Items that may only interest or educate me ….

Canadian Economic news, US Economic news …

But first….

…. Thank you!

It is earnings report season again, this time for the third quarter. The number of companies reporting in the three portfolios has been increasing steadily, reaching 35 this week. I admit it can cause one’s eyes to glaze over, however, these reports are crucial to understanding how the companies you own are faring.

With all the reports this past week, fortunately, there were no key economic reports in Canada or the US this past week. Otherwise, this Weekly Update would have gone on forever, writing it certainly seemed like it did. Sigh! 😊

Canadian Economic news

This past week there were no key economic reports that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Bank of Canada monetary policy notes

The Bank of Canada’s governing council released the Summary of Governing Council deliberations (yes, that is what the minutes are called) from their October 25 monetary policy meeting, where they set the benchmark interest rate.

In the meeting, the BoC’s governing council discussed the key factors that influenced their decisions about interest rates. They acknowledged the challenge of combating inflation, which currently stands at 3.8%. Core inflation, excluding volatile gas and food prices, remains high at around 4%. Both are well above the target rate of 2%. The bank mentioned rising oil prices and increased government spending as factors that contributed to upward pressure on inflation. They also noted the role their higher interest rates have played in driving housing costs up.

They discussed both the global and domestic economic situation. On the global stage, many economies showed signs of slowing down, with inflation falling in most economies. The US economy remained robust, while China experienced slower growth than expected. Domestically, Canada’s economic growth slowed to 1%, indicating the desired impact of the increased interest rates. Consumer spending was reduced due to higher interest rates. Job creation dipped below the growth rate of the labor force, leading to a slight easing in labour shortages. However, wages continued to grow at an annual rate of 4% – 5%.

In terms of policy decisions, the council members expressed concerns about core inflation remaining between 3% – 4%, which could be a sign that inflation is becoming more entrenched. Although a few members of the six-person council felt another hike would be necessary, they reached a consensus to be ‘patient’ and leave the rate unchanged at 5%, a 22 year high. They anticipate leaving the rate higher for longer will lead to a gradual decline in inflation, reaching the 2% target in 2025.

Their next and final meeting of the year is scheduled for December 6, 2023. Until then, the BoC emphasized it will continue to closely monitor the impact of its policy decisions on the Canadian economy and financial system.

Bank of Canada comments

Following the publication of the ‘Summary of Governing Council deliberations,’ Senior Deputy Governor Carolyn Rogers of the BoC issued a cautionary note. She suggested that the era of extremely low-interest rates is likely coming to an end. Throughout the pandemic, the BoC kept the benchmark rate within the lower range of their 1% – 3% target, specifically at 0.25% – 1.75%. Rogers advised consumers and businesses to “proactively adjust to a future where interest rates may be higher than they’ve been over the past 15 years.” In simpler terms, once inflation reaches 2%, it is unlikely that interest rates will return to the levels seen during the pandemic.

Canadian market volatility

The Canadian Volatility Index (VIXC), represented by the TSX 60 VIXI, ended the week at 15.03, up from last week’s reading of 14.14. While there was a perceived increase in market volatility in the Canadian stock markets, the VIXC remains comfortably below 20. In the context of the VIXC, a reading above 20 is considered high, while below 20 is deemed low. The current reading of 15.03 suggests that investors maintained a predominantly bullish outlook on the Canadian stock markets, despite perceived increase volatility.

US Economic news

This past week there were no key economic reports that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Consumer Sentiment Index

The preliminary reading on consumer sentiment from the University of Michigan for November came in at 60.4. This is a significant drop from October’s 63.8 and falls below analysts’ expectations of a 63.7 reading. On a monthly basis, the Consumer Sentiment Index (CSI) declined by 5.3%, but on an annual basis, it is still up 6.5%.

This marks the lowest reading since May and the fourth consecutive month of decline, indicating an ongoing dip in consumer confidence and optimism about their economic outlook. The primary concerns voiced by consumers were concerns about higher interest rates and geopolitical tensions, particularly the conflicts in Ukraine and the Middle East.

The CSI is a key metric used to assess how consumers perceive the current economic situation and their expectations for the future.

American market volatility

During the week, the CBOE Volatility Index (VIX) dropped to 14.17, down slightly from 14.91 the previous week. This indicates that investors maintain a bullish outlook on the stock markets, despite this week’s hawkish remarks from various Fed officials. The marginal decline in VIX suggests they are relatively unconcerned about volatility in the American stock markets.

Last week’s rally was sparked by hopes the Fed was finished with rates hikes and could switch to interest rate reductions sooner rather than later. Did it carryover into this week. Let’s see what happened ….

Weekly Market Review

Monday: there was no solid direction one way or the other today. Canada’s Toronto Stock Exchange Composite Index (TSX) ended in the red, while the three American indexes – the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – bounced back and forth before ending slightly higher. Oil prices rose after Saudi Arabia and Russia confirmed they will continue with their production cuts, reducing global oil supplies.

In Canada, the TSX’s winning streak came to an end as commodity prices fell. In trading in the Canadian sectors, the Consumer twins, Staples and Cyclicals, were the only sectors to advance. Basic Materials (miners and fertilizer manufacturers) and Technology sectors suffered the largest losses.

In the US, investors await speeches from various Fed officials throughout the week to get clues what the Fed will do at their next session in December. In trading in the American sectors, Healthcare and Technology posted the biggest gains, while Energy and Financials dropped the most.

Tuesday: a mixed bag for the indexes as the TSX began a losing streak, while the three American indexes each extended their winning streaks. Signs of a weaker US economy caused investors to believe the Fed was finished with rate hikes. Today, various Fed officials said not so fast. They felt the economy was still running stronger than expected and another interest rate may be necessary to bring inflation down. Oil prices faltered on the possibility of another rate hike and signs of lower demand for oil coming from China.

In Canada, after last week’s rally on the TSX, the index has now fallen for the second straight day. Lower commodity prices sparked a drop in energy and other commodities companies. In trading, the Technology sector was the only Canadian sector to advance, while Energy and Basic Materials posted the biggest losses.

In the US, spurred on by falling yields on government bonds and gains by the big technology companies, the S&P and DJIA stretched their winning streaks to seven, while the Nasdaq posted its eight consecutive day in the green. It was the longest streak in two years for both the S&P and the Nasdaq. In trading, the biggest gains in the American sectors were Technology and Consumer Cyclicals, while Energy and Basic Materials suffered the heaviest losses.

Wednesday: a mixed day for the indexes with the more value oriented TSX and DJIA declining. The growth-oriented Nasdaq and S&P climbed out of negative territory in afternoon trading to end slightly higher. Much of the recent upward momentum has stalled after Fed officials cooled investor optimism with warnings another rate hike was not off the table.

In Canada, lower commodity prices continued to weigh on the TSX, sending it to a third day of losses. In trading in the Canadian sectors, Technology and Industrials posted the biggest gains, while Basic Materials and Energy suffered the largest losses.

In the US, the American markets were essentially flat, however, the Nasdaq was able to stretch its winning streak to nine and the S&P ran its winning streak to eight. In trading, the Technology and Industrials sectors were the only ones to end higher. Energy and Utilities had the biggest decline.

Thursday: another mixed day in the markets with Canada’s TSX ending higher while all three American indexes ended lower. The Nasdaq and S&P both saw their longest winning streaks in two years come to an end. Oil prices rebounded after a sell off earlier this week caused by concerns higher for longer interest rates would lead to lower demand.

In Canada, the TSX finally broke out of its losing streak on the strength of a rebound in oil and commodity prices, propelling the resource heavy index into the green. In trading, the Basic Materials and Telecommunications Services sector had the biggest increases while the Technology and Healthcare sectors had the largest losses.

In the USA, the American indexes were dragged down by hawkish comments from Fed Chair Jerome Powell who said the Fed “are not confident” interest rates are high enough to push inflation down to their desired 2% target. Yields on government bonds rose, adding additional downward pressure on stocks. In trading, the Energy sector was the only one of the American sectors to post a gain. Healthcare and Consumer Cyclicals posted the largest losses.

Friday: despite hawkish comments from various Fed officials, all four indexes ended the day in the green. Investors were feeling confident that interest rates will remain unchanged for the rest of the year and moved back into the markets, particularly the higher growth sectors like Technology. Oil prices rose after Iraq supported production cuts by OPEC+ members. As prices rose, investors who had shorted oil company stocks earlier this week started to cover their positions, pushing share prices even higher.

In Canada, rising oil prices provided a boost to energy stocks in the TSX. In trading, Technology and Energy were the big winners on the day, while Basic Materials and Utilities suffered the biggest losses.

In the USA, the Nasdaq had its best day since late May and all three American indexes are at their highest level since mid September. In trading on Wall Street, every sector ended in positive territory, led by the growth-oriented Technology and Consumer Cyclicals sectors. The defensive sectors Consumer Staples and Utilities trailed the pack but still posted gains.

Weekly Market and Portfolio Review

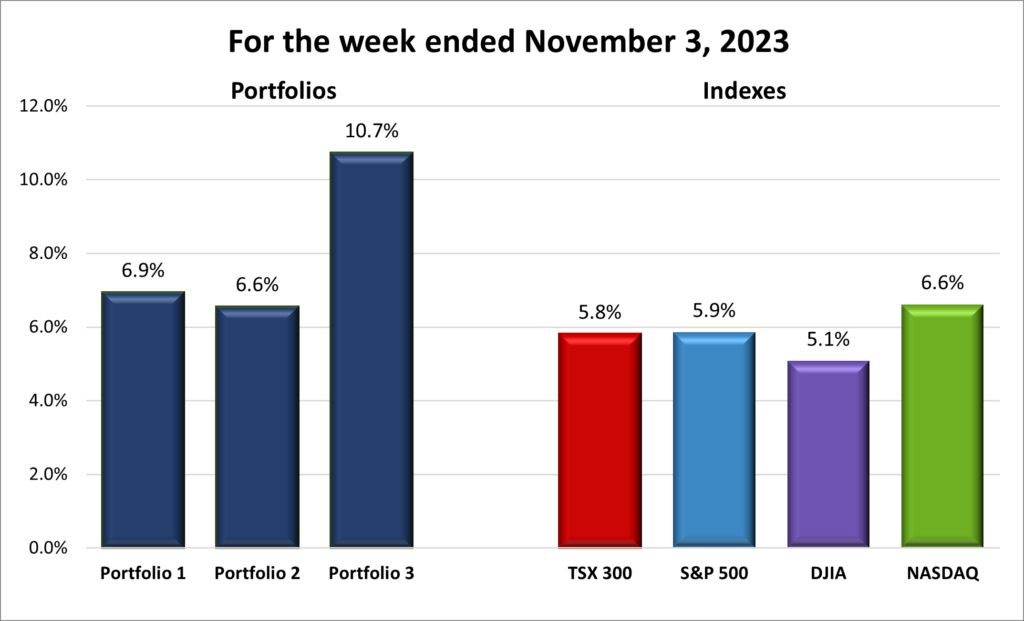

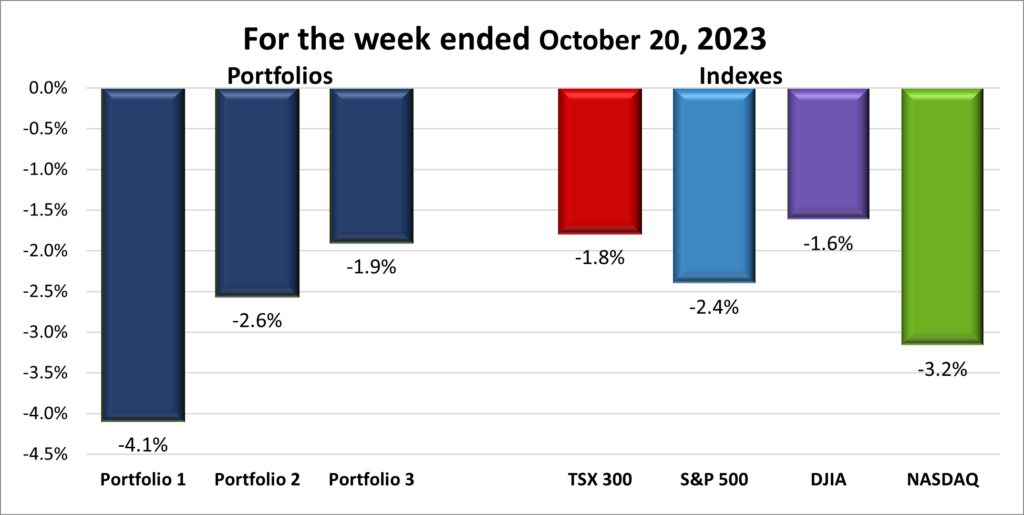

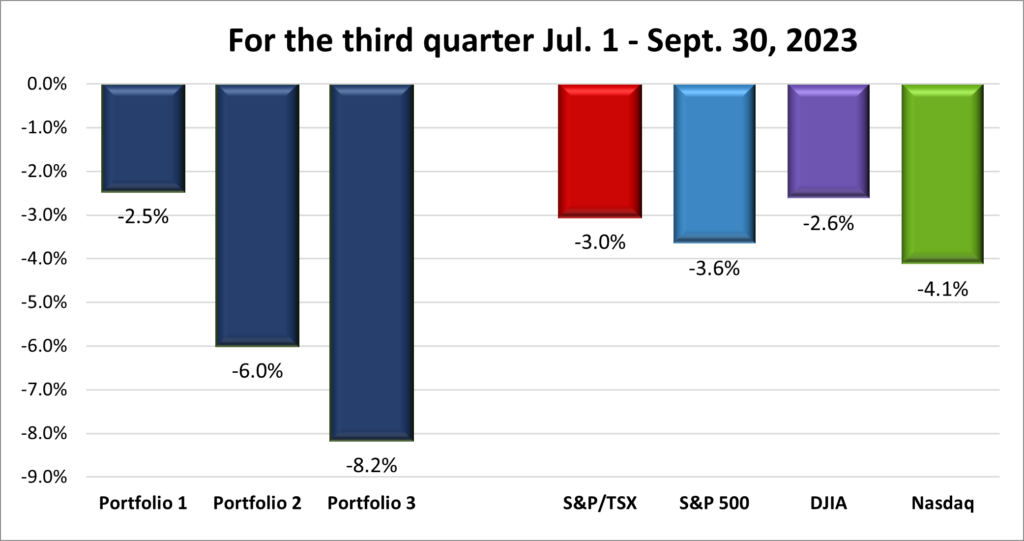

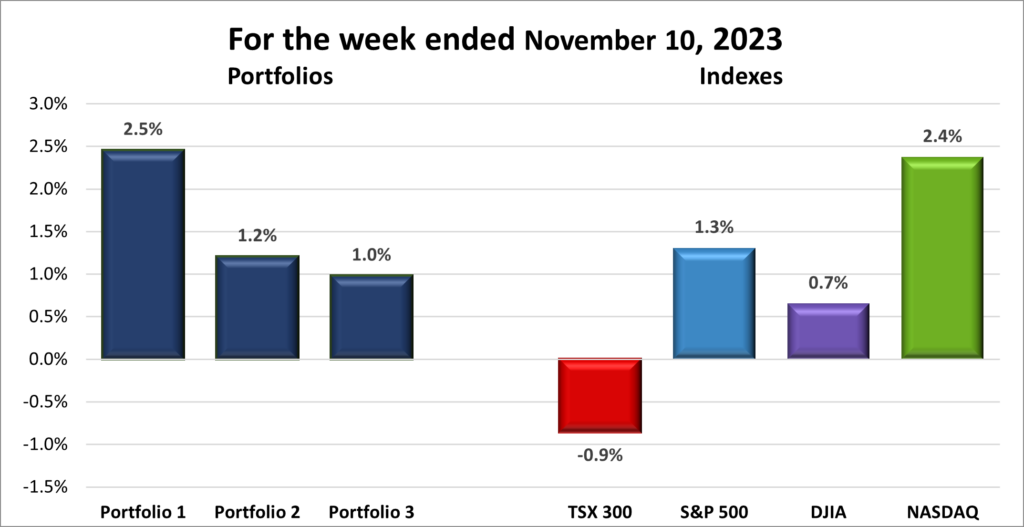

For the week, the TSX (SPTSX) slipped 0.9%, the S&P 500 (SPX) advanced 1.3%, the DJIA (INDU) gained 0.7% and the Nasdaq (CCMP) jumped 2.4%.

![]() Overall, another good week for the indexes with three of four posting gains for the week, as you can see in the chart above. November got off to a fast start last week thanks to the Fed leaving the US interest rate unchanged. Upward momentum slowed this week after various Fed officials said another interest hike may be necessary given the ongoing strength of the US labour market. However, investors shrugged this off and believe there will not be another rate hike in 2023, keeping the American indexes moving upward and posting their second consecutive week of weekly gains thanks to a surge in the mega cap technology companies.

Overall, another good week for the indexes with three of four posting gains for the week, as you can see in the chart above. November got off to a fast start last week thanks to the Fed leaving the US interest rate unchanged. Upward momentum slowed this week after various Fed officials said another interest hike may be necessary given the ongoing strength of the US labour market. However, investors shrugged this off and believe there will not be another rate hike in 2023, keeping the American indexes moving upward and posting their second consecutive week of weekly gains thanks to a surge in the mega cap technology companies.

As for the TSX, after posting a six-week high last Friday, it went on a three-day losing streak on fears of lower demand for oil and commodities, due to the ongoing slowdown in the global economy. However, the TSX rallied at the end of the week, recouping some of its earlier losses.

![]() The portfolios had another solid week, with all three gaining in value. Portfolio 1 got a sizable boost from its mega cap technology companies as well as notable strong performances from Docebo (TSE: DCBO), Datadog (NASD: DDOG) and Nuvei (TSE: NVEI). On the downside, the Trade Desk (NASD: TTD) dropped 20% after it issued disappointing guidance for the fourth quarter.

The portfolios had another solid week, with all three gaining in value. Portfolio 1 got a sizable boost from its mega cap technology companies as well as notable strong performances from Docebo (TSE: DCBO), Datadog (NASD: DDOG) and Nuvei (TSE: NVEI). On the downside, the Trade Desk (NASD: TTD) dropped 20% after it issued disappointing guidance for the fourth quarter.

In Portfolio 2, it seemed for every stock that had a good week there was an offsetting stock that had a poor week. Solid gains from Take-Two Interactive (NASD: TTWO), MongoDB (NASD: MDB), Disney (NYSE: DIS), and Alimentation Touche Card (TSE: ATD) were offset by drops in Guardant Health (NASD: GH) and the oil companies. Fortunately, the strong performances overcame the poor performances.

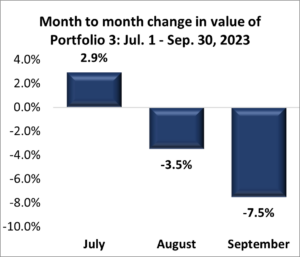

Portfolio 3 benefitted from strong performances from Microsoft, which reached an all time high, and Adyen (OTCM: ADYEY) which gained 30% after the company said it would slow hiring and lowered its forecast for net sales growth over the next year. However, poor performances from GDI Integrated Services (TSE: GDI) and the Brookfield family of companies in the portfolio limited the gains.

Next week is highlighted by the American Consumer Price Index report for October. A higher-than-expected inflation reading could stop this rally in its tracks and send stocks lower, while a lower number could see the return of the bulls. I have my fingers crossed for the later. 😊

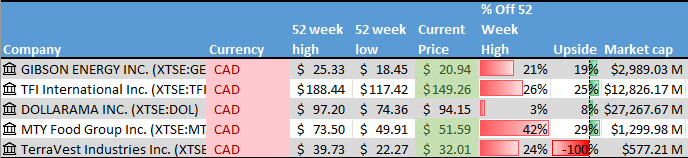

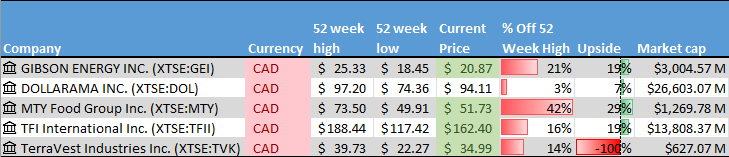

Companies on the Radar

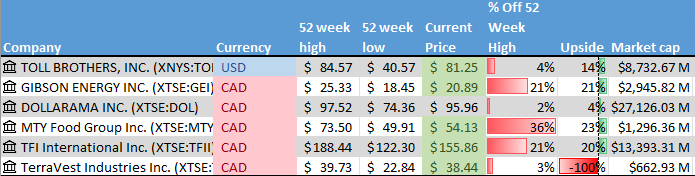

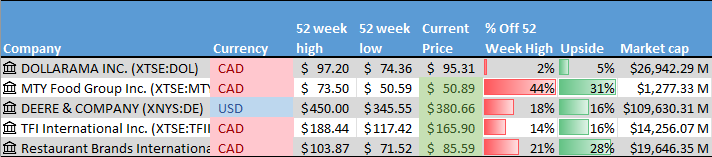

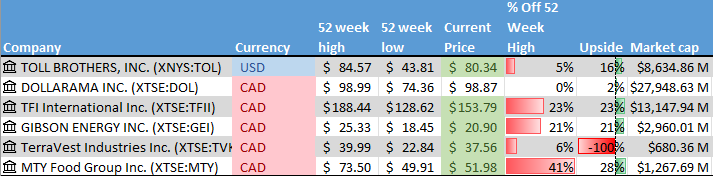

It has been such a busy week with quarterly earnings that I have not had a chance to perform any due diligence on the companies currently on my radar, let alone come across any additions. For another week these six companies remain on my radar list:

It has been such a busy week with quarterly earnings that I have not had a chance to perform any due diligence on the companies currently on my radar, let alone come across any additions. For another week these six companies remain on my radar list:

- Toll Brothers Inc. (NYSE: TOL), a mid cap American company that builds luxury homes throughout the US.

- Dollarama (TSE: DOL), a large Canadian company that operates dollar stores across Canada.

- TFI International Inc. (TSE: TFII), a mid-sized Canadian transportation and logistics company operating throughout North America.

- Gibson Energy (TSE: GEI), a small-cap Canadian company specializing in providing liquid infrastructure products and services to the North American energy sector.

- TerraVest Industries (TSE: TVK), a small-cap Canadian company that manufactures and sells goods and services to energy, agriculture, mining, and transportation sectors across North America. NOTE: because TerraVest has a market capitalization in the range of $300 million to $3 billion), it is not followed by any analysts. Therefore, there is no twelve-month price target for this company’s share price.

- MTY Food Group Inc. (TSE: MTY), a small cap Canadian consumer cyclical company that operates and franchises quick service and casual dining restaurants throughout North America and internationally.

The Radar Check was last updated November 10, 2023.

Portfolio Update

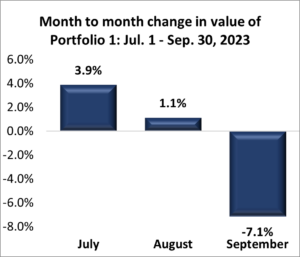

Portfolio 1

Portfolio 1 for the week ended November 10, 2023: UP ![]()

- Berkshire Hathaway (NYSE: BRK.B) reported a 40% increase in operating profits to US$10.8 billion, while growing cash to US $157 billion in the third quarter. During that time, the company sold more than US$5 billion worth of stocks. And where did Warren Buffet, one of the world’s top investors, put all that money? US Treasury bills yielding 5% or more. A 5% return on a few billion dollars is a lot of money. Best of all, its almost risk free.

- Tesla (NASD: TSLA) plans to build a 25,000 euro (~ C$ 36,700 or ~US$ 26,800) electric vehicle (EV) at their Berlin factory. No date has been set for the start of production.

- The US Consumer Financial Protection Bureau (CFPB) is proposing they start regulating digital payments and smartphone wallet services provided by technology companies. The CFPB says the new breed of financial services providers rival traditional payment methods in both scale and scope but do not come with any consumer safeguards. Among the companies impacted are Apple (NASD: AAPL), Alphabet (NASD: GOOGL) and PayPal (NASD: PYPL).

- General Motors’ (NYSE: GM) self driving unit Cruise is recalling 950 driverless cars after one of its driverless taxis dragged a pedestrian after being involved in an accident. The current software may cause the car to pull over after being in an accident rather than remaining at a standstill.

In other GM news, United Auto Workers (UAW) members at GM’s Flint, Michigan factory narrowly voted against GM’s proposed deal, raising doubts on the approval of the contract. - Amazon (NASD: AMZN) continue to lower its headcount. This time their Music division is the latest unit to scale back its workforce as the company continues to lower expenses.

- In response to the US government’s ban on the sale to China of advanced semiconductors used for artificial intelligence applications, Nvidia (NASD: NVDA) announced the production of three new chips for the Chinese market. The chips would have much of the latest features of their high-end chips but have had some of their computing power limited to comply with US export rules.

Activity

Sold Marqeta, Inc. (NASD: MQ) I invested in Marqeta back in November 2021, when the markets had reached their peak before the downdraft of 2022 was even on the horizon. At the time, almost every company saw its share price rise. My reason for investing in the company was “Companies will continue to move to ‘modern cards’ to replace traditional debit and credit cards.”

When the market was rising, and every company had access to cheap money it sounded like a good idea that companies would move to the ‘new’ type of debit and credit card. Now that money is no longer cheap, I do not think many companies will be spending their cash on items that are not core to their business. A new type of card is not critical to many companies when they can do fine accepting payments from existing credit and debit card companies like Visa (NYSE: V).

I thought the share price was reasonable at the time, but it has lost over 70% since I invested and has stayed at its current level for most of 2023. I finally decided to cut my losses and look for other opportunities. ☹

My takeaway, from this investment is smaller, niche companies like Marqeta may have a good idea, but when economic times are tough, many potential customers are reluctant to spend money on items not essential to their business.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Bank of Nova Scotia (TSE: BNS) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

Formula One Group

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 3, 2023

- Revenue of $887 for the three months ended September 30, compared to $715 for the same period in 2022. An increase of almost 44%.

- Net income of $118 for the three months ended September 30, compared to net income of $108 in the same period in 2022.

- Diluted earnings per ordinary share of $0.39 for the three months ended September 30, compared to earnings of $0.31 per share for the same period in 2022.

- Revenue of $1,992 for the nine months ended September 30, compared to $1,819 for the same period in 2022. An increase of over 24%.

- Net earnings of $125 for the nine months ended September 30, compared to net earnings of $184 in the same period in 2022.

- Diluted earnings per ordinary share of $0.37 for the nine months ended September 30, compared to earnings of $0.60 per share for the same period in 2022.

Berkshire Hathaway Inc.

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 4, 2023

- Revenue of $93,210 for the three months ended September 30, compared to $76,904 for the same period in 2022. An increase of over 22%.

- Net loss of $12,567 for the three months ended September 30, compared to a net loss of $2,698 in the same period in 2022.

- Diluted loss per ordinary share of $5.88 for the three months ended September 30, compared to a loss of $1.27 per share for the same period in 2022.

- Revenue of $271,106 for the nine months ended September 30, compared to $223,948 for the same period in 2022. An increase of over 21%.

- Net earnings of $59,389 for the nine months ended September 30, compared to net earnings of $40,235 in the same period in 2022.

- Diluted earnings per ordinary share of $26.95 for the nine months ended September 30, compared to a loss of $18.51 per share for the same period in 2022.

Celsius Holdings, Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 7, 2023

- Revenue of $384,757 for the three months ended September 30, compared to $188,233 for the same period in 2022. An increase of over 104%.

- Net income of $83,949 for the three months ended September 30, compared to a net loss of $181,896 in the same period in 2022.

- Diluted earnings per ordinary share of $0.89 for the three months ended September 30, compared to a loss of $2.46 per share for the same period in 2022.

- Revenue of $970,579 for the nine months ended September 30, compared to $475,640 for the same period in 2022. An increase of over 104%.

- Net earnings of $176,685 for the nine months ended September 30, compared to a net loss of $175,468 in the same period in 2022.

- Diluted earnings per ordinary share of $1.81 for the nine months ended September 30, compared to a loss of $2.26 per share for the same period in 2022.

Cargojet Inc.

All currency listed in millions of Canadian dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 7, 2023

- Revenue of $214.0 for the three months ended September 30, compared to $232.7 for the same period in 2022. A decrease of over 8%.

- Net income of $10.5 for the three months ended September 30, compared to net income of $83.4 in the same period in 2022.

- Diluted earnings per ordinary share of $0.61 for the three months ended September 30, compared to earnings of $4.33 per share for the same period in 2022.

- Revenue of $655.6 for the nine months ended September 30, compared to $712.9 for the same period in 2022. A decrease of over 8%.

- Net earnings of $72.2 for the nine months ended September 30, compared to net earnings of $187.8 in the same period in 2022.

- Diluted earnings per ordinary share of $3.99 for the nine months ended September 30, compared to earnings of $9.82 per share for the same period in 2022.

Datadog, Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 7, 2023

- Revenue of 547,536 for the three months ended September 30, compared to $436,533 for the same period in 2022. An increase of over 25%.

- Net income of $22,630 for the three months ended September 30, compared to a net loss of $25,985 in the same period in 2022.

- Diluted earnings per ordinary share of $0.06 for the three months ended September 30, compared to a loss of $0.08 per share for the same period in 2022.

- Revenue of $1,538,710 for the nine months ended September 30, compared to $1,205,701 for the same period in 2022. An increase of almost 28%.

- Net loss of $5,425 for the nine months ended September 30, compared to a net loss of $21,126 in the same period in 2022.

- Diluted loss per ordinary share of $0.02 for the nine months ended September 30, compared to a loss of $0.07 per share for the same period in 2022.

Progeny, Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 7, 2023

- Revenue of $280,891 for the three months ended September 30, compared to $205,371 for the same period in 2022. An increase of almost 37%.

- Net income of $15,898 for the three months ended September 30, compared to net income of $13,211 in the same period in 2022.

- Diluted earnings per ordinary share of $0.16 for the three months ended September 30, compared to earnings of $0.13 per share for the same period in 2022.

- Revenue of $818,658 for the nine months ended September 30, compared to $572,592 for the same period in 2022. An increase of almost 43%.

- Net earnings of $48,567 for the nine months ended September 30, compared to net earnings of $26,950 in the same period in 2022.

- Diluted earnings per ordinary share of $0.48 for the nine months ended September 30, compared to earnings of $0.27 per share for the same period in 2022.

Rivian Automotive, Inc.

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 7, 2023

- Revenue of $1,337 for the three months ended September 30, compared to $536 for the same period in 2022. An increase of almost 150%.

- Net loss of $1,440 for the three months ended September 30, compared to a net loss of $1,774 in the same period in 2022.

- Diluted loss per ordinary share of $1.44 for the three months ended September 30, compared to a loss of $1.88 per share for the same period in 2022.

- Revenue of $3,119 for the nine months ended September 30, compared to $995 for the same period in 2022. An increase of over 213%.

- Net loss of $3,911 for the nine months ended September 30, compared to a net loss of $5,029 in the same period in 2022.

- Diluted loss per ordinary share of $4.15 for the nine months ended September 30, compared to a loss of $5.53 per share for the same period in 2022.

Marqeta, Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 7, 2023

- Revenue of $108,891 for the three months ended September 30, compared to $191,621 for the same period in 2022. A decrease of almost 43%.

- Net loss of $54,990 for the three months ended September 30, compared to a net loss of $53,168 in the same period in 2022.

- Diluted loss per ordinary share of $0.10 for the three months ended September 30, compared to a loss of $0.10 per share for the same period in 2022.

- Revenue of $557,349 for the nine months ended September 30, compared to $544,401 for the same period in 2022. An increase of over 2%.

- Net loss of $182,587 for the nine months ended September 30, compared to net earnings of $158,454 in the same period in 2022.

- Diluted loss per ordinary share of $0.34 for the nine months ended September 30, compared to a loss of $0.29 per share for the same period in 2022.

Magnite, Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 8, 2023

- Revenue of $150,085 for the three months ended September 30, compared to $145,815 for the same period in 2022. An increase of almost 3%.

- Net loss of $17,477 for the three months ended September 30, compared to a net loss of $24,391 in the same period in 2022.

- Diluted loss per ordinary share of $0.13 for the three months ended September 30, compared to a loss of $0.18 per share for the same period in 2022.

- Revenue of $432,778 for the nine months ended September 30, compared to $401,670 for the same period in 2022. An increase of almost 8%.

- Net loss of $190,098 for the nine months ended September 30, compared to a net loss of $93,938 in the same period in 2022.

- Diluted loss per ordinary share of $1.40 for the nine months ended September 30, compared to a loss of $0.71 per share for the same period in 2022.

Nuvei Corporation

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 8, 2023

- Revenue of $304,852 for the three months ended September 30, compared to $197,146 for the same period in 2022. An increase of almost 55%.

- Net loss of $18,120 for the three months ended September 30, compared to net income of $13,006 in the same period in 2022.

- Diluted loss per ordinary share of $0.14 for the three months ended September 30, compared to earnings of $0.08 per share for the same period in 2022.

- Revenue of $868,376 for the nine months ended September 30, compared to $622,984 for the same period in 2022. An increase of over 39%.

- Net loss of $14,792 for the nine months ended September 30, compared to net earnings of $52,603 in the same period in 2022.

- Diluted loss per ordinary share of $0.14 for the nine months ended September 30, compared to earnings of $0.34 per share for the same period in 2022.

kneat.com, inc.

All currency listed in thousands of Canadian dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 8, 2023

- Revenue of $8,405,262 for the three months ended September 30, compared to $5,751,558 for the same period in 2022. An increase of over 46%.

- Net loss of $3,591,428 for the three months ended September 30, compared to a net loss of $2,546,960 in the same period in 2022.

- Diluted loss per ordinary share of $0.05 for the three months ended September 30, compared to a loss of $0.03 per share for the same period in 2022.

- Revenue of $24,409,409 for the nine months ended September 30, compared to $16,449,162 for the same period in 2022. An increase of over 48%.

- Net loss of $11,464,497 for the nine months ended September 30, compared to a net loss of $9,607,108 in the same period in 2022.

- Diluted loss per ordinary share of $0.15 for the nine months ended September 30, compared to a loss of $0.12 per share for the same period in 2022.

Copperleaf Technologies Inc.

All currency listed in thousands of Canadian dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 8, 2023

- Revenue of $19,888 for the three months ended September 30, compared to $18,061 for the same period in 2022. An increase of over 10%.

- Net loss of $5,237 for the three months ended September 30, compared to a net loss of $7,502 in the same period in 2022.

- Diluted loss per ordinary share of $0.07 for the three months ended September 30, compared to a loss of $0.11 per share for the same period in 2022.

- Revenue of $58,358 for the nine months ended September 30, compared to $54,214 for the same period in 2022. An increase of almost 8%.

- Net loss of $29,633 for the nine months ended September 30, compared to a net loss of $25,895 in the same period in 2022.

- Diluted loss per ordinary share of $0.41 for the nine months ended September 30, compared to a loss of $0.37 per share for the same period in 2022.

Crew Energy Inc.

All currency listed in thousands of Canadian dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 8, 2023

- Revenue of $70,317 for the three months ended September 30, compared to $132,950 for the same period in 2022. A decrease of over 47%.

- Net income of $4,878 for the three months ended September 30, compared to net income of $105,658 in the same period in 2022.

- Diluted earnings per ordinary share of $0.03 for the three months ended September 30, compared to earnings of $0.65 per share for the same period in 2022.

- Revenue of $237,624 for the nine months ended September 30, compared to $461,621 for the same period in 2022. An increase of over 48%.

- Net income of $79,961 for the nine months ended September 30, compared to net income of $192,976 in the same period in 2022.

- Diluted earnings per ordinary share of $0.49 for the nine months ended September 30, compared to earnings of $1.19 per share for the same period in 2022.

Trade Desk, Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 9, 2023

- Revenue of $493,266 for the three months ended September 30, compared to $394,773 for the same period in 2022. An increase of almost 25%.

- Net income of $39,352 for the three months ended September 30, compared to net income of $15,869 in the same period in 2022.

- Diluted earnings per ordinary share of $0.08 for the three months ended September 30, compared to earnings of $0.03 per share for the same period in 2022.

- Revenue of $1,340,323 for the nine months ended September 30, compared to $1,087,058 for the same period in 2022. An increase of over 23%.

- Net earnings of $81,617 for the nine months ended September 30, compared to a net loss of $17,802 in the same period in 2022.

- Diluted earnings per ordinary share of $0.16 for the nine months ended September 30, compared to a loss of $0.04 per share for the same period in 2022.

Navitas Semiconductor Corporation

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 9, 2023

- Revenue of $21,978 for the three months ended September 30, compared to $10,243 for the same period in 2022. An increase of almost 115%.

- Net income of $7,519 for the three months ended September 30, compared to a net loss of $32,828 in the same period in 2022.

- Diluted earnings per ordinary share of $0.04 for the three months ended September 30, compared to a loss of $0.24 per share for the same period in 2022.

- Revenue of $53,399 for the nine months ended September 30, compared to $25,594 for the same period in 2022. An increase of over 108%.

- Net loss of $112,855 for the nine months ended September 30, compared to net earnings of $81,039 in the same period in 2022.

- Diluted loss per ordinary share of $0.68 for the nine months ended September 30, compared to earnings of $0.58 per share for the same period in 2022.

indie Semiconductor, Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 9, 2023

- Revenue of $60,476 for the three months ended September 30, compared to $30,016 for the same period in 2022. An increase of over 101%.

- Net loss of $18,677 for the three months ended September 30, compared to a net loss of $45,432 in the same period in 2022.

- Diluted loss per ordinary share of $0.12 for the three months ended September 30, compared to a loss of $0.31 per share for the same period in 2022.

- Revenue of $153,036 for the nine months ended September 30, compared to $77,770 for the same period in 2022. An increase of almost 97%.

- Net loss of $114,206 for the nine months ended September 30, compared to a net loss of $37,030 in the same period in 2022.

- Diluted loss per ordinary share of $0.73 for the nine months ended September 30, compared to a loss of $0.27 per share for the same period in 2022.

GDI Integrated Facility Services Inc.

All currency listed in millions of Canadian dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 9, 2023

- Revenue of $615 for the three months ended September 30, compared to $563 for the same period in 2022. An increase of over 9%.

- Net income of $8 for the three months ended September 30, compared to net income of $11 in the same period in 2022.

- Diluted earnings per ordinary share of $0.35 for the three months ended September 30, compared to earnings of $0.44 per share for the same period in 2022.

- Revenue of $1,815 for the nine months ended September 30, compared to $1,584 for the same period in 2022. An increase of almost 16%.

- Net earnings of $13 for the nine months ended September 30, compared to net earnings of $27 in the same period in 2022.

- Diluted earnings per ordinary share of $0.54 for the nine months ended September 30, compared to earnings of $1.13 per share for the same period in 2022.

Unity Software Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 9, 2023

- Revenue of $544,210 for the three months ended September 30, compared to $322,881 for the same period in 2022. An increase of over 68%.

- Net loss of $125,310 for the three months ended September 30, compared to a net loss of $250,021 in the same period in 2022.

- Diluted loss per ordinary share of $0.32 for the three months ended September 30, compared to a loss of $0.84 per share for the same period in 2022.

- Revenue of $1,578,049 for the nine months ended September 30, compared to $940,050 for the same period in 2022. An increase of almost 68%.

- Net loss of $572,337 for the nine months ended September 30, compared to a net loss of $631,734 in the same period in 2022.

- Diluted loss per ordinary share of $1.49 for the nine months ended September 30, compared to a loss of $2.13 per share for the same period in 2022.

Docebo Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 9, 2023

- Revenue of $46,506 for the three months ended September 30, compared to $36,966 for the same period in 2022. An increase of almost 26%.

- Net income of $4,047 for the three months ended September 30, compared to net income of $10,274 in the same period in 2022.

- Diluted earnings per ordinary share of $0.12 for the three months ended September 30, compared to earnings of $0.30 per share for the same period in 2022.

- Revenue of $131,559 for the nine months ended September 30, compared to $103,957 for the same period in 2022. An increase of over 26%.

- Net loss of $382 for the nine months ended September 30, compared to net earnings of $5,418 in the same period in 2022.

- Diluted loss per ordinary share of $0.01 for the nine months ended September 30, compared to earnings of $0.16 per share for the same period in 2022.

Brookfield Reinsurance

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 9, 2023

- Revenue of $1,450 for the three months ended September 30, compared to $1,376 for the same period in 2022. An increase of over 5%.

- Net income of $77 for the three months ended September 30, compared to net income of $139 in the same period in 2022.

- Diluted earnings per ordinary share of $0.07 for the three months ended September 30, compared to earnings of $0.14 per share for the same period in 2022.

- Revenue of $4,963 for the nine months ended September 30, compared to $2,934 for the same period in 2022. An increase of over 69%.

- Net earnings of $344 for the nine months ended September 30, compared to net earnings of $320 in the same period in 2022.

- Diluted earnings per ordinary share of $0.21 for the nine months ended September 30, compared to earnings of $0.42 per share for the same period in 2022.

Algonquin Power & Utilities Corp.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 10, 2023

- Revenue of $624,738 for the three months ended September 30, compared to $664,440 for the same period in 2022. A decrease of almost 6%.

- Net loss of $187,326 for the three months ended September 30, compared to a net loss of $207,335 in the same period in 2022.

- Diluted loss per ordinary share of $0.26 for the three months ended September 30, compared to a loss of $0.29 per share for the same period in 2022.

- Revenue of $2,031,236 for the nine months ended September 30, compared to $2,017,063 for the same period in 2022. An increase of almost 1%.

- Net loss of $200,037 for the nine months ended September 30, compared to a net loss of $217,059 in the same period in 2022.

- Diluted loss per ordinary share of $0.24 for the nine months ended September 30, compared to a loss of $0.21 per share for the same period in 2022.

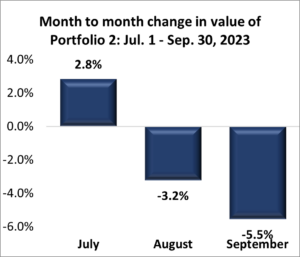

Portfolio 2

Portfolio 2 for the week ended November 10, 2023: UP ![]()

- Walt Disney Corporation has hired Hugh Johnston as its latest Chief Financial Officer. Mr. Johnston was previously PepsiCo’s (NYSE: PEP) CFO. He will start at Disney in early December.

- MongoDB announced they were partnering with Amazon’s Amazon Web Services (AWS) to enhance and train AWS’s CodeWhisperer, an artificial intelligence (AI) coding writing companion. This will allow AWS customers to accelerate application development.

- Guardant Health announced their Chief Operating Officer has resigned, effective November 10. However, she will remain with the company until December 1 to help with the transition.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Bank of Nova Scotia (TSE: BNS) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

Brookfield Infrastructure Partners L.P.

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 1, 2023

- Revenue of $4,487 for the three months ended September 30, compared to $3,627 for the same period in 2022. An increase of almost 24%.

- Net income of $256 for the three months ended September 30, compared to net income of $361 in the same period in 2022.

- Diluted earnings per ordinary share of $0.03 for the three months ended September 30, compared to earnings of $0.05 per share for the same period in 2022.

- Revenue of $12,961 for the nine months ended September 30, compared to $10,719 for the same period in 2022. An increase of almost 21%.

- Net earnings of $1,172 for the nine months ended September 30, compared to net earnings of $1,080 in the same period in 2022.

- Diluted earnings per ordinary share of $0.34 for the nine months ended September 30, compared to earnings of $0.17 per share for the same period in 2022.

Guardant Health, Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 6, 2023

- Revenue of $143,030 for the three months ended September 30, compared to $117,404 for the same period in 2022. An increase of almost 22%.

- Net loss of $86,102 for the three months ended September 30, compared to a net loss of $161,994 in the same period in 2022.

- Diluted loss per ordinary share of $0.73 for the three months ended September 30, compared to a loss of $1.58 per share for the same period in 2022.

- Revenue of $408,894 for the nine months ended September 30, compared to $322,647 for the same period in 2022. An increase of almost 27%.

- Net loss of $292,406 for the nine months ended September 30, compared to a net loss of $514,654 in the same period in 2022.

- Diluted loss per ordinary share of $2.66 for the nine months ended September 30, compared to a loss of $5.04 per share for the same period in 2022.

iA Financial Corporation Inc.

All currency listed in millions of Canadian dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 7, 2023

- Revenue of $1,458 for the three months ended September 30, compared to $1,275 for the same period in 2022. An increase of over 14%.

- Net income of $56 for the three months ended September 30, compared to net income of $4 in the same period in 2022.

- Diluted earnings per ordinary share of $0.65 for the three months ended September 30, compared to earnings of $0.01 per share for the same period in 2022.

- Revenue of $4,193 for the nine months ended September 30, compared to $3,755 for the same period in 2022. An increase of almost 12%.

- Net earnings of $533 for the nine months ended September 30, compared to net earnings of $142 in the same period in 2022.

- Diluted earnings per ordinary share of $5.04 for the nine months ended September 30, compared to earnings of $1.19 per share for the same period in 2022.

TC Energy Corporation

All currency listed in millions of Canadian dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 8, 2023

- Revenue of $3,940 for the three months ended September 30, compared to $3,799 for the same period in 2022. An increase of almost 4%.

- Net loss of $173 for the three months ended September 30, compared to net income of $862 in the same period in 2022.

- Diluted loss per ordinary share of $0.19 for the three months ended September 30, compared to earnings of $0.84 per share for the same period in 2022.

- Revenue of $3,829 for the nine months ended September 30, compared to $3,497 for the same period in 2022. An increase of over 9%.

- Net earnings of $1,366 for the nine months ended September 30, compared to net earnings of $2,088 in the same period in 2022.

- Diluted earnings per ordinary share of $1.33 for the nine months ended September 30, compared to earnings of $2.11 per share for the same period in 2022.

Chorus Aviation Inc.

All currency listed in thousands of Canadian dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 8, 2023

- Revenue of $447,596 for the three months ended September 30, compared to $421,326 for the same period in 2022. An increase of over 6%.

- Net income of $17,148 for the three months ended September 30, compared to net income of $23,561 in the same period in 2022.

- Diluted earnings per ordinary share of $0.04 for the three months ended September 30, compared to earnings of $0.06 per share for the same period in 2022.

- Revenue of $1,259,623 for the nine months ended September 30, compared to $1,156,049 for the same period in 2022. An increase of almost 9%.

- Net earnings of $69,485 for the nine months ended September 30, compared to net earnings of $6,065 in the same period in 2022.

- Diluted earnings per ordinary share of $0.20 for the nine months ended September 30, compared to a loss of $0.05 per share for the same period in 2022.

Kneat.com

See report under Portfolio 1.

The Walt Disney Company

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their fourth quarter 2023 financial results on November 8, 2023

- Revenue of $21,241 for the three months ended September 30, compared to $20,150 for the same period in 2022. An increase of over 5%.

- Net income of $694 for the three months ended September 30, compared to net income of $254 in the same period in 2022.

- Diluted earnings per ordinary share of $0.14 for the three months ended September 30, compared to earnings of $0.09 per share for the same period in 2022.

- Revenue of $88,898 for the nine months ended September 30, compared to $82,722 for the same period in 2022. An increase of almost 5%.

- Net earnings of $2,354 for the nine months ended September 30, compared to net earnings of $3,145 in the same period in 2022.

- Diluted earnings per ordinary share of $1.29 for the nine months ended September 30, compared to earnings of $1.72 per share for the same period in 2022.

Take-Two Interactive Software, Inc.

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their second quarter 2023 financial results on November 8, 2023

- Revenue of $1,299.2 for the three months ended September 30, compared to $1,393.5 for the same period in 2022. A decrease of almost 7%.

- Net loss of $543.6 for the three months ended September 30, compared to a net loss of $257.0 in the same period in 2022.

- Diluted loss per ordinary share of $3.20 for the three months ended September 30, compared to a loss of $1.54 per share for the same period in 2022.

- Revenue of $2,583.9 for the nine months ended September 30, compared to $2,495.9 for the same period in 2022. An increase of over 3%.

- Net loss of $749.6 for the nine months ended September 30, compared to a net loss of $361.0 in the same period in 2022.

- Diluted loss per ordinary share of $4.42 for the nine months ended September 30, compared to a loss of $2.38 per share for the same period in 2022.

SmartCentres Real Estate Investment Trust

All currency listed in thousands of Canadian dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 8, 2023

- Revenue of $206,016 for the three months ended September 30, compared to $196,962 for the same period in 2022. An increase of almost 44%.

- Net income of $215,175 for the three months ended September 30, compared to net income of $3,548 in the same period in 2022.

- Revenue of $623,560 for the nine months ended September 30, compared to $598,375 for the same period in 2022. An increase of over 4%.

- Net earnings of $495,938 for the nine months ended September 30, compared to net earnings of $535,655 in the same period in 2022.

Crew Energy Inc.

See report under Portfolio 1.

Supremex Inc.

All currency listed in thousands of Canadian dollars.

Selected highlights from their third quarter 2023 financial results on November 9, 2023

- Revenue of $69,798,092 for the three months ended September 30, compared to $67,918,827 for the same period in 2022. An increase of almost 3%.

- Net income of $5,000,707 for the three months ended September 30, compared to net income of $8,110,570 in the same period in 2022.

- Diluted earnings per ordinary share of $0.19 for the three months ended September 30, compared to earnings of $0.31 per share for the same period in 2022.

- Revenue of $229,886,140 for the nine months ended September 30, compared to $193,705,893 for the same period in 2022. An increase of over 73%.

- Net earnings of $16,609,748 for the nine months ended September 30, compared to net earnings of $21,776,377 in the same period in 2022.

- Diluted earnings per ordinary share of $0.64 for the nine months ended September 30, compared to earnings of $0.83 per share for the same period in 2022.

Portfolio 3

Portfolio 3 for the week ended November 10, 2023: UP ![]()

- Microsoft (NASD: MSFT) announced the release of Call of Duty: Modern Warfare III, the first Activision title released since Microsoft’s acquisition of Activision Blizzard. The availability of this title on all major gaming platforms was one of the major roadblocks to completion of the deal. As Microsoft said, it was released on all major platforms.

- Alvopetro Energy (TSXV: ALV) announced the completion of drilling on their 183-A3 well, located on their Murucututu natural gas field, in October. The company hopes to have the well operational by the end of November.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Brookfield Asset Management ULC

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 6, 2023

- Revenue of $778 for the three months ended September 30, compared to $715 for the same period in 2022. An increase of almost 9%.

- Net income of $510 for the three months ended September 30, compared to net income of $695 in the same period in 2022.

- Diluted earnings per ordinary share of $0.31 for the three months ended September 30.

- Revenue of $2,339 for the nine months ended September 30, compared to $2,051 for the same period in 2022. An increase of over 14%.

- Net earnings of $1,606 for the nine months ended September 30, compared to net earnings of $2,252 in the same period in 2022.

- Diluted earnings per ordinary share of $089 for the nine months ended September 30.

Kneat.com

See report under Portfolio 1.

goeasy Ltd.

All currency listed in thousands of Canadian dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 7, 2023

- Revenue of $321,732 for the three months ended September 30, compared to $262,216 for the same period in 2022. An increase of almost 23%.

- Net income of $66,310 for the three months ended September 30, compared to net income of $47,189 in the same period in 2022.

- Diluted earnings per ordinary share of $3.87 for the three months ended September 30, compared to earnings of $2.86 per share for the same period in 2022.

- Revenue of $911,957 for the nine months ended September 30, compared to $746,010 for the same period in 2022. An increase of over 22%.

- Net earnings of $173,296 for the nine months ended September 30, compared to net earnings of $111,585 in the same period in 2022.

- Diluted earnings per ordinary share of $10.14 for the nine months ended September 30, compared to earnings of $6.71 per share for the same period in 2022.

Fortuna Silver Mines Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 8, 2023

- Revenue of $243,055 for the three months ended September 30, compared to $166,568 for the same period in 2022. An increase of almost 46%.

- Net income of $30,883 for the three months ended September 30, compared to a net loss of $4,126 in the same period in 2022.

- Diluted earnings per ordinary share of $0.09 for the three months ended September 30, compared to a loss of $0.01 per share for the same period in 2022.

- Revenue of $577,114 for the nine months ended September 30, compared to $516,768 for the same period in 2022. An increase of almost 12%.

- Net earnings of $46,209 for the nine months ended September 30, compared to net earnings of $24,528 in the same period in 2022.

- Diluted earnings per ordinary share of $0.14 for the nine months ended September 30, compared to earnings of $0.08 per share for the same period in 2022.

Magnite

See report under Portfolio 1.

Alvopetro Energy Ltd.

All currency listed in thousands of Canadian dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 8, 2023

- Revenue of $12,313 for the three months ended September 30, compared to $16,672 for the same period in 2022. A decrease of over 26%.

- Net income of $5,819 for the three months ended September 30, compared to net income of $8,795 in the same period in 2022.

- Diluted earnings per ordinary share of $0.15 for the three months ended September 30, compared to earnings of $0.24 per share for the same period in 2022.

- Revenue of $44,387 for the nine months ended September 30, compared to $46,431 for the same period in 2022. A decrease of over 4%.

- Net earnings of $27,873 for the nine months ended September 30, compared to net earnings of $26,541 in the same period in 2022.

- Diluted earnings per ordinary share of $0.74 for the nine months ended September 30, compared to earnings of $0.72 per share for the same period in 2022.

GDI Integrated Services

See report under Portfolio 1.

Unity Software

See report under Portfolio 1.

SmartCentres Real Estate Investment Trust

See report under Portfolio 2.

Brookfield Corporation

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 9, 2023

- Revenue of $24,441 for the three months ended September 30, compared to $23,418 for the same period in 2022. An increase of over 4%.

- Net income of $35 for the three months ended September 30, compared to net income of $716 in the same period in 2022.

- Diluted earnings per ordinary share of $0.12 for the three months ended September 30, compared to earnings of $0.24 per share for the same period in 2022.

- Revenue of $71,406 for the nine months ended September 30, compared to $68,556 for the same period in 2022. An increase of over 4%.

- Net earnings of $1,971 for the nine months ended September 30, compared to net earnings of $5,151 in the same period in 2022.

- Diluted earnings per ordinary share of $0.20 for the nine months ended September 30, compared to earnings of $1.40 per share for the same period in 2022.