Items that may only interest or educate me ….

Canadian Economic news, US Economic news, …

Canadian Economic news

This week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate:

International trade balance

The Canadian international trade balance for August was a surprising C$718 million trade surplus, a significant contrast to the C$437 million deficit recorded in July, defying analysts’ projection of a C$1.5 billion deficit. This marked the first surplus since April. Both exports and imports surged, up 5.7% and 3.8% respectively, thanks to a the end of the labour strike on Canada’s west coast. However, on an annual basis, exports and imports were down 1% and 2.3%.

Exports posted their largest increase since October 2021, with ‘Metal and non-metallic mineral products’ posting a substantial gain in August, soaring by 29%. Exports also received a bump from higher oil prices during the quarter. Year over year, ‘motor vehicles and parts’ posted a significant gain of 29.1%. Conversely, the ‘Aircraft and other transportation equipment and parts’ sector saw a sharp monthly decline of 26.1%. ‘Metal ores and non-metallic minerals’ recorded a significant year-over-year drop at 31.3%.

On the import side, ‘Metal ores and non-metallic minerals’ recorded the largest increase in August, rising by 13.6%, while ‘Aircraft and other transportation equipment and parts’ suffered the largest decline. Yearly statistics showed ‘Motor vehicles and parts’ with a gain of 14.7%, whereas ‘Energy products’ experienced a decline of 18.7%.

When a country exports more than it imports, it can indicate economic health. This surplus can instill market optimism and boost investor confidence, and drive growth in sectors benefiting from increased exports.

Labour Force Survey

The Labour Force Survey for September showed Canada added 64,000 jobs in September, three times analysts’ expectations of 20,000 new jobs. The blow out jobs report follows a gain of 40,000 in August. The unemployment rate remained at 5.5% for the third straight month. Finally, wages rose by 5.0% in September, which is the highest rate of wage growth in decades. This follows wage gains of 4.9% in August and 5.0% in July.

The Canadian economy appears to be very strong. However, with the number of jobs soaring, a stable unemployment rate, and wages continuing to climb, the likelihood increases that the BoC will increase Canada’s benchmark rate. The strong jobs report and the high rate of wage growth are likely to put further upward pressure on inflation, so the BoC is inclined to continue raising interest rates in an effort to cool the economy and bring inflation under control.

Canadian market volatility

The Canadian Volatility Index (VIXC), as measured by the TSX 60 VIXC, ended the week at 11.27, suggesting low market volatility and relatively calm investor sentiment in the Canadian stock market. This could indicate a period of stability, potentially encouraging investment in equities.

US Economic news

This week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Jobs reports

There were three main job reports this week: the Labor Department’s Job Openings and Labor Turnover Survey (JOLTS), followed by ADP’s private payrolls report, and finally, the Labor Department’s Employment Situation Summary (ESS).

First up, the Labor Department’s JOLTS for August reported job openings unexpectedly jumped higher to 9.61 million in August, up significantly from July’s 8.92 million openings in July. Analysts had predicted job openings for September would come in significantly lower at 8.80 million. Year-over-year, the number of openings was lower than the 10,198 openings in August 2022.

This report is likely to put upward pressure on inflation and give the Fed reason to increase the benchmark interest rate.

Next there was the ADP National Employment report that showed private payrolls rose by 89,000 in September, compared to an increase of 180,000 in August. The lower than-expected data was the slowest level of job growth since 2021. The data shows the pace in job growth is slowing, as well as a slowdown in wage growth.

The increase in openings suggests the labour market has gone from tight to too tight, likely putting upward pressure on inflation. However, the ADP report indicating slowing jobs and wage growth contrasts sharply with the JOLTS data. Fortunately, we have a tie breaker in the third labour report of the week, the ESS.

The Labor Department’s ESS for September revealed that non-farm payrolls surged by 336,000 in September, well above August’s 187,000 increase, and the average gain of 267,000 over the previous twelve months. It was also double analysts’ expectations of 170,000. The unemployment rate maintained a rate of 3.8% last month, the same as in August. Wage growth slowed but still rose 0.2% in September, and 4.2% on an annual basis.

Well, the ESS data seems an emphatic vote for a strong economy and corroborates the findings of the JOLTS report. The Fed has raised rates, inflation is coming down, yet the economy continues to run smoothly. The surprising strength of the job market indicates companies are confident about their sales prospects and is good news for employees. Plus, wages still continue to grow, albeit at a slower pace. At the same time, the labour market’s strength complicates the Fed’s efforts to combat inflation. And that is the downside, since the Fed may see this data as justification to raise rates again.

American market volatility

During the week, the CBOE Volatility Index (VIX) reached 20.49, its highest reading since March when the mid size regional bank crisis hit. However, by the end of the week, after all the job-related reports, the VIX had settled down to 17.45. Earlier in the week investors were concerned about higher for longer interest rates. However, the strong job-related reports helped to reassure investors and calm market volatility.

The big news items this past week were the surprisingly strong job reports in Canada and the US, but there were other items that moved the markets. Let’s see what else moved the markets this past week….

Weekly Market Review

Monday: The markets got off to a mixed start this week with the Toronto Stock Exchange Composite Index (TSX) and the Dow Jones Industrial Average (DJIA) ending lower, the S&P 500 Index (S&P), was essentially flat, while the Nasdaq Composite Index (Nasdaq) ended higher. Comments from various Fed officials suggested that interest rates will need to remain high, the only question was for how long. As well, one Fed member went further and reiterated a call for multiple additional rate hikes. Ouch!

In Canada, last weeks weak Gross Domestic Product (GDP) data, suggesting a recession is coming, combined with lower energy and commodity prices pushed the TSX sharply lower. In trading, Consumer Staples was the only Canadian sector to gain ground. The Telecommunications Services and Utilities sectors dropped the furthest.

In the US, US government bond yields increased after a deal was reached to avoid a government shutdown. The higher yields led many investors to move into less risky government bonds. Despite the fear of higher interest rates, the Technology sector still managed to perform better than the rest of the market. In trading, Technology was the only American sector to post a gain, while Utilities and Energy posted the biggest losses.

Tuesday: Hawkish comments from various Fed officials sent all four indexes sharply lower. Yesterday’s comments from Fed officials have reinforced their higher rates for longer sentiment, sending investors into US government bonds, where the 10-year yield on Treasury bonds reached a 16 year high.

In Canada, concerns about higher interest rates caused investors to flee the TSX, causing it to hit its lowest point since October 22, 2022. A struggling Chinese economy is also dragging down commodity prices associated with the Basic Materials sector (miners and fertilizer manufacturers) which adversely effects the commodity oriented TSX. In trading, Consumer Staples, Telecommunications Services and Energy were the only Canadian sectors to end in the green. At the other end of the spectrum, Technology and Financials were the farthest into the red.

In the US, all three American indexes dropped more than 1% as investors digested news that the number of job openings increased more than expected. A tighter job market could lead to rising wages and prices which fuels inflation. The selloff caused the DJIA to fall into negative territory for the year. In trading, Utilities was the only American sector to end in the green. The interest sensitive Consumer Cyclicals and Technology sectors suffered the biggest declines.

Wednesday: All four indexes rebounded after yesterday’s selloff, some better than others. Investors appear to be coming to grips with the ‘higher for longer’ interest rates as two more Fed members reiterated the message. US Treasury yields eased lower from 16-year highs, opening the door for investors to wade back into stocks.

In Canada, the TSX barely made it into positive territory, inching into the green at the end of the day. However, gains were limited as oil prices plunged to a six-week low as the investors believe demand is weakening. In trading, the odd pair of Utilities (a defensive sector) and Technology (a high growth sector) led Canadian sectors, while Energy and Basic Materials were the only sectors to fall back.

In the US, the American markets rallied on news that private payrolls in the US came in lower than expected, suggesting the labour market is cooling off and sending the markets higher. It was a day of broad-based gains in the American sectors, led by Consumer Cyclicals and Technology. Energy was the only sector not to advance.

Thursday: The markets were relatively quiet, with the TSX ending higher while the three American indexes all ended slightly lower as investors wait for Friday’s Canadian and US employment reports. The jobs report could go along way to determining whether the respective central banks will hold or raise their benchmark interest rates.

In Canada, after closing at its lowest point in a year earlier this week, the TSX has rebounded and is now on a two-day winning streak. In trading, the Utilities and Telecommunications Services had the largest gains while the Consumer twins, Cyclicals and Staples, posted the biggest declines.

In the US, investors weighed the mixed signals of the latest employment reports. Job openings came in higher than expected on Tuesday, while Wednesday’s private payrolls came in lower than expected. Higher job openings suggest the economy is growing, along with inflation. On the other hand, lower private payroll data suggests the US economy, and inflation, is cooling. Tomorrow’s jobs report will be the tie breaker and is likely to be a big driver of investor sentiment going forward. Strong numbers would suggest another interest rate increase, while low numbers could leave the door open for the Fed to hold the rate at 5.5%. In trading, Financials and Healthcare were the big winners of the American sectors, with Consumer Staples and Basic Materials suffered the biggest losses.

Friday: Each index started the day in the red ahead of the release of jobs reports in Canada and the US. Once the data came out, each index rebounded to finish the day in the green. Investors were hoping the numbers would be in line with expectations but both numbers came in much hotter than expected. Oil prices rose after Russia partially lifted their fuel export ban. However, it was not enough to avoid the price of oil’s biggest weekly loss since March.

In Canada, the TSX ran its winning streak to three thanks to higher oil prices which boosted the share price of energy companies. Higher oil prices more than offset concerns of the higher for longer interest rate concerns brought on by the blowout jobs report that was three times higher than expected. On Bay Street, Technology and Basic Materials posted the biggest gains, while Consumer Cyclicals, Telecommunications Services and Healthcare were the only sectors to decline.

In the US, despite the news that the economy added almost twice as many jobs as expected, investors set aside their concerns about higher interest rates, sending all three indexes higher. The higher number of jobs points to a strong economy but it also boosts the Fed’s case for another interest rate hike. On Wall Street, Technology and Utilities were the best performers of the American sectors, while Telecommunications Services and Consumer Staples were the only sectors to slide lower.

Weekly Market and Portfolio Review

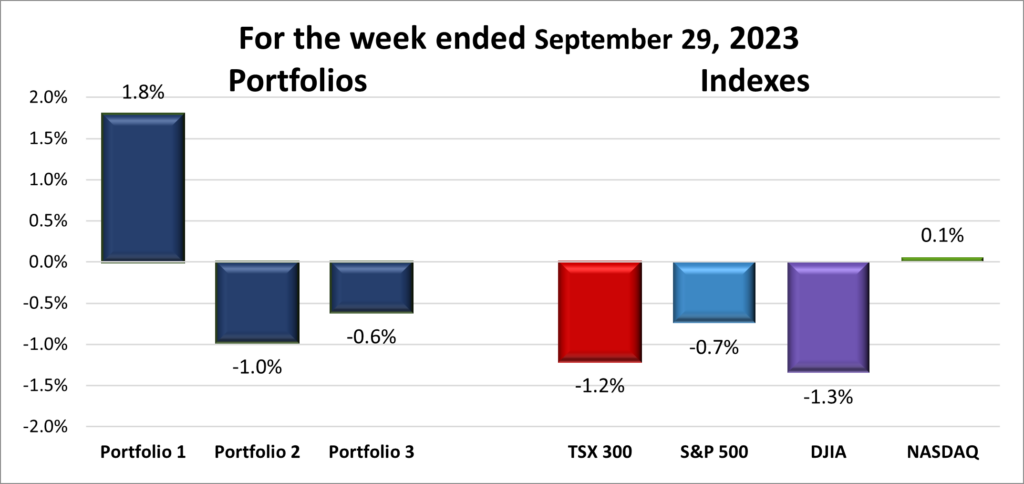

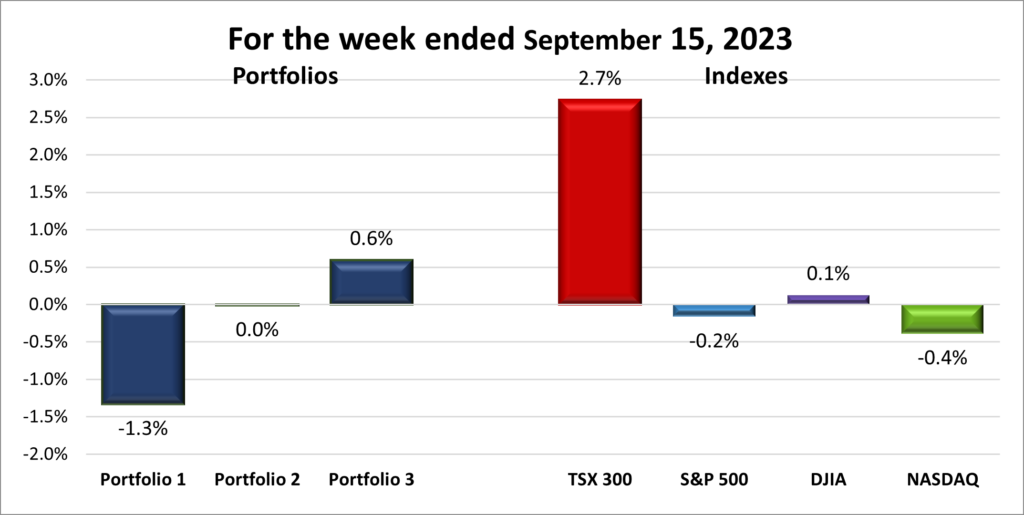

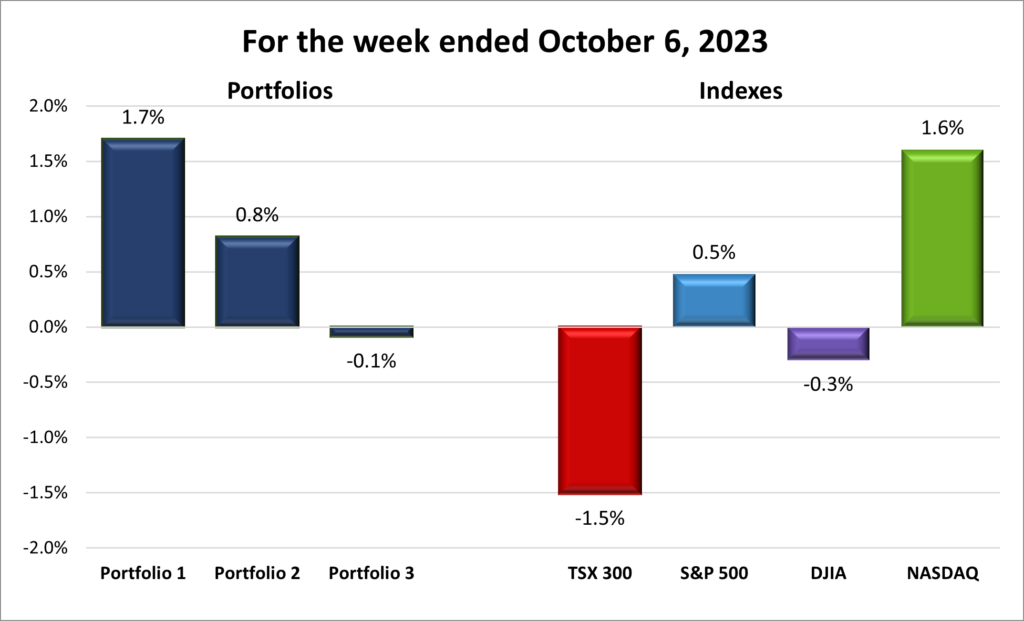

For the week, the TSX (SPTSX) lost 1.5%, the S&P 500 (SPX) added 0.5%, the DJIA (INDU) slipped 0.3% and the Nasdaq (CCMP) advanced 1.6%.

![]()

![]() The first week of the fourth and final quarter ended, with the growth-oriented indexes, the Nasdaq and S&P, able to advance, while the value-oriented TSX and DJIA ended the week lower. The week started with the US government able to avoid a shutdown after Congress passed a funding bill that would keep the government operating like normal… for another six weeks, when they will play a game of chicken again.

The first week of the fourth and final quarter ended, with the growth-oriented indexes, the Nasdaq and S&P, able to advance, while the value-oriented TSX and DJIA ended the week lower. The week started with the US government able to avoid a shutdown after Congress passed a funding bill that would keep the government operating like normal… for another six weeks, when they will play a game of chicken again.

However, that was not the big driver of the markets this past week.

At the start of the week, another wave of higher for longer interest rate fears drove all four indexes lower, as you can see in the graph above. This led to many investors moving into less risky government bonds as the yields kept going higher, causing the markets, represented by the stock market indexes, to fall. A good example of the higher interest rates is Canadian government bonds. They had a yield of 2.8% in late April. This past week, those same bonds now had a yield of 4.2%. Similar situations occurred in the US bond market. The increase in bond yields was largely the result of investors finally accepting that the BoC and the Fed were not bluffing about ‘higher for longer’ interest rates. Investors had previously believed that interest rate would start falling in early 2024. That no longer appears to be the case.

By mid week, bond rates had come down slightly, but a series of job reports started to lift the indexes. In the US, there were three reports culminating in a blow out report at the end of the week. Investors interpreted the reports as showing a strong and growing economy. In Canada, the jobs report came in three times as high as forecast. Again, investors interpreted the job reports as a sign of a strong economy. I suspect next week investors will start to consider the implications strong job reports have for inflation and the reaction both central banks will have to hot labour markets.

![]() As for the three portfolios, two of the three did better than expected. A strong performance from the Nasdaq helped lift both Portfolio 1 and 2 higher, with the more aggressive Portfolio 1 outperforming all four indexes. Portfolio 3 likely would have ended in positive territory but was held down by the split of Lithium Americas into two companies, and by the continued underperformance of the Brookfield family of companies. Hopefully, Portfolio 3 will get back in the weekly win column next week.

As for the three portfolios, two of the three did better than expected. A strong performance from the Nasdaq helped lift both Portfolio 1 and 2 higher, with the more aggressive Portfolio 1 outperforming all four indexes. Portfolio 3 likely would have ended in positive territory but was held down by the split of Lithium Americas into two companies, and by the continued underperformance of the Brookfield family of companies. Hopefully, Portfolio 3 will get back in the weekly win column next week.

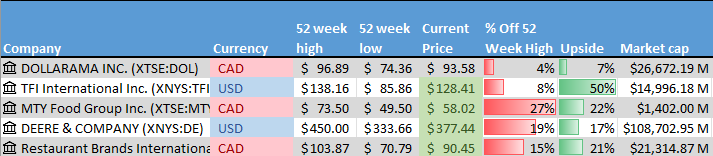

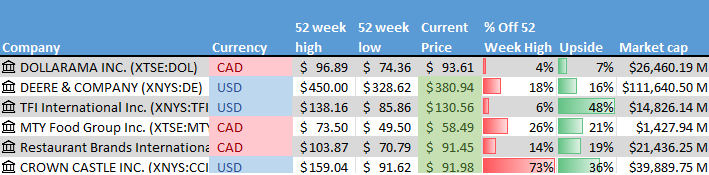

Companies on the Radar

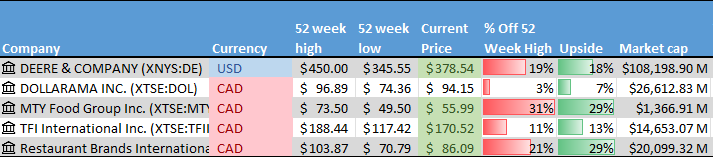

There were no new companies that came across my radar this past week. Currently the five companies below remain on my mirror:

There were no new companies that came across my radar this past week. Currently the five companies below remain on my mirror:

- Dollarama (TSX: DOL), a large Canadian company that operates dollar stores across Canada.

- TFI International Inc. (TSX: TFII), a mid-sized Canadian transportation and logistics company operating across North America.

- MTY Food Group Inc. (TSE: MTY), A small cap Canadian consumer cyclical company that operates and franchises quick service and casual dining restaurants throughout North America and internationally.

- Deere & Company (NYSE: DE), a large American company that manufactures and sells agricultural equipment worldwide.

- Restaurant Brands International Inc. (TSE: QSR), A large cap Canadian consumer cyclical company that operates in the North American quick serve restaurant industry. The company owns Tim Horton’s, Burger King, and Popeye’s Louisiana Kitchen among others.

The Radar Check was last updated October 6, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended October 6, 2023: UP ![]()

- Tesla (NASD: TSLA) missed analysts’ expectations for the number of vehicles the company would ship in the third quarter. The company shipped 435,059 cars globally, down 7% from the number they shipped in the second quarter. The company indicated the shortfall was a result of factory downtime needed to upgrade the facilities for the latest versions of their popular Model 3 electric vehicle (EV).

In related news, the company reduced pricing on its Model 3 and Model Y EVs by 2.7% to 4.2%. - Rivian (NASD: RIVN) beat expectations of 14,000 deliveries in the third quarter, delivering 15,564 EVs. That is an increase of 23% from same period in the previous year. The bad news: it is reported the company is losing US$33,000 on each sale of their US$80,000 trucks. I am not a business major, but that is not sustainable.

Separately, Rivian announced it plans to sell US$1.5 billion of convertible bonds. They will mature in October 2030 and investors will have the option to convert to cash or shares. - Lattice Semiconductor (NASD: LSCC) was given another award this week. This time the company won a 2023 AutoTech Breakthrough Award in the “Automotive Infotainment Solution of the Year” category for its Lattice Drive solution stack. Lattice Drive helps accelerate infotainment application development and improves the time to market for those applications.

- General Motors (NYSE: GM) secured a US$6 billon line of credit in the event the United Autoworkers strike lasts for an extended period.

In other GM news, sales jumped 21% in the third quarter on strong demand for its pickup trucks and SUVs. GM sold 674,336 vehicles in the third quarter compared to 555,580 in the same period a year ago. - Alphabet’s Google (NASD: GOOGL) released the Pixel 8 smartphone and a new smartwatch. Both devices feature built in artificial intelligence (AI) capabilities to provide owners with more useful information. One impressive feature is the ability to block spam calls. 😊

- The co-founder of Voyager Digital (OTCM: VYGVQ) was found to have broken derivatives regulations before the cryptocurrency lender fell into bankruptcy in 2022. Members of the Commodity Futures Trading Commission’s enforcement division said the co-founder misled customers about the safety of their assets after they investigated Voyageur’s conduct.

- Amazon (NASD: AMZN) launched their first two of many satellites that will become their planned Kuiper internet network. Amazon plans to eventually launch more than 3,200 satellites as part of this project.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Telus Corp (TSX: T)

Cargojet Inc (TSX: CJT)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended October 6, 2023: UP ![]()

- MongoDB (NASD: MDB) announced Jim Scharf as their new Chief technology Officer. Mr. Scharf spent the previous 17 at Amazon’s Amazon Web Services (AWS), where he was one of AWS’s first employees. He was involved in growing and scaling AWS’s capabilities as it became the top cloud computing platform globally.

Separately, MongoDB announced the launch of two new initiatives: MongoDB Atlas for Healthcare and MongoDB Atlas for Insurance. Both services should help companies in the respective industries increase their speed of innovation with data driven applications to better serve users. - Microsoft (NASD: MSFT) and Amazon are in the crosshairs of British media regulator Ofcom, and now Britain’s antitrust regulator the Competition and Markets Authority (CMA). The CMA will investigate the two companies’ dominance of the British cloud computing market. Together, the two cloud platform behemoths control 60-70% of the British market. Add in Google’s roughly 10% and that does not leave much room for smaller companies.

In other Microsoft news, the company is hoping to close their deal to acquire Activision Blizzard (NASD: ATVI) late next week, assuming it gets the green light from Britain’s anti trust regulators, the CMA. The deal received preliminary approval in September and is waiting for final approval.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Canadian Natural Resources Ltd (TSX: CNQ)

Telus Corp (TSX: T) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week, except for per share data.

Portfolio 3

Portfolio 3 for the week ended October 6, 2023: DOWN ![]()

- Brookfield Corporation (TSX: BN) purchased the British renewables division of Britain’s Banks Group. Brookfield will pay US$1 billion and in return will receive eleven offshore wind farms spread across Scotland and northern England, plus other solar and wind projects in development.

- Lithium Americas (TSX: LAC) split into two separate lithium producers this week. Lithium Americas and Lithium Americas (Argentina) Corp (TSX: LAAC).

- Cloudflare (NYSE: NET) was named as one of the ‘Top 100 Most Loved Workplaces in 2023’, coming in 55th. It was the second straight year Cloudflare was recognized as a top place to work.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Brookfield Asset Management (TSX: BAM)

Brookfield Corp (TSX: BN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.