs. They can be bought and sold through standard investment platforms.

Examples of CDRs include well-known companies like Apple (NEO: AAPL.NE), Nvidia, Berkshire Hathaway (NEO: BRK.NE), Walmart (NEO: WMT.NE), and Coca-Cola (NE: KO.NE). If you click on any of these links to the CDRs you will notice the CDR is much less than a share of the actual company. For example, compare the price of the Apple CDR with Apple stock (NASD: AAPL). You will see a significant difference. For an up-to-date list of available CDRs on Cboe Canada, consult their platform.

As with any investment, consider potential downsides to CDRs such as lower trading volumes leading to increased volatility, management fees impacting returns, and limited access to shareholder benefits like dividends and voting rights. Additionally, dividends paid to CDR holders may be subject to withholding tax, affecting net returns.

For Canadian investors seeking exposure to leading global companies while managing currency risks and transaction costs, CDRs offer a convenient and cost-effective avenue. Unlike buying shares on a US exchange, CDRs provide favorable currency conversion rates, trade at fractions of their US-listed counterparts, and minimizes the impact of currency fluctuations.

If you are interested in CDRs, check with your online broker or a financial planner to see if they are right for you.

Since I have been doing this investing blog, I have often read of various central banks’ target of a 2% rate of inflation. This is the figure that the Bank of Canada, the US Federal Reserve, European Central Bank, and other central banks often site. It got me to wondering why 2%? Was it arbitrary or was there some logical rationale? So, I decided to investigate it.

The 2% inflation target became widely adopted by central banks in the 1990s and early 2000s for several reasons:

Stable Prices: Aiming for a 2% inflation rate helps keep prices rising moderately. This stability is crucial because it allows businesses and consumers to plan for the future without worrying about sudden price increases (inflation) or decreases (deflation).

Economic Predictability: When inflation is around 2%, it signals a healthy economy where businesses can invest and grow, and consumers can confidently spend. This predictability reduces uncertainty, which is beneficial for long-term investment planning.

Impact on Interest Rates: Central banks such as the Bank of Canada and the US Federal Reserve adjust interest rates based on inflation. If inflation is too low (close to or below 0%), it can lead to deflation, where prices fall, and economic activity slows down. To prevent this, central banks might lower interest rates to encourage borrowing and spending. On the other hand, if inflation is too high, they might raise interest rates to cool down the economy and prevent excessive price increases.

Investment Strategy: Knowing that central banks target 2% inflation can help investors make informed decisions. For example, during periods of low inflation, interest rates might be lower, making borrowing cheaper and potentially encouraging investment in assets like stocks and real estate. During high inflation, investors might look for assets that historically perform well during inflationary periods, such as commodities or inflation-protected bonds.

Global Consensus: The fact that major central banks worldwide aim for a 2% inflation target creates a framework that investors can rely on. It fosters stability in financial markets and encourages global economic cooperation, which can impact international investments and trade.

Understanding why central banks target 2% inflation can really help you see how economic policies shape market conditions and investment opportunities. It highlights why keeping an eye on inflation trends and central bank actions is key to a solid investment strategy. That is why these ‘Weekly Update’ posts kick off with Canadian and US economic conditions – even if they seem a bit dry 😊 – to give you insight into what central banks watch as they work to maintain that 2% inflation target.

Since we are talking about economic news, let’s see what happened this past week….

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, How do I get started investing in publicly traded companies? …

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

BoC Monetary Policy meeting minutes

With inflation remaining a top concern, the Bank of Canada’s Governing Council met on June 5th to decide the fate of Canada’s interest rate. The minutes revealed that after four consecutive months of easing core inflation (a measure of inflation that excludes food and energy prices), the Bank opted for a rate cut. April’s data showed headline inflation at 2.7%, staying below the upper end of the Bank’s target range for the fourth month.

The global economy also factored into the decision. While overall growth was healthy at nearly 3%, a slowing American economy was balanced by increased growth in Europe and China. Inflation concerns remain globally, with core inflation measures rising in both the US and the Euro zone despite expectations of a gradual decrease. Back in Canada, the economy grew at a solid pace of 1.7% in the first quarter of 2024, but employment indicators showed easing pressures. Annual wage growth, however, remained around 4%, a potential future risk for inflation but also a sign of a healthy economy.

The higher interest rates appear to have dampened inflation, with both the overall and core inflation rates dipping in April. The Bank is aware of the potential for future inflation spikes due to factors like wage growth, but also recognizes the benefits of a strong labour market.

Overall, the Bank of Canada remains cautious, emphasizing a data-driven approach to future rate decisions. Officials agreed that any further rate cuts would be gradual and based on incoming data, with the next announcement scheduled for July 24th.

Canadian market volatility

Canada’s Volatility Index, the VIXC, tracked by the TSX 60, jumped 18% this week, rising from 9.56 to 11.31. This is a noteworthy increase, but despite the VIXC’s rise, the markets remain relatively stable overall, likely due to the lack of major economic news this past week. Investors are still hoping for another BoC rate cut in July and a potential follow-up by the US Federal Reserve in September.

The VIXC reflects anticipated market volatility, with lower values indicating less uncertainty and a calmer investor mood.

Retail Sales

Statistics Canada reported that in April, retail sales in Canada increased 0.7%, bouncing back from a 0.2% decline in March. This marks the largest increase since September 2023. Here are some of the highlights:

Sector Highlights:

Gasoline Stations and Fuel Vendors had the biggest gain with a 4.5% increase, primarily driven by higher fuel prices.

Motor Vehicle and Parts Dealers faced the biggest drop, down by 2.2%.

Yearly Performance:

Retail sales climbed by 1.8% compared to last year.

Health and Personal Care Retailers led all sectors with a 6.2% rise.

Sporting Goods, Hobby, Musical Instrument, Book, and Miscellaneous Retailers experienced the steepest decline, down by 3.7%.

Core Retail Sales: Excluding gasoline stations, fuel vendors, motor vehicle, and parts dealers:

Monthly Growth was up by 1.4%.

Annual Growth Increased by 1.5%.

Food and Beverage Retailers (which accounts for 19% of total retail sales) was up by 1.9%.

Building Material and Garden Equipment and Supplies Dealers recorded the biggest monthly drop, down by 1.4%.

The report highlights ongoing cautious consumer spending, influenced by rising inflation and higher interest rates, reducing disposable income. Until these economic pressures ease, consumer spending is expected to remain cautious.

Preliminary data for May indicates a potential 0.6% drop in retail sales, which, if confirmed, would be the steepest decline since January. This could offset much of April’s gains.

In summary, while April brought a welcome boost in retail sales, the outlook remains uncertain as consumers navigate inflation and higher interest rates.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

American market volatility

he CBOE Volatility Index (VIX), known as the market’s fear gauge, ticked up to 13.20 from last week’s 12.66. This rise likely reflects recent economic data showing a slowdown in consumer spending and a cooling economy. Despite the increase, the VIX remains below the 20 threshold, which generally indicates market calmness. This suggests that investors are still relatively relaxed about near-term market conditions.

Retail Sales

The Commerce Department’s May retail sales report showed that retail sales grew by a lower-than-expected 0.1% in May, following a revised decline of 0.2% in April. Analysts had anticipated a growth rate of 0.2%. Annually, retail sales rose at a pace of 2.3%.

The biggest monthly increase was recorded in ‘Sporting goods, hobby, musical instrument, & bookstores,’ which were up 2.8%, while the largest decline occurred in ‘Gasoline stations,’ which fell by 2.2%. Annually, the most significant increase was in ‘Miscellaneous store retailers,’ up 7.3%, whereas ‘Furniture & home furnishing stores’ experienced the biggest drop, down 6.8%.

Excluding ‘motor vehicle & parts dealers’ and ‘gasoline stations,’ retail sales still grew by 0.1% in May, meeting expectations. On a year-over-year basis, core retail sales grew by 2.6%.

This latest report indicates that consumer spending has slowed as persistent inflation and high interest rates continue to affect consumer behavior. This week’s report is yet another sign of a decelerating economy. Analysts and, more importantly, the Fed, will be watching future retail sales reports to see if this slowdown persists. For those hoping for a cut to interest rates, this slowdown is a positive indicator. 😊

How do I get started investing in publicly traded companies?

After reading in last week’s Weekly Update that now is the best time to start investing, you are ready to start. Great! You have made the decision to start investing to meet your financial goals. Now you are wondering, “How do I get started?” Well, let us see if we can help you navigate the process.

First, ensure you have the basics covered: set aside an emergency fund, pay off high-interest debt, create an investment plan, and consult with a certified financial planner to ensure everything is in order. Once these steps are completed, you are ready to dive into investing! The first step is to open an investment account, which allows you to buy and sell shares, effectively making you a part-owner of those companies. 😊 Investment accounts can hold cash and a variety of investment products, including stocks, bonds, mutual funds, and exchange-traded funds (ETFs). This gives you the flexibility to choose investments that align with your risk tolerance and financial goals.

Step 1: Open an Investment Account Consider using a no-cost trading app like TD Easy Trade or Wealthsimple. For Canadians, you will receive both a Cash account and a Tax-Free Savings Account (TFSA), each with Canadian and US dollar subaccounts. TFSAs are a great way to grow your wealth tax free because any interest, dividends, or capital gains earned in a TFSA are not subject to Canadian income tax. Additionally, withdrawals from a TFSA are not taxed, offering flexibility as you can access your funds without worrying about additional tax implications. Remember, there is an annual contribution limit for TFSAs, so check with a financial advisor or the Canada Revenue Agency (CRA).

Step 2: Choose Your Platform Back in the early 90s, investing meant calling a stockbroker, buying shares in lots of 100, and paying a $50 transaction fee. Today, online trading is much more accessible. Fees are minimal, if not free, and you can buy as little as one share, or a fraction of a share in some cases. All you need is either a computer with secure, fast internet access or a smartphone with an appropriate app. Here are some well-known online brokers:

Big 5 Canadian Banks: RBC Direct Investing, Scotia i-Trade, TD Direct Investing, BMO InvestorLine, CIBC Investors Edge

Many banks require a minimum balance to avoid maintenance fees, but these fees are often waived if you or your household have a substantial financial relationship with the bank (e.g., mortgage, savings account, etc.). Using your financial institution for your trading account simplifies money transfers and usually they offer comprehensive financial planning services to assist with overall wealth management. In addition to cash, and TFSA accounts, many financial institutions can also provide tax sheltered Registered Retirement Savings Plan (RRSP) or Registered Income Fund (RIF) accounts in both Canadian and US currencies. Additionally, you can buy and sell on major Canadian and US exchanges, as well as secondary exchanges like the Canadian Securities Exchange (CSE) and the Over-the-Counter Market (OTCM) in the US. If you are opening your first direct trading account, consider starting with your financial institution for these conveniences.

Step 3: Determine Your Needs If you do not meet the bank’s fee waiver criteria, explore other trading platforms. Consider what is important to you:

Research capabilities to look for investments or perform your own due diligence on companies

Low transaction fees

Access to all North American stock markets and stocks

Educational resources to help you understand this investing thing

Customer support and the ability to easily talk to someone if you have any questions

Assess your investing knowledge, experience, and desired features, then choose the platform that fits you best.

Happy investing! Remember, the key is to understand what you are investing in and make decisions that align with your financial goals and ability to take on risk.

Weekly Market Review

Monday: it was a tale of two countries as far as the indexes go. Canada’ Toronto Stock Exchange Composite Index (TSX) ended lower, while the S&P 500 Index (S&P), the Nasdaq Composite Index (Nasdaq) and the Dow Jones Industrial Average (DJIA) ended higher. Oil prices rose on the prospects of increased demand during the summer.

In Canada, the TSX fell to a three-month low as investors rotate away from resource-oriented stocks in favour of high-flying technology companies. In trading, Industrials, Consumer Cyclicals and Consumer Staples were the only Canadian sectors to advance, while Technology and Utilities suffered the biggest declines.

In the US, the rally in artificial intelligence (AI) companies propelled the Nasdaq to its sixth consecutive record high, and the S&P reached a record high for the 30th time this year. In trading, Consumer Cyclicals and Technology were the big gainers, while Utilities and Healthcare dropped the most.

Tuesday: it was a good day in the markets, with all four indexes ending in the green. Weaker US retail sales has investors hoping this opens the door for the Fed to lower interest rates sooner rather than late. Oil prices rose on supply concerns due to rising tensions in the Middle East region.

In Canada, higher oil and commodity prices pushed the TSX into positive territory. In trading, Basic Materials (miners and fertilizer manufacturers) and Energy posted the biggest sectoral gains, while Technology and Telecommunications were the biggest losers in the Canadian sectors.

In the US, technology companies associated with AI continue to extend the current bull run, sending the Nasdaq to its seventh straight record close, and the S&P to its 31st record high close of 2024. A surge in share price by Nvidia (NASD: NVDA) has pushed Nvidia into the number 1 spot as the world’s most valuable company, as measured by market capitalization (number of shares outstanding X share price). In trading, Energy and Financials were the top performers, while Consumer Cyclicals and healthcare were the only two sectors to end lower.

Wednesday: the TSX was dragged lower by seasonally weak commodity prices, while the US stock markets were closed for the American national holiday Juneteenth. The price of oil moved higher, however, all ten Canadian sectors lost ground today. The steepest declines were in the Healthcare and Industrials sectors, while Basic Materials and Utilities declined the least.

Thursday: a mixed day for the indexes with the TSX and DJIA advancing. Despite hitting record highs during today’s session, the Nasdaq and S&P ended lower when investors took some money off the table after the recent rally in AI stocks. Oil prices continued to climb as investors anticipate lower interest rates in time for the busy summer travel season.

In Canada, higher commodity prices lifted the TSX off an almost four month low. In trading, buoyed by higher commodity prices, Basic Materials was the best performing sector, while Utilities performed the worst.

In the US, the Nasdaq’s streak of record high closings ended at seven when the Nvidia rally stalled and then the share price fell 3%. In trading, Energy posted the biggest gain while Technology had the biggest drop.

Friday: the markets fluctuated throughout the day as the AI-fueled rally lost momentum. Consequently, the DJIA was the only index to end in positive territory, with investors seemingly booking profits after the AI surge. Oil prices retreated on concerns of lower-than-expected demand.

In Canada, lower commodity prices caused by oversupply and lower demand weighed on the TSX. In trading, The Technology sector gained the most while Basic Materials suffered the biggest drop.

In the US, Nvidia stock pulled back another 3%, dragging the Nasdaq and S&P into the red. In trading, Consumer Cyclicals advanced the most, while Energy fell the furthest.

Weekly Market and Portfolio Review

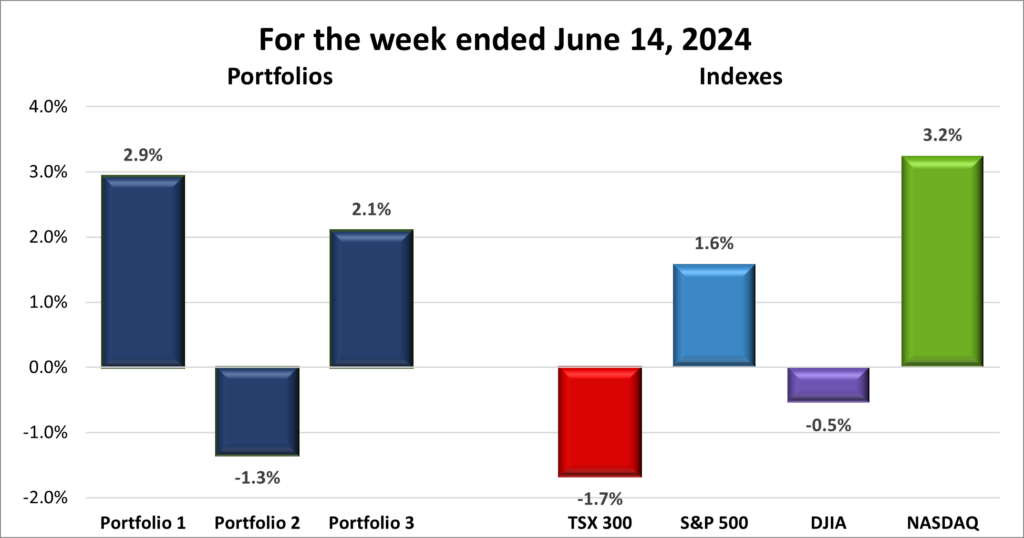

For the week, the TSX (SPTSX) fell 0.4%, the S&P 500 (SPX) grew 0.6%, the DJIA (INDU) rose 1.5% and the Nasdaq (CCMP) was essentially flat, adding 0.003%.

Index

Weekly Streak

TSX:

5 – week losing streak

S&P:

3 – week winning streak

DJIA:

1 – week winning streak

Nasdaq:

3 – week winning streak

The past week saw mixed results for the four major North American indexes. While the American indexes recorded modest gains, the TSX ended lower. The American trading week was interrupted by the Juneteenth national holiday, which fell in the middle of the week.

Nvidia and the AI-fueled rally were the main drivers for the American markets, initially lifting the S&P and Nasdaq to record highs. However, after the midweek holiday, the rally lost steam, causing the S&P and Nasdaq to give back some of their earlier gains. The DJIA didn’t get the same boost from the AI rally, but managed to maintain its upward momentum since technology companies make up a smaller portion (20%) of this index and have less influence overall. Despite the technology sector’s wobble, the three US indexes managed to eke out modest gains for the week.

In Canada, the resource-driven TSX was influenced by fluctuating commodity prices, which ultimately saw the TSX trend downward throughout the week, as you can see in the chart above.

Overall, the week started strong but lost momentum towards the end, with three of the indexes heading downward. This week reminds us that markets can be unpredictable, even after strong starts. This is not a great sign for next week, but there is plenty of economic news on the horizon. Let us hope the latest inflation and productivity reports from Canada and the US bring positive news for consumers and investors alike. 😊

Portfolio

Weekly Streak

Portfolio 1:

1 – week losing streak

Portfolio 2:

2 – week losing streak

Portfolio 3:

1 – week losing streak

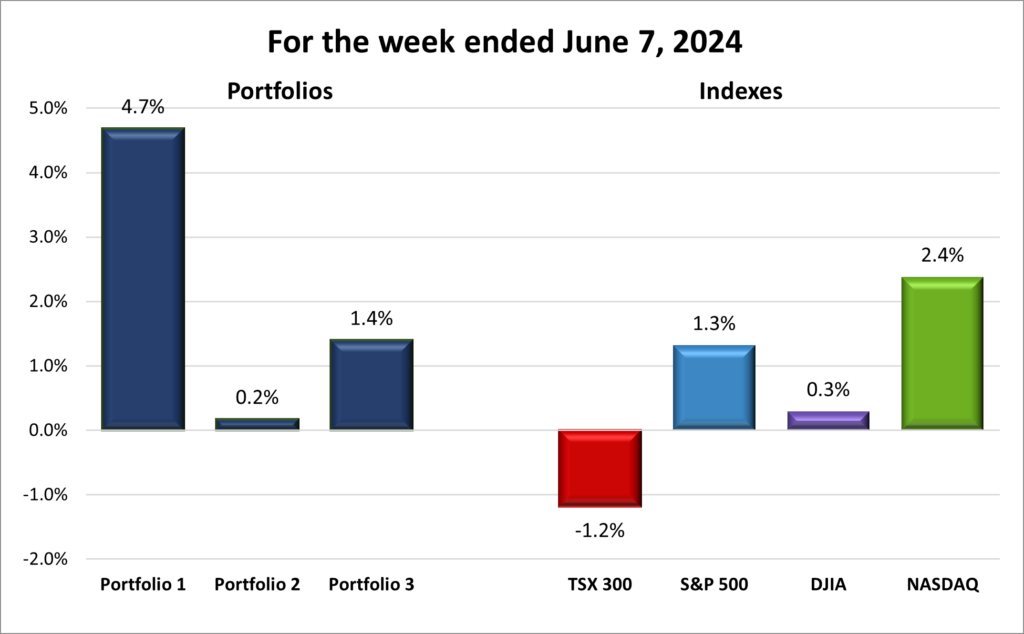

It’s not often that a good week for the indexes translates to a tough week for portfolios, but that’s exactly what happened this past week. All three portfolios experienced losses greater than the worst-performing index, as illustrated in the chart below.

Portfolio 1 had the toughest week among the three. Despite over half the companies in this portfolio recording gains, the overall value still dropped. This was largely due to Nvidia, the portfolio’s largest holding at 38%, falling by 6%. Additionally, significant losses from Nano-X Imaging Ltd (NASD: NNOX) and indie Semiconductor Inc. (NASD: INDI), both down 11%, added to the portfolio’s woes.

Portfolio 2 saw a majority (56%) of its companies posting weekly gains, with no significant individual gains or losses. Microsoft (NASD: MSFT) and MongoDB (NASD: MDB), the second and third largest holdings, both recorded weekly gains. However, the largest holding, the Bank of Nova Scotia (TSE: BNS), registered a loss. Despite these mixed results, the portfolio fell for a second straight week.

Portfolio 3’s decline was straightforward: more than 66% of its companies posted weekly losses. When that many companies in a portfolio decline, it’s tough to achieve a weekly gain. The situation was exacerbated by Unity Software (NYSE: U) and Lithium Americas (Argentina) (TSE: LAAC), both hitting 52-week lows.

Overall, it was a challenging week for all three portfolios. No one said investing was always sunshine and rainbows. 😊 With fingers crossed, let us hope for a significantly better performance next week.

Weekly Portfolio & Index performance for the week ended June 21, 2024.

Companies on the Radar

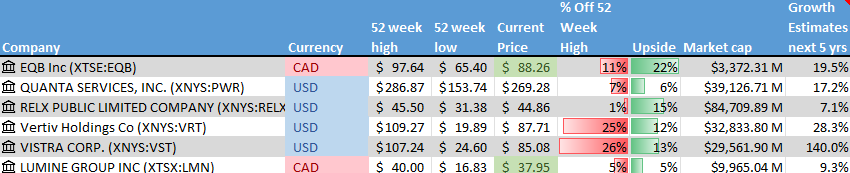

No new companies caught my eye this past week, but I did manage to shorten my watchlist by removing RELX PLC (NYSE: RELX). With a growth estimate of 7.1% over the next five years, RELX seemed the least promising compared to the other five companies on my list, which all appeared to have better upside potential. So, I decided to drop it from consideration.

The radar list now comprises these five companies listed below.

Equitable Bank (TSE: EQB), a mid sized Canadian bank, considered Canada’s 7th bank, that provides financial services to consumers and businesses.

Quanta Services, Ltd. (NYSE: PWR), a large-cap American company offering a wide range of specialty infrastructure solutions throughout the world

Vertiv Holdings (NYSE: VRT), an American company that designs and builds infrastructure and continuity solutions to businesses around the world.

Vistra Corp (NYSE: VST), an American company operating in the integrated retail electricity and power generation sector.

Lumine Group (TSE: LMN), a young Canadian mid sized company that acquires communications and media software companies, and then strengthens and grows those companies.

Please keep in mind that these are only companies that have piqued my interest. This is not a recommendation or financial advice. You should do your own research or contact a professional before making any investment decisions.

The Radar Check was last updated June 21, 2024.

Stock on the Radar List. 1 of 2.Stock on the Radar List. 2 of 2.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended June 21, 2024: DOWN

Apple (NASD: AAPL) announced they were shutting down their ‘Buy now, pay later’ (BNPL) service in the US as the company transitions to a successor program that uses third party BNPL companies. Existing users of Apple’s BNPL service will still be able to manage and pay outstanding loans via Apple’s Wallet app.

The Trade Desk (NASD: TTD) announced they had expanded their partnership with Fox Corporation (NASD: FOX) to help advertisers reach their target audiences and measure the success of those campaigns.

Amazon (NASD: AMZN) plans to overhaul its Alexa voice assistant service into two levels with a monthly fee to utilize the higher AI integrated tier.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Portfolio 2 for the week ended June 21, 2024: DOWN

Alimentation Couche-Tard (TSE: ATD) subsidiary Circle K has been quietly selling stores that do not fit their business model. Despite actively purchasing convenience stores, they recently sold 110 stores across Canada and the US and are currently in the process of unloading 68 more stores.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

iA Financial Corporation Inc. (TSE: IAG)

Dream Industrial Real Estate Investment Trust (TSE: DIR.UN) DRIP

Supremex Inc. (TSE: SXP)

iA Financial Corporation Inc (TSE: IAG)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended June 21, 2024: DOWN

TD Bank (TSE: TD) has started a new business unit, called TD Innovations Partners, focused on providing banking and financial services to Canadian technology companies. The new unit will provide a full suite of services, from setting up bank accounts for new startups through to connecting companies to potential investors, board members, customers, and vendors.

Magnite (NASD: MGNI) announced their SpringServe ad serving technology is being used by Japan’s Yomiuri Telecasting Corporation to provide video advertising for their on-demand services.

GDI Integrated Facility Services (TSE: GDI) announced their Chief Financial Officer will retire in September, however he will serve as an advisor for the following twelve months. Charles-Etienne Girouard was promoted to senior vice president of finance operations, effective immediately. Mr. Girouard has been with GDI for the past six years.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

SmartCentres Real Estate Investment Trust (TSE: SRU.UN) DRIP

Over the last few weeks, I have been writing about common questions people ask when they first start investing. From ‘What is Investing?’ to today’s topic of ‘When should I start investing?’ with a few more questions to come in the next few weeks. While answering these questions, it occurred to me: before people even start asking questions (which is a good place to start), what else is preventing people from starting to invest? Here are a few common barriers that I’ve either encountered myself or heard other people cite:

Lack of knowledge: Many people feel they do not have enough knowledge about the financial markets or investing strategies, making them hesitant to start.

Limited financial resources: Investing often requires some initial capital, which can be a barrier for those with limited savings.

Risk Aversion: Fear of losing money often holds people back from investing, as the potential for financial loss can seem overwhelming.

Investment complexity: The vast array of investment options and complex financial jargon can be intimidating for new investors.

Time constraints: Investing requires research and ongoing monitoring, which can be challenging for busy individuals.

Debt: Debt payments can limit available funds for investing and create financial pressure.

Life events: Major life events like starting a family or buying a home can impact your financial situation and risk tolerance, potentially affecting investment decisions.

Inertia: Even with knowledge and resources, you need to avoid procrastination and take the first step.

Do any of them look familiar to you? I have faced them all at one time or another. The first step to overcoming these barriers is to acknowledge them, then make a plan to address them head-on.

Do not be discouraged by the initial complexity. Do not overthink it, avoid paralysis by analysis. It becomes easier once you overcome the initial inertia and get started. Open a free trading account and deposit a bit of cash. There, you have made your first investment. 😊 Keep adding money to your investing account while you learn and decide what to invest in. When you find an investment that fits your plan and risk tolerance, you will have already put some money aside.

I hope these weekly updates help you with some of the questions you may have and will provide you with some knowledge and confidence to take control of your financial future. With that said, let’s see what happened this past week….

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, When should I start investing?, What I learned this week?, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Canadian market volatility

Canada’s Volatility Index (VIXC), tracked by the TSX 60, dipped to 9.56 over the past week, down from 9.73. This slight decline occurred amid a generally stable market environment but was influenced by a few factors. Speculation about potential rate cuts by the BoC in July and the US Federal Reserve’s decision to maintain US interest rates at 5.5% likely played roles in this movement.

The VIXC, often dubbed Canada’s ‘fear gauge,’ offers insights into expected market volatility. When the VIXC trends lower, it suggests reduced uncertainty and a calmer market sentiment among investors.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Federal Open Market Committee monetary policy meeting

The Federal Open Market Committee (FOMC), which is responsible for setting the benchmark interest rate, decided to hold the benchmark interest rate steady at their current range of 5.25% – 5.5%. While investors were hoping for a September rate cut, the FOMC hinted at a delay until December. They also revised their forecast from three cuts to just one in 2024. Looking ahead, they project four rate cuts in 2025, maintaining a policy of “higher for longer” interest rates as inflation continues to cool. (For those unfamiliar, “higher for longer” refers to keeping rates elevated for a sustained period to combat inflation.)

Although inflation has moderated, it remains above the Fed’s 2% target. With a robust labour market and strong economy, the FOMC plans to keep rates steady until clear evidence of sustained inflation reduction, such as significant price declines or increased unemployment, emerges. Fed Chair Jerome Powell described the decision to hold rates as a close call, reflecting the Fed’s willingness to accept a gradual decline toward the 2% target amidst ongoing economic strength.

Recent data on both headline (all items) and core CPI indicates a slowdown in inflation on a monthly and annual basis, aligning with the Fed’s objectives. Further reports showing continued inflation slowdown could pave the way for anticipated rate cuts. And lower rates would be welcomed by consumers and businesses in the US, Canada, and globally.

Consumer price Index (CPI)

As expected, the May CPI was unchanged (0.0%), down from a 0.3% gain in April. Year over year, the CPI slowed to 3.3%, slightly below April’s 3.4% growth. The biggest monthly increase was in ‘Tobacco and smoking products,’ which rose by 1.6%, while the largest decline was in ‘Energy commodities,’ including fuel and oil products, which dropped by 3.5%. Annually, ‘Transportation services’ saw the most significant increase, up 10.5% due to higher fuel costs. This rise in ‘Transportation services’ was partly driven by a 3.6% year-over-year increase in fuel prices, despite some cooling in recent months. Meanwhile, ‘Used cars and trucks’ experienced the biggest annual decline, falling by 9.3%.

Core CPI, which excludes the volatile food and energy components, grew 0.2% in May, slightly below April’s 0.3% increase. On an annual basis, core CPI slowed to 3.4% in May from 3.6% in April, marking the slowest pace in three years. Analysts had predicted an increase of 3.5%.

The May CPI report was a sign the Fed had been waiting for: both the pace of headline (all items) and core inflation were slowing down, both monthly and year over year. While the Fed was likely pleased to see inflation cooling, they still considered it too high to start lowering the benchmark rate. However, this report was a step in the right direction. If future reports indicate that inflation continues to move towards the Fed’s 2% target, we could see a rate cut as early as September, with the possibility of a second cut later in the year.

American market volatility

The CBOE Volatility Index (VIX), often referred to as the market’s fear gauge, edged up to 12.66 from the previous week’s 12.22. This slight increase likely stems from the Fed’s decision to maintain the current interest rate of 5.5%, reduce the anticipated rate cuts from three to one, and delay a potential rate cut towards the end of the year. With the VIX remaining below the 20 threshold, which typically indicates market calmness, investors appear to be less apprehensive in the near term.

Consumer Sentiment Index (CSI)

The University of Michigan’s preliminary reading on the overall index of consumer sentiment, a gauge of consumer confidence, fell to 65.6 in June, marking a 5.1% drop from 69.1 in May. This was the third consecutive monthly decrease and the lowest reading in seven months. Analysts had predicted a higher reading of 72. Despite the monthly decline, the CSI was up 2.2% year-over-year.

The lower reading likely reflects consumer concerns about persistent inflation, which is causing interest rates to remain higher for longer, and slowing wage growth.

When should I start investing?

If you are not already investing your money, the best time to start is now! However, before diving in, make sure you have a stable financial foundation. This means having an emergency fund, being free of high-interest debt, and understanding your financial goals and risk tolerance. Once you are financially stable, the best time to start investing is as early as possible. Now, let us take a look at why starting early is so crucial:

Compound Interest: The earlier you start, the more time your investments have to grow. Compound interest can significantly boost your wealth over time, as you earn returns on your returns.

Learning Curve: Investing is a skill that improves with experience. Starting early allows you to learn from mistakes and successes, refine your strategies, and build confidence.

Risk Tolerance: Younger investors typically have a higher risk tolerance because they have more time to recover from potential losses. This allows for more aggressive investment strategies that can lead to higher returns.

Financial Goals: Early investing helps you work towards long-term financial goals, such as retirement, buying a home, or funding education.

Habit Formation: Starting early helps you develop good financial habits, such as regular saving and investing, budgeting, and financial planning.

To illustrate the power of early investing, consider the following example:

Marie starts investing at age 20, investing $2,400 annually at the beginning of each year. Life starts to ‘happen’ at 30, so she stops contributing at age 30. Meanwhile, John starts to ‘enjoy life’ at 20 but when he turns 40, he starts to think he should plan for his future, so he invests $4,800 at the start of every year until he reaches 65. Both assume an 8% annual growth rate (The historical average growth rate of the S&P 500 is around 10.26% but let us be conservative). Who will have the larger retirement nest egg at 65?

Marie

John

Age

Amt invested

YE Value

Age

Amt invested

YE Value

20

$ 2,400

$ 2,592

40

$ 4,800

$ 5,184

21

$ 2,400

$ 5,391

41

$ 4,800

$ 10,783

22

$ 2,400

$ 8,415

42

$ 4,800

$ 16,829

23

$ 2,400

$ 11,680

43

$ 4,800

$ 23,360

24

$ 2,400

$ 15,206

44

$ 4,800

$ 30,412

25

$ 2,400

$ 19,015

45

$ 4,800

$ 38,029

26

$ 2,400

$ 23,128

46

$ 4,800

$ 46,256

27

$ 2,400

$ 27,570

47

$ 4,800

$ 55,140

28

$ 2,400

$ 32,368

48

$ 4,800

$ 64,735

29

$ 2,400

$ 37,549

49

$ 4,800

$ 75,098

30

$ 2,400

$ 43,145

50

$ 4,800

$ 86,290

Stops contributing at 30

Contributes for another 15 years

65

$ –

$ 637,915

65

$ 4,800

$ 414,484

Over 11 years, Marie invests a total of $26,400 (11 x $2,400) and ends up with a nest egg of $637,915. John, on the other hand, invests a total of $124,800 over 26 years (26 x $4,800) and accumulates $414,484. Despite investing more than twice as much, John’s nest egg is almost 54% less than Marie’s, highlighting the power of compounding.

It is pretty obvious that the earlier you jump into investing, the better. Think of it like laying the foundation for a sturdy financial future. By starting early, you give your money more time to grow and multiply. So, do not wait around—get started as soon as you can, and let your money start doing the heavy lifting for your financial goals! 😊

Cautionary note: The downside of compound interest

Just as compound interest can grow your savings, it can also work against you when paying off debt. Some credit cards compound interest daily on your balance, leading to higher interest amounts if you carry a balance month-to-month. Therefore, it is essential to pay off debt as quickly as possible.

What I learned this week

When I decided to increase my investment in Shopify, I found myself short on Canadian dollars in my TFSA Canadian dollar account, which I intended to use for purchasing shares on the Toronto Stock Exchange (TSE). To proceed, I transferred funds from my US dollar TFSA account into the Canadian dollar TFSA account. Although the transfer itself incurred no fees, I did experience a minor loss due to currency exchange between the US and Canadian dollars.However, given that Shopify is listed on both the TSE and the Nasdaq Stock Exchange, I could have alternatively purchased the Shopify shares on the Nasdaq exchange. This would have allowed me to sidestep any losses stemming from currency exchange fluctuations. While the loss was not significant, I will keep this in mind for future investments in companies listed in both Canada and the US. Every little bit helps. 😊

Something else I learned about was brand value, which refers to the financial worth attributed to a brand itself, such as Apple (NASD: AAPL). Factors contributing to brand value include:

Brand recognition and reputation: How well-known and respected the brand is.

Customer loyalty: The degree to which customers prefer a particular brand over competitors.

Perceived quality and value: How consumers perceive the quality and value of the brand’s products or services.

Brand associations: The positive attributes and associations that consumers connect with the brand.

Intellectual property: Trademarks, logos, and other brand-specific elements.

I think it would be fair to say Apple meets all five of these points. 😊

Brand valuation differs from market valuation (also known as market capitalization). Market valuation refers to the total market value of a publicly traded company’s outstanding shares of stock. It is calculated by multiplying the current share price by the total number of outstanding shares. Whereas brand value is a component of a company’s overall worth, typically listed as Intangible Assets, that captures the power and influence of the brand itself, while market valuation provides a broader picture of the company’s financial standing and investor confidence.

Weekly Market Review

Monday: the week got off to a good start with the four major North American indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – all ending higher. The price of oil joined the rally, finishing higher thanks to prospects of increased demand this summer.

In Canada, higher oil and commodity prices helped the TSX get in and stay in positive territory. In trading, Technology and Basic Materials (miners and fertilizer manufacturers) advanced the most of the Canadian sectors, while Telecommunications Services and Consumer Staples declined the most.

In the US, the S&P and Nasdaq set record highs, again, as investors prepare for Wednesday’s double whammy of the latest inflation report and an update from the Fed on interest rates. In trading, Utilities and Energy posted the biggest gains in the US sectors, while Telecommunications Services and Consumer Staples were the only sectors to end lower.

Tuesday: it was mixed day with the TSX and the DJIA ending in the red. All eyes turned towards tomorrow’s announcement from the Fed. Not so much for their interest rate decision, but more for clues they provide on when the rates might be lowered.

In Canada, the TSX slipped on shrinking commodities prices, concerns about a slowing global economy, and fears of a hawkish stance taken by the Fed regarding interest rates remaining higher for longer. In trading, Technology and Healthcare advanced the most while Utilities and Consumer Cyclicals fell the farthest.

In the US, once again the S&P and Nasdaq closed at record highs thanks in part to Apple jumping 7%. In trading, Technology and Financials were the top performers, while Telecommunications Services and Consumer Staples incurred the biggest drops.

Wednesday: another mixed bag day for the four indexes, this time the DJIA ended barely in the red. Otherwise, the indexes ended higher thanks to the May CPI report that showed inflation had slowed, and the Fed maintained their pause in interest rates. The price of oil rose on supply concerns from increasing tensions in the Middle East.

In Canada, lower US inflation and a merger of two Canadian banks – National Bank of Canada (TSE: NA) acquired Canadian Western Bank (TSE: CWB) – helped get the TSX back into positive territory. In trading, Technology and Healthcare posted the biggest gains while Consumer Cyclicals and Utilities were the only sectors to end lower.

In the USA, the S&P and Nasdaq set record closes for the third straight session on news of slowing inflation. In trading, Technology and Industrials gained the most, while Telecommunications Services and Consumer Staples lost the most.

Thursday: after a bullish day on Wednesday, the markets were mixed, with the Nasdaq and S&P closing higher while the DJIA and TSX edged lower. Investors were processing the likelihood that the Fed would postpone US rate cuts until year-end, at the same time reducing the number of cuts from three to one. Oil prices bounced around most of the day before finally falling into the red at the end of the day.

In Canada, the TSX fell to a two-month low as investors’ concerns about higher for longer interest rates south of the border weighed on the TSX. In trading, all sectors ended lower. Consumer Staples and Consumer Cyclicals dropped the least, while Energy and Basic Materials suffered the biggest losses.

In the US, the Nasdaq and S&P both set record closes for the fourth straight day as stocks of Technology companies continue to rally. In trading, technology, Consumer Staples, and Utilities were the only sectors to climb higher, while Energy and Financials slid the farthest.

Friday: the week ended on a down note as only the Nasdaq was able to finish above the flatline. The price of oil fell today but oil still had its best week since April due to forecasts of growing demand.

In Canada, the TSX fell to a three-month low as lower oil prices weighed on the TSX. In trading, Technology was the only sector to advance while Telecommunications Services and Energy suffered the biggest losses.

In the US, the Nasdaq set a record high close for the fifth straight day. Lower wholesale prices provided more evidence that inflation was slowing. In trading, Technology was the only one of the American sectors to end higher, while Energy and Industrials fell the farthest into the red.

Weekly Market and Portfolio Review

For the week, the TSX (SPTSX) slumped 1.7%, the S&P 500 (SPX) rose 1.6%, the DJIA (INDU) slid 0.5% and the Nasdaq (CCMP) jumped 3.2%.

Index

Weekly Streak

TSX:

4 – week losing streak

S&P:

2 – week winning streak

DJIA:

1 – week losing streak

Nasdaq:

2 – week winning streak

An impressive performance from the Technology sector helped counterbalance the impact of a hawkish Fed, allowing the S&P and Nasdaq to extend their weekly winning streaks, as illustrated in the chart above. Meanwhile, the DJIA lost ground, and the TSX continued its losing streak.

It was an eventful week on the economic front in the US. The May CPI report and other economic indicators showed signs of continued slowing inflation. At the FOMC meeting, Fed Chair Powell acknowledged this significant easing but emphasized that inflation remains too high. The Fed seeks more consistent data to ensure inflation is on track to hit their 2% target. As expected, the Fed stuck with its higher-for-longer rate strategy, stating they expect only one rate cut in 2024, rather than the three initially forecasted at the beginning of the year. Despite the Fed’s stance, investors seemed to believe otherwise.

The combination of positive economic data and investors’ belief that rates might drop more than once, and possibly as soon as September, seemed to ignite the S&P and Nasdaq. The S&P enjoyed a four-day streak of record closing highs, while the Nasdaq set new record highs each day of the week. However, the TSX and DJIA did not share in the tech-driven rally. The technology sector’s lighter weight in these indices meant they did not benefit as much from the surge in technology stocks.

The Fed’s news about fewer rate was also felt in the Canadian markets. As the old saying goes, ‘when the US sneezes, Canada catches a cold.’ ☹ The TSX recorded its fourth consecutive weekly decline and its biggest weekly decline since October 2023. Many are speculating that if the BoC cuts the rate in July while the Fed holds steady, the Canadian dollar is likely to weaken against the US dollar. This would make imports from the US more expensive, possibly triggering another round of high prices.

Looking forward, I will be keeping an eye for further signs of falling inflation that could lead to lower interest rates, both in Canada and the US. While it is great that the technology sector continues to outperform, it would be even better if the current rally could broaden. A broader rally implies increased investor confidence and economic strength, which in turn reduces risks and improves the sustainability of market gains. A more balanced rally benefits a larger portion of the economy and us investors alike. 😊

Portfolio

Weekly Streak

Portfolio 1:

2 – week winning streak

Portfolio 2:

1 – week losing streak

Portfolio 3:

2 – week winning streak

As illustrated in the chart below, it was a mixed week for the portfolios with two of the three increasing in value.

Portfolio 1 continues to shine, even with more than half the holdings losing ground. Despite a significant (more than 10%) drop of 14% in Celsius Holdings (NASD: CELH), the portfolio was buoyed by a stellar 15% surge in Skyworks Solutions Inc (NASD: SWKS) and strong performances from tech titans Nvidia and Apple. Talk about resilience!

Portfolio 2 hit a bit of a rough patch, extending its losing streak to two weeks. Over half the holdings took a dip, but there were no dramatic swings. The silver lining? MongoDB, which had taken a steep dive the previous week, seems to have found its footing and is inching upward, posting a slight weekly gain.

Portfolio 3 joined the winner’s circle this week. Despite more than half of its holdings slipping, there were no major price swings. Shopify, however, came through with a notable dollar value increase, pushing the portfolio into the green.

Overall, not a bad week! Sure, I would love to see all three portfolios on the rise, but as Mick Jagger wisely sings, “You can’t always get what you want.” 😊

Weekly Portfolio & Index performance for the week ended June 14, 2024.

Companies on the Radar

No new companies came across my radar this past week, leaving my list with the six companies listed below.

Equitable Bank (TSE: EQB), a mid sized Canadian bank, considered Canada’s 7th bank, that provides financial services to consumers and businesses.

Quanta Services, Ltd. (NYSE: PWR), a large-cap American company offering a wide range of specialty infrastructure solutions throughout the world

RELX PLC (NYSE: RELX), provides information-based analytics and decision tools for professional and business customers worldwide.

Vertiv Holdings (NYSE: VRT), an American company that designs and builds infrastructure and continuity solutions to businesses around the world.

Vistra Corp (NYSE: VST), an American company operating in the integrated retail electricity and power generation sector.

Lumine Group (TSE: LMN), a young Canadian mid sized company that acquires communications and media software companies, and then strengthens and grows those companies.

Please keep in mind that these are only companies that have piqued my interest. This is not a recommendation or financial advice. You should do your own research or contact a professional before making any investment decisions.

The Radar Check was last updated June 14, 2024.

Stock on the Radar List. 1 of 2.Stock on the Radar List. 2 of 2.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended June 14, 2024: UP

At Apple’s annual developer conference, the company unveiled their artificial intelligence (AI) strategy and their latest software, complete with its new integrated ‘Apple Intelligence.’ Apple also announced a deal with leading AI developer OpenAI that will allow Apple to integrate ChatGPT with their voice assistant Siri and other Apple software.

Following the recent surge in Apple’s share price, the company regained the title of world’s most valuable company. They also became the first brand to surpass the US$ 1 billion in brand value, up 15% from a year ago.

In other Apple news, the company was served a possible class action lawsuit that claims Apple underpays women performing the same or comparable jobs as men.

CrowdStrike (NASD: CRWD) has been added to the S&P 500 index list of companies. Any mutual or index fund that tracks the S&P will have to purchase an appropriate number of CrowdStrike shares, which should raise the share price.

Following, Nvidia’s (NASD: NVDA) recent 10 for 1 stock split, there is talk Nvidia could possibly replace fellow chipmaker Intel (NASD: INTC) in the DJIA. That would mean any fund that tracks the DJIA would have to purchase shares in Nvidia, which would likely give the share price a nice little bump. 😊

Amazon (NASD: AMZN) announced they have partnered with South American telecom company Vrio to beam broadband internet down over the actual Amazon. The deal will see Amazon’s Project Kuiper satellite internet business unit provide internet access across even the remotest parts of the Amazon, which spans Argentina, Brazil, Chile, Uruguay, Peru, Ecuador, and Colombia.

A federal judge has ruled that Alphabet’s (NASD: GOOGL) Google must face trial on antitrust claims by the US Department of Justice (DOJ) who claim the company illegally dominates the online advertising market.

Activity

Bought: Shopify (TSE: SHOP) This is my second investment in Shopify, but the first for this portfolio. Shopify had performed exceptionally well in Portfolio 3, so I decided to add more shares, this time in Portfolio 1. This also aligns with my strategy of re-investing in companies that have proven they can grow their business and share price.

Shopify is a major player in the e-commerce industry, providing a user-friendly platform for businesses to set up and manage their online stores. With a large and growing merchant base, Shopify benefits from a strong network effect. The more merchants that join Shopify, the more valuable the platform becomes for everyone involved. Given the expected continued growth of the e-commerce market, Shopify is well-positioned to thrive. Their recurring revenue from subscription fees offers stability and predictability to its cash flow. Moreover, Shopify is an innovative company, constantly expanding its product offerings, including payments, fulfillment services, and marketing tools.

Of course, there are some risks to consider. The e-commerce industry is highly competitive, and Shopify faces significant competition. Economic slowdowns could also impact Shopify as businesses might cut back on e-commerce spending. Additionally, the current environment of high inflation and high interest rates could pose challenges to Shopify’s business.

Despite these risks, Shopify is considered one of the best, if not the best, all-in-one e-commerce, and retail platform. They continue to innovate with new tools and are integrating AI features into their existing products. They continue to expand globally and are constantly acquiring more customers while driving down their customer acquisition costs and improving operational efficiency.

Overall, Shopify holds a strong position in a growing industry and should make a great addition to the portfolio.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSE: DIR.UN) US $

Home Depot, Inc. (NYSE: HD)

Skyworks Solutions Inc (NASD: SWKS)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended June 14, 2024: DOWN

At Microsoft’s (NASD: MSFT) Xbox Games Showcase, the company announced their all-digital Xbox console, and a host of new video games.

In other Microsoft news, the company announced they have cancelled the rollout of their new AI powered feature ‘Recall’ which tracks computer usage. ‘Recall’ allows users to search their computers browsing and web chat histories for something they did previously, even months earlier. The downside is anyone accessing the computer could also see another user’s history. The feature will be available only to those with new CoPilot+ enhanced computers and enrolled in Microsoft’s Windows Insider Program.

The company announced they plan to invest over US$ 7 billion to develop datacentres in northeastern Spain.

Canadian Natural Resources Limited (TSX: CNQ) executed a 2-for-1 split basis on Tuesday, June 11, 2024. While stock splits change the number of outstanding shares in circulation, they do not change a company’s market capitalization (outstanding shares X share price), nor underlying fundamentals.

MongoDB partnered with Bendigo and Adelaide Bank (ASX: BEN), a leading Australian bank, to update BEN’s core banking technology using MongoDB Atlas with AI as the underlying platform of the modernization. As a result of using MongoDB Atlas with AI, BEN cut the migration time by up to 90%, completing the task in three months, and doing it at 10% of the cost of a typical legacy system to cloud migration. Very impressive!

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Shopify was on quite the winning streak, reaching 13 straight days before the shares ended lower on June 13. Its previous longest winning streak was 10 days ending May 6, 2024.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

This week’s update kicks off with some promising news that could impact your future investments and for borrowers across the board, whether they are individuals with mortgages, personal loans, or businesses with loans. As anticipated, the Bank of Canada trimmed the Canadian benchmark interest rate by 0.25%. While it may seem like a small adjustment, it is a step in the right direction. Additionally, positive developments emerged on the US economic front, indicating a cooling job market, which often signals a slowdown in the US economy. This shift raises the possibility of a rate cut in the US later this fall.

In addition to the economic updates, we will continue our series addressing frequent questions from those new to investing, along with insights gained from my personal experiences. This week, while researching our question of the week, I stumbled upon something new of which I was not previously aware. Once again, the process of writing this blog proves to be a learning experience for me. 😊 Let’s take a look at other highlights from this past week….

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, What about fractional shares?, What I learned this week, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Interest rate update

As expected, the Bank of Canada (BoC) reduced the Canadian benchmark interest rate by 0.25%, bringing it down to 4.75%. This move marked the first rate cut in over four years and positioned Canada’s central bank as the first among the G7 nations (Canada, France, Germany, Italy, Japan, United Kingdom, and the USA) to take such action. The rate had remained steady at 5.0% for eleven consecutive months prior to this adjustment.

The rate cut was prompted by inflation dropping below 3.0%, putting it within the BoC’s target range of 1.0% – 3.0%. BoC officials expressed confidence in the direction of inflation, anticipating reaching the 2% target sometime in 2025. However, they also noted concerns about a slowdown in the Canadian economy. The BoC is attempting to achieve a ‘soft landing,’ where inflation returns to 2% without stalling economic growth entirely. Additionally, they pointed out that the US economy is starting to slow, which could lead to decreased demand for Canadian products.

The modest 0.25% rate cut suggests the BoC is taking a gradual approach to adjusting interest rates while carefully monitoring the impact of their actions on inflation and economic growth. BoC Governor Tiff Macklem hinted at further cuts in the future but cautioned against expecting a return to pre-pandemic levels. For those who believe high rates have been a drag on stocks for the last two years, lower rates cannot come soon enough.

Lowering interest rates carries the risk of widening the gap between the Canadian and US benchmark rates. With US Federal Reserve officials signaling no imminent cuts to the US rate, such a gap could weaken the Canadian dollar against the US dollar, making imports more expensive for Canadians. Following the announcement, the Canadian dollar only experienced a slight decline. However, if the BoC follows through on its indications to lower the Canadian rate further, the disparity with the US rate could widen, potentially resulting in a more pronounced drop in the Canadian dollar’s value.

Labour Force Survey (LFS)

Statistics Canada’s May Labour Force Survey (LFS) presented a mixed picture of the job market, with jobs, unemployment and wages all higher. The Canadian economy added 27,000 jobs in May, surpassing analysts’ expectations of 22,500 jobs. This follows an unexpected surge of 90,400 jobs in April. The increase was mainly due to a 1.7% rise in part-time employment, while full-time employment dipped by 0.2%.

The unemployment rate matched analysts’ predictions, coming in at 6.2% in May, slightly up from 6.1% in April. Unemployment has been on the rise since April 2023, climbing by 1.1% over that period.

Wage growth, a key concern for the BoC, also picked up pace, accelerating to an annual rate of 5.1%, compared to 4.7% in April.

Following April’s unexpected surge of 90,400 jobs, the lower number of jobs in May suggests the Canadian economy is cooling. However, the job numbers were still higher than expected. Of more concern to the BoC would be the increased wage growth. Yet, as far as the BoC is concerned, the rise in unemployment might offset the impact of higher jobs and wages.

After the BoC’s recent decision to lower the benchmark rate by 0.25% to 4.75%, many analysts anticipated another 0.25% cut in July. However, this mixed report has reduced the likelihood of a July cut.

Canadian market volatility

During the past week, Canada’s Volatility Index (VIXC), measured by the TSX 60, experienced a slight uptick, closing at 9.73, up from 8.30, amidst an otherwise stable period. This rise could be attributed to investor optimism stemming from the BoC’s interest rate cut and mixed US labour reports, which have fueled expectations of a potential rate cuts by the US Federal Reserve.

Often referred to as Canada’s ‘fear gauge,’ the VIXC offers insights into expected volatility within the Canadian stock markets. Readings above 20 typically indicate high volatility, while those below 20 suggest lower levels.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Labour data

Each month, three labour market reports provide a snapshot of the current state of the American economy. Analyzing the latest data from the Job Openings and Labor Turnover Survey (JOLTS), ADP National Employment Report, and the Employment Situation Summary (ESS) provides a comprehensive view of the US labour market and reveals key trends in employment, and wage growth that can influence future economic policy.

Labor Department’s Job Openings and Labor Turnover Survey (JOLTS)

The Labor Department’s April JOLTS report revealed fewer job openings than expected, with 8.1 million available positions on the last business day of April. Analysts had been anticipating 8.340 million. This represents a 4% drop from the 8.488 million openings in March and an 18% decrease from the 9.9 million openings a year ago. These April numbers are the lowest since June 2021. Additionally, the ratio of job openings to each unemployed person fell to 1.24 from 1.3 in March.

When we look at the year-over-year data, ‘Private education and health services’ saw the largest increase in job openings, rising by 6.2%. In contrast, the ‘Information’ industry had the smallest increase at 3.5%. On a month-to-month basis, ‘Professional business services’ led the way with a 0.5% increase, while the ‘Information’ sector again underperformed, dropping by 1.3%. This decline in information sector jobs aligns with recent news that Alphabet (NASD: GOOGL) and Microsoft (NASD: MSFT) are planning to lay off hundreds of employees in the coming weeks.

The reduced number of job openings suggests that the labour market is continuing to cool down and is heading towards a more balanced state between labour supply and demand. This cooling labour market could help ease upward pressure on prices and continue to reduce inflation. However, with 1.24 job openings per unemployed person, the labour market remains relatively tight, indicating that there are still more job openings than unemployed individuals available to fill them.

ADP Employment Report

The May ADP Employment Report showed private payrolls growing by 152,000, a noticeable drop from the revised 188,000 in April and well below the analysts’ forecast of 175,000. Annual pay growth held steady at 5.0% for those who stayed in the same job. However, for job switchers, pay growth continued its decline, slipping to 7.8% from a revised 8.0% in April.

These lower hiring numbers and slower wage growth hint at a cooling job market, suggesting the possibility of a broader economic slowdown.

Bureau of Labor Statistics’ Employment Situation Summary (ESS).

The Labor Department’s ESS for May brought some surprises to the table. Nonfarm payroll employment saw a significant uptick, surging to 272,000 jobs, compared to a gain of 175,000 jobs in April. Analysts, who were expecting an increase of 185,000, were caught off guard by the robust numbers following a slowdown in April. Meanwhile, the unemployment rate saw a slight increase, coming in at 4.0% in May, contrary to analysts’ predictions of it remaining unchanged at 3.9%. This marked the first time in 27 months that it was not below 4.0%. Additionally, average hourly earnings rose 0.4% in May, up slightly from April’s 0.2% gain. On a year over year basis, the pace of wage growth accelerated to 4.1% from April’s 3.9% increase. Both number came in higher than analysts’ expectations of increases of 0.3% and 3.9%, respectively.

Despite April’s data showing signs of a slowing labour market, the May report paints a different picture. With more people joining the workforce and wages showing steady growth, the labour market remains robust. However, this unexpected surge in employment and wages does little to advance the case for the Fed to lower the interest rate.

Conclusion