Bank of Canada lowers the interest rate

As expected, the Bank of Canada (BoC) cut its interest rate by 0.25% on Wednesday, marking the second consecutive rate reduction. The rate now sits at 4.5%. This decision was driven by weakening consumer spending and economic growth, including rising unemployment and declining job creation. As well, inflation continues to decline and is now within the BoC’s target range of 1% to 3%. BoC Governor Tiff Macklem indicated a potential for further rate cuts if inflation continues to decline. The bank is now forecasting inflation to reach 2.4% by the end of the year.

The lower rates and an openness to further rate cuts is good news for consumers, businesses, and anyone who has a variable rate loan or mortgage. For consumers, lower interest rates mean cheaper loans for big-ticket items like homes, cars, and student loans. They may also have more money to spend on goods and services which is good for the economy. Businesses will benefit because they will be able to borrow money at lower rates to invest in expansion, research and development, or equipment. They may also see increased sales from consumers who have more disposable income. All of this is good news for us investors as companies with more cash and improved cash flow should lead to companies becoming more profitable, which in turn leads to higher share prices.

While the central bank is optimistic about inflation easing to their 2% target, it remains cautious about the overall economic outlook. The possibility of a prolonged economic slowdown and the potential for renewed inflationary pressures are key concerns. Essentially, the Bank of Canada is trying to balance the need to cool down inflation with the risk of a weakening economy.

With that bit of good news to start off the weekly update, let’s see what else happened this past week….

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, If investing is so easy…..

Canadian Economic news

This past week’s key economic data that the BoC considers when deciding whether to raise or lower the interest rate.

Canadian market volatility

Canada’s Volatility Index, the CVIX, saw a notable uptick this past week, jumping from 10.77 to a high of 14.51 before settling at 13.14 by week’s end. This surge likely mirrors the recent selloff in heavyweight US technology companies as investors shift gears towards smaller-cap companies with higher growth potential. Additionally, the uncertainty surrounding the upcoming US election and the possibility of the US Federal Reserve lowering the US interest rate in September adds to the market’s cautious mood.

Tracked as the VIXI on the Toronto Stock Exchange (TSE), the CVIX measures expected market volatility. A reading below 10 signals a calm and stable market, while 10 to 20 indicates moderate volatility and normal fluctuations. Readings above 20 suggest high volatility and significant market uncertainty. With the CVIX at 13.14, it reflects moderate volatility, suggesting relative investor confidence despite some caution due to recent events or underlying concerns. Overall, this level points to a relatively stable market environment with some risks present.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Personal Consumption Expenditures (PCE)

The Bureau of Economic Analysis reported a modest 0.1% increase in the PCE price index for June, following a flat reading in May. Annually, the index rose by 2.5%, down slightly from May’s 2.6% increase. Both the monthly and annual readings met analysts’ expectations. PCE are the value of the goods and services purchased by, or on the behalf of, “persons” who reside in the US.

Looking closer, the cost of goods decreased by 0.2% in June, following a 0.4% decline in May. This was offset by a 0.2% rise in the cost of services, matching May’s increase. Year-over-year, the price of goods edged up to 2.3% from 2.2%, while the price of services eased to 2.8% from 2.9%.

Core PCE, which excludes the volatile food and energy sectors, increased by 0.2% in June, slightly above an expected increase of 0.1%. On an annual basis, core PCE matched May’s increase of 2.6%, exceeding the forecast of 2.5%. Despite this higher-than-expected reading, it represents the slowest annual rise in over three years. This latest PCE report reinforces the trend that inflation continues to fall towards the Fed’s 2% inflation target.

The continued cooling of both headline PCE, or all items, and core PCE supports the case for potentially lower interest rates. Analysts expect the Fed to maintain the key interest rate at 5.5% during their July 30-31 meeting, with expectations for a rate cut following their September 17 – 18 meetings. Lower rates would be beneficial for consumers and businesses alike in that less cash would go towards debt payments and could be spent on goods and services which would further stimulate the economy.

Gross Domestic Product (GDP)

The Commerce Department’s Bureau of Economic Analysis delivered some surprising news with their advance estimate of GDP for the second quarter, showing a surge at an annual rate of 2.8%. This was well above analysts’ expectations of 2.0% growth and a significant jump from the 1.4% growth in the first quarter.

The second quarter’s robust performance was driven by a significant upturn in private inventory investment and robust consumer spending, offsetting a dip in residential fixed investment. Consumer spending was especially strong, increasing across both services (up 1.02%) and goods (up 0.55%), reflecting strong demand in healthcare, housing, recreation services, and more. Meanwhile, private inventory investment saw gains in wholesale and retail trade, which helped counterbalance declines in mining, utilities, and construction. Non-residential fixed investment also played a key role, with growth in equipment and intellectual property products, even as structures (construction of new buildings and other structures, as well as the improvements to existing structures that are intended for commercial, industrial, or other non-residential uses) investment took a hit. Notably, imports rose, especially in capital goods excluding automotive, indicating strong business investment.

GDP is a key indicator of a country’s economic health. A rising GDP generally points to a growing economy, while a decline can signal a slowdown. This latest report paints a picture of an American economy that is gaining momentum, though some areas show signs of slowing.

It is important to note that this ‘advance’ estimate is based on source data that are incomplete or subject to further revision. The ‘second’ estimate, which will include more complete data, is scheduled to be released on August 29, 2024.

American market volatility

The CBOE Volatility Index (VIX), known as the market’s “fear gauge,” surged to a peak of 19.24—its highest level since mid-April—before settling slightly lower at 16.38, down from 16.52 at the start of the week. This spike in volatility reflects investor concerns that major tech stocks, which have driven the market for the past eighteen months, may be losing steam. Additionally, speculation about a potential rate cut in September has led investors to cash in on profits and shift towards smaller, more volatile stocks. Meanwhile, uncertainties surrounding the upcoming presidential election and geopolitical tensions are further fueling market anxiety.

The VIX gauges expected market volatility over the next 30 days. Readings below 12 suggest calm and stability, while 12 to 20 indicates normal fluctuations. Levels between 20 and 30 point to heightened volatility and uncertainty, and above 30 signals high stress, often seen during crises. The recent uptick in the VIX indicates growing investor uncertainty and potential market volatility in the near term.

Consumer Sentiment Index (CSI)

The University of Michigan’s latest reading on the Consumer Sentiment Index (CSI) for July dipped to 66.4, down from 66 earlier in the month and 68.2 in June. This marks a 2.6% drop from June and a 7.1% decrease compared to a year ago, and while analysts had predicted a reading of 66, this decline marks the fourth straight month of falling consumer confidence. Despite this downturn, the CSI still stands above its historic low from June 2022.

Diving into the details, the Current Economic Conditions component of the CSI fell to 62.7, its lowest point in nineteen months, while the Index of Consumer Expectations for the next six months component came in at 68.8. It is clear that consumer sentiment is still recovering, as the overall index remains well below the pre-pandemic high of 101 set in February 2020.

The drop in the CSI this July likely stems from ongoing frustration with high prices due to persistent inflation. Additionally, the looming uncertainty of the upcoming presidential election seems to be adding to consumer jitters.

If investing is so easy, why aren’t more people making more money?

Many newcomers to investing wonder why more people are not making significant money in the stock market if it is as easy as it has been made out to be on all the ads for investing. The reality is that successful investing involves several factors that can complicate the process. Here are some key reasons why making money in the stock market is not as straightforward as it seems:

- Time, Compounding, and Starting Early: Investing is a long-term endeavor where the magic of compounding plays a crucial role. Just like an acorn does not turn into an oak tree overnight, investments need time to grow. Its never too late to start investing, but the sooner you start, the more time your investments have to compound, leading to greater potential gains.

- Lack of Knowledge and Monitoring: Many people do not fully understand how the stock market works and fail to keep an eye on their investments. This can lead to poor choices and missed opportunities.

- Emotional Decisions: Fear and greed can lead to impulsive decisions, such as selling during a market dip—like the recent drop in CrowdStrike’s stock after the global IT outage—or buying at a market peak. Sometimes, this fear of losses can even deter people from investing altogether.

- Short-Term Focus and Market Timing: Successful investing usually requires a long-term view. Many new investors get impatient, expecting quick returns, and trying to time the market often results in losses.

- Lack of Diversification: Putting all your money into one or a few stocks can be risky. If those investments perform poorly, it can lead to significant losses. Diversifying across different stocks and sectors helps spread risk.

- Life Circumstances and Unexpected Expenses: Unexpected expenses or life events can force people to withdraw their investments early, affecting overall returns.

- Starting Late: Compounding benefits grow over time, so starting late can limit potential gains.

- High Fees and Costs: Investing in high-fee funds or incurring high transaction costs can eat into profits. Choosing low-fee funds and minimizing transactions can help retain more of your returns.

- Unnoticed Gains: People might be making money but not tracking their investments closely. They might not realize they are making money because they are not monitoring their portfolios regularly.

Making money in the stock market requires knowledge, patience, and discipline. It is not always easy, but with the right strategy, you can get your money working for you and build wealth over time.

Weekly Market Review

Monday: the markets rebounded from Friday’s pullback, with all four indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – ending in the green. The recent shake up in the race to become the next US president has investors re-examining their views on the upcoming election. Oil prices dropped on rising inventories and lower demand.

In Canada, the TSX rose as investors anticipate another 0.25% rate cut later this week. In trading, Healthcare posted the biggest gain, while Basic Materials (miners and fertilizer manufacturers) and Telecommunications Services were the only two Canadian sectors to end in the red.

In the US, investors piled back into the mega cap technology after last weeks sell off. In trading, the Technology sector was the big winner, while Energy was the big loser.

Tuesday: the indexes ended on a down note with all four in the red. Alphabet (NASD: GOOGL), was the first of the big technology companies to report their latest quarterly earnings. Oil prices tumbled to a six-week low amid rising hopes for a ceasefire in Gaza and increasing worries about demand in China.

In Canada, lower oil prices weighed on the TSX as investors await tomorrow’s interest rate announcement from the BoC. In trading, Technology reported the biggest gain, while Energy saw the biggest decline.

Iin the US, the three indexes remained fairly tight to the flatline most of the day before dipping into the red at the end of the day as investors prepared for a flood of earnings reports. In trading, Basic Materials advanced the farthest, while Energy declined the most.

Wednesday: it was not a good day for the indexes, with all firmly lower in the red. Investors are growing concerned that the growth that fueled the big technology companies, and much of the overall rally, may be ending. Oil prices rose as US inventories declined.

In Canada, the good news that the BoC had lowered rates to 4.5% was offset by a sell off in technology companies as many investors took profits after a prolonged run up in share prices. In trading, Utilities advanced the most while Healthcare had the biggest fall.

In the USA, the S&P had its wort day in over a year as it snapped a 356-session streak without a decline over 2%. As well, the Nasdaq had its worst day since October 2022 and fell by more than 3% for the first time in 400 sessions. With underwhelming earnings reports from two of the Magnificent 7 companies, Alphabet and Tesla (NASD: TSLA), investors have grown skeptical of the potential payoff in artificial intelligence (AI). In trading, Utilities rose the farthest into the green, while Technology declined the most.

Thursday: the indexes teetered along the baseline all session before the TSX, S&P and Nasdaq all fell into the red at the end of the day. The DJIA was the only index to end in the green as the markets failed to recover to recover any of the ground lost in Wednesday’s sell off in the big technology companies. Oil prices rose after the latest US GDP report showed the American economy remained strong, offsetting concerns about lower demand from China.

In Canada, the TSX was weighed down by lower oil and commodity prices, as well as some lacklustre earnings reports. In trading, Healthcare gained the most, while Basic Materials sunk the deepest.

In the US, the latest GDP report showed the economy remains strong, growing by 2.8% in the second quarter. In contrast, some unimpressive earnings reports has investors wondering if the magic of the AI fuelled rally is starting to wear off. In trading, Energy posted the biggest gain with Telecommunications Services recording the biggest loss.

Friday: all four indexes bounced back from a turbulent week and ended the day solidly in the green. The latest US inflation data showed inflation continues to cool, increasing expectations the Fed will lower US rates in September. Oil prices fell on reports of lower demand out of China.

In Canada, falling inflation in the US helped the TSX got back in the win column as all ten sectors ended higher. Healthcare was the big winner, while Consumer Staples brought up the rear.

In the US, it was a day of broad-based gains, with both mega-cap technology companies and small-cap stocks rallying. All ten sectors recorded gains, with Industrials leading the charge and Energy trailing behind.

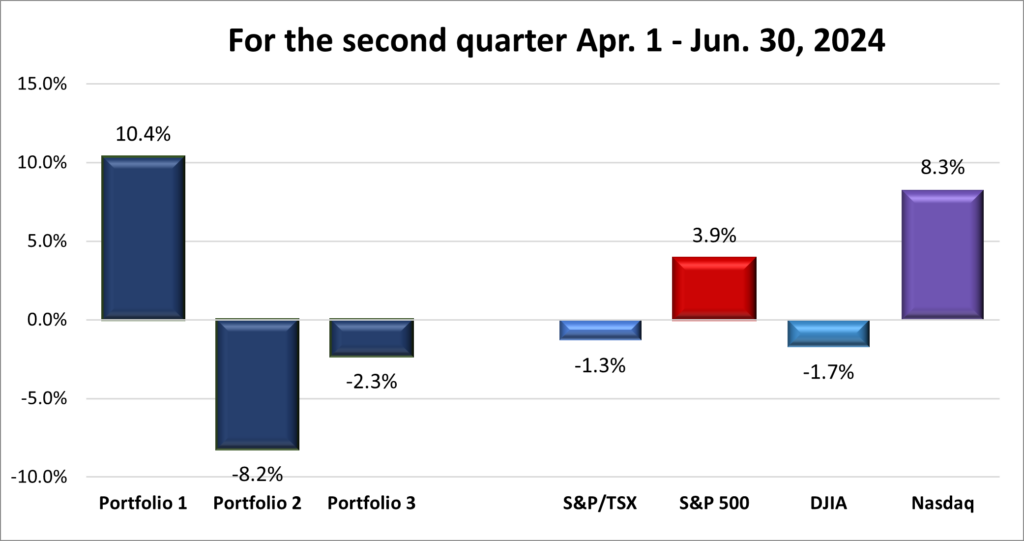

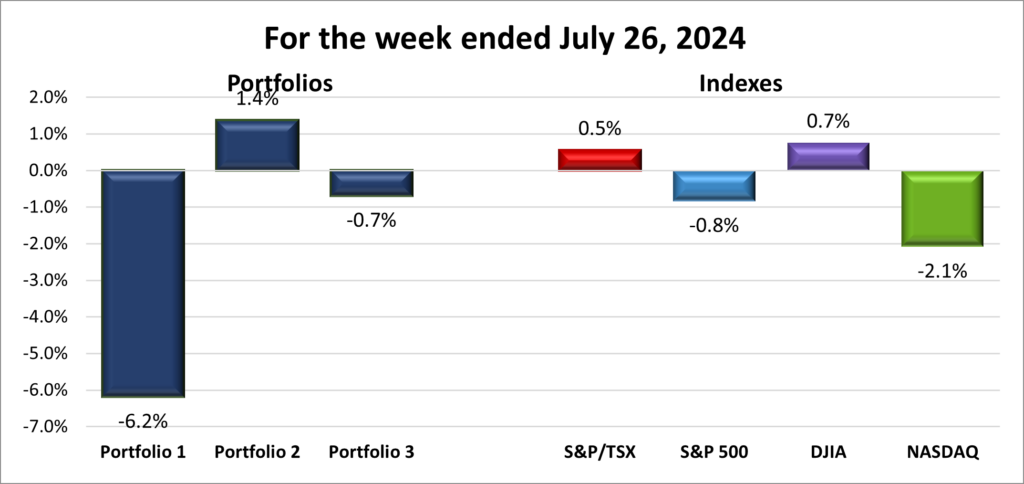

Weekly Market and Portfolio Review

For the week, the TSX (SPTSX) advanced 0.5%, the S&P 500 (SPX) fell 0.8%, the DJIA (INDU) gained 0.7% and the Nasdaq (CCMP) sank 2.1%.

| Index | Weekly Streak |

| TSX: | 5 – week winning streak |

| S&P: | 2 – week losing streak |

| DJIA: | 4 – week winning streak |

| Nasdaq: | 2 – week losing streak |

![]()

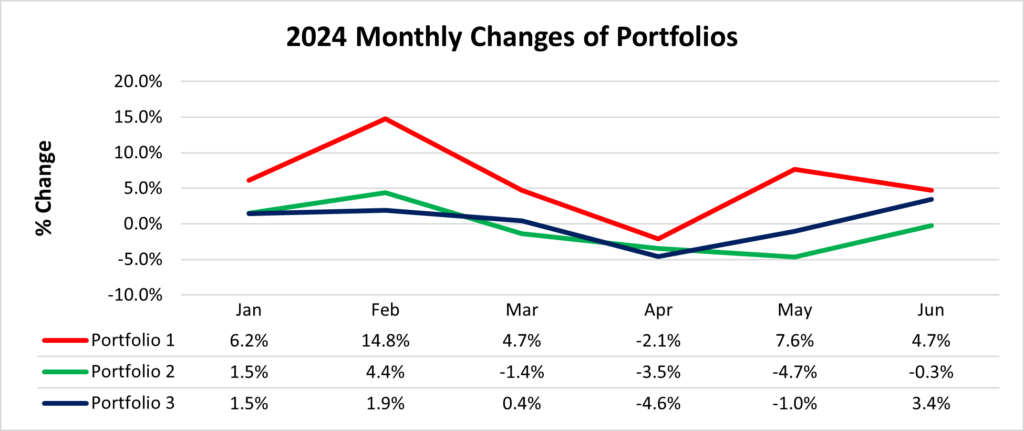

![]() It was a mixed week for the indexes, which faced turbulence before rebounding on the last day. As seen in the chart above, only the DJIA and the TSX managed to end in positive territory.

It was a mixed week for the indexes, which faced turbulence before rebounding on the last day. As seen in the chart above, only the DJIA and the TSX managed to end in positive territory.

The markets were influenced by a combination of economic news and the beginning of the second-quarter earnings season. In Canada, the TSX had a relatively calm week, ending positively after the BoC lowered interest rates for the second time. The BoC also shifted its focus from curbing inflation to stimulating economic growth. With Canada’s economy slowing, this shift likely signals more rate cuts in the coming months. The BoC is now focused on supporting the economy as inflation trends toward their 2% target.

In the US, the second-quarter GDP reading came in stronger than expected, indicating a robust economy. Simultaneously, the latest inflation report shows that inflation continues to fall.

Despite generally positive economic news, the markets experienced volatility due to mixed earnings reports and a rotation of investor interest from mega-cap technology companies (a market capitalization of $200 billion or more) to small-cap stocks (companies with a market capitalization of less than $2 billion). The early-year market rally, largely driven by excitement over AI, seems to have lost momentum as investors begin to question whether big tech companies can continue to meet ever-rising expectations. There are growing concerns about whether the substantial investments in AI will ultimately pay off.

This uncertainty led to a significant stock market selloff on Wednesday, wiping out hundreds of billions of dollars in value from the Magnificent 7 group of tech giants. Fortunately, many of these companies rebounded on Friday, recovering some of the losses. However, investors are now betting that small-cap stocks will likely outperform them as interest rates decline.

For the past two weeks, the Magnificent 7 technology companies, which have led the market all year, have been struggling. Alphabet’s recent report showed rising revenues and net income, but it was not enough to impress investors. The upcoming week is crucial for this group, with Amazon (NASD: AMZN), Apple (NASD: AAPL), and Microsoft (NASD: MSFT) all set to report their quarterly earnings. These reports will be closely watched to see if they can exceed expectations or, like Alphabet’s recent earnings, be strong but not strong enough.

Next week could be pivotal for the markets. The outcome of the Magnificent 7’s earnings announcements will play a crucial role in determining whether this is just a typical bull-market pullback or the start of an extended downturn. Additionally, the combination of a strong economy and falling inflation has created an opportunity for the Fed to lower interest rates in September. The big question is whether they will take advantage of this opportunity. 😊 Next week, the Fed takes centre stage as they announce their latest US interest rate decision and set the tone for their September meeting, where a rate cut is expected. Let us keep our fingers crossed for good news on all fronts. 😊

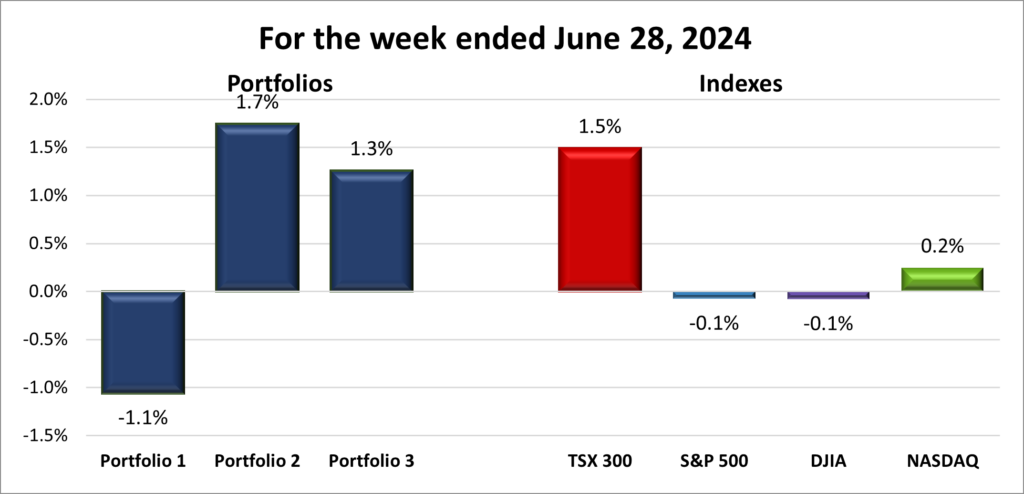

| Portfolio | Weekly Streak |

| Portfolio 1: | 2 – week losing streak |

| Portfolio 2: | 5 – week winning streak |

| Portfolio 3: | 2 – week losing streak |

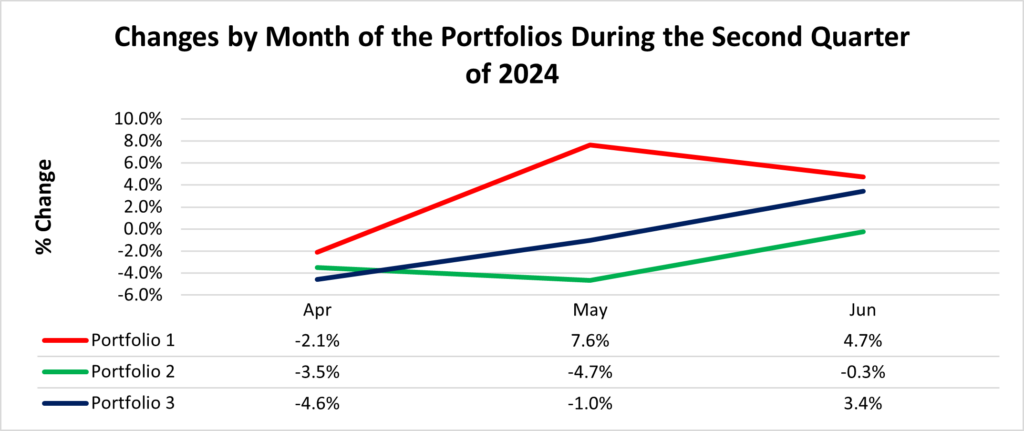

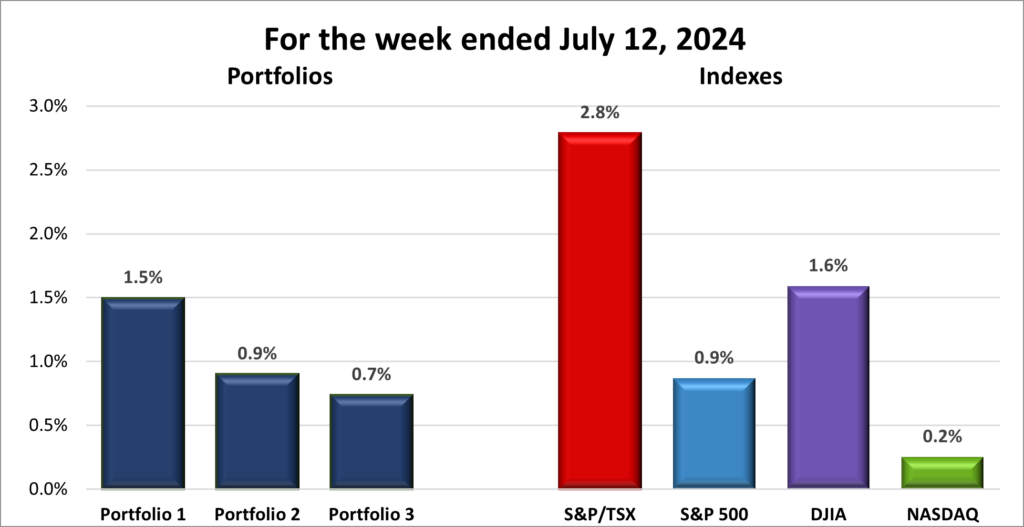

![]() It was another mixed week for the three portfolios. Once again, Portfolio 2 was the star, being the only one to see an increase in value, as shown in the chart below.

It was another mixed week for the three portfolios. Once again, Portfolio 2 was the star, being the only one to see an increase in value, as shown in the chart below.

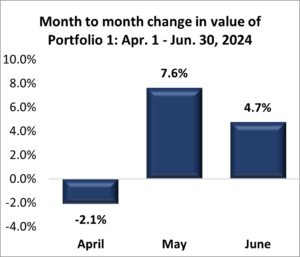

Portfolio 1 had a particularly rough week, losing almost nine times more than Portfolio 3. The downturn in mega-cap tech stocks hit the portfolio hard, overshadowing a record high by Formula One Group (NASD: FWONK) and a 12% gain from Hammond Power Solutions (TSE: HPS.A).

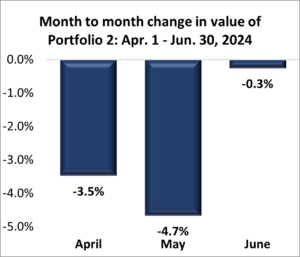

Portfolio 2, on the other hand, extended its winning streak to five weeks, with nearly 75% of its holdings gaining value, including the impressive 12% increase from Hammond Power Solutions. If only the other portfolios could have 70% or more of their companies posting weekly gains consistently! 😊

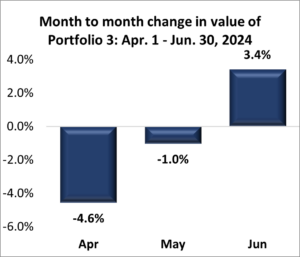

Unfortunately, Portfolio 3 also decreased in value this week. While the number of stocks that gained and lost value was evenly split, the losses were greater in dollar terms than the gains. ☹

Overall, it wasn’t the best week for the portfolios, with Portfolio 1 taking a significant hit and Portfolio 3 struggling to gain ground. However, Portfolio 2’s consistent performance underscores the benefits of a balanced and conservative stock selection. Unfortunately, this week’s gains in Portfolio 2 were overshadowed by the losses in Portfolio 1. Hopefully, the positive momentum from the end of the week carries into the next, allowing Portfolio 2 to extend its winning streak and giving Portfolios 1 and 3 a chance to rebound. 😊

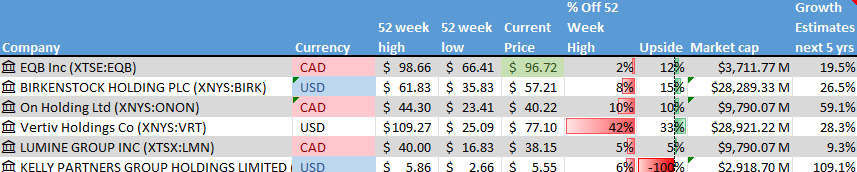

Companies on the Radar

Two footwear companies caught my attention last week, one familiar and the other not so much. First up is Birkenstock Holding plc (NYSE: BIRK). I always imagined Birkenstock as a California brand that emerged in the 1960s. Boy, was I wrong. Birkenstock is actually a British-based company that has been around since 1774. Famous for their iconic sandals, it is a family-run business now in its sixth generation. Surviving for 250 years is no small feat, so they must be doing something right.

Two footwear companies caught my attention last week, one familiar and the other not so much. First up is Birkenstock Holding plc (NYSE: BIRK). I always imagined Birkenstock as a California brand that emerged in the 1960s. Boy, was I wrong. Birkenstock is actually a British-based company that has been around since 1774. Famous for their iconic sandals, it is a family-run business now in its sixth generation. Surviving for 250 years is no small feat, so they must be doing something right.

The other company is On Holding AG (NYSE: ONON), a lesser-known but equally interesting Swiss-based, founder-run, sports products company. Founded in 2010, they specialize in athletic shoes, apparel, and accessories.

Both companies sound interesting, and I plan to dig a little deeper into these companies. They will be joining the four holdovers from last week:

- Equitable Bank (TSE: EQB), a mid sized Canadian bank, considered Canada’s 7th bank, that provides financial services to consumers and businesses.

- Vertiv Holdings (NYSE: VRT), a large American company that designs and builds infrastructure and continuity solutions to businesses around the world.

- Lumine Group (TSE: LMN), a young Canadian mid sized company that acquires communications and media software companies, and then strengthens and grows those companies.

- Kelly Partners Group (OTCM: KPGHF), a small Australian accounting firm that is growing through serial acquiring of other small accounting firms in Australia. They have recently expanded into the USA and other English-speaking countries.

Please keep in mind that these are only companies that have piqued my interest. This is not a recommendation or financial advice. You should do your own research or contact a professional before making any investment decisions.

The Radar Check was last updated July 26, 2024.

NOTE: Morningstar and Thomson-Reuters analysis is unavailable for Kelly Partners Group most likely because it is a small-cap Australian company with a market value of less than US$360 million and primarily listed on the Australian Stock Exchange. While you can invest in Kelly Partners through the Over-the-Counter Market (OTCM) here in North America, the analysis is not as readily available as it is for companies on major North American exchanges like the Toronto Stock Exchange, New York Stock Exchange, and Nasdaq.

Unlike other non-North American companies I have investigated, even Yahoo! Finance did not have any information under the Analysis tab for Kelly Partners. This means I could not get any ratings during my usual radar check.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended July 26, 2024: DOWN ![]()

- Nvidia is developing a version of its high-end AI chips for the Chinese market that would comply with current US export restrictions.

- General Motors (NYSE: GM) announced they were delaying the release of a Buick electric vehicle (EV) and pausing the construction of an EV truck factory.

- Grab Holdings (NASD: GRAB) announced they acquired dining reservation platform Chope to compliment heir food delivery operations in southeast Asia.

- Canadian National Railway (TSE: CNR) resumed shipping goods through Jasper National Park after a major wildfire forced it to suspend operations.

- Walmart (NYSE: WMT) is considering investing up to US$ 200 million on autonomous forklifts to increase the automation of their warehouse operations. They are currently conducting pilot projects in four locations.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Decisive Dividend Corp (TSE: DE) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

Canadian National Railway Company

Second quarter 2024 financial results on July 23, 2024

General Motors Co.

Second quarter 2024 financial results on July 23, 2024

Alphabet Inc.

Second quarter 2024 financial results on July 23, 2024

Visa Inc.

Third quarter 2024 financial results on July 23, 2024

Celestica Inc.

Second quarter 2024 financial results on July 24, 2024

Portfolio 2

Portfolio 2 for the week ended July 26, 2024: UP ![]()

- The Walt Disney Company (NYSE: DIS) announced they had reached a tentative labour deal with their Disneyland employees. The new deal is for three years and includes higher wages plus other benefits.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Canadian $

No C$ dividends this past week.

US $

Walt Disney Co. (NYSE: DIS)

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended July 26, 2024: DOWN ![]()

- Microsoft reported that the previous week’s IT outage caused by a CrowdStrike (NASD: CRWD) software update impacted almost 8.5 million Microsoft devices. That is fewer than 1% of all Windows devices in the world. CrowdStrike reported that most impacted devices were back online and operational.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.

In the US, investor sentiment shifted from early-year optimism about imminent rate cuts to a more cautious “higher for longer” outlook, as persistent inflation and robust labour market data complicated the Federal Reserve’s (Fed) plans. Yet, by May, cooling inflation rekindled hopes for potential rate cuts later in the year, propelling the Nasdaq Composite Index (Nasdaq) and S&P 500 (S&P) to record highs, largely driven by the surge in artificial intelligence (AI) stocks.

In the US, investor sentiment shifted from early-year optimism about imminent rate cuts to a more cautious “higher for longer” outlook, as persistent inflation and robust labour market data complicated the Federal Reserve’s (Fed) plans. Yet, by May, cooling inflation rekindled hopes for potential rate cuts later in the year, propelling the Nasdaq Composite Index (Nasdaq) and S&P 500 (S&P) to record highs, largely driven by the surge in artificial intelligence (AI) stocks.