Items that may only interest or educate me ….

US debt ceiling increased, Canadian economic news, US economic news, EU economic news, OPEC+ lowers oil production …

With the resolution of the US debt ceiling issue, attention has now shifted back to the ongoing global battle with inflation. While recent data in both Canada and the US has shown a decline in inflation numbers, indicating some progress, it is important to note that the fight against inflation is far from over. Despite this, both countries have demonstrated strong economies, particularly the US, as evidenced by their robust job numbers.

In terms of monetary policy, the Bank of Canada (BoC) recently decided to raise the Canadian benchmark rate to 4.75%. Looking ahead to the upcoming week, it remains uncertain whether the US Federal Reserve (Fed) will follow suit and raise the US rate or opt to pause their hiking. Personally, I am hopeful that the Fed will pause their rate hikes. Regardless of the decision they make, it is likely that interest rates will remain at their current levels for some time before any potential decrease.

Canadian economic news

Interest rate hike

The Bank of Canada (BoC) has raised its key interest rate by 0.25% to 4.75%, marking the first increase in the overnight interest rate since it was paused at 4.50% in January 2023. This decision is a response to the higher-than-expected Gross Domestic Product (GDP) growth of 3.1% for the first three months of 2023. Furthermore, inflation has accelerated to 4.4% on a yearly basis, marking the first increase since June 2022 and well above the BoC’s target of 2%. With this increase, the interest rate is now at its highest level since May 2001.

The BoC’s decision is influenced by the persistence of high global inflation, despite lower energy prices. Earlier in the week, the Reserve Bank of Australia hiked its benchmark interest rate to 4.1%, an eleven-year high, in their fight with inflation. In the US, the world’s largest economy, inflation remains elevated despite a slowdown in economic growth. Both the Canadian and US economies are being driven by strong consumer spending and tight job markets. In Canada specifically, various goods and services continue to be priced higher than estimated, indicating that demand is still exceeding supply.

This latest interest rate increase reflects the BoC’s efforts to address the rising and persistent inflationary pressures. The central bank also indicated that further interest rate hikes are possible in the future, possibly as early as their next meeting in July. The BoC faced criticism in 2022 for not acting sooner in response to rising inflation. This time the BoC is proactively attempting to tackle inflation.

As a result of the BoC’s interest rate hike, Canadian banks immediately increased their respective lending rates by 0.25%. Not only do higher interest rates make any form of a loan or mortgage more expensive, but they also dampen the growth prospects of technology firms and other high growth-oriented companies.

Canada’s trade balance

Overshadowed by the interest rate hike, Canada’s exports surged by 2.5% in April, reaching an all-time high by volume, while imports saw a slight decline of 0.2%. As a result, Canada recorded a surplus of C$ 1.94 billion, more than double the anticipated C$ 900 million.

The leading exports included metal and non-metallic mineral products, such as gold (up 13.6%), motor vehicles (up 7.4%), and energy products (up 6.4%). On the other hand, there was a drop in exports of farm and fish products (down 6.4%) and consumer goods (down 5.5%).

Imports experienced a decline for the third consecutive month, primarily driven by a decrease in energy, metal ores, and non-metallic minerals. However, there were significant gains in imports of aircraft equipment (up 17.4%) and consumer goods (up 4.0%).

Unsurprisingly, the United States remained Canada’s largest trading partner both in terms of exports and imports. Export to the US increased by 4.4%, accounting for 76% of total exports, while imports from the US decreased by 0.4%, making up nearly 64% of total imports.

The report indicates a robust Canadian economy that has surpassed pre-pandemic levels. However, the question remains whether Canada can sustain strong export numbers throughout the summer.

Jobs data

Statistics Canada’s jobs data showed that the economy unexpectedly lost 17,300 jobs in May, representing a decline of 0.1%. Employment gains have been decelerating since February and eventually turned into a net loss in May. However, when compared to the previous year, employment is still up by 1.8%. The unemployment rate also increased by 0.2% to 5.2% in May, marking the first monthly rise since August 2022. Analysts had anticipated a gain of 23,200 jobs and an unemployment rate of 5.1% for May. Finally, hourly wages for permanent, full-time employees saw a year-over-year increase of 5.1%, slightly lower than the 5.2% rise observed in April.

These economic indicators suggest that the BoC’s rate hikes are starting to have an effect. The question now is whether this impact is sufficient for the BoC to pause the rate increases at their upcoming July meeting.

US economic news

The US debt ceiling issue was resolved last weekend when President Biden signed the bill, suspending the debt ceiling for two years, after which they will have to address it again. Neither side appeared overly enthusiastic about the deal, but both parties claimed victory. President Biden and the Democrats celebrated avoiding a historic crisis, while the Republicans touted their success in curbing spending (conveniently ignoring their previous willingness to spend under the previous administration).

The looming question now is whether the Federal Reserve (Fed) will increase the US benchmark interest rate at the upcoming meeting of the Federal Open Market Committee (FOMC), the body responsible for determining the interest rate. Could the Bank of Canada’s recent rate hike be a hint of the Fed’s next move? We will have to wait and see.

In other news, the weekly jobless claims data revealed a significant jump in unemployment claims, increasing by 28,000 to 261,000. This marks the highest level in eighteen months and indicates a slowdown in the once robust US job market.

Meanwhile, the CBOE Volatility index fell by 2.01% to 13.66, suggesting a moderate level of market volatility. Please see the April 21 Weekly Update for an explanation of the VIX.

EU economic news

According to the latest economic data for the first three months of 2023, the European Union (EU) has officially entered a technical recession. A recession is typically defined as two consecutive quarters of economic contraction, and following a decline in the last quarter of 2022, the EU experienced a further loss of 0.1% in the first quarter of 2023. This slowdown was primarily attributed to a significant decrease in German output and government spending, as well as a 4.6% drop in output in Ireland.

Despite the challenging economic conditions, there are some positive indicators. Employment showed a slight increase of 0.6%, suggesting some resilience in the labor market. Additionally, investment saw a rise of 0.6%, which could potentially contribute to future economic growth. Furthermore, inflation appears to be cooling down, which can alleviate some economic pressures.

Analysts maintain an optimistic outlook for the EU economy, expecting growth to rebound in the second quarter. However, it is noteworthy that analysts believe the EU central bank will still proceed with raising its benchmark interest rate following the June 15 meeting, despite the technical recession. This suggests that the central bank is prioritizing inflation control and financial stability over the short-term recessionary conditions.

OPEC+ lowers oil production

At the OPEC+ meeting held on June 3-4, Saudi Arabia made the decision to unilaterally reduce its crude oil production by 1 million barrels per day. This move aims to limit the global oil supply and support higher oil prices. Meanwhile, the other OPEC+ members have agreed to maintain their current production levels, as previously agreed upon in April, and extend those levels through 2024.

Saudi Arabia’s decision to cut production is driven by their goal of keeping oil prices above $75 per barrel. They are concerned about a potential slowdown in the global economy, which could lead to reduced consumption as consumers and businesses scale back their expenses. For instance, individuals might opt for stay-at-home vacations instead of traveling by car or plane.

The revenue generated from oil sales will be utilized by Saudi Arabia to transform the country into a global supply chain hub, develop green technologies, and support their ambitious “city of tomorrow” project known as Noem. These plans reflect Saudi Arabia’s efforts to diversify its economy and reduce its dependence on oil.

* OPEC+ members: Algeria, Angola, Azerbaijan, Bahrain, Brunei, Congo, Equatorial Guinea, Gabon, Iraq, Kazakhstan, Kuwait, Malaysia, Mexico, Nigeria, Oman, Russia, Saudi Arabia, Sudan, South Sudan, and United Arab Emirates.

With all those economic updates out of the way, let’s see what happened this past week….

Weekly Market Review

Monday: With the US debt ceiling crisis in the rear-view mirror, investors’ attention turned to next week’s Fed meeting. Concerns over another US interest rate hike, led to a fair bit of uncertainty in the markets, and the markets do not like uncertainty. Accordingly, the four major North American indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – all ended lower. As for oil companies, it was a good day after Saudi Arabia announced it would reduce its supply of crude oil by 1 million barrels a day starting in July.

In Canada, stronger than expected Canadian economic data had investors wondering if the BoC may be forced to increase the Canadian benchmark interest rate later this week. Despite the announced Saudi Arabia oil production cut that boosted the price of oil, energy companies on the TSX still saw share prices fall. In trading, Technology and Consumer Cyclicals were the only Canadian sectors to advance, while the biggest drops were by Financials and Consumer Staples.

In the USA, mixed economic news may turn out to be good news for the Fed and enable them to hold off on an increase to the interest rate. Investors are betting the Fed will not increase the interest rate, despite the hawkish tone from Fed members over the last few weeks. In trading, Telecommunications Services and Utilities had the biggest gains in the American sectors. Industrials and Financials had the biggest drops.

Tuesday: All four major indexes closed the day higher suggesting investors were optimistic. However, oil prices retreated from their previous day’s increase as optimism surrounding a potential supply cut diminished.

In Canada, despite the falling oil prices, the TSX spent the day on an upward trajectory in anticipation of the BoC’s interest rate announcement tomorrow. The growth-oriented sectors Technology and Consumer Cyclicals were the best performers of the Canadian sectors, while Utilities, Industrials and Healthcare were the only sectors to end lower.

In the US, the American indexes bounced above and below the breakeven line as investors await tomorrow’s Consumer Price Index. The top performers in the American sectors were the Financials and Consumer Cyclicals, while Healthcare and Consumer Staples were the only sectors to fall.

Wednesday: After the BoC unexpectedly raised its benchmark interest rate, the fear of higher interest rates led to a drop in all indexes except for the blue chip DJIA. A slowdown in Chinese exports raised concerns of a global recession further dampening investors optimism.

In Canada, the TSX dropped after the BoC raised the key rate to 4.75%. Higher oil prices lifted energy companies which prevented the TSX was falling further. On Bay Street, Energy and Consumer Staples had the biggest gains of the Canadian sectors, while Technology and Consumer Staples fell the furthest.

In the US, investors took profits after a bullish May for the mega cap technology companies, sending the tech heavy Nasdaq and S&P lower. After Canada’s surprise interest rate increase, investors now nervously await next week’s update by the Fed. On Wall Street, Energy and Utilities were the biggest winners of the American sectors, while interest sensitive, Technology and Consumer Staples had the biggest drops.

Thursday: Another day of mixed indexes, with the TSX retreating while all three American indexes advanced. Investors were uncertain whether way the Fed would pause rate increases or increase the rate after unexpected rate hikes in Australia and Canada.

In Canada, Wednesday’s surprise interest rate hike, with the likelihood of an additional 0.25% increase in July, dragged the TSX down. Basic Materials (miners and fertilizer manufacturers) and Utilities were the only two Canadian sectors to advance, while Industrials and Telecommunications Services suffered the biggest drops.

In the US, other than a rebound in technology companies, investors essentially sat on the sidelines ahead of next week’s Fed meeting. Among the American sectors, Consumer Cyclicals and Technology led the charge, while Financials and Energy slipped.

Friday: Once again the TSX ended lower, while the three American indexes ended higher. It was a relatively quiet day in the markets as investors await a slew of news next week, including the latest American inflation report and the latest interest rate decision by the Fed. Oil prices ended lower after China reported disappointing economic data leading to concerns about lower demand.

In Canada, the TSX was dragged down by a recent jobs report that indicated the country shed over 17,000 jobs and unemployment rose for the first time in nine months. The loss of jobs could signal the start of an economic slowdown while inflation remained high. Not a good combination. In the Canadian sectors, Technology was the only sector to end higher. Consumer Staples and Industrials fell the farthest.

In the US, the rally that has lifted the mega cap technology companies is beginning to spread beyond a group of mega cap technology companies and other high growth companies. Small cap companies were late to the rally but have recently started to gain upward momentum. In trading, Technology, Consumer Cyclicals and Consumer Staples were the only American sectors to advance, while Basic Materials and Utilities had the biggest declines.

Weekly Market and Portfolio Review

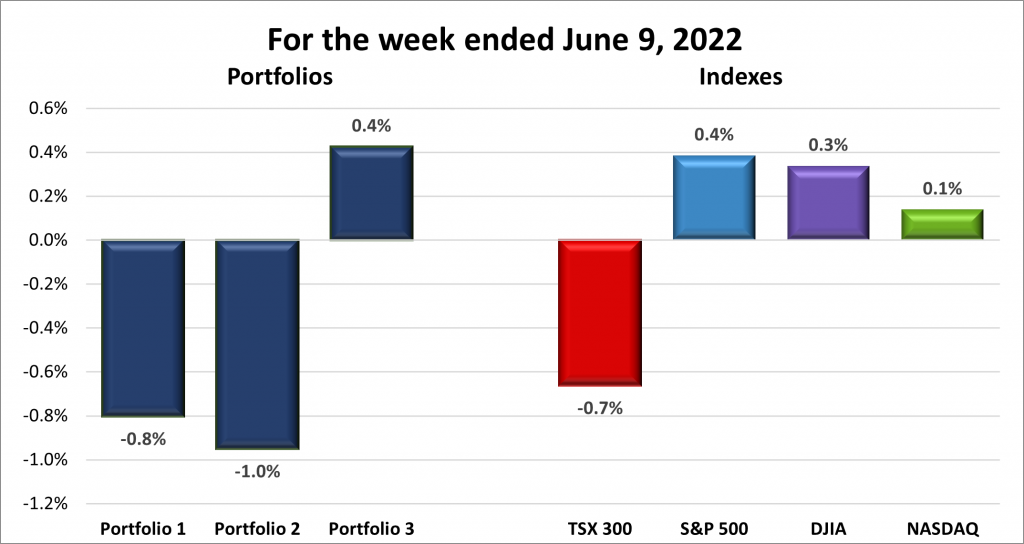

For the week, the TSX (SPTSX) fell 0.7%, the S&P 500 (SPX) gained 0.4%, the DJIA (INDU) increased 0.3% and the Nasdaq (CCMP) posted a seventh straight weekly gain, this time rising 0.1%.

![]() It was a positive week for the American markets, as all three indexes recorded gains, as shown in the chart above. The Nasdaq has been particularly strong, with a 30% increase since its low point in December, indicating a bull market trend in recent weeks. The S&P also experienced a mid-week rally, pushing it up by over 20% since its October 2022 lows, officially entering a bull market. The DJIA is not far behind, with an 18% increase since October.

It was a positive week for the American markets, as all three indexes recorded gains, as shown in the chart above. The Nasdaq has been particularly strong, with a 30% increase since its low point in December, indicating a bull market trend in recent weeks. The S&P also experienced a mid-week rally, pushing it up by over 20% since its October 2022 lows, officially entering a bull market. The DJIA is not far behind, with an 18% increase since October.

During the past week, the American indexes were primarily driven by a small group of mega-cap technology companies. These companies, fueled by the optimism surrounding artificial intelligence (AI) and the potential pause in rate hikes by the Fed, contributed to the market’s positive performance.

In contrast, the TSX has been underperforming in comparison to the technology-heavy S&P and Nasdaq indexes. This is mainly due to the limited presence of mega cap technology companies in Canada, which hampers the index’s ability to make gains like its American cousins. The TSX is predominantly composed of the Financials, Energy, and Basic Materials sectors, accounting for 58% of the index. The Financial sector has been affected by higher interest rates, while the sluggish economic recovery in China has led to lower commodity prices, which have traditionally been a key driver for the TSX.

![]() Last week was tough for the portfolios, as only one of them experienced a gain in value. Portfolio 1 faced a decline due to the drop in bank stocks following the Bank of Canada’s decision to raise the interest rate. The possibility of another rate increase as early as July further impacted the portfolio. However, the ongoing rally in American mega-cap companies helped limit the overall decline.

Last week was tough for the portfolios, as only one of them experienced a gain in value. Portfolio 1 faced a decline due to the drop in bank stocks following the Bank of Canada’s decision to raise the interest rate. The possibility of another rate increase as early as July further impacted the portfolio. However, the ongoing rally in American mega-cap companies helped limit the overall decline.

Similarly, Portfolio 2 was negatively affected by its holdings in the Financials sector, which contributed to the downward movement. Unlike Portfolio 1, Portfolio 2 did not have multiple Technology sector companies to offset the decline.

On a more positive note, Portfolio 3 managed to advance during the week, primarily driven by the strong performance of Shopify(TSX: SHOP). The upcoming week is expected to be eventful, with the release of key data on US inflation and retail sales. Of significant importance is the update on the US interest rate, and a potential pause in its increase would be favorable for the market.

Companies on the Radar

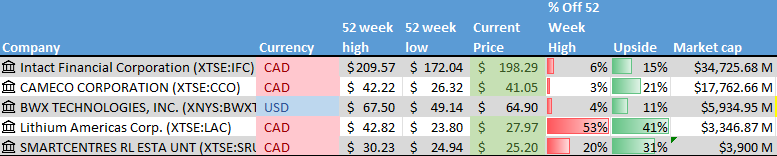

I have decided to remove Amphenol (NYSE: APH) from my radar list and add Lithium Americas (TSX: LAC) instead. Based on my research, it seems that the world may face a shortage of lithium to meet the increasing demand for electric vehicles (EVs), possibly by 2025. Furthermore, General Motors recently invested US$ 650 million in LAC to secure a lithium supply for their Ultima EV batteries. Although LAC carries risks, it is worth a closer examination so I will place it on my radar list alongside the companies below.

I have decided to remove Amphenol (NYSE: APH) from my radar list and add Lithium Americas (TSX: LAC) instead. Based on my research, it seems that the world may face a shortage of lithium to meet the increasing demand for electric vehicles (EVs), possibly by 2025. Furthermore, General Motors recently invested US$ 650 million in LAC to secure a lithium supply for their Ultima EV batteries. Although LAC carries risks, it is worth a closer examination so I will place it on my radar list alongside the companies below.

- Intact Financial (TSX: IFC): A Canadian mid-size insurance company that offers home, car, and business insurance in Canada, the US, and the UK.

- Cameco (TSX: CCO): A large Canadian company involved in uranium mining, sales, and the construction of reactor components.

- BWX Technologies (NYSE: BWXT): A mid cap size American company specializing in the construction and sale of nuclear components to customers worldwide, including the US Navy.

- Smartcentres Real Estate Investment Trust (TSX: SRU.UN): A mid size fully integrated REIT that owns and manages a number of income producing shopping centres and retails spaces throughout Canada.

The Radar Check was last updated June 9, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended June 9, 2023: DOWN ![]()

- Apple (NASD: AAPL) announced their latest device to take your money – the Vision Pro augmented reality headset – at last week’s Apple Developers Conference. It will be available for US$ 3,499 starting early in 2024, initially in the US before spreading to other countries.

- Unity Software (NYSE: U) announced a new partnership with Apple to port iOS apps to Apple’s visionOS operating system for their new Vision Pro2 mixed-reality headset.

- General Motors (NYSE: GM) announced they plan to spend up to US$ 1 billion to re-tool two of their manufacturing plants in Flint, Michigan. The upgrades will be at facilities that produce GM’s combustion engine heavy duty trucks. Apparently there still is demand for conventional engine trucks. 😊

In other GM news, the company announced it planned to use Tesla’s EV charging network. With the three largest automakers (Tesla (NASD: TSLA), GM and Ford (NYSE: F)), accounting for almost 60% of the North American EV market, it will be very hard for any company to compete with Tesla for the charging market. - Segueing into Tesla, the company is eligible for government subsidies to build more charging stations if they include the Combined Charging System adapters so other EVs can use the Tesla charging devices.

Tesla has been in talks with Spanish government officials about the possibility of building a car factory in Valencia, Spain. All this good news certainly did not hurt the share price. 😊 - According to the Wall Street Journal, Amazon (NASD: AMZN) is considering advertising supported version of their Prime Video service. They are contemplating making the current Prime Video included with a Prime subscription ad supported, with an additional fee for an ad free service.

- CrowdStrike (NASD: CRWD) announced a new set of cloud security capabilities featuring their “1 click XDR” that automatically identifies and deploys their Falcon security agent to secure unprotected cloud assets. This will help secure any computing and network assets that slip through the cracks.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

DocuSign, Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their first quarter 2024 financial results on June 8, 2023

- Revenue of $661,388 for the three months ended April 30, compared to $588,692 for the same period in 2022. An increase of over 12%.

- Net income of $539 for the three months ended April 30, compared to a net loss of $27,373 in the same period in 2022.

- Diluted earnings per ordinary share of $0.00 for the three months ended April 30, compared to a loss of $0.14 per share for the same period in 2022.

Portfolio 2

Portfolio 2 for the week ended June 9, 2023: DOWN ![]()

- Microsoft (NASD: MSFT) announced they were bringing their AI capabilities to US government agencies that use Microsoft’s Azure Cloud Services platform. Government customers will be able to use it for a variety of uses including content generation, coding assistance, and summarization.

- Alimentation Couche-Tard (TSX: ATD) appointed Filipe Da Silva as Chief Financial Officer to succeed Claude Tessier, who plans to retire, effective July 1.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

No C$ dividends this past week.

US $

Microsoft Corp. (NASD: MSFT)

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended June 9, 2023: UP ![]()

- Alvopetro Energy (TSXV: ALV) began production on another of their natural gas fields in Brazil. The well is now generating 1.3 million standard cubic feet per day.

- Fortuna Silver Mines (TSX: FVI) reported the death of a contractor at one of their underground mines in Peru. The nature of the accident has not been revealed but no other personnel were injured.

- Shopify closed on the sale of its Shopify Logistics unit to Flexport. In exchange, Shopify now has a 13% stake in Flexport.

- Brookfield Asset Management (TSX: BAM) will sell it 49.5% interest in New Zealand’s One New Zealand for C$ 1.1 billion to New Zealand based Infratil. One New Zealand is the countries second largest mobility operator.

BAM also announced they were buying payments provider Network International for US$ 2.5 billion, as part of their efforts to expand their payments footprint in the Middle East and Africa.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

No C$ dividends this past week.

US $

Microsoft Corp. (NASD: MSFT)

Quarterly Reports

No quarterly reports this past week.