This will be the final ‘Weekly Update’ of 2023. I am sure you will miss the scintillating commentary 😊, as I take a break for the last week of the year. Do not fret, the posts will resume January 5, 2024.

This will be the final ‘Weekly Update’ of 2023. I am sure you will miss the scintillating commentary 😊, as I take a break for the last week of the year. Do not fret, the posts will resume January 5, 2024.

I would like to thank you for following along and bearing with me throughout the year. Hopefully, the 2024 markets will be more like this past year than 2022. 😊 In any event, enjoy the Christmas holiday as 2023 comes to a close and all the best in the coming year!

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, Stock market’s holiday hours …

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Bank of Canada monetary policy notes

The minutes from the last meeting of the Bank of Canada’s Governing Council meeting on December 6 revealed that officials were confident the current 5% interest rate was sufficiently high to drive inflation down to their goal of 2%. Consequently, they opted to leave the benchmark rate unchanged but expressed readiness to raise it should inflation show an upward trajectory.

During the meeting, members observed a global trend of falling inflation and slowing economic growth, with the exception of the US, which exhibited a growing economy and sustained strong consumer spending. Lower oil prices played a significant role in the falling rate of inflation, although the pace of price growth was decelerating in food and other goods, as well.

In Canada, the Council members deliberated on the stagnant domestic economy due to reduced consumer and business spending. Notably, government spending was on the rise, serving as the primary driver for third-quarter economic growth. Discussions also encompassed the slowdown in job growth, the increase in unemployment, and the deceleration of wage growth in the private sector, in contrast to the rising wage growth in the public sector. Rising wages can lead to increased demand, putting upward pressure on inflation. Additionally, they addressed the latest inflation data, indicating an ongoing decline, although housing prices, continued to rise at a pace higher than desired.

Members acknowledged that the current interest rate was exerting a slowing effect on the economy as it continued to filter through the system. They highlighted that wages were consistently increasing by 4% – 5%, a factor not conducive to lower prices and diminishing inflation.

In conclusion, the officials believed that inflation was moving in the right direction, but uncertainties remained regarding the sustainability of the downward trend in inflation. The council will reconvene in the new year, on January 24 when they will make their next interest rate announcement and publish their next quarterly Monetary Policy Report.

Consumer Price Index

Statistics Canada’s inflation report for November showed the country’s annual inflation rate, as measured by the Consumer Price Index (CPI), unexpectedly remained at 3.1% in November, the same as it was in October. Analysts had been expecting inflation to drop to 2.9%. Month-over-month, the consumer price index rose 0.1% in November, after rising 0.1% the previous month. Analysts had been expecting a drop of 0.1%.

Core CPI, a measure of inflation that excludes the volatile food and energy prices price movements, rose to 3.5% in November on the heels of a 3.4% increase in October. On a monthly basis, core CPI grew at a 0.2% pace following a 0.1% increase in October.

The primary contributor to the yearly increase was higher ‘mortgage interest costs’ (thanks to the higher interest rates) up 29.8%, while the largest drop was in ‘fuel oil and other fuels,’ down 23.6%. On a monthly perspective, the biggest price increases were seen in ‘fresh vegetables,’ up 7.4%, while the biggest drop was 15.4% in ‘traveler accommodation.’

The higher inflation numbers were not what analysts were expecting, and it is not ideal for Canadian households already contending with higher costs for essentials. The data suggests progress on reducing inflation was slowing. The persistent inflation also provided a dose of reality for investors envisioning the BoC lowering interest rates sooner rather than later. Not the best news to end the year but the BoC will continue to monitor the inflation situation closely and adjust its policies as needed to bring inflation down to their 2% target.

Gross Domestic Product

Canada’s Gross Domestic Product (GDP) for October was once again flat at 0.0%. Analysts had predicted 0.2% growth. After the GDP for September was revised downward to 0.0% from 0.1% growth, which made it three consecutive months with little to no growth. On an annual basis, GDP is up 0.9%. Based on preliminary indicators, GDP for November is expected to rise by 0.1% thanks to increases in manufacturing that were partially offset by decreases in retail trade.

On a monthly basis, goods producing industries were flat, led by the ‘Agriculture, forestry, fishing and hunting’ industry, up 1.1%, while ‘Manufacturing’ was down 0.6%. The services producing industries rose 0.1%, led by the ‘Retail trade’ industry, up 1.2%, while ‘Management of companies and enterprises’ was down 2.5%. On an annual basis, the goods producing industries were down 1.0%, with the biggest drop in ‘Agriculture, forestry, fishing and hunting,’ down 12.5%. The services producing industries overall was up 1.5%, led by ‘Public administration,’ up 3.8%, while the biggest drop was in ‘Management of companies and enterprises,’ down 35.5%

As the Canadian economy continues to stutter, investors see this as support for their belief the BoC will start to lower the interest rate in the second quarter of 2024. We will get our first signs of the BoC plan for 2024 at their next meeting on January 24, 2024.

Canadian market volatility

The Canadian Volatility Index (VIXC), represented by the TSX 60 VIXI, ended the week at 9.77, slightly lower than last week’s reading of 10.35. This slight decline suggests lower level of volatility as investors remain optimistic considering the possibility that the BoC will start lowering rates to match the US Federal Reserve’s projected interest rate cuts in 2024.

The VIXC’s “high” and “low” volatility thresholds are generally defined as readings above 20 and below 20, respectively. Therefore, the current level of 9.77 indicates a relatively calm market environment.

Retail Sales

Canadian retail sales rose 0.7% in October after climbing 0.6% in September. Analysts had been expecting a monthly increase of 0.8%. ‘Clothing, clothing accessories, shoes, jewellery, luggage, and leather goods retailers’ saw the biggest increase, up 2.4%, while sales at ‘Gasoline stations and fuel vendors’ suffered the biggest decline, dropping 3.1%. Year over year, retail sales was up 2.2%. Sales of ‘motor vehicles and parts,’ up 7.8%, more than offset the drop in sales at ‘gas stations and fuel vendors,’ down 10.8%.

After 2 straight months of declines, core retail sales (excludes sales at ‘gasoline stations and fuel vendors’, and ‘motor vehicle and parts dealers’) was up 1.2% for October. Annually, core retail sales were up 2.3%. ‘General merchandise retailers’ were the big winners, up 4.7%, while the biggest drop was in ‘Building material and garden equipment and supplies dealers,’ down 6.3%.

However, early indications suggest that retail sales for November were flat, potentially hindering fourth quarter economic growth and dampening consumer spending power. This could be a further challenge for Canadians already facing rising costs of living.

Budget update

The latest update to the Canadian budget for the period April through October showed a C$15.13 billion deficit, a significant shift compared to the C$174 million surplus for the same period in 2022. Revenues increased 1.2%, however, that was offset increased government spending and higher interest rates due to rising borrowing costs contributed to the larger deficit. On a monthly basis, the deficit for October was C$6.96 billion compared to C$1.9 billion in 2022.

The higher deficit could potentially lead to a higher tax burden as the higher interest charges divert funds from other potential services and programs. It also raises the question of long-term sustainability of current fiscal policies. Canadians are already feeling overtaxed so the government will have to take a hard look at its expenses and where it can afford to trim expenses.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Personal Consumption Expenditures

Inflation, as measured by the Commerce Department’s Personal Consumption Expenditures (PCE) price index, fell 0.1% last month. That was the first monthly decline in the PCE price index since April 2020 and followed an unchanged reading in October. Year over year, the PCE price index increased by 2.6%, down from 2.9% in October and marking the lowest level since February 2022.

The so-called core PCE price index, PCE excluding the more volatile food and energy components, advanced 3.2% year-on-year in November, the smallest rise since April 2021, after increasing 3.4% in October. That was the fifth straight monthly decline. On a monthly basis, core PCE was up 0.1%.

The lower-than-expected inflation numbers boosted investor confidence and led to gains across various market sectors. The falling inflation numbers provide the Fed with another reason to lower the benchmark interest rate. It also indicates the Fed is making progress driving inflation down to their target of 2%, further raising hopes for a softer landing for the economy.

This latest PCE report, the Fed’s preferred measure of inflation, is good news, suggesting that their fight against inflation is making progress. While some uncertainties remain, the declining inflation trend brings optimism for a more stable economic environment and potentially better returns for investors next year.

American market volatility

Heading into the Christmas weekend, Wall Street’s “fear gauge,” the CBOE Volatility Index (VIX), rose to 13.03 at the end of the week, after registering 12.28 the previous week. The increase in the VIX suggests investors are perceiving greater uncertainty and risk in the market, potentially leading to more frequent price fluctuations and changes in investor sentiment. A plausible reason for the increase in the ‘fear gauge’ is the heightened geopolitical tensions as well as concern the markets may have gotten ahead of themselves and a pullback may be coming.

While the “fear gauge” did rise, it is still quite low and may be only a minor fluctuation.

The VIX is a measure of the market’s expectation of short-term volatility based on S&P 500 options prices.

Consumer Confidence Index

The Conference Board’s December Consumer Confidence Index (CCI) surged to 110.7, marking a five-month high, up significantly from a downwardly revised 101.0 in November. The latest reading easily surpassed analysts’ expectations of 104.0. This jump points to a substantial surge in consumer optimism towards both current and future business conditions and employment opportunities resulting from a strong labour market.

A greater number of consumers are now reporting “good” business conditions, suggesting a heightened likelihood of increased spending on major purchases like vehicles, appliances, and vacation packages. While factors like inflation and interest rates can still influence individual spending decisions, the current high level of consumer confidence bodes well for a potentially brighter economic outlook in the coming months.

Consumer Sentiment Index

The University of Michigan’s final reading of the December Consumer Sentiment Index (CSI) edged slightly higher to 69.7 from an initial reading of 69.4 in early December. On a monthly basis, the December CSI was 13.7% higher than the November reading of 61.3, and 16.6% higher than a year ago when it was 59.8.

The improved sentiment was a result of consumers seeing lower inflation, and they expect it to continue to fall over the next few years. The December increase reversed the last four months of declines. The improved sentiment may lead to increased spending by consumers which is good for the economy.

Stock market’s holiday hours

The North American stock markets will have a modified schedule next week due to the holidays. All markets will be closed on Christmas Day (December 25) and New Year’s Day (January 1, 2024). Canadian markets will also be closed on Boxing Day (December 26). Otherwise, markets are open regular hours on December 27 through December 29.

Remember, many investors, especially the big institutional investors, take time off between Christmas and New Year’s, so expect lower trading volume and potentially more price fluctuations during this time. When the big investors are away it gives us individual investors more time to play. 😊

As we conclude the last full week of trading in 2023 and prepare for Christmas long weekend holiday, let’s see what happened this past week….

Weekly Market Review

Monday: Despite Fed officials attempts to temper investor enthusiasm over the weekend, the rally continued as investors hope interest rate cuts will come sooner rather than later. Three of the four indexes ended the day higher, while the Dow Jones Industrial Average (DJIA) ended flat. Oil prices moved higher as multiple shipping lines cancelled trips through the Red Sea to avoid attacks on their ships by Yemeni Houthi rebels.

In Canada, the week got off on the right foot as the Toronto Stock Exchange Composite Index (TSX) rose on the back of higher energy prices. In trading, Energy and Consumer Cyclicals were the biggest winners, while Utilities and Healthcare sank the most.

In the US, building on seven consecutive weeks of weekly gains, the S&P 500 Index (S&P) and the Nasdaq Composite Index (Nasdaq) ended higher. Investor enthusiasm over the possibility of lower rates continues to drive the indexes higher. In trading, most of the American sectors finished higher, led by Energy and Consumer Staples. Utilities and Financials were the only sectors to end lower.

Tuesday: investors seem to have caught the Christmas spirit as they continue to push the markets higher, with all four indexes ending solidly in the green. For now, investors are ignoring warnings from the Fed that it is premature to conclude rate hikes are over. Oil prices continue to inch higher as more shipping companies are avoiding transiting the Red Sea with their cargos of oil.

In Canada, the road to lower inflation hit a pothole when the inflation rate for November unexpectedly remained unchanged, after analysts had predicted the inflation rate to drop. Despite the bump, the TSX moved higher as investors who have been sitting on cash are moving back into the stock markets. They do not want to be on the sidelines when the markets are rallying. In trading, it was a broad-based rally, led by Basic Materials (miners and fertilizer manufacturers) and Consumer Staples. The only Canadian sector to end in the red was the Technology sector.

In the US, the DJIA recorded its fifth consecutive record close, and the S&P is within 1% of its all time high. In trading, every sector ended higher, led by Basic Materials and Energy, with Telecommunications Services and Consumer Staples trailing the pack.

Wednesday: the markets took a breather, sending all indexes sharply lower to close the day. The indexes were doing fine until late in the afternoon when they each took a nosedive and fell more than 1%. After this latest mini rally, investors decided to take some money off the table.

In Canada, the BoC minutes from their December 6 monetary session showed the members are confident that interest rates are high enough to continue to bring inflation down to their 2% goal. In trading, every Canadian sector was down. Consumer Staples and Telecommunications Services were the best of a bad lot, while Basic Materials and Technology had the worst day.

In the US of A, the DJIA consecutive closing highs came to an end, the S&P came with 0.5% of its all time high before reversing course to end with its worst day since October. The DJIA and the Nasdaq’s nine day winning streaks ended with a thud. US consumer confidence came in higher than expected. In trading, all the American sectors ended in the red with Telecommunications Services and Energy dropping the least, while Consumer Cyclicals and Utilities fell the deepest into the red.

Thursday: after taking a breather yesterday, the markets bounced back to end the day solidly in the green. US economic data provided investors with confidence that the Fed could lower the US benchmark rate as early as its March meeting.

In Canada, the TSX rose on investor optimism that the central banks would start cutting interest rates by the second quarter of 2024. In trading, it was a broad-based rally with all Canadian sectors ending higher. Basic Materials and Consumer Cyclicals led the way, with Healthcare and Telecommunications Services trailing the pack.

In the US, the indexes recouped most of Wednesday’s losses as investors stepped back into the markets. Economic data showed the economy was not as strong as analysts expected. In trading, all sectors ended higher, led by Basic Materials and Consumer Cyclicals. Bringing up the rear were Utilities and Consumer Staples.

Friday: the markets ended the week going into Christmas on a high note with three of the four indexes ending in positive territory. The catalyst for today’s markets was the Fed’s preferred measure of inflation, PCE, showed inflation continued to fall in November, as both PCE and core PCE came in lower than expected. Investors see this as another sign the door is open for the Fed to start lowering the benchmark interest rate. Oil prices ended slightly lower after Angola decided to leave OPEC, enabling them to increase the production of their oil reserves.

In Canada, the TSX rode the tailwind of the US inflation good news to reach an 18-month high. In trading on Bay Street, it was a day of broad-based gains led by the Healthcare and Utilities sectors. Telecommunications Services was the only sector to end lower.

In the US, the DJIA ended the day slightly lower but not enough to prevent the index from stretching its weekly winning streak to eight weeks. The S&P and Nasdaq also notched another weekly win, to match the DJIA streak. In trading on Wall Street, gains were seen across almost all the sectors. Healthcare and Basic Materials led the gains while consumer cyclicals was the only sector to not make it into positive territory.

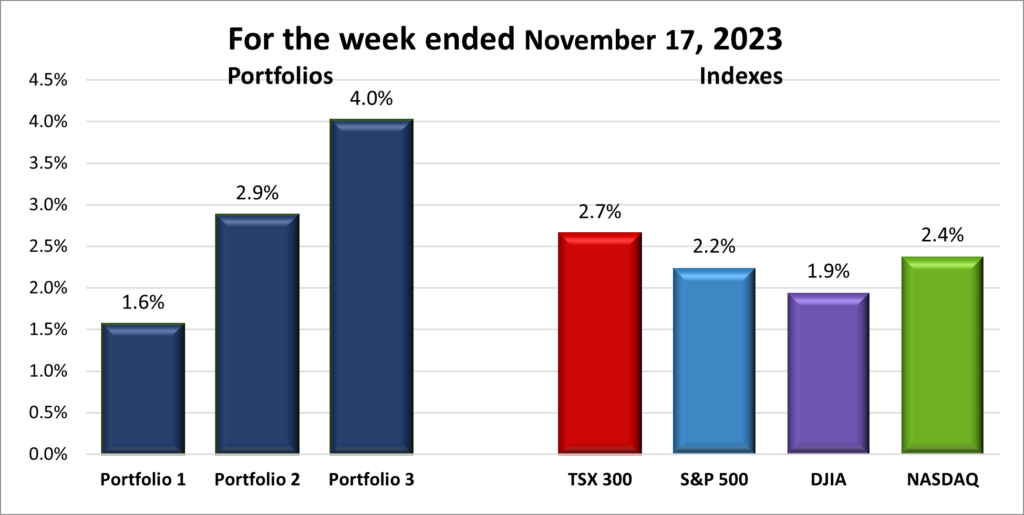

Weekly Market and Portfolio Review

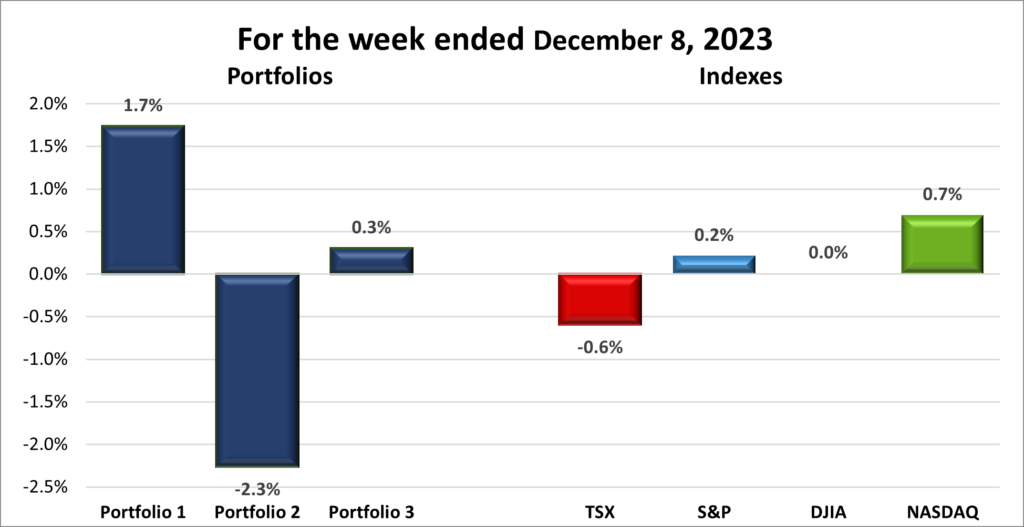

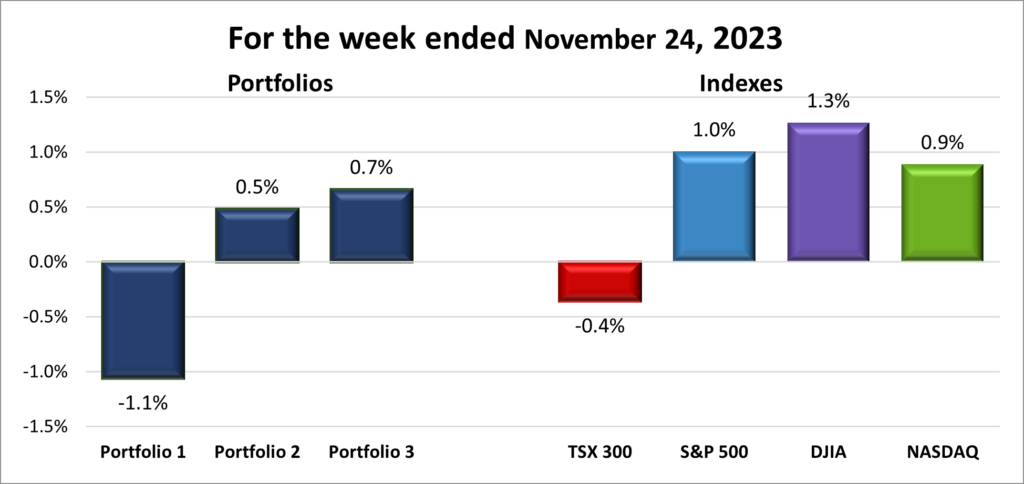

For the week, the TSX (SPTSX) surged 1.7%, the S&P 500 (SPX) rose 0.8%, the DJIA (INDU) gained 0.2% and the Nasdaq (CCMP) advanced 1.3%.

| Index | Weekly Streak |

| TSX: | 2-week winning streak |

| S&P: | 8-week winning streak |

| DJIA: | 8-week winning streak |

| Nasdaq: | 8-week winning streak |

![]() Another good week in the North American stock markets that saw all four indexes end the week higher, as shown in the chart above. Other than the Wednesday when investors took a breather, and some money off the table, the indexes moved higher every day this past week. The PCE report in the US and the CPI report in Canada showed inflation continues to fall in both countries. It is looking increasingly likely the Fed will thread the needle and bring inflation down without sending the US economy into a recession. The picture is less clear in Canada, where the latest GDP report indicates the economy has stagnated, and there has been no talk of Canada avoiding a recession.

Another good week in the North American stock markets that saw all four indexes end the week higher, as shown in the chart above. Other than the Wednesday when investors took a breather, and some money off the table, the indexes moved higher every day this past week. The PCE report in the US and the CPI report in Canada showed inflation continues to fall in both countries. It is looking increasingly likely the Fed will thread the needle and bring inflation down without sending the US economy into a recession. The picture is less clear in Canada, where the latest GDP report indicates the economy has stagnated, and there has been no talk of Canada avoiding a recession.

The rally, which started in November and has become a Santa Claus rally, continues to be driven by growing investor optimism that the Fed will start lowering the US benchmark rate in March or April. In Canada, the BoC has not signaled it has reached the end of interest rate hikes like the Fed has, however, the Canadian economy has been flat for the last three months. If the BoC wishes to avoid a recession, they will need to signal an end to rate hikes sooner rather than later.

Unlike the market rally at the start of the year which was largely driven by the Magnificent 7 companies, the current rally is characterized by the breadth of the rally which continues to expand. This broad rally is much more sustainable than the tightly focused rally at the start of the year and is better for us investors in the long run. 😊

![]()

![]() It was a mixed bag for the three portfolios, with Portfolios 1 and 2 gaining ground, while Portfolio 2 lost ground, as shown in the chart below. Fortunately, the gains of Portfolio 3 were greater than the losses in Portfolio 2, pushing the overall value of the portfolios higher.

It was a mixed bag for the three portfolios, with Portfolios 1 and 2 gaining ground, while Portfolio 2 lost ground, as shown in the chart below. Fortunately, the gains of Portfolio 3 were greater than the losses in Portfolio 2, pushing the overall value of the portfolios higher.

Portfolio 1 was barely higher due to most of the companies share prices were just above or just below the price they started the week. There were two notable performers, gains, or losses greater than 10%. Fortunately, both Progeny (NASD: PGNY) and Nuvei (TSE: NVEI) were on the positive side and able to offset the losses.

This week is a strange one for Portfolio 2 as there is no obvious reason for the decline. There were no notable weekly winners or losers. More than half the companies ended the week higher. The only thing I can see is that Telus (TSE: T), one of the larger holdings, ended approximately 2% lower on concerns of its debt and the higher interest payments caused by the higher interest rate, dragging the overall portfolio down.

Finally, Portfolio 3 had no big winners or losers. All the companies were either slightly higher or slightly lower. Fortunately, there were almost twice as many companies that ended higher than lower.

All in all, not a bad week. All the portfolios cannot end higher every week. Hopefully, the Santa Claus rally will continue into the last week of the year and will deliver us a present of all indexes and portfolios solidly in the green for the week. One can hope. 😊

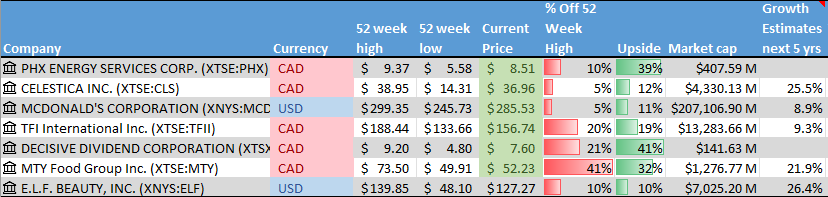

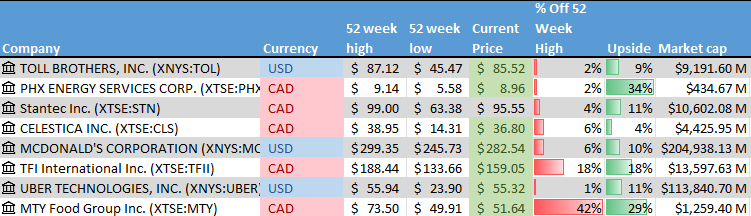

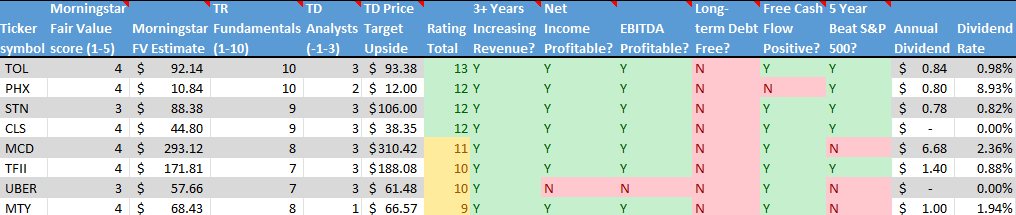

Companies on the Radar

I was a little busy the week before Christmas, so no new companies came on my Radar. However, I was able get an early Christmas present with an investment in Decisive Dividend (TSXV: DE). 😊

I was a little busy the week before Christmas, so no new companies came on my Radar. However, I was able get an early Christmas present with an investment in Decisive Dividend (TSXV: DE). 😊

As for the four remaining companies on the radar list, I am hoping to have some time over the coming week to finally get a chance to dig a little deeper into each of these companies.

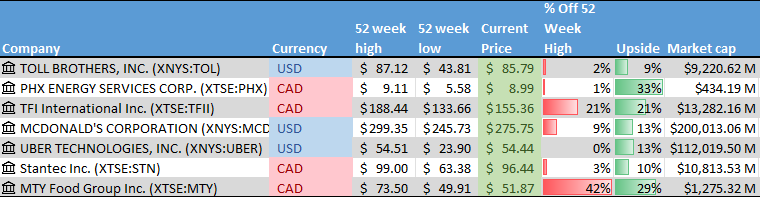

- PHX Energy Services (TSE: PHX) a small Canadian company that provides drilling technology and services to oil and natural gas exploration companies throughout the world, but mainly in North America.

- McDonald’s (NYSE: MCD), the large cap American fast-food chain.

- Celestica Inc. (TSE: CLS), a medium sized Canadian company that manufactures electronic products and provides supply chain services to companies around the world.

- TFI International Inc. (TSE: TFII), a mid-sized Canadian transportation and logistics company operating across North America.

The Radar Check was last updated December 22, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended December 22, 2023: UP ![]()

- Apple (NASD: AAPL) paused sales of its Series 9 and Ultra 2 smartwatches to comply with a ruling from the US International Trade Commission (ITC) that the company infringed on the patent of a medical technology company. The decision is currently being reviewed but Apple decided to stop sales in the event the ruling is not overturned.

- Amazon (NASD: AMZN) is considering making an investment in US regional sports network Diamond Sports Group. In return for the investment (cash), Amazon would receive a multiyear streaming partnership with Diamond and become the streaming home for all of Diamond’s game. Diamond currently holds the broadcast rights for more than forty professional teams throughout the NHL, MLB, and NFL. This would provide Amazon with a major inroad into streaming sports games.

- Alphabet’s (NASD: GOOGL) has been accused of overcharging users through unlawful restrictions on apps available on Android devices and charging unnecessary fees for in-app transactions. Google must pay US$700 million into a settlement fund.

Google has been fined US$50.4 million by a Russian court for failing to remove ‘fake’ information about the Russian invasion of Ukraine. - Tesla (NASD: TSLA) is being investigated by both Sweden’s and Norway’s respective traffic safety regulators over concerns about suspension failures.

In a separate situation, Tesla has recalled approximately 140,000 Model S and Model X cars due to door locks unlocking during a crash.

Activity

Bought: Decisive Dividend. About ten years ago I was talking with a friend about building a business through acquiring small, family-owned businesses as the founders retired. While doing my due diligence on Decisive Dividend, I quickly discovered that this company was doing something similar to which I had considered many years ago, so it resonated with me.

The two company founders are still on the Board of Directors, with one serving as the Chair. Insiders own approximately 10% of the shares outstanding so their interests are aligned with shareholders. The company’s purpose is to be the “sought-out choice for exiting legacy-minded business owners, while supporting the long-term success of the businesses acquired.” They want the companies they acquire to continue to succeed rather than to absorb them or break them up.

Financially, the company has growing revenues, net income, free cash flow and earnings per share. Long term debt is growing but I expect that from a company that grows through acquisition. It is paying a monthly dividend of over 6%. Not bad for a small company with lots of room to grow. 😊

I see the key considerations as: the company incurs too much debt; there is turnover in management; or the company acquires a business that is a poor fit. The company recently refreshed its upper management ranks with experienced personal and the company seems to have a disciplined approach to the companies it acquires so I do not think these are big risks.

Overall, I like their strategy of growth through acquiring companies whose owners come to them seeking to be acquired. As well, the company is part of the Industrials sector, providing some diversity to a technology heavy portfolio. I feel the risk is low, and getting in early on this small, growing company is worth the risk.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended December 22, 2023: DOWN ![]()

- The Bank of Nova Scotia (TSE: BNS) is reducing its efforts in South America to concentrate on North America’s US$1.6 trillion in trade. BNS is betting the Mexican market will give it an edge over other Canadian banks by offering end to end financing through Canada, the US and Mexico.

- Guardant Health (NASD: GH) announced their Shield(TM) blood test which screens for colorectal cancer is scheduled to be reviewed by the US Food and Drug Administration.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSE: DIR.UN) DRIP

Alimentation Couche-Tard Inc (TSE: ATD)

Supremex Inc (TSE: SXP)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week, except for per share data.

Portfolio 3

Portfolio 3 for the week ended December 22, 2023: UP ![]()

- Brookfield Corporation (TSE: BN) is looking to sell US$1.64 billion of its renewable energy assets. Brookfield is working with two other companies to sell its wind and photovoltaic plants in Portugal and Spain.

- Microsoft (NASD: MSFT) and OpenAI are being sued by a group of nonfiction authors. The writers claim these companies infringed on their copyright by using their books to train OpenAI’s GPT large language models.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.

The US Federal Reserve just gave the markets the gift they have been waiting for: potential cuts to the US interest rate next year! That was enough to get the bulls attention. Investors are cheering, confidence is surging, and it might just be the start of the Santa Claus Rally. Let us dive into what the Fed’s signal means for the portfolios and whether this means we are officially in for a holly jolly market ride.

The US Federal Reserve just gave the markets the gift they have been waiting for: potential cuts to the US interest rate next year! That was enough to get the bulls attention. Investors are cheering, confidence is surging, and it might just be the start of the Santa Claus Rally. Let us dive into what the Fed’s signal means for the portfolios and whether this means we are officially in for a holly jolly market ride.