Items that may only interest or educate me ….

Canadian economic news, US economic news, Global economic news, Google versus the European Commission …

The good news is that the ongoing bull market in the US has managed to recover most of the S&P’s losses from 2022 and has completely offset the losses incurred since the Fed’s initial rate hike in March 2022. However, the not-so-good news is that this rally has primarily been driven by a select group of large and mega cap technology companies, rather than a broad-based market rally. On a positive note, investors have recently begun exploring other sectors of the market, such as small-cap, energy, and industrial companies, which have resulted in significant gains in those areas as well as lifting the American markets in general.

Despite the recent advancements, the TSX continues to lag the American indexes by a significant margin. The bull market has primarily been fueled by growth in the technology sector, especially through an Artificial Intelligence (AI) driven rally in the US markets. In contrast, the TSX lacks major technology companies, with Shopify (TSX: SHOP) being one of the exceptions. The technology sector only accounts for 7.7% of the TSX so its hard for that sector to drive the TSX. On the other hand, the energy sector constitutes 16.6% of the TSX. In 2022, the energy sector drove the TSX and helped limit losses, but this year it is acting as a drag rather than a driver for the index.

Canadian economic news

Last week, the Bank of Canada (BoC) raised the Canadian benchmark interest rate to 4.75%, marking 22-year high and surprising many analysts. Despite this unexpected increase, many of those same analysts are predicting that the BoC will raise the rate by another 0.25% at their upcoming July meeting.

Their reasoning is that a mere 0.25% hike would not be sufficient to drive down inflation fast enough to reach the BoC’s desired goal of a 2% inflation rate. Analysts point to several factors supporting their prediction, including a robust labor market, a surging housing market, a strong economy in the first quarter with a growth rate of 3.1%, and inflation falling at a slower pace than desired. Housing prices have started to rise as banks extend the terms of variable interest rate loans to minimize the impact of higher rates. Furthermore, these analysts are also predicting that there will be no rate decrease in 2023.

US economic news

Latest from the Fed

As expected, the Federal Reserve’s (Fed) Federal Open Market Committee (FOMC) maintained the US benchmark interest rate at 5.25%, marking the first pause in rate hikes in fifteen months. However, the FOMC cautioned that additional rate hikes were likely, with the possibility of raising the rate as high as 5.75% by the end of 2023.

The pause in rate hikes suggests that the FOMC is giving the economy time to adjust to the higher rates and evaluate the implications of future actions. Fed Chair Jerome Powell noted that while conditions for reducing inflation were emerging, it would take time for the impact to be felt. These conditions include slower economic growth, a weaker labor market, and improved supply chains to meet demand.

Looking ahead, FOMC officials conveyed a hawkish stance, indicating that additional rate hikes would be necessary to bring inflation down to the Fed’s 2% target. They project an inflation rate of 4.6% in 2024, which is expected to drop to 3.4% in 2025. Additionally, the FOMC predicts by the end of 2023 a 1% gain in Gross Domestic Product (GDP), compared to their initial 0.4% forecast, and an increase in unemployment to 4.1% from the current rate of 3.7%.

While the decision to pause rate hikes was anticipated, the markets initially reacted negatively due to the FOMC signaling the likelihood of two more rate hikes before year-end. However, Fed Chair Powell reassured investors that no definitive decisions had been made regarding a rate hike at their July 25-26 meeting. Once the markets were calmed, they resumed their upward trajectory, albeit somewhat flatter. The press release from the Fed can be read here.

CPI

Consumer Price Index (CPI) rose by 0.1% in May, following a 0.4% increase in April, indicating a decrease in the growth rate. On an annual basis, the CPI saw a growth rate of 4.0%, marking the slowest pace of growth since April 2021. Analysts had predicted a monthly increase of 0.2% and an annual rise of 4.1% for the CPI.

Meanwhile, the Core CPI, which excludes the more volatile food and energy prices, remained unchanged at 0.4% in May, matching the April figure. On a yearly basis, the core CPI increased by 5.3%, down slightly from the 5.5% growth observed in April. Analysts had projected a monthly rise of 0.4% and an annual increase of 5.2% for the core CPI.

While it would have been great to see decline in both the core CPI and overall CPI in May, it is expected that the core CPI will begin to decrease as the effects of the interest rate hikes continue to work their way through the economy. We will never know if this bit of economic news indicating slowing and falling inflation was what caused the FOMC to pause their rate hikes, but it did not hurt.

The CPI serves as a measure of the price changes experienced by consumers for various goods and

services over a specified period, typically on a monthly or yearly basis.

PPI

The Labor Department reported the May Producer Price Index (PPI) for final demand dropped more than expected, falling 0.3%. This comes on the heels of a 0.2% climb in April. On an annual basis, the PPI increased 1.1%, the smallest gain since 2020. The decrease in the PPI can be attributed primarily to a significant drop in the costs of energy goods (such as gasoline) by 6.8% and food by 1.3%. Meanwhile, the Core PPI, which excludes food, energy, and trade services, remained unchanged at the same rate as in April. On a yearly basis, the Core PPI showed a 2.8% increase.

Falling PPI is one factor the Fed considers when deciding whether to adjust interest rates to stimulate economic activity and avoid deflationary risks. The lower PPI data indicates that producers are facing reduced costs, particularly in energy, which in turn leads to lower prices for finished goods. This can contribute to an overall decrease in inflationary pressures within the economy and suggests a drop in inflation.

Retail sales

The Commerce Department recently announced that retail sales in May unexpectedly rose by 0.3%, following a 0.4% increase in April. Among the areas that experienced the largest increases were building materials, which saw a growth of 2.2%, and motor vehicles, which saw a rise of 1.4%. On the other hand, gas stations had the biggest decline, experiencing a decrease of 2.6%.

When comparing the retail sales data to May 2022, there was an overall increase of 1.6%. The sectors that showed the most significant increases were restaurants, with a rise of 8.0%, and personal care products, which saw growth of 7.8%. Conversely, gas stations experienced a substantial decline of 20.5%, while furniture retailers saw a decrease of 6.4%.

Consumer Sentiment Index

The University of Michigan’s preliminary reading on the June consumer sentiment index came in at 63.9, better than expectations of 60.0 and up from 59.2 in May. The overall sentiment remains at a moderate level, but it does indicate a slight improvement in consumer sentiment regarding factors such as job prospects, income expectations, and general economic conditions. As a result, there could be a minor increase in consumer spending which would be good for the economy.

Global economic news

The European Central Bank (ECB) followed the lead of the BoC and The Reserve Bank of Australia, Australia’s central bank, and raised the European Union (EU) benchmark rate by 0.25% to 3.5%. This was the ECB’s eighth straight increase. ECB officials also said they “will continue to hike at our next meeting. So we are not thinking about pausing, as you can tell.”

As in North America, the higher rates are slowly starting to have an impact but there is still along way to go from the current EU inflation rate of 6.1% to the ECB’s target of 2% (2% seems to be every central bank’s target 😊). The ECB said additional increases are likely, possibly as soon as their next meeting on July 27.

Google versus the European Commission

Alphabet’s (NASD: GOOGL) Google is currently engaged in a high-stakes battle with the European Union’s antitrust regulator, the European Commission (EC). The EC alleges that Google has exploited its dominant position in the online advertising market to the detriment of its competitors. Google holds a significant role as both a buyer and seller of online ads, as well as owning the intermediary service that connects advertisers and publishers. This gives Google substantial control over the online advertising ecosystem, as it commands a 28% share of the global digital advertising market. Consequently, the EC may require Google to divest a portion of its advertising technology business and it could potentially impose a fine of up to 10% of Google’s annual global revenue. Google, naturally, disputes these allegations and has been granted several months to respond to the charges brought by the EC. This is a significant threat for Alphabet since advertising revenue accounts for 79% of their total revenue.

Now that we have gone over the big economic news of the past week, let’s see what happened this past week….

Weekly Market Review

Monday: Investors were bullish to start the week, pushing all four major North American indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – into the green. Investors are betting the Fed will pause their interest rate hikes. Oil prices slid over concerns about the global economy and demand for energy.

In Canada, a rally in technology companies was mostly offset by a drop in energy companies, allowing the TSX to make it into positive territory. In trading in the Canadian sectors, the Technology and Consumer Cyclicals had the biggest gains while Energy and Utilities had the biggest losses.

In the US, investors appear confident there will be no change to the US interest rate and pushed the Nasdaq and S&P to their August 2022 highs. In trading, Technology and Consumer Cyclicals advanced the most of the American sectors, while Energy and Financials dropped the most.

Tuesday: All four indexes advanced after the US inflation data showed prices continue to fall, rising less than forecast. Investors are now keeping their fingers crossed that the Fed will pause their rate hikes when they conclude their meeting tomorrow. Oil prices inched higher on news China lowered its short-term lending rate for the first time in almost a year to kickstart their economy.

In Canada, signs of slowing inflation in the world’s largest economy (the USA) spurred the TSX higher. In trading, Consumer Cyclicals and Consumer Staples led the Canadian sectors higher, while Technology, Utilities and Healthcare were the only sectors to slide back.

In the US, investors believe there is a 95% chance the Fed will not increase the benchmark interest rate tomorrow. This optimism sent the Nasdaq and S&P to their highest closing numbers since April 2022. The American sectors were led higher by the Basic Materials and Consumer Cyclicals sectors. Telecommunications Services and Utilities were the only sectors to end lower.

Wednesday: A mixed day in the North American stock markets. The DJIA headed south early and stayed down all day. The other three indexes had a temporary dip into negative territory following the Fed’s decision to maintain the US interest rate at 5.0% before rallying to each end the day higher. The possibility of additional rate hikes sent oil prices lower.

In Canada, the TSX edged higher as investors digested the implications of the Fed’s interest rate pause. In trading on Bay Street, the interest sensitive Technology and Consumer Cyclicals sectors posted the biggest gains with Energy and Utilities the biggest losses.

In the US, the pause in interest rates was good news for the technology heavy Nasdaq and S&P, lifting both into positive territory. In trading on Wall Street, the Technology and Consumer Staples sectors had the biggest advances, while Healthcare and Energy had the biggest declines.

Thursday: Despite warnings from the Fed of possible rate hikes down the road, investors focused on yesterday’s good news of a pause in rate increases and pushed all four indexes higher.

In Canada, the TSX ended up slightly, lifted by the rising tide of optimism in the US that the Fed is nearing the end of their rate hikes. In trading, it was a mixed day in the Canadian sectors with half of the sectors ending higher, led by Energy and Financials. On the other side, Utilities and Technology suffered the biggest losses.

In the US, a day after the Fed paused their rate hikes, investors believe the end of the Fed’s rate hikes are on the horizon and are returning to the stock markets. It was a day of broad-based gains that saw every American sector end higher, led by Telecommunications Services and Healthcare, while Consumer Cyclicals and Financials brought up the rear.

Friday: The indexes were up and down most of the day before ending lower. The recent rally lost momentum as investors took some profits as they try to figure out the Fed’s next move. There was additional volatility in the markets due to the expiration of index futures and options that all came due today. Oil prices ended the week on an upbeat note as supply cuts and increased Chinese demand combined to send oil prices higher.

In Canada, the TSX ended its four-day winning streak as investors took some of their money off the table after a run up in Canadian technology companies. Leading the winners in the Canadian sectors were Telecommunications Services and Consumer Cyclicals, while Technology and Consumer Staples had the largest drops.

In the USA, all three indexes dropped slightly after Fed officials said they were ‘comfortable’ with additional rate hikes. The Nasdaq and S&P both fell back after a week of big gains, dragged downward by the big technology companies like Microsoft (NASD: MSFT) and Apple (NASD: AAPL) — which had recently closed at all-time highs. In trading, the defensive sectors Utilities and Consumer Staples were the only ones to advance, while Technology and Telecommunications Services had the biggest declines.

Weekly Market and Portfolio Review

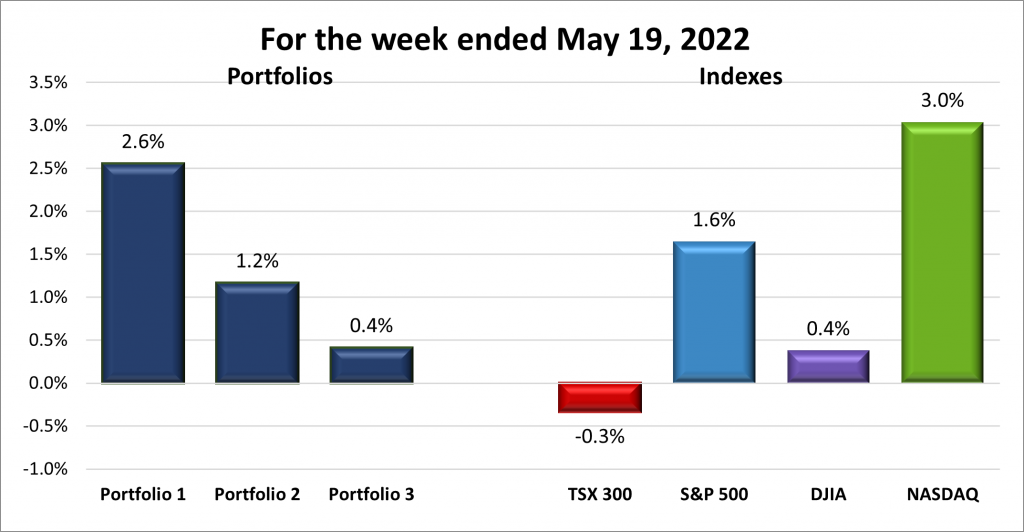

For the week, the TSX (SPTSX) rose 0.4%, the S&P 500 (SPX) had its best week since March gaining 2.6%, the DJIA (INDU) advancing 1.2%, and the Nasdaq (CCMP) posted its eighth consecutive winning week, its longest winning streak since March 2019, up 3.2%.

![]() The chart above illustrates another positive week for all four indexes. The Nasdaq and S&P, driven by major technology companies, particularly those with artificial intelligence (AI) capabilities, continued their upward momentum. Throughout the week, apart from the DJIA, the indexes maintained a consistent upward trend. However, on Friday, some investors opted to lock in profits following the recent rally, leading to a slight pullback.

The chart above illustrates another positive week for all four indexes. The Nasdaq and S&P, driven by major technology companies, particularly those with artificial intelligence (AI) capabilities, continued their upward momentum. Throughout the week, apart from the DJIA, the indexes maintained a consistent upward trend. However, on Friday, some investors opted to lock in profits following the recent rally, leading to a slight pullback.

On Wednesday, the Fed paused their rate hikes. As a result, all three American indexes closed significantly higher on Thursday as optimistic investors regained confidence and returned to the markets.

The TSX also posted a weekly gain, helped by the Canadian technology sector but that was barely enough to lift the TSX into positive territory for the week. The Canadian technology sector accounts for 7.7% of the TSX, while the energy and financials sectors constitute 16.6% and 30.1% of the TSX, respectively. For the TSX to have a good week, it usually needs one of these two sectors to have a good week.

![]() It was another positive week for all three portfolios. Portfolio 1 had a good week thanks to the strong performance of its core holdings of dominant technology companies Alphabet, Amazon (NASD: AMZN), Apple, Nvidia (NASD: NVDA), and Tesla (NASD: TSLA). Portfolio 3 also experienced a good week, driven by the continued strength of Microsoft and Shopify.

It was another positive week for all three portfolios. Portfolio 1 had a good week thanks to the strong performance of its core holdings of dominant technology companies Alphabet, Amazon (NASD: AMZN), Apple, Nvidia (NASD: NVDA), and Tesla (NASD: TSLA). Portfolio 3 also experienced a good week, driven by the continued strength of Microsoft and Shopify.

Portfolio 2 also gained ground this past week. While its technology companies performed well, the gains were limited by the lacklustre performance of its energy companies. A year ago, the diversified and balanced nature of Portfolio 2 was seen as an advantage during the 2022 bear market. However, those advantages now limit the gains during a bull market like the ones in the Nasdaq and S&P.

While I would prefer all three Portfolios to post 3+% gains in each portfolio on a weekly basis, I will be happy as long as the portfolios each keep posting weekly gains. 😊

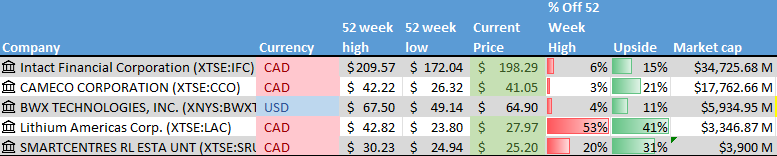

Companies on the Radar

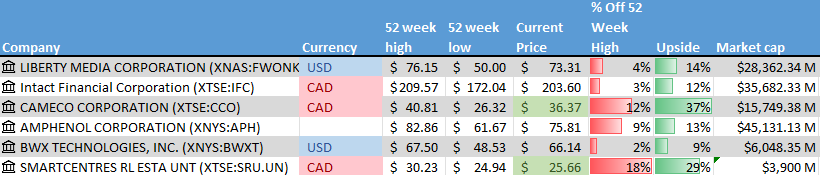

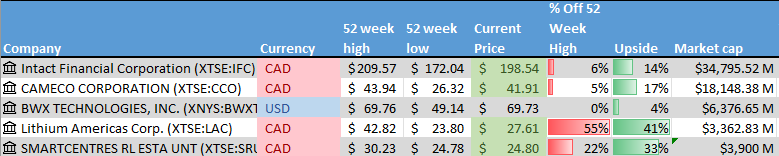

No new companies came across my radar this past week, leaving the companies listed below as the frontrunners if I were to add a new company to any of the portfolios.

No new companies came across my radar this past week, leaving the companies listed below as the frontrunners if I were to add a new company to any of the portfolios.

- Intact Financial (TSX: IFC): A Canadian mid-size insurance company that offers home, car, and business insurance in Canada, the US, and the UK.

- Cameco (TSX: CCO): A large Canadian company involved in uranium mining, sales, and the construction of reactor components.

- BWX Technologies (NYSE: BWXT): A mid cap size American company specializing in the construction and sale of nuclear components to customers worldwide, including the US Navy.

- Lithium Americas (TSX: LAC): A mid size Canadian company operating lithium mines in the USA and Argentina. They are a provider of lithium to the emerging electric vehicle battery industry.

- Smartcentres Real Estate Investment Trust (TSX: SRU.UN): A mid size fully integrated REIT that owns and manages a number of income producing shopping centres and retails spaces throughout Canada.

The Radar Check was last updated June 16, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended June 23, 2023: UP ![]()

- Copperleaf’s (TSX: CPLF) Asset Solution for Investment Planning was chosen by Baltimore Gas & Electric (BGE) to manage its transmission and substation asset sustainment plans. BGE is Maryland’s largest natural gas and electric utility provider.

- Docebo (TSX: DCBO) enhances its AI capabilities with the acquisition of Edugo.AI. This will help Docebo optimize learning paths for individual users.

- General Motors (NYSE: GM) will partner with Samsung SDI to build a US$ 3 billion electric vehicle (EV) battery plant in Indiana. This will help secure a reliable supply of batteries for GM’s EVs. I assume this facility will be eligible for any tax deductions under the US’s Inflation Reduction Act.

In other GM news, GM has indicated it plans to keep producing its highly profitable trucks and SUVs for another 10 – 12 years. GM has said it will be years before their electric trucks and SUVs can match the profit from their conventional trucks and SUVs. By extending the timeline, GM has the potential to make US$ 50+ billion in profit. - TMX Group (TSX: X) owners of the Toronto Stock Exchange and other Canadian based exchanges executed a 5 for 1 stock split.

- Bell (TSX: BCE) closed six radio stations and let go 1,300 employees across Canada as part of reducing expenses. Bell also closed their London and Los Angeles bureaus and reduced staff at their Washington bureau. Bell plans to operate a single newsroom across Canada. I am sure everyone outside the greater Toronto area will be thrilled to know what is going on in Toronto but not in their hometown.

- Britain’s competition regulator, Competition and Markets Authority (CMA), signed off on Amazon’s acquisition of iRobot (NASD: IRBT), the manufacturer of Roomba vacuum cleaners. The deal now waits approval from the US Federal Trade Commission and the European Union’s European Commission.

Activity

Bought: Amazon. After reading the letter to shareholders in their Annual Report, I decided to increase my holdings. Amazon stands to benefit from optimizing its workforce, concentrating on its core strengths, and leveraging the increasing advancements in AI.

One thing that intrigues me is they are developing their own semiconductors, specifically tailored for their Amazon Web Services (AWS) AI services. These custom chips have the potential to enhance both Amazon’s internal AI capabilities and the services offered by AWS. This should put Amazon in a good position to capitalize on the growing demand for AI-related technologies and services and take a leadership position in the emerging AI market.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX: DIR.UN)

Yellow Pages Ltd (TSX: Y)

US $

BSR Real Estate Investment Trust (TSX: HOM.U)

General Motors Co (NYSE: GM)

Home Depot Inc (NYSE: HD)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended June 23, 2023: UP ![]()

- The US Federal Trade Commission (FTC) has asked a federal court to block Microsoft’s purchase of gaming developer Activision Blizzard (NASD: ATVI). So far, the deal has been vetoed by the United Kingdom’s Competition & Markets Authority, while it was approved by the European Union’s European Commission and Japan’s Fair Trade Commission.

- Mitek Systems (NASD: MITK) announced they have been notified by the Nasdaq Stock Market company they have started the process to delist Mitek from the exchange. Mitek has not filed its Form 10-K for the fiscal year ended September 30, 2022, nor its Quarterly Reports (Form 10-Q) for the quarters ended December 31, 2022, and March 31, 2023, in a timely manner and did not meet the terms of a previously granted filing extension by the compliance deadline.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

iA Financial Corporation Inc (TSX: IAG)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week

Portfolio 3

Portfolio 3 for the week ended June 23, 2023: UP ![]()

- Brookfield Renewables (TSX: BEP.UN) has agreed to buy Duke Energy Corp’s (NYSE: DUKE) unregulated utility scale Commercial Renewables business for US$ 2.8 billion. The sale adds more than 3,400 megawatts of utility-scale solar, wind and battery storage throughout the US to BEP.UN’s renewable energy portfolio.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Enghouse Systems Limited

All currency listed in thousands of Canadian dollars, except for per share data.

Selected highlights from their second quarter 2023 financial results on June 12, 2023

- Revenue of $113,461 for the three months ended April 30, compared to $106,312 for the same period in 2022. An increase of almost 7%.

- Net income of $12,536 for the three months ended April 30, compared to net income of $17,871 in the same period in 2022.

- Diluted earnings per ordinary share of $0.23 for the three months ended April 30, compared to earnings of $0.32 per share for the same period in 2022.

- Revenue of $219,896 for the six months ended April 30, compared to $217,414 for the same period in 2021. An increase of over 1%.

- Net earnings of $29,599 for the six months ended April 30, compared to net earnings of $39,468 in the same period in 2021.

- Diluted earnings per ordinary share of $0.53 for the six months ended April 30, compared to earnings of $0.71 per share for the same period in 2021.