The North American stock markets have had a good run through the first two months of 2024. March has a tough act to follow but the month has a reputation for being a strong month for the North American stock markets, with historical trends showing positive movement more often than not. But remember, past performance is not a guarantee of future results.

Investor enthusiasm over all things related to artificial intelligence should continue to drive the markets higher. With fourth quarter earnings almost over, investors will now cast their eyes towards the Federal Reserve. Each bit of economic news, as well as speeches from Fed officials, will be dissected in an attempt to determine when the rates could begin to fall. I am sure there will be lots of ups and downs with each bit of news, hopefully a lot more ups than downs. So, buckle up, the rollercoaster is about to leave the platform.

Before the ride begins, let’s see what happened this past week….

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, US government shutdown avoided, NVIDIA

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Gross Domestic Product (GDP)

Statistics Canada’s latest report reveals the country’s economy expanded by 1.0% in the fourth quarter on a year-over-year basis, surpassing analysts’ estimates of 0.8% growth. This performance marks a significant improvement compared to the third quarter’s contraction of 1.1%. On a monthly basis, however, GDP growth stalled in December, remaining flat following two months of growth, and falling short of the anticipated 0.2% growth. Year-over-year, the GDP for December increased by 1.1%. Preliminary figures for January look promising, with an advance estimate indicating the economy grew by 0.4%.

This economic expansion reduces the urgency for the BoC to cut the benchmark interest rate. Given the ongoing growth, it is probable that the interest rate will stay at its 22-year high of 5% for the next few months as the BoC focuses on bringing inflation closer to their 2% target. Analysts now anticipate that the central bank may begin to lower the rate after their June meeting, based on the economy’s current strength and inflation’s downward trajectory.

Canadian market volatility

This past week Canada’s volatility index (VIXC) or ‘fear gauge,’ represented by the TSX 60 VIX, rose to 12.53, a slight increase from the previous week’s 11.76.

A rise in the VIXC suggests that investors are feeling a less certain about future market movements. It does not necessarily predict a downturn; it just means people are expecting stock prices to be more erratic.

The VIXC gauges volatility within the Canadian stock markets, with readings above 20 generally viewed as ‘high’ and those below 20 as ‘low.’ The current reading of 12.53 sits on the lower end of the spectrum, indicating a prevailing sense of confidence among investors in the Canadian markets.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Personal Consumption Expenditures (PCE)

The Bureau of Economic Analysis’ January Personal Consumption Expenditures (PCE) report showed a 0.3% increase in prices, following a 0.2% rise in December. Core PCE, which excludes the more volatile categories of food and energy, rose by 0.4% in January, a significant increase from December’s 0.2% uptick. Both these figures met analyst expectations. Year-over-year, the PCE price index saw a 2.4% increase in January. Over the same 12-month period, the core PCE price index recorded a 2.8% gain in January, slightly down from December’s 2.9% increase.

This annual increase in PCE marks smallest gain in three years, while the monthly increase in core PCE was the biggest increase since the previous February. Although the slowdown in overall inflation growth may not be as much as the Fed might have preferred, investors are hopeful it is sufficient to keep the prospect of an interest rate cut in June alive.

Gross Domestic Product

The Department of Commerce’s second estimate for the fourth quarter Gross Domestic Product (GDP) indicated that the American economy expanded at an annualized rate of 3.2%. This marks a significant slowdown from the third quarter’s growth rate of 4.9%. The revised figure, or second estimate, slightly adjusts the initial ‘advance’ estimate released in January, which had suggested a 3.3% growth rate.

The deceleration in growth during the quarter can primarily be attributed to a slowdown in private inventory investment, alongside declines in federal government spending and consumer expenditures.

Over the course of 2023, the GDP witnessed a 2.5% increase compared to the previous year. This growth was driven predominantly by a rise in consumer spending, alongside increased expenditures by federal, state, and local governments, and an increase in non-residential fixed investment. Conversely, reductions were recorded in residential fixed investment and private inventory investment.

American market volatility

The CBOE Volatility Index (VIX), often seen as a measure of market fear and uncertainty, experienced a marginal decline of 0.64 points from 13.75 to 13.11. This decline suggests a slight increase in investor confidence and a reduction in expectations for market volatility in the near term. Historically, a decrease in the VIX often signals a bullish outlook among investors, anticipating steadier or rising stock prices in the near term.

Consumer Confidence Index

The Conference Board’s Consumer Confidence Index (CCI) for February reported a surprising decline, falling to 106.7 from a revised 110.9 in January, a six-month peak. This decrease, the first in three months, was significantly below the analyst expectations of 115. One has to wonder if this is just a blip in an upward trend given the resilient economy, strong job market, rising stock market, and the anticipation of falling interest rates later in the year. Although confidence has shown improvement since late last year, buoyed by decelerating inflation rates, it remains significantly lower than pre-pandemic levels.

One potential explanation for this unexpected dip in consumer sentiment may be the prevailing political climate, particularly the upcoming presidential election, where both candidates have failed to attract favorable opinions from the majority.

The CCI is a vital economic indicator, gauging the optimism or pessimism consumers feel about the economy and their personal financial situation. This sentiment directly influences their spending decisions, making the CCI a key predictor of economic health. The Fed closely monitors this index, as high consumer confidence suggests that people feel secure financially and are likely to spend more, driving economic growth. Conversely, low consumer confidence, indicating a tendency towards saving rather than spending, can signal an economic slowdown.

Consumer Sentiment Index

The University of Michigan’s final Consumer Sentiment Index (CSI) for February was reported at 76.9, marking a slight decrease from January’s reading of 79.0 but showing a significant improvement of 14.9% over February 2023’s figure of 66.9. This final February reading fell short of the preliminary estimate of 79.6, which matched with analysts’ predictions, and is still below the historical average.

Despite the marginal dip from January, consumer sentiment in February remained healthy, supported by several key factors. These include easing inflation pressures, a resilient economy and job market, appreciating stock market values, and expectations of decreasing interest rates starting in the summer. This combination of factors suggests that while there was a slight month-over-month decline, the overall consumer outlook remains positive, buoyed by the anticipation of favorable economic conditions.

US government shutdown avoided

Once again, members of the US Congress found themselves in a game of brinkmanship before finally reaching a consensus to extend government funding beyond March 1, 2024. This agreement postpones the expiration date for six crucial funding bills—covering the Departments of Agriculture, Justice, Interior, Veterans Affairs, and other federal entities—from March 1 to March 8. Furthermore, the deadline for the subsequent six bills, which finance the Departments of Defense, Labor, Homeland Security, and additional federal agencies that were initially set to expire on March 8, has been extended to March 22. This delay provides lawmakers the necessary time to review and debate the full-year funding legislation.

The Senate Majority Leader, the Speaker of the House, and President Biden negotiated the spending bills necessary to avoid a partial government shutdown. These twelve bills are designed to fund government programs through the end of the fiscal year, which concludes on September 30, 2024. This marks the third instance within a year that efforts to authorize funds to keep the US government operational approached the deadline.

NVIDIA

NVIDIA (NASD: NVDA) has recently captured investor attention, especially following its impressive fourth-quarter earnings report that exceeded expectations and offered a bullish forecast for 2024. The company’s share price has surged over 400% since January 2, 2023, elevating it to the third largest company with a market capitalization (number of shares outstanding X share price) of over US$ 2 trillion.

The surge in Nvidia’s revenue is largely driven by significant investments from major tech companies racing to integrate artificial intelligence (AI) capabilities and secure a position in the burgeoning AI landscape. These companies, with their substantial resources, are not only able to afford Nvidia’s chips but also recognize the strategic importance of not falling behind in this technological revolution. The ongoing investment in AI is translating into tangible applications and, ultimately, substantial revenue streams, highlighting AI’s dual role as both a strategic investment during growth periods and a tool for enhancing efficiency and reducing costs during economic downturns.

With its meteoric rise, I thought it would be interesting to take a closer look at the factors that have captured investors’ attention and propelled the company and its share price to new heights.

NVIDIA’s share in the advanced semiconductor industry is significant. Its focus on AI, high-performance computing, and graphics processing units (GPUs) has propelled it to the forefront. While exact market share percentages can fluctuate, NVIDIA’s dominance in specific segments is undeniable.

Here are some key points about NVIDIA’s position in the advanced semiconductor landscape:

- AI and Deep Learning: NVIDIA’s GPUs are widely used for AI training and inference. Their CUDA architecture and specialized hardware (such as Google’s Tensor Cores) make them indispensable for machine learning tasks. Many data centers, research institutions, and companies rely on NVIDIA GPUs for AI workloads.

- Automotive: The NVIDIA DRIVE platform is integral to the development of autonomous vehicles, providing essential hardware and software for self-driving technologies. Customers include Audi and Volkswagen.

- Gaming: Nvidia continues to dominate the gaming sector with its GeForce series GPUs, especially with the release of the RTX 30 series GPUs, attracting a broad customer base including major hardware manufacturers and creative professionals. Customers include computer hardware manufacturers ASUS and MSI, as well as many other video editors and 3D artists.

- Data Centers: GPUs like the A100 are preferred for scientific simulations, data analytics, and deep learning applications, boasting unmatched performance and efficiency. Their customers includes the big three cloud providers and data centre companies Amazon, Microsoft and Google (NASD: GOOGL).

- Edge Computing: NVIDIA’s Jetson platform provides AI capabilities at the edge (in devices like drones, robots, and IoT devices). It enables real-time inference without relying on cloud servers.

- Healthcare and Life Sciences: Nvidia’s technology supports medical imaging, drug discovery, and genomics research, partnering with leading healthcare companies such as GE Healthcare, Siemens Healthineers, and others.

- Partnerships and Collaborations: NVIDIA collaborates with other semiconductor companies, research institutions, and software developers. For example, their partnership with Taiwan Semiconductor Manufacturing (NYSE: TSM) ensures efficient production of advanced chips.

Remember that the semiconductor industry is dynamic, and market shares can change based on technological advancements, competition, and global trends. Past performance does not guarantee future performance, especially with many companies looking to carve out a piece of Nvidia’s market share. However, NVIDIA’s impact and influence remain significant in shaping the future of advanced computing and AI. The company’s success is a testament to its strategic focus on key technological advancements and its ability to cater to diverse, high-demand sectors.

Weekly Market Review

Monday: the four major North American indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – stumbled out of the gate to start the week, with each index ending the day in the red. Oil prices ended higher as demand in Europe for diesel fuel increased.

In Canada, lower commodity prices led to the drop in the TSX today. This week investors will be watching the earnings reports from Canada’s big six banks. Investors will be watching the results to get an idea how well the Canadian economy is performing. Strong reports from the banks are a good indicator that the economy is performing reasonably well. In trading, Consumer Staples, Industrials and Energy were the only sectors to end higher, while Utilities and Telecommunications Services saw the biggest declines.

In the US, it was a quiet day in the markets with no major news to drive the markets. As fourth quarter earnings wrap up, analysts and investors await the PCE index reading later this week to see if inflation continues to fall. In trading, Consumer Cyclicals and Energy were the only sectors to advance, while Utilities and Telecommunications Services experienced the biggest setbacks.

Tuesday: A mixed day for the indexes as investors took profits or sat on the sidelines ahead of the latest US PCE inflation report. Oil prices dipped slightly despite OPEC+ members indicating they were considering extending their voluntary cutback on oil production.

In Canada, the TSX posted its second straight day of losses as the big 6 Canadian banks begin reporting their first quarter results. In trading, the biggest gains were in the Consumer Cyclicals and Consumer Staples sectors, while the Technology, Industrials and Financials were the only sectors to end lower.

In the US, the S&P and Nasdaq finished in the green, while the DJIA ended in the red. Last week’s rally seems to have lost momentum as investors await the latest inflation data. Two Fed officials said separately that they were in no rush to lower rates. In trading, Utilities and Telecommunications Services gained the most, while Energy was the only American sector to end lower.

Wednesday: All four indexes ended lower ahead of Thursday’s latest PCE data. The report is a pivotal point in determining when the US interest rate could start to fall. If the PCE data is similar to the recent Consumer Product Inflation readings on consumer and producer prices, it could cause the Fed to hold rates at current levels longer than the market is anticipating. Conversely, if the data is lower it could open the door to the Fed lowering the interest rate following the April/May meeting.

In Canada, the TSX recorded its third straight decline as investors prepare for tomorrow’s Canadian GDP report and the US PCE inflation report. In trading, Consumer Cyclicals was the only Canadian sector to advance, Healthcare and Telecommunications Services posted the largest drops.

In the US, investors were being cautious, taking some profits before the latest inflation report. In trading, Utilities and Industrials posted the biggest gains, while Healthcare and Energy fell the farthest.

Thursday: the US PCE showed the rate of inflation in the US continues to cool. The latest data matched analysts’ expectations and kept a June rate cut by the Fed on the table. The good news sent all four indexes higher for the day. Oil prices slipped on concerns the combination of lower demand and greater supply from OPEC nations could lead to lower oil prices.

In Canada, the TSX got back on track thanks to stronger than expected growth in the Canadian economy. In trading, the top performing sectors were Energy and Basic Materials (miners and fertilizer manufacturers), while the biggest declines were in the Consumer Staples and Consumer Cyclicals sectors.

In the US, the Nasdaq finally broke its all-time high and the S&P also closed at a new high, both indexes also had there best February since 2015. In trading, Basic Materials and Technology posted the largest gains, while Healthcare and Consumer Staples suffered the biggest losses.

Friday: March started on a high note with all four indexes ending the day higher as investors reacted to yesterday’s inflation report that left the door open for a June rate cut. Oil prices ended higher in anticipation of new supply agreements from OPEC+ nations.

In Canada, the TSX closed near a two year high as a result of higher commodity prices that boosted the share prices of resource companies. The TSX also benefitted from the technology rally in the US. In trading on Bay Street, Basic Materials and Energy spearheaded a broad advance that saw only the Consumer Cyclical sector end lower.

In the US, the S&P and Nasdaq both set new closing highs as the rally in technology companies continued. For the S&P it was its 15th record high of 2024. Nvidia closed the week with a market cap of over US$ 2 trillion, just over six months since it broke the US$ 1 trillion mark. In trading on Wall Street, today’s rally was led by the Technology and Energy sectors. Utilities and Consumer Staples were the only sectors to end lower.

Weekly Market and Portfolio Review

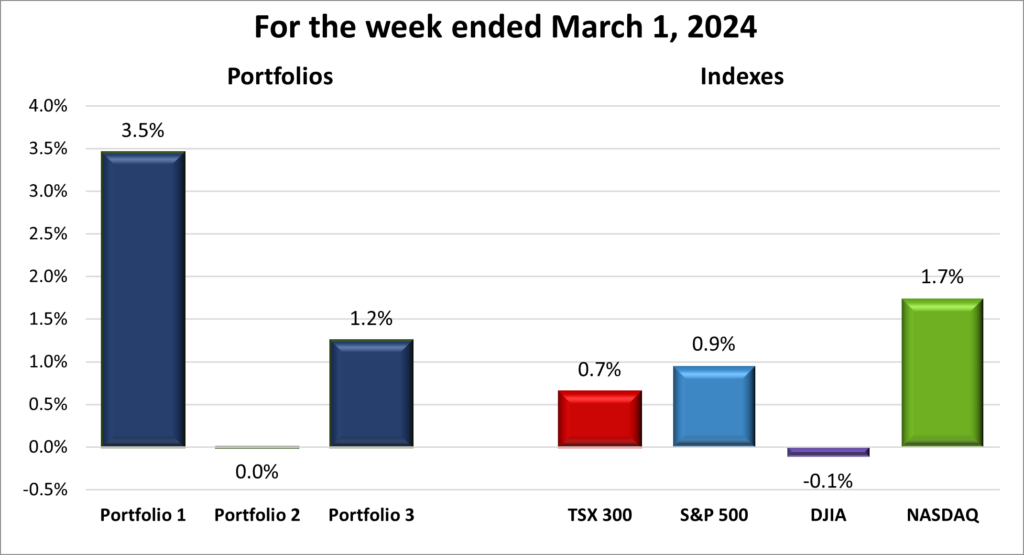

For the week, the TSX (SPTSX) rose 0.7%, the S&P 500 (SPX) added 0.9%, the DJIA (INDU) lost 0.1% and the Nasdaq (CCMP) gained 1.7%.

| Index | Weekly Streak |

| TSX: | 3-week winning streak |

| S&P: | 2-week winning streak |

| DJIA: | 1-week losing streak |

| Nasdaq: | 2-week winning streak |

![]() The stock market wrapped up the week with a positive rally, extending winning streaks for three major indexes. This upward momentum came despite a wait-and-see approach earlier in the week leading up to the PCE inflation report.

The stock market wrapped up the week with a positive rally, extending winning streaks for three major indexes. This upward momentum came despite a wait-and-see approach earlier in the week leading up to the PCE inflation report.

The PCE report, released on Thursday, provided some relief to investors. Inflation came in as expected, marking the lowest annual growth in three years. With the latest inflation numbers from both the US and Canada, investors seem to understand that central banks, despite analyst predictions of June rate cuts, are in no hurry to lower interest rates.

This week’s rally was spurred by the PCE report but was led by technology companies and investor enthusiasm for companies involved with AI. Comments from Fed officials hinting at a potential June rate cut, positive corporate earnings, and investor excitement surrounding AI fueled optimism.

Fourth quarter earnings season wound down this past week as more than 90% of S&P 500 index companies have already reported. Investors will now switch their focus from earnings back to interest rates and when the Fed might lower the benchmark rate.

March started with a bang. Hopefully, it does not go out with a whimper. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 9-week winning streak |

| Portfolio 2: | 3-week losing streak |

| Portfolio 3: | 1-week winning streak |

![]() Overall, the portfolios had another good week, as shown in the chart below. While I would have liked to have seen Portfolio 2 join the other two portfolios in positive territory, Portfolio 1 led the pack this week, even doubling the Nasdaq, the best performing index.

Overall, the portfolios had another good week, as shown in the chart below. While I would have liked to have seen Portfolio 2 join the other two portfolios in positive territory, Portfolio 1 led the pack this week, even doubling the Nasdaq, the best performing index.

Portfolio 1 was driven higher by significant (more than 10%) gains in a wide variety of companies, including Magnite (NASD: MGNI) up 31%, %, Nano-X Imaging (NASD: NNOX) up 24%, Celsius Holdings (NASD: CELH) up 23%, indie Semiconductor (NASD: INDI) up 15%, Sea Limited (NYSE: SE) up 13%, and Rivian Automotive (NASD: RIVN) was up 12%. Another positive was that Portfolio 1 did not experience any significant share price drops this past week.

Portfolio 2 essentially broke even this past week. However, upon closer inspection the portfolio was down 0.004% this past week, stretching its weekly losing streak to 3 weeks. Although Canadian Natural Resources (TSE: CNQ) posted an 11% increase, it wasn’t enough to offset small losses elsewhere.

Portfolio 3 also had a good week, though not as impressive as Portfolio 1. The portfolio was lifted by notable gains in Lithium Americas (Argentina) (TSE: LAAC) up 26% and Lithium Americas (TSE: LAC) up 32%. It is encouraging to see that both lithium producers finally reversed the downward trend they had experienced in recent weeks.

Looking ahead to next week, I hope to see the markets maintain their upward trajectory, with all three portfolios ending on a high note. Onward and upward! 😊

Monthly Market and Portfolio Review

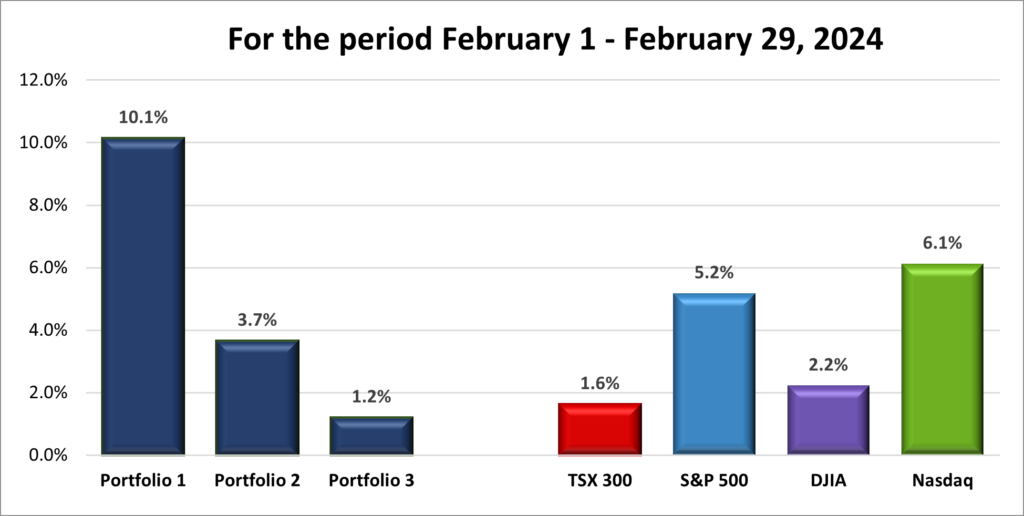

For February, the TSX (SPTSX) rose 1.6%, the S&P 500 (SPX) advanced 5.2%, the DJIA (INDU) gained 2.2% and the Nasdaq (CCMP) surged 6.1%.

![]() February marked another strong month for the four major indexes, underscoring the market’s continued upward momentum, as you can see in the chart above. The standout performance of Nvidia’s fourth quarter earnings report and the broader excitement around AI technologies have been pivotal, driving not just sector-specific gains but also influencing the broader market. This AI-led rally has notably benefited semiconductor companies and has been a key factor in the sustained growth of the indexes.

February marked another strong month for the four major indexes, underscoring the market’s continued upward momentum, as you can see in the chart above. The standout performance of Nvidia’s fourth quarter earnings report and the broader excitement around AI technologies have been pivotal, driving not just sector-specific gains but also influencing the broader market. This AI-led rally has notably benefited semiconductor companies and has been a key factor in the sustained growth of the indexes.

In addition to technological advancements, the corporate sector in both Canada and the US has shown resilience, with many companies beating fourth-quarter 2023 earnings expectations and providing cautiously optimistic future earnings forecasts. This has further buoyed investor confidence.

While initial hopes for a March interest rate cut in the US were tempered by unexpected inflation figures, Fed officials remain optimistic they will be able to start reducing rates within the year, potentially by June. Such adjustments would be beneficial for both consumers and investors, signaling a responsive approach to evolving economic conditions.

The positive earnings season, combined with strong investor interest in AI, has contributed to the fourth consecutive month of gains for the three American indexes (Nasdaq up 6.1%, S&P up 5.2%, the DJIA up 2.2%). Similarly, the TSX experienced fluctuations in commodity and energy prices but ultimately posted a monthly gain of 1.6%, extending its winning streak to its longest since 2021, fueled by the positive sentiment and performance of the US markets.

The alignment of technological advancements and strong corporate performance provides an encouraging start to the year, pointing towards a sustained upward trend in the markets. Hopefully, the markets can keep the monthly winning streaks going.

![]() February was not only a favourable month for the broader markets but also for my three portfolios, as illustrated in the chart below. Portfolio 1, riding a nine-week winning streak, had an exceptional month. This stellar performance was fueled by the significant appreciation of Nvidia’s share price and the growth of other tech companies, especially those in the AI sector.

February was not only a favourable month for the broader markets but also for my three portfolios, as illustrated in the chart below. Portfolio 1, riding a nine-week winning streak, had an exceptional month. This stellar performance was fueled by the significant appreciation of Nvidia’s share price and the growth of other tech companies, especially those in the AI sector.

Portfolio 2 also saw a strong performance, buoyed by a 15% increase in Disney shares. The cumulative gains from other holdings in the portfolio more than offset any losses, contributing to its overall success.

However, Portfolio 3’s performance was unexpectedly modest. Given its tech-heavy composition, I anticipated a performance similar to the Nasdaq’s surge. A closer examination pinpointed the main culprit: Shopify (TSE: SHOP), the portfolio’s largest holding, which underperformed in February, dampening the portfolio’s overall gains.

In February, the buoyant market mood lifted all my portfolios, albeit to varying degrees. Some experienced significantly more substantial gains, much to my delight. Hopefully, I will see more months of 10% gains for all three portfolios. 😊

Companies on the Radar

No new companies came across my radar this past week, but I was able to trim the number of companies on my radar list. After adding Walmart (NYSE: WMT) to the radar list last week I decided I didn’t need two of what I consider defensive stocks. I feel Walmart has more upside than Macdonald’s (NYSE: MCD), so I’ve dropped the golden arches from my radar list. I also dropped Brown & Brown (NYSE: BRO) from the list. It appears to be a fine company, but I like the five remaining on the list better.

No new companies came across my radar this past week, but I was able to trim the number of companies on my radar list. After adding Walmart (NYSE: WMT) to the radar list last week I decided I didn’t need two of what I consider defensive stocks. I feel Walmart has more upside than Macdonald’s (NYSE: MCD), so I’ve dropped the golden arches from my radar list. I also dropped Brown & Brown (NYSE: BRO) from the list. It appears to be a fine company, but I like the five remaining on the list better.

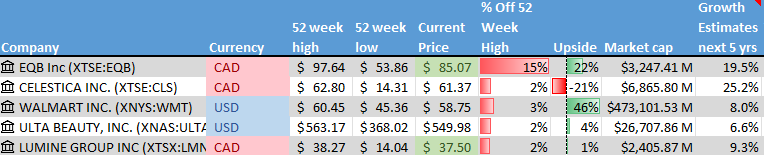

The five holdovers from last week are:

- Equitable Bank (TSE: EQB), a mid sized Canadian bank that provides financial services to consumers and businesses.

- Celestica Inc. (TSE: CLS), a medium sized Canadian company that manufactures electronic products and provides supply chain services to companies around the world.

- Walmart: the large American global retail chain.

- Ulta Beauty (NASD: ULTA), a major American beauty product retailer, with over 25,000 products from 600 brands.

- Lumine Group (TSE: LMN), a young Canadian mid sized company that acquires communications and media software companies and then strengthens and grows those companies.

Please keep in mind that these are only companies that have piqued my interest. This is not a recommendation or financial advice. You should do your own research or contact a professional before making any investment decisions.

The Radar Check was last updated March 1, 2024.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended March 1, 2024: UP ![]()

- Berkshire Hathaway’s (NYSE: BRK.B) power company PacifCorp (OTCM: PPWLO) faces the risk of a significant lawsuit over its alleged failure to cover the costs associated with a wildfire in northern California in 2020.

- Amazon’s (NASD: AMZN) cloud computing unit Amazon Web Services plans to invest US$ 5 billion in Mexico over the next 15 years. The company plans to build data centres to enhance their cloud computing capabilities in the region.

- A jury has recommended a US$ 12 million fine against Google for infringing on five internet voice calling patents belonging to Flyp, an app maker.

In separate Google news, the company was slapped with a US$ 2.3 billion lawsuit by 32 media groups. The lawsuit claims the groups suffered financial losses because of Google’s digital advertising practices. It was not a good week on the legal front for Google. - Apple (NASD: AAPL) made a surprise announcement when they said they were cancelling their efforts to build an autonomous electric car. The company had been working on the project for almost a decade with almost 2,000 employees working on the project.

In other Apple news, a touch of irony that European regulators forced Apple to open its in-app payment system to third parties. Now European government agencies have voiced concerns about the security risks associated with allowing third party payment systems onto Apple devices. Government regulators were not happy with Apple’s closed system, now federal agencies are not happy with the open systems.

Activity

Received interest on TD 1-year cashable GIC.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

No C$ dividends this past week.

US $

Visa Inc (NYSE: V)

Quarterly Reports

Cargojet Inc.

Fourth quarter 2023 financial results on February 26, 2024

Innovative Industrial Properties, Inc.

Fourth quarter 2023 financial results on February 26, 2024

Unity Software Inc.

Fourth quarter 2023 financial results on February 26, 2024

The Bank of Nova Scotia

First quarter 2024 financial results on February 27, 2024

Progeny, Inc.

Fourth quarter 2023 financial results on February 27, 2024

GDI Integrated Facility Services Inc.

Fourth quarter 2023 financial results on February 28, 2024

Magnite, Inc.

Fouth quarter 2023 financial results on February 28, 2024

TD Bank Group

First quarter 2024 financial results on February 29, 2024

Navitas Semiconductor Corporation

Fourth quarter 2023 financial results on February 29, 2024

Celsius Holdings, Inc.

Fourth quarter 2023 financial results on February 29, 2024

Portfolio 2

Portfolio 2 for the week ended March 1, 2024: ![]()

- Disney (NYSE: DIS) announced the merger of Disney’s streaming assets with Indian conglomerate Reliance Industries’ India TV to create a media juggernaut in India. Reliance will put in an additional US$ 1.4 billion into the merged entity, bringing its share of the company to 63%. Disney will own the remaining 37%. The Reliance/Disney unit will have 120 TV channels, two streaming channels, and the streaming rights to key cricket tournaments.

In other Disney news, the grandchildren of founder Roy and Walt Disney have come out in support of Chief Executive Officer Bob Iger and the current Board of Directors in their battle with activist shareholders. - MongoDB (NASD: MDB) announced their Atlas cloud data platform was now available in six more cloud regions, including Canada, Germany, Israel, Italy, and Poland. This brings the availability of the company’s data platform to 117 cloud regions across the three most popular cloud services – Amazon Web Services (AWS), Google Cloud, and Microsoft Azure.

- A survey done by Guardant Health (NASD: GH) showed doctors and patients strongly agreed that blood-based testing could help narrow the colorectal cancer screening gap between those who regularly take colorectal cancer screening tests and those who don’t by offering a “more pleasant and convenient option.”

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Fortis Inc (TSE: FTS)

US $

No US$ dividends this past week.

Quarterly Reports

BNS

See report under Portfolio 1.

Canadian Natural Resources Limited

Fourth quarter 2023 financial results on February 29, 2024

Portfolio 3

Portfolio 3 for the week ended March 1, 2024: UP ![]()

- Microsoft (NASD: MSFT), along with Amazon, is facing scrutiny in the European Union (EU) over their supposed domination of the European cloud computing market. Cloud computing rival Alphabet’s Google claims Microsoft is attempting to create a cloud computing monopoly, similar to what they had in desktop computing for a few years.

In other Microsoft news, the company signed a deal with France’s Mistral AI to provide an alternate AI model to their existing OpenAI model that runs on the Microsoft Azure cloud platform. In exchange for the use of Mistral AI’s AI models, Microsoft made a US$ 16 million-dollar investment in the company. The deal with Mistral AI should provide some protection if European regulators go looking at Microsoft’s relationship with OpenAI. - Lithium Americas (Argentina) Corp. (TSE: LAAC) announced Sam Pigott as their next President and Chief Executive Officer (CEO), effective on March 18, 2024. John Kanellitsas, the current President and Interim CEO, as well as the Executive Chair of the Board of Directors, will continue in his role as Chair of the Board.

- Alvopetro Energy (TSX: ALV) announced its proven reserves fell by 30% in 2023 due to technical difficulties at two if its wells.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Enghouse Systems Ltd (TSE: ENGH)

Royal Bank of Canada (TSE: RY)

US $

No US$ dividends this past week.

Quarterly Reports

Unity Software Inc.

See report under Portfolio 1.

Royal Bank of Canada

First quarter 2024 financial results on February 28, 2024

Magnite, Inc.

See report under Portfolio 1.

GDI Integrated Facility Services Inc.

See report under Portfolio 1.

TD Bank Group

See report under Portfolio 1.