Items that may only interest or educate me ….

Canadian budget, Canadian GDP, US Economic data, latest Silicon Bank chapter, …

Prior to releasing the latest budget, the current Canadian government said they would be “fiscally responsible” while at the same time spending a whole lot of your taxpayer dollars on the new green economy (OK, that last part are my words). I did not think those two were compatible and it turns out I was right. The government increased this year’s deficit to C$40 billion and plans to run larger deficits every year until 2028 as the current government went all-in on spending and borrowing. Turns out “fiscally responsible” means something different to the government.

Statistics Canada reported Canada’s Gross Domestic Product (GDP), the sum of all the goods and services produced in Canada, for January grew 0.5% on a monthly basis, a significant reversal after shrinking 0.1% in December. Analysts were expecting an increase of 0.4%. Preliminary data indicated the Canadian economy grew 0.3% in February.

Analysts suggest the numbers indicate Canada’s GDP grew at an annual rate of 2.5% for the first quarter, well above the Bank of Canada’s (BoC) 0.5% estimate. The data implies the Canadian economy is performing better than expected. While this is good news on one level, the strong economic growth could stop the downward trend of Canadian inflation. The BoC will be paying close attention to upcoming economic data to see if any action on their part is required at their next meeting April 12.

The US Commerce Department reported the fourth-quarter GDP was 2.6%, down slightly from the previous estimate of 2.7%. With 3.2% growth in the third quarter, the data suggests the US economy is slowing down. As well, more than 50% of the fourth quarter’s growth came from companies restocking their inventories rather than meeting consumer demand. Based on the data, it would appear the underlying economic growth is slowing because of the higher interest rates.

The US Federal Reserve’s (Fed) preferred measure of inflation, the Personal Consumption Expenditures (PCE) for February, gained 0.3%, down from January’s 0.6% increase. On an annual basis, the PCE rose 5.0%, down from January’s 5.3% increase. Core PCE rose 0.3% down from January’s 0.5%, and 4.6% on a yearly basis, basically inline with analysts’ expectations of 0.4% and 4.7%, respectively.

Taken together, both of these bits of information suggest the higher interest rates are slowing both consumer spending and the US economy, which should to a drop in inflation. Hopefully, the Fed is satisfied with the latest economic data to pause interest rates to let the previous rate hikes continue to work their way through the economy before taking any action.

First Citizens BancShares (NASD: FCNCA), a North Carolina regional bank, bought Silicon Valley Investment Bank’s (SIVB) deposits, loans, and 17 branches that reopened under the First Citizens Bancshares banner. The CEO of First Citizens said the purchase was designed to “instill confidence in the banking system.” The acquisition will nearly double the assets of First Citizens. Based on the huge jump in the share price, it also seemed to benefit First Citizens’ shareholders quite nicely.

To get the deal done, the Federal Deposit Insurance Corporation (FDIC) sold US$72 billion worth of SIVB loans to First Citizens at a discount of US$16.5 billion and agreed to share with First Citizens any losses or gains on those loans in the future. FDIC also provided a US$70 billion line of credit in the event of liquidity issues in exchange for up to US$500 million in First Citizens shares.

To backstop the purchase, rather than a government bailout, the FDIC took a hit of US$20 billion to its deposit insurance fund. The remaining US$90 billion of SIVB’s assets, mainly low yielding assets, remain with the FDIC until they can find a buyer.

Now, let’s see what happened this past week….

Weekly Market Review

Monday: The last week of the first quarter got off to a mixed start with three of the four major North American indexes advancing. Shares of banks in Canada and the US rose on the news that First Citizens Bank bought the loans and assets of SIVB, calming investors concerns about the banking crisis. Easing concerns about the financial crisis, in combination with news Iraq halted oil exports, pushed the price of oil up 5%.

In Canada, the Toronto Stock Exchange Composite Index (TSX) was buoyed by the higher oil prices and bank stocks. On Bay Street, the home of the TSX, Consumer Staples and Energy sectors gained the most. Telecommunications Services was the only Canadian sector to end the day lower.

In the US, the S&P 500 Index (S&P) and the Dow Jones Industrial Average (DJIA) both ended the day higher, while the Nasdaq Composite Index (Nasdaq) fell on weakness in the Technology sector. On Wall Street, home of the American financial markets, the Energy and Financials sectors advanced the most while the Technology sector was the only American sector to end lower.

Tuesday: Another mixed day for the four indexes, this time the TSX advanced and the American indexes stumbled. After a surge in bank stocks yesterday, especially American banks, the banking sector gave back some of those gains.

In Canada, money was moving back into Mining companies as the Basic Materials (miners and fertilizer manufacturers) was the biggest gainer of the Canadian sectors, followed by the Consumer Staples and Energy sectors. Meanwhile, the Technology and Healthcare sectors dropped the most.

In the US, profit taking in the technology sector and concerns about risk management by bank executives caused all three indexes to sink. On a positive note, despite the ongoing banking crisis, American consumer confidence rebounded after dropping in February. In trading in the American sectors, Energy and Basic Materials advanced the most, while the Healthcare and Technology sectors dropped the most.

Wednesday: The day started sharply higher for all four indexes, and they remained high for the rest of the day. In a case of no news is good news, there was no banking news to rattle the market today. It seems banking sector fears are fading. With one eye on the Fed for signs what they will do at their next meeting in May, investors cautiously moved back into growth-oriented sectors in both countries.

In Canada, the TSX stretched its winning streak to four days as all the Canadian sectors finished higher. Leading the way were the growth-oriented Technology and Consumer Cyclicals sectors, while Telecommunications Services and Basic Materials trailed the pack.

In America, the Nasdaq ended the day on a promising note, up 20% since December. A gain of 20% or more means the Nasdaq is in a bull market. Let us hope this young bull is long lived. 😊 In trading, all the American S&P sectors finished in the green today, led by Technology and Consumer Cyclicals sectors. Healthcare and Consumer Staples brought up the rear.

Thursday: It appears investors want to end the first quarter on an uptrend as all four indexes once again ended the day higher. Professional money managers want their portfolios to look good for the quarterly reviews with their clients, so they unload losers and add to their winners. With no banking problems this week, investors are starting to feel the banking crisis is largely behind us.

In Canada, the beat goes on for the TSX as it runs its winning streak to five days. In the Canadian sectors it was a day of broad based gains as all sectors ended higher. The defensive sectors Utilities and Consumer Staples led the way, with Healthcare and Energy bringing up the rear.

In the US, the bull run in the Nasdaq continued as investors continue to move into technology companies. On a sobering note, the Fed said it was open to another interest rate hike if inflation doesn’t continue to fall. In trading, all American sectors ended in the green, led by the Basic Materials and Technology sectors. The Financials and Healthcare sectors rounded out a positive day in the American markets.

Friday: All four indexes ended higher on the last day of the week, month, and quarter. The US Personal Consumption Expenditures (PCE) data indicated US inflation continues to cool, leading investors to believe the Fed will be able to pause its interest rate hikes.

In Canada, the TSX stretched its winning streak to six. Statistics Canada data showed Canada’s economy did better than expected in January with signs of further growth in February. In trading, the Technology and the Consumer Cyclicals led the Canadian sectors higher, while Telecommunications Services and Utilities were the only sectors to end lower.

In the US, all three indexes ended the day in the green as data showed US inflation was falling. The positive news was music to investors ears as it was a day of across the board gains for the American indexes. The rally was led by the growth-oriented Consumer Cyclicals and Technology sectors while the Telecommunications Services and Energy stocks brought up the rear.

Weekly Portfolio Review

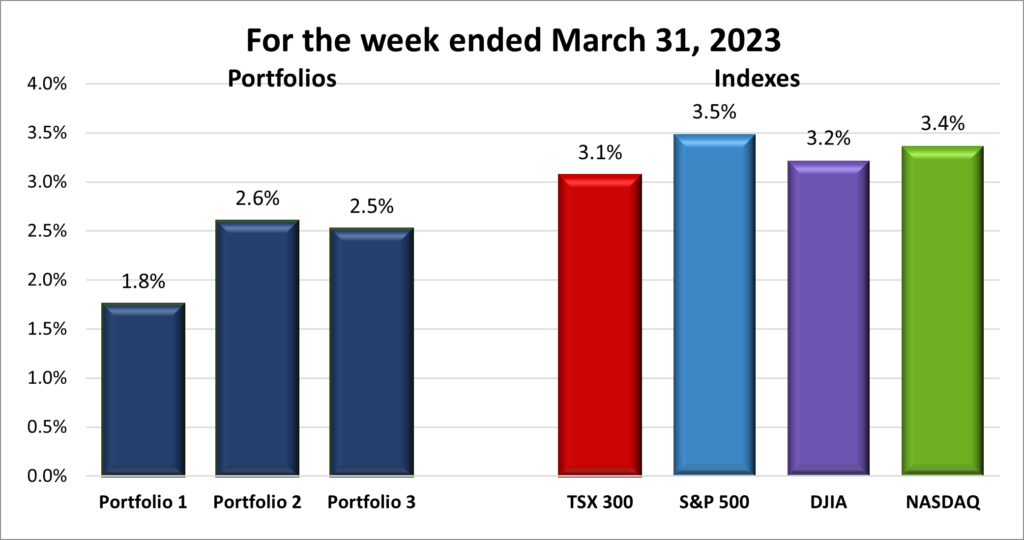

For the week, the TSX (SPTSX) added 3.1%, the S&P 500 (SPX) gained 3.5%, the DJIA (INDU) grew 3.2% and the Nasdaq (CCMP) rose 3.4%.

![]() After the previous two weeks, this past week was relatively calm. No banks collapsed, the financial stocks rebounded, oil prices climbed for the second week in a row and investor optimism returned. There wasn’t any significant bad news to upset investors. Overall, a fairly good week to end the month on an upbeat note, as shown in the chart above.

After the previous two weeks, this past week was relatively calm. No banks collapsed, the financial stocks rebounded, oil prices climbed for the second week in a row and investor optimism returned. There wasn’t any significant bad news to upset investors. Overall, a fairly good week to end the month on an upbeat note, as shown in the chart above.

Another good week for the indexes usually means another good week for the Portfolios. And it was as they each benefited from the rise in technology companies primarily found on the Nasdaq. Unfortunately, none of the portfolios gained as much as the lowest index, as shown below. After 2022, any time all three portfolios advance, is a good week. 😊

Monthly Portfolio Review

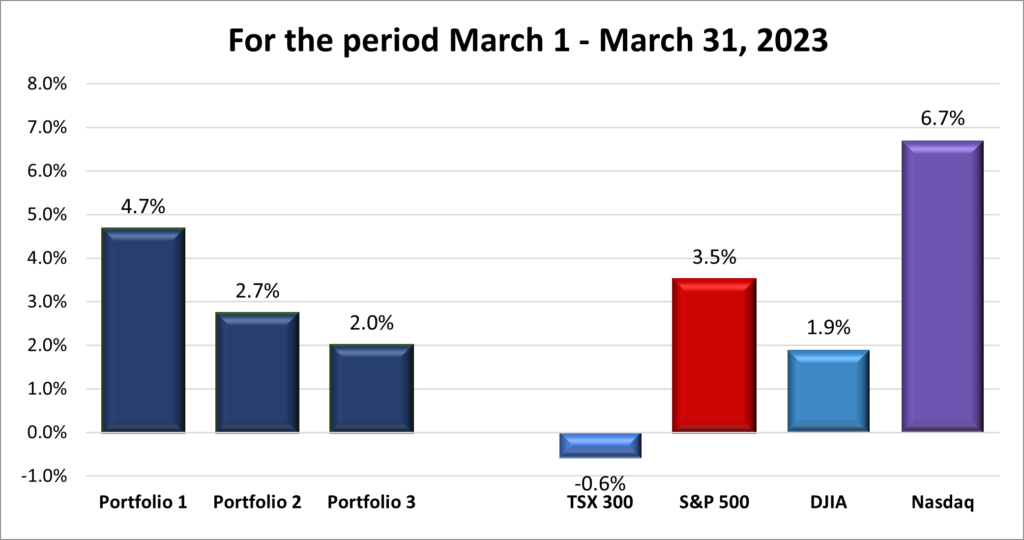

For March, the TSX (SPTSX) dropped 0.6%, the S&P 500 (SPX) advanced 3.5%, the DJIA (INDU) added 1.9% and the Nasdaq (CCMP) gained 6.7%.

![]()

As shown in the chart above, March got off to a rough start due to a selloff in bank stocks caused by the unfolding global banking crisis, and oil price volatility. As the month wound down, with the bank crisis fading, inflation down slightly and investors believing the Fed may pause their interest rate hikes, investors responded by sending all four indexes higher. The three American indexes benefitted from the rotation of money from bank stocks into the big technology companies, especially the Nasdaq, and were able to post solid gains for March.

Canada’s TSX did not benefit from the rotation to big technology companies as much as the American indexes because it is heavily weighted with bank and energy companies (47%), two of the sectors most impacted by the bank crisis. As a result, the TSX took longer to reverse its downward trend and was unable to climb get back into positive territory like the American indexes.

The portfolios rebounded nicely after stumbling in February. The rise of the big tech companies was the big driver for all three portfolios, especially Portfolio 1 which contains Alphabet (NASD: GOOGL), Amazon (NASD: AMZN), Apple (NASD: AAPL) and Nvidia (NASD: NVDA). Portfolio 1 has now advanced every month in 2023. After stumbling in February, it was good to see Portfolios 2 and 3 back in the win column. Both benefitted from owning shares in Microsoft (NASD: MSFT), as well as other technology companies.

Companies on the Radar

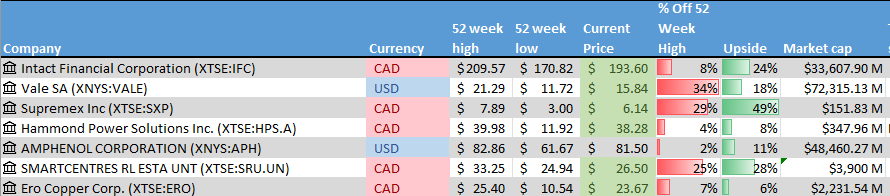

This past week one new company popped up on my radar: Amphenol (NYSE: APH). This company produces a wide variety of high-technology interconnect, sensor, and antenna solutions for the automotive, aerospace, industrial and various technology industries. The company is in several industries, providing great optionality, and should be able to ride the tailwinds of EV and digital revolution.

This past week one new company popped up on my radar: Amphenol (NYSE: APH). This company produces a wide variety of high-technology interconnect, sensor, and antenna solutions for the automotive, aerospace, industrial and various technology industries. The company is in several industries, providing great optionality, and should be able to ride the tailwinds of EV and digital revolution.

- Intact Financial (TSX: IFC): A Canadian mid size insurance company supplying home, car and business insurance in Canada, the US, and the UK.

- Vale (NYSE: VALE): A global mining company that extracts various metals and rare earth elements such as nickel, cobalt, gold, copper, that are used in electric vehicles.

- Supremex (TSX: SXP): A small cap company selling packing solutions throughout Canada and the USA.

- Hammond Power Solutions (TSX: HPS.A): A small cap Canadian company manufacturing transformers used throughout the world in a wide variety of industries.

- Smartcentres Real Estate Investment Trust (TSX: SRU.UN): Owns and manages a number of income producing malls and retails spaces throughout Canada.

- Ero Copper Corp. (TSX: ERO): A small cap Canadian copper mining company with mines in Brazil.

The Radar Check was last updated March 31, 2022.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended March 31, 2023: UP ![]()

- Tesla (NASD: TSLA) is back in court. This time to determine the size of the payment Tesla must pay in a workplace discrimination case. Tesla lost the case and was ordered to pay the plaintiff US$137 million but the amount was cut to US$15 million by the judge.

- Apple released it’s Apple Pay Later service to compete in the lucrative ‘Buy Now Pay Later’ (BNPL) financial technology arena. Using the service, users can divide payments into four payments over six weeks, with no interest or fees; users can apply for loans of $50 to $,1000 for online and in app purchases from within their iPhone or iPad (merchants must accept Apple Pay). Because of Apple’s size, reputation and ease of use, look for them to take market share from many of the smaller companies in the financial technology industry.

Apple won a 13-year battle with VirnetX Holding Corp (NYSE: VHC), a patent licensing company. The two companies were battling over two virtual private network patents that VirnetX accused Apple of infringing upon. This past week the US Court of Appeals for the Federal Circuit affirmed a decision from the US Patent and Trademark Office that VirnetX’s two patents were invalid because earlier publications described the inventions VirnetX claimed were theirs. - The merger of Rogers Communications (TSX: RCI.B) and Shaw Communications (TSX: SJR.B) has finally been approved. The deal will see Rogers receive the bulk of Shaw’s assets for C$26 billion. Part of the deal is the sale of Shaw’s Freedom Mobile licences to Quebecor’s (TSX: QBR.B) Videotron unit for C$2.85 billion. At the end of the day, there will be no more Shaw, and Videotron will become a national wireless provider. It is expected that Freedom Mobile customers will see a 20% reduction in their wireless bills. It does not say what will happen to Shaw Mobile customers (of which I am one) or their monthly bills.

- Telus (TSX: T) was named best Canadian major mobile carrier in PC Magazines’ first ever Canadian Readers’ Choice Awards 2023 and Business Choice Awards 2023. Telus won the Top Major Carrier in Canada award in both the Readers’ Choice and Business Choice categories, as well as Top Digital Carrier in Canada for its Public Mobile brand.

- Docebo (TSX: DCBO) was named one of The Americas’ Fastest Growing Companies 2023 by The Financial Times. Docebo ranked 201 out of 500 companies for the highest compound annual growth rate (CAGR) in revenues between 2018 and 2021. Docebo was among the top five IT companies based in Canada, and sixth best for publicly traded companies in Canada.

Activity

Sold Viemed Healthcare (TSX: VMD). With the pandemic behind us, demand for respirators is slowing and the company is back to its pre-pandemic growth rate. The share price had recently risen considerably for no obvious reason, and I did not want to see it fall farther like has happened with a few other small cap companies I’ve owned.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Canadian National Railway Co (TSX: CNR)

Shaw Communications Inc (TSX: SJR.B)

US $

NVIDIA Corp (NASD: NVDA)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended March 31, 2023: UP ![]()

- Walt Disney (NYSE: DIS) started letting go over 7,000 employees as the company seeks to lower costs by US$5.5 billion and streamline its operations in order to make its streaming business profitable.

Some of those employees let go was the Marvel Entertainment unit, including the head of the unit. The head of the unit recently backed an activist shareholder who was seeking a seat on Disney’s Board of Directors. Reminds me of the saying, “when you go for the king, you best not miss.” The Marvel Entertainment unit is separate from the movie making Marvel Studios, which was unaffected by the dismissal of the Entertainment unit. Other layoffs include several senior executives at Disney’s ABC News unit.

In a bit of Disney magic, Disney effectively neutered the new special tax district board that oversees the Disney World area setup by the state of Florida. Before the new board took over from the ‘old’ board, the old board installed new covenants that prevented the ‘new’ board from using the Disney name and intellectual property and gave the company the right to review any proposed changes to properties in the special tax district. Well played, Mickey. Well played.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Brookfield Infrastructure Partners LP (TSX: BIP.UN)

Brookfield Infrastructure Corp (TSX: BIPC)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended March 31, 2023: UP ![]()

- In a case of the kettle calling out the pot, Alphabet has asked the European Union antitrust regulators to take a closer look at the deals Microsoft has recently struck with European cloud vendors. Alphabet claims Microsoft is too dominant in the cloud services market. Alphabet seems to have forgotten it owns 94% of the search market, 80% of the online maps market, and nearly 25% of the global email provider market. Meanwhile, Microsoft owns 20% of the cloud services market. Hmmm.

Activity

Sold Viemed Healthcare. With the pandemic behind us, demand for respirators is slowing and the company is back to its pre-pandemic growth rate. The share price had recently risen considerably for no obvious reason, and I did not want to lock in the gains.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Brookfield Asset Management (TSX: BAM)

Brookfield Reinsurance Ltd (TSX: BNRE)

Brookfield Renewable Corp (TSX: BEPC)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.