Items that may only interest or educate me ….

Canadian Economic news, US Economic news, Magnificent Seven, An AI primer, …

Canadian Economic news

Consumer Price Index report for June

Statistics Canada reported that Canada’s annual inflation rate for June, as measured by the Consumer Price Index (CPI), dropped to 2.8%, marking a 27-month low. This rate was lower than May’s 3.4% increase and below analysts’ expectations of 3% growth. On a month-over-month basis, the CPI increased by 0.1%, which was lower than May’s 0.4% rise and below analysts’ expectations of a 0.3% increase. The decrease in gas prices, which were down 21.6% since June 2022, was the primary factor contributing to the lower CPI. However, grocery prices continued to rise, up 9.1%, and mortgage interest costs were up by more than 30% in the past year.

Before getting too excited and thinking the Bank of Canada (BoC) is done with rate hikes, it is important to consider core CPI, which is the BoC’s preferred measure. Core CPI grew by 3.5% on an annual basis, down from May’s 4.0%. On a monthly basis, core CPI remained unchanged at 0.0%. Core CPI is a version of the CPI that excludes the volatile components food and energy, providing a more stable and accurate measure of underlying inflation trends. It provides a clearer view of longer-term inflation trends in the economy.

CPI and core CPI are key pieces of the puzzle that the BoC considers when deciding whether to raise or lower the benchmark interest rate. The CPI is commonly used to track changes in the cost of living for consumers, representing the average price change of a basket of goods and services typically purchased by households over a period of time. This is also known as ‘headline CPI.’ A decrease in the CPI suggests lower costs for everyday goods and services, something we all can appreciate. Core CPI provides a more accurate view of the underlying inflationary pressures in the economy and helps policymakers gauge longer-term trends in inflation more accurately.

Retail Sales

The May retail sales report from Statistics Canada shows a slowdown in consumer spending compared to the previous month. Retail sales increased by 0.2%, which is lower than the 1.1% gain observed in April and below analysts’ expectations of a 0.5% increase for May. On an annual basis, retail sales were up by 0.5%, led by strong performances in motor vehicle and parts dealers, up 6.3%, as well as food and beverage retailers, up 5.2%.

Core retail sales, which exclude the sub sectors gas stations and fuel vendors, and, motor vehicle and parts dealers, remained flat in May. Food and beverage sales saw an increase of 1.0%, but this was offset by a decline of 1.5% in building materials and garden equipment and supplies dealers.

The slowing growth in retail sales indicates a potential slowdown in the Canadian economy. While the Consumer Price Index (CPI) is within the BoC target range of 1% – 3%, the higher core CPI, which now exceeds headline CPI, is a cause for concern for the BoC. If core inflation remains elevated, there is a possibility that the BoC may opt for an additional rate hike at their next meeting in September.

US Economic news

Retail sales

The Commerce Department’s June report on retail sales indicated a slowdown in consumer spending compared to the previous month. Retail sales rose by 0.2%, which was lower than the 0.5% pace observed in May. On an annual basis, retail sales increased by 1.5%, marking the second slowest pace since May 2020.

The decline in gas station purchases by 22.7% and home furnishings by 4.6% contributed to the overall decrease in retail sales. However, there were some areas where consumers continued to spend, such as motor vehicles and personal care, which saw increases of 5.3% and 6.3%, respectively.

Retail sales serve as an important measure of household spending. The Federal Reserve (Fed) is likely to view this slowdown in spending positively, since slower consumer spending can alleviate some of the demand-driven inflation that the economy has experienced.

Retail sales data are some of the key data points the Fed considers regarding the US interest rate. If the trend of slower spending continues, it will likely give the Fed more confidence to hold off on increasing the interest rate and consider lowering it in the future.

Magnificent Seven

The rise of the “Magnificent Seven”, namely Apple (NASD: AAPL), Microsoft (NASD: MSFT), Alphabet (NASD: GOOGL), Amazon (NASD: AMZN), Nvidia (NASD: NVDA), Tesla (NASD: TSLA), and Meta Platforms (NASD: META), has been nothing short of remarkable in 2023. Their collective surge, with share price increases ranging from 40% to over 200%, has been the driving force behind the S&P 500’s impressive 17% year-to-date rise, pushing the index to its highest level since April 2022.

These mega-cap stocks, each valued at over US$200 billion, have come to dominate benchmark indexes, accounting for a substantial 27.9% of the S&P 500’s total weight. Because of their meteoric rise, I now consider them essential core holdings rather than growth stocks. Each portfolio contains at least one of these companies and has become a critical component of all three portfolios.

One of the key factors contributing to their dominance is their strong presence in the current artificial intelligence (AI) trend. Being at the forefront of AI development, these companies have positioned themselves to capitalize on future technological advancements.

Given their significant impact on the overall market and their potential for future growth, the “Magnificent Seven” have become almost necessary additions to any portfolio. It is important to have exposure to these companies, not only for their outstanding performance but also for their potential to lead technological innovations in the years to come. For more information on the Magnificent Seven, check out this post here.

An AI primer

If you are looking for a decent primer on AI, check out this article on AI, it is as good as anything I have seen. It is a bit technical, but it covers the key terms and the key players in the emerging market. A quick example of AI, while typing this, when I typed “art” the program instantly suggested artificial intelligence. Now, if I can get it to tell me the next hot stock. 😊

Now, let’s see what moved the markets this past week….

Weekly Market Review

Monday: The American markets got the week off to a good start with the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) all advancing. Unfortunately, Canada’s Toronto Stock Exchange Composite Index (TSX) stumbled on news that China’s Gross Domestic Product data for the second quarter came in lower than expected, up only 0.8% from the first quarter. Slow growth in China will likely have some negative spillovers for Canada and the US, such as lower oil and commodity prices because of lower demand from China.

In Canada, the TSX was dragged down by the lower commodity price as a result of slowing demand from China. In trading, Healthcare, Technology and Financials were the only Canadian sectors to end in the green. The biggest drops were in Telecommunications Services and Energy.

In the US, the DJIA had its best day of the year as investors await second quarter earning from many of the big US banks and technology companies. As long as earnings report match expectations, the markets should continue moving higher. In trading, Technology and Financials were the best performing American sectors, while Telecommunications Services and Utilities had the biggest declines.

Tuesday: After yesterday’s dip into the red, the TSX reached a two-month high and joined the other indexes in the green at the end of the day. Oil prices rebounded from yesterday’s sell off on hopes a Chinese economic support plan will increase demand. In Canada and the US, data continues to indicate a positive combination of strong economies, cooling inflation, and a robust labour market. A great combination for the economies and the markets.

In Canada, spurred on by the declining rate of inflation, investors gained confidence that rising interest rates will end sooner rather than later and pushed the TSX higher. In trading, Basic Materials (miners and fertilizer manufacturers) gained the most, while Consumer Staples and Technology had the biggest declines,

In the USA, thanks to strong earning from the big American banks that reside on the DJIA, the DJIA led all indexes higher and stretched its winning streak to seven. The markets were led higher by the Financials and Energy sectors. The defensive sectors Utilities and Consumer Staples were the only sectors to end lower.

Wednesday: Its hump day and all four indexes ended higher as better than expected earnings reports continue to roll in for DJIA listed companies and several other US banks.

In Canada, Canadian banks were lifted higher by the positive earnings reports coming from US banks, helping the TSX to its highest close in two months. The Canadian Financials sector accounts for 29% of the TSX’s market capitalization, so a good day for the sector is usually a good day for the index. On Bay Street, Telecommunications Services and Utilities posted the biggest gains while Consumer Staples was the only sector to end in the red.

In the US, the DJIA ran its winning streak to eight while the Nasdaq barely ended in the green after a dip from Microsoft after Apple announced it was getting into the artificial intelligence game. Elsewhere on Wall Street, Telecommunications Services and Utilities were the best performers, while Basic Materials, Technology and Industrials were the only American sectors to end lower.

Thursday: Investors were not impressed with yesterday’s weak earnings from Netflix (NASD: NFLX) and shrinking margins from Tesla, casting a pall over the markets. The DJIA was the only index to end in the green. Oil prices rose on news US crude oil inventories were low, and China reported higher imports of crude oil.

In Canada, the TSX fell as investors moved away from Canadian technology companies as concerns higher interest rates will reduce their cash flow these firms require to further their high growth needs. Of the four Canadian sectors that ended higher, Utilities and Energy led the way. On the downside, Technology and Basic Materials had the biggest drops.

In the US, the disappointing results from big name technology companies Netflix and Tesla dragged the technology heavy Nasdaq lower and weighed on the S&P. Meanwhile, the blue chip oriented DJIA touched a 52-week high while running its winning streak to nine days. In the American sectors, Utilities and Healthcare posted the biggest gains while Technology and Consumer Cyclicals suffered the biggest declines.

Friday: A mixed day for the four major North American indexes, with the TSX posting the day’s biggest gain, the Nasdaq posted the biggest loss, and the DJIA and S&P were essentially flat. Investors are looking ahead to next week’s Fed meeting and earnings reports from many of the technology titans. Investors are hoping lacklustre reports from Netflix and Tesla are not a sign of things to come for the big technology companies. Oil prices moved higher after China said they would introduce measures to jumpstart the Chinese economy.

In Canada, higher oil prices drove the TSX higher despite the latest Canadian retail sales data showing retail sales slowing down. In trading on Bay Street, Telecommunications Services and Energy were the big gainers, Technology was flat, while Basic Materials was the only Canadian sector to fall back.

In the US, the DJIA inched into positive territory to run its streak to an impressive ten days, its longest winning streak since August 2017. The Nasdaq was choppy as various funds that track the Nasdaq 100 index must rebalance themselves to lower their concentration of some of the biggest technology companies to match the Nasdaq 100’s new weightings. In trading on Wall Street, the Utilities and Healthcare sectors notched the biggest gains, while Financials and Industrials had the biggest drops.

Weekly Market and Portfolio Review

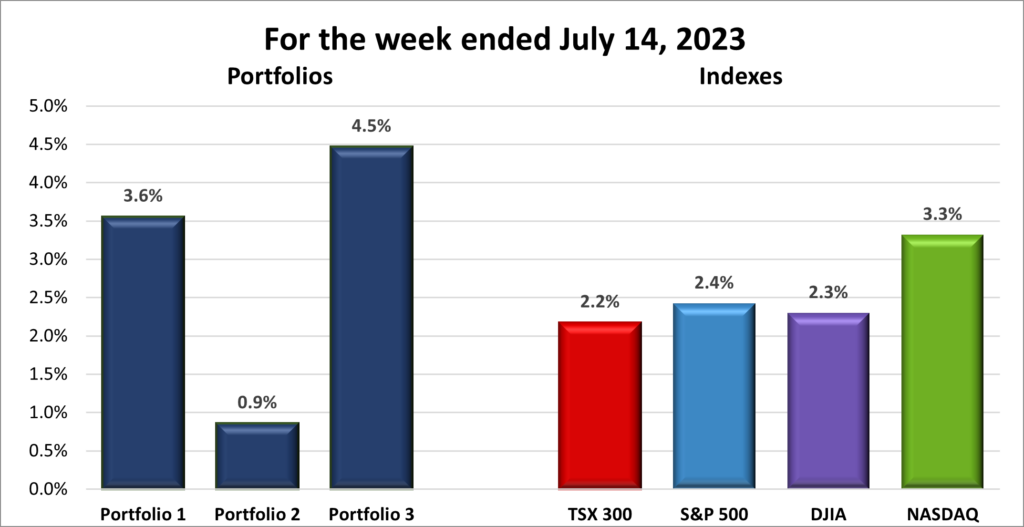

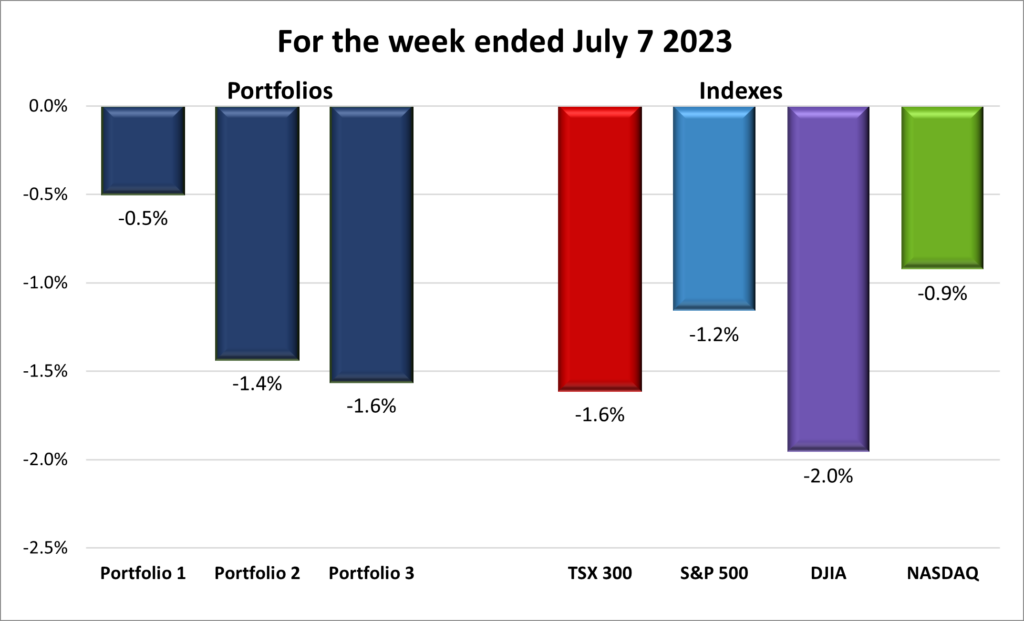

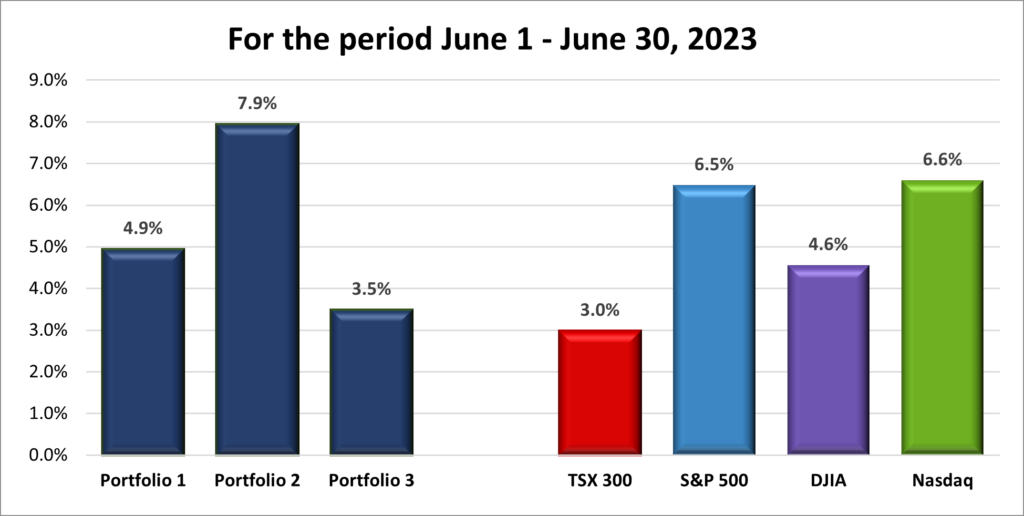

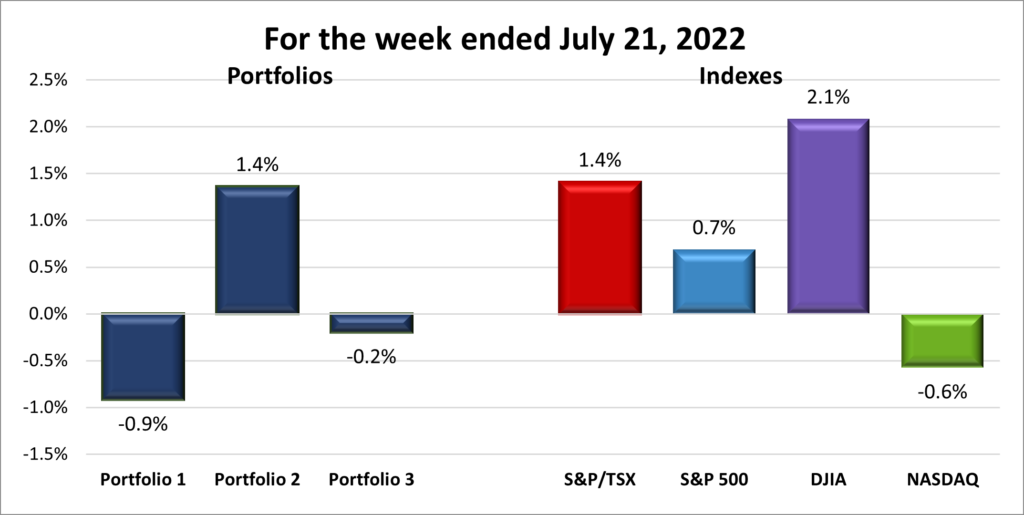

For the week, the TSX (SPTSX) advanced 1.4%, the S&P 500 (SPX) rose 0.7%, the DJIA (INDU) jumped 2.1% and the Nasdaq (CCMP) slumped 0.6%.

![]() It was a mostly positive week for the stock markets, with three of the four indexes advancing, as seen in the graph above. The Nasdaq saw a decline due to concerns over the earnings reports of well-known technology companies Netflix and Tesla. This dragged down both the Nasdaq, which is home to many technology companies, and the S&P 500, which includes the largest 500 companies, including major technology firms.

It was a mostly positive week for the stock markets, with three of the four indexes advancing, as seen in the graph above. The Nasdaq saw a decline due to concerns over the earnings reports of well-known technology companies Netflix and Tesla. This dragged down both the Nasdaq, which is home to many technology companies, and the S&P 500, which includes the largest 500 companies, including major technology firms.

On the other hand, the DJIA was the clear winner of the week, benefiting from solid earnings reports from big American banks.

In Canada, the TSX saw gains driven by higher oil prices. Analysts expect increased demand from China thanks to government programs aimed at stimulating their economy. At the same time, supply shortages caused by production cutbacks from Saudi Arabia and Russia, along with ongoing tensions between Russia and Ukraine, are likely to lead to higher oil prices.

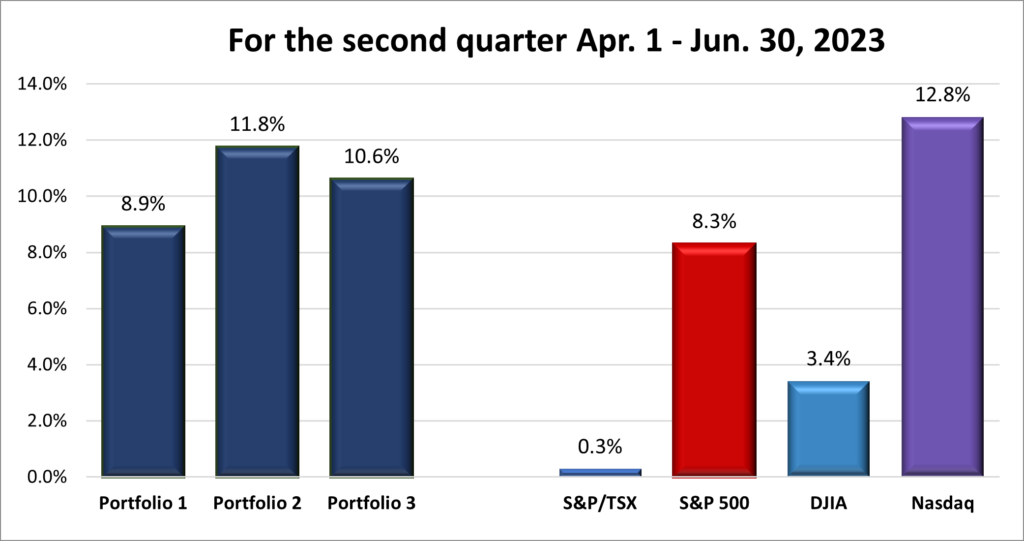

![]() As you can see in the chart below, it was a mixed week for the portfolios, with two of the three ending lower. Portfolio 2 saw gains thanks to strong performances from its financial companies, which were lifted by solid results from American banks. However, Portfolio 1 was dragged down by Tesla’s lackluster earnings report and the overall drop in the technology sector. Portfolio 3 also experienced a decline as the gains in its financial companies were outweighed by the decline in technology companies.

As you can see in the chart below, it was a mixed week for the portfolios, with two of the three ending lower. Portfolio 2 saw gains thanks to strong performances from its financial companies, which were lifted by solid results from American banks. However, Portfolio 1 was dragged down by Tesla’s lackluster earnings report and the overall drop in the technology sector. Portfolio 3 also experienced a decline as the gains in its financial companies were outweighed by the decline in technology companies.

Looking ahead to the upcoming week, the focus will be on the second-quarter earnings reports of many big technology companies. Investors will be hoping for more impressive results compared to this past week. If earnings disappoint, it could lead to share price declines for many technology firms.

Additionally, the Fed’s update on the US benchmark interest rate will be closely watched. While an interest rate increase is widely expected after it was left unchanged in the last June session, investors will be more interested in the path the Fed outlines going forward. The central bank’s approach will likely be data-driven, meaning they will consider relevant economic data to determine their future policy decisions. Hopefully the data indicates inflation continues to fall. 😊

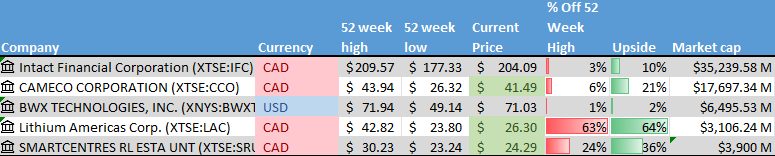

Companies on the Radar

After weeks of remining unchanged, my Radar List has now dropped to just two companies. I am still working my way through deeper dives on each company but so far, I like what I see in each company. Cameco and BWX should benefit from a tailwind if nuclear energy gains more prominence as an alternative energy option. As governments focus on reducing carbon emissions and addressing climate change, nuclear power is being considered for its low greenhouse gas emissions compared to traditional fossil fuel-based sources.

After weeks of remining unchanged, my Radar List has now dropped to just two companies. I am still working my way through deeper dives on each company but so far, I like what I see in each company. Cameco and BWX should benefit from a tailwind if nuclear energy gains more prominence as an alternative energy option. As governments focus on reducing carbon emissions and addressing climate change, nuclear power is being considered for its low greenhouse gas emissions compared to traditional fossil fuel-based sources.

- Cameco (TSX: CCO): A large Canadian company involved in uranium mining, sales, and the construction of nuclear reactor components.

- BWX Technologies (NYSE: BWXT): A mid cap size American company specializing in the construction and sale of nuclear components to customers worldwide, including the US Navy.

The Radar Check was last updated July 21, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended July 21, 2023: DOWN ![]()

- After years of delays, Tesla’s first Cybertruck finally came off their Texas giga-factory assembly line, two years later than planned. The Cybertruck prototype was first unveiled in 2019 and after a few stumbles has finally started shipping. It will take a while to fulfill all the orders if rumours are true that 2 million people made $100 refundable deposits. Even if half the depositors back out, that is still a huge backorder.

Separately, Tesla is facing a National Highway Traffic Safety Administration (NHTSA) special crash investigation into a fatal accident. The Tesla involved is suspected of using Tesla’s advanced driver assistance systems when it collided head on with another vehicle.

Tesla reported strong revenue growth thanks to its strategy price cuts to boost sales. However, their margins hit a three year low of 18.9%, down from 25.9% a year ago. What was not in the report is the boost from other electric vehicle (EV) manufacturers adopting Tesla’s American Charging Standard. That revenue should appear in their next earnings report.

Finally, Tesla is prepared to make additional price cuts to drive sales if the economy stalls. The lower prices would be offset by the tax cuts provided in the US government’s Inflation Reduction Act. - Amazon is building a satellite launch facility for the launching of its planned 3,200 low Earth-orbiting satellites that will create a network to beam broadband internet globally. Amazon will spend a US$ 120 million on the facility as part of their US$ 10 billion satellite program, named Kuiper. The facility is expected to receive its first batch of satellites for processing in 2025.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Andlauer Healthcare Group Inc (TSX: AND)

BCE Inc (TSX: BCE)

US $

BSR Real Estate Investment Trust (TSX: HOM.U)

Quarterly Reports

Tesla, Inc.

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their second quarter 2023 financial results on July 19, 2023

- Revenue of $24,927 for the three months ended June 30, compared to $16,934 for the same period in 2022. An increase of over 47%.

- Net income of $2,614 for the three months ended June 30, compared to net income of $2,269 in the same period in 2022.

- Diluted earnings per ordinary share of $0.78 for the three months ended June 30, compared to earnings of $0.65 per share for the same period in 2022.

Portfolio 2

Portfolio 2 for the week ended July 21, 2023: UP ![]()

- MongoDB (NASD: MDB) announced they have extended their partnership with Microsoft to help customers move their MongoDB applications to Microsoft’s Azure cloud computing platform.

- Telus (TSX: T) signed a multi year agreement with Canada Soccer to become their Official Telecommunications, Digital Health, and Home Security Partner for the Federation and its National Teams. Hopefully this deal will turn out a lot better for Canada Soccer than a deal with Canada Soccer Business which all but hid the national teams from Canadian soccer fans.

As well, Telus teamed up with the Victoria Cool Aid Society to provide a second mobile health van to provide aid to the homeless in Victoria. - Guardant Health (NASD: GH) announced their Guardant Reveal molecular residual disease (MRD) test will be covered by Blue Cross and Blue Shield of Louisiana. This is a blood test that detects circulating tumor DNA in blood after treatment, including surgery, to help identify cancer patients with residual or recurring disease who may benefit most from further therapy or surveillance.

- The House of the Mouse, Walt Disney Company (NYSE: DIS) has spoken with both the NFL and NBA about the two leagues becoming minority investors in Disney’s ESPN sports broadcasting unit.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Alimentation Couche-Tard Inc (TSX: ATD)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week, except for per share data.

Portfolio 3

Portfolio 3 for the week ended July 21, 2023: DOWN ![]()

- Microsoft finally was able to sign an agreement with Sony that would keep the ‘Call of Duty’ game on PlayStation devices for the next 10 years. The agreement was necessary for Microsoft to close its acquisition of Activision Blizzard (NASD: ATVI). Now, to get the OK from British regulators. Microsoft and Britain’s competition regulator, the Competition and Markets Authority (CMA) have been granted a three-month extension to resolve their differences so Microsoft and Activision can close their deal.

While potentially dodging the Activison bullet, Microsoft now finds itself in the crosshairs of the European Unions’ (EU) anti trust regulator, the European Commission (EC). The last time Microsoft was under investigation by the EC was in 2008 over Internet Explorer (now known as Edge) imbedded in Windows. This time its over their Teams workplace messaging platform, which until April automatically enrolled users in Teams.

Finally, Microsoft’s share price hit an all time high this past week after they announced they will charge at least 53% more for its Microsoft 365 plans that included AI.

Activity

Bought Lithium Americas (TSX: LAC): Investing in a company with no revenues is riskier, but it also provides a significant opportunity due to the growing demand for lithium in the expanding EV market.

Lithium is a crucial component in EV batteries, and as more countries and industries shift towards EVs, the demand for lithium is expected to surge. The company’s existing contract to supply lithium to GM (NYSE: GM) for their Ultium batteries adds credibility to their potential in the EV market.

The company’s plan to split into two separate entities, Lithium Americas Corp, and Lithium Argentina, provides investors with exposure to different geographic regions and markets. The US-based Lithium Americas Corp will retain the agreement with GM and stands to benefit from the US government’s desire for domestic manufacturers and supply chains, potentially gaining access to tax breaks and financial incentives provided by the US government.

Moreover, given the global push towards renewable energy and clean transportation, the Argentine operation can provide opportunities in the international market as well.

While this investment carries more risk, it does offer an opportunity to capitalize on the growing global demand for lithium. However, I expect the share price to be quite volatile as the industry and company matures.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

goeasy Ltd (TSX: GSY)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.