After a dismal 2022 for the four major North American indexes, it was great to see they closed out 2023 with big gains in the fourth quarter, leading to record highs. The three American indexes – the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – all ended the year riding a 9-week weekly winning streak. The Toronto Stock Exchange Composite Index (TSX) was not as hot but still concluded the year with three straight weeks of gains.

Despite initial concerns about inflation and recession, 2023 turned out to be a remarkable year for stock market performance. This unexpected rally was led by mega-cap technology stocks and other growth companies that had faced significant losses during the bear market in 2022.

In Canada, the economy slowed before becoming stagnant towards the end of the year and the Bank of Canada (BoC) raised the Canadian interest rate four times in the first half of the year to 5.0% before pausing additional increases. The American economy remained solid throughout the year despite the regional banking crises in the first quarter. The Federal Reserve (Fed) raised interest rates four times during the year to 5.5% but signaled no further increases and potential rate cuts in the coming year.

The year ended on a high note with a rally that started in early November before turning into a Santa Claus rally to end the year on a high note. After the bear market of 2022 that took a big bite out of all three portfolios, you will hear no complaints from me about the gift Santa left in the form of a fourth quarter rally. 😊

Let’s take a look at what transpired over the last three months as well as a quick review of the entire year ….

Fourth Quarter Portfolio Update

Portfolio 1 for the fourth quarter

Portfolio 2 for the fourth quarter

Portfolio 3 for the fourth quarter

Going Forward: The First Quarter 2024 and beyond

Fourth Quarter Review

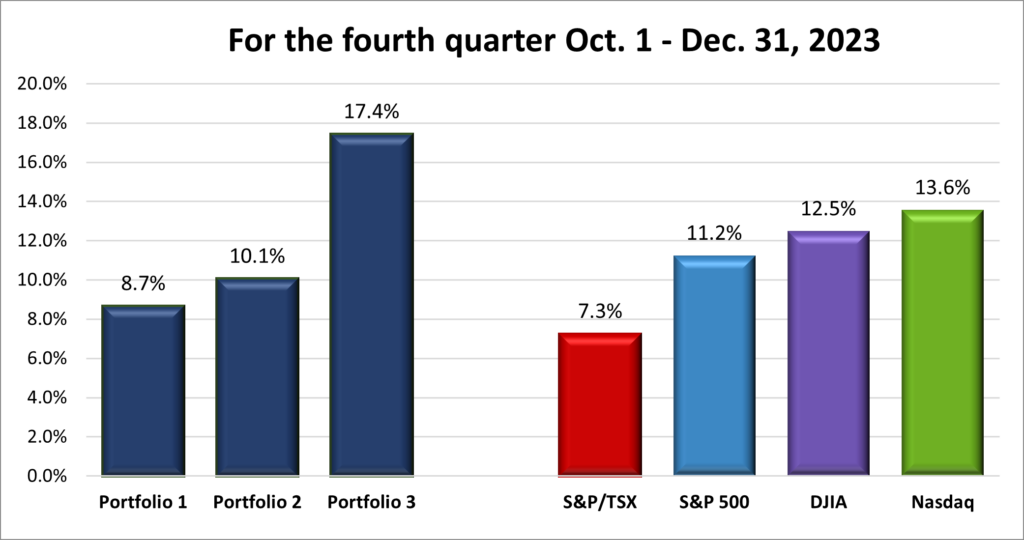

For the fourth quarter, the TSX, gained 7.3%, the S&P surged 11.2%, the DJIA rose 12.5% while the Nasdaq advanced 13.6%.

![]() The North American stock markets experienced quite the upward ride during the fourth quarter of 2023, fueled by investor optimism surrounding the prospect of falling interest rates. This enthusiasm, rooted in falling inflation and the anticipation of rate cuts in the approaching year, propelled the markets to new heights, buoyed further by the year-end “Santa Claus rally.” Despite a brief dip in October, the quarter concluded with all four major North American indexes notching positive returns, propelled by a robust rally in November and December.

The North American stock markets experienced quite the upward ride during the fourth quarter of 2023, fueled by investor optimism surrounding the prospect of falling interest rates. This enthusiasm, rooted in falling inflation and the anticipation of rate cuts in the approaching year, propelled the markets to new heights, buoyed further by the year-end “Santa Claus rally.” Despite a brief dip in October, the quarter concluded with all four major North American indexes notching positive returns, propelled by a robust rally in November and December.

Several factors contributed to the markets’ movements, including the ongoing conflict in Ukraine and conflict in the Middle East. However, the overarching drivers were the cooling inflation and the growing belief that the Fed would begin lowering the benchmark interest rate in the first quarter of 2024. Following inflation’s decline from multi-decade highs, thanks in part to the BoC and the Fed’s interest rate hikes, the pause in rate hikes and hints at potential cuts fueled investor optimism for future economic growth, mitigating fears of a looming recession and adding momentum to the rally.

Unlike at the start of 2023 when the indexes were lifted by the Magnificent 7 technology companies – Apple Inc. (NASD: AAPL), Alphabet Inc. (NASD: GOOGL), Amazon.com Inc. (NASD: AMZN), Meta Platforms Inc. (NASD: META), Microsoft Corp. (NASD: MSFT), Nvidia Corp. (NASD: NVDA), and Tesla Inc. (NASD: TSLA) – the rally saw gains across a wider range of sectors, including energy, healthcare, and consumer staples. This diversification contributed to its stability and resilience. Technology companies continue to drive the Nasdaq, but the increased breadth of the rally pushed the S&P and DJIA higher, with the DJIA setting an all time high.

In Canada, the BoC did not signal an end to rate hikes like the Fed did at their last meeting in December. However, the TSX also benefited from falling inflation throughout the final quarter of 2023. This lowered concerns about rising interest rates. Unlike 2022, which saw strong performances in the energy and basic materials sectors, the fourth quarter saw a shift towards value (underpriced) stocks on the TSX. This included sectors like financials, consumer staples, and utilities, which are typically seen as less volatile and offer relatively higher dividend yields. This rotation towards value was likely driven by a combination of factors, including the easing inflation concerns and the pursuit of income in a potentially slowing economic environment.

Overall, after a stumbling start, the fourth quarter had a remarkable turnaround. Following a downturn in the third quarter, the markets surged in November and continued into December, steering all three American indexes to double-digit growth for the quarter, with the TSX trailing at a commendable 7.3%. Not a bad recovery for a quarter that initially stumbled out of the gate. 😊

Fourth Quarter Portfolio Update

The portfolios rode the tailwind of the November rally that became a Santa Claus rally in December to end the fourth quarter. All three portfolios had a strong fourth quarter, with Portfolio 3 having a great quarter, easily outperforming the indexes, as shown in the chart below.

Portfolio 1 for the fourth quarter:

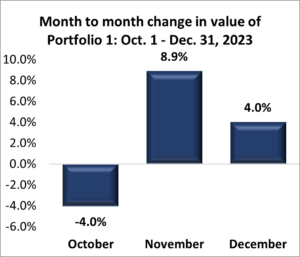

Portfolio 1 got off to a disappointing start, weighed down by the overall market’s decline that was caused by fears of an economic slowdown and stubborn inflation. However, the portfolio reversed course and rode the tailwinds of the two-month rally to end the quarter in positive territory. Strong performances from the mega cap technology companies helped the portfolio reach double digit gains for the quarter.

Activity: Second investment in Rivian Automotive Inc. An initial Investment in Decisive Dividends Corporation. Sold Marqeta Inc., Copperleaf Technologies Inc., WELL Health Technologies Corp., and Voyager Digital Ltd.

Portfolio 2 for the fourth quarter

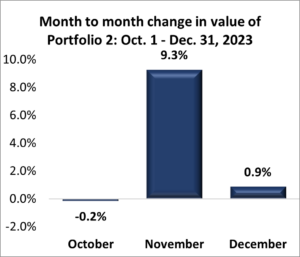

Despite a significant drop in the markets at the start of the fourth quarter, Portfolio 2 managed to achieve double-digit gains for the quarter. Riding the coattails of the overall market surge during the year-end rally, the portfolio was propelled higher, notably by the stellar performance of Microsoft. The more balanced composition of the portfolio, which helped it avoid a substantial decline in October, also contributed to limiting its gains in December. ☹

Activity: Bought Dollarama Inc.

Portfolio 3 for the fourth quarter

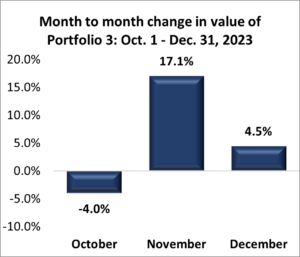

When the markets dropped in October, Portfolio 3 fell farther than the four indexes, weighed down by its overwight in Shopify. However, when the markets reversed course, it was Shopify that propelled the portfolio to a huge monthly gain in November, as shown in the chart below. Portfolio 3 posted a more modest gain in December, inline with the monthly gains of the indexes, to end a great fourth quarter that saw it out perform the four indexes. Here is to more quarters with double-digit gains! 😊

Activity: Lithium Americas Corp. split into Lithium Americas Corp (North America operations) and Lithium Americas (Argentina) Corp. (South America operations). Sold Fortuna Silver Mines Inc.

Twelve Month Review

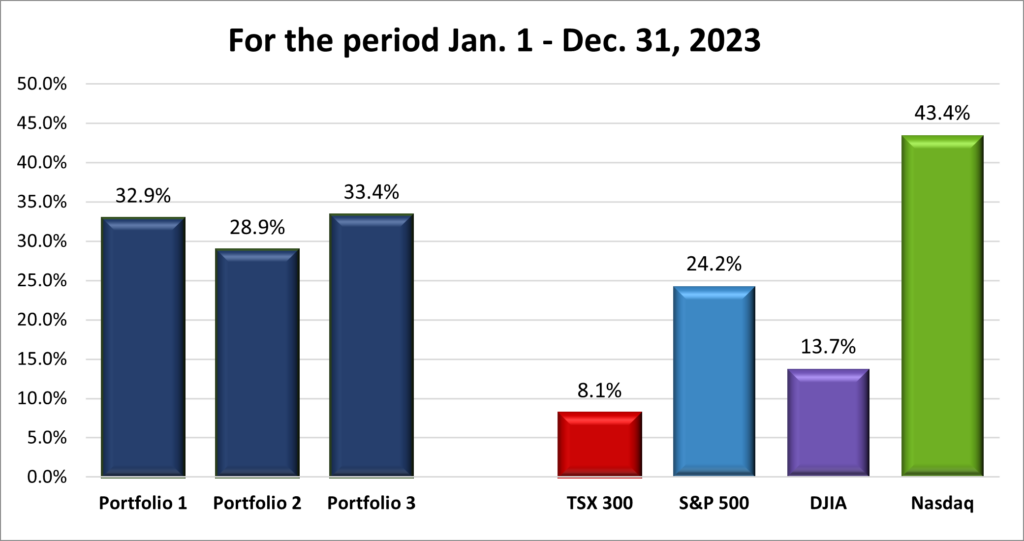

For 2023, the TSX rose 8.1%, the S&P surged 24.2%, the DJIA climbed 13.7% while the Nasdaq soared 43.4%.

![]() Twelve months ago, analysts almost universally anticipated a recession, arguing that only an economic downturn triggered by the steepest interest rate increases since the 1990s could temper inflation. Yet, the expected downturn did not materialize as predicted. In Canada, inflation decreased from 5.9% in January to 3.4% by December, however, the economy was stagnant in the latter half of the year. In the US, inflation dropped from 6.4% to 3.4% over the same period. Unlike in Canada where the economy stalled, the American economy remained robust. A strong economy suggests that the Fed may indeed achieve a ‘soft landing’ (where inflation falls to the 2% target without the economy going into a recession), highlighting the precarious nature of market predictions.

Twelve months ago, analysts almost universally anticipated a recession, arguing that only an economic downturn triggered by the steepest interest rate increases since the 1990s could temper inflation. Yet, the expected downturn did not materialize as predicted. In Canada, inflation decreased from 5.9% in January to 3.4% by December, however, the economy was stagnant in the latter half of the year. In the US, inflation dropped from 6.4% to 3.4% over the same period. Unlike in Canada where the economy stalled, the American economy remained robust. A strong economy suggests that the Fed may indeed achieve a ‘soft landing’ (where inflation falls to the 2% target without the economy going into a recession), highlighting the precarious nature of market predictions.

As shown in the chart above, all four major North American indexes posted sizable gains in 2023. The S&P closed the year up 24.2%, marking its largest gain since 2021, though it fell short of reaching a new record high. This past year’s performance underscores the S&P’s resilience, despite the absence of setting a new peak for the first time since 2012. Over 65% of S&P member companies ended the year higher, though more than half underperformed the index itself. The year’s gains were disproportionately driven by the ‘Magnificent 7’ technology companies, which capitalized on the artificial intelligence (AI) tailwind, highlighting the increasing market concentration in these top performers. Their dominance reflects the broader sectoral performance, with Technology and Communications Services sectors soaring by 56.4% and 54.4%, respectively, and together constituting 38% of the S&P’s weight.

Despite its 43.4% surge, the Nasdaq did not reach a new high, while the DJIA set a record on December 13, contributing to its 13.7% annual gain. The TSX lagged behind, with ‘only’ an 8.1% increase. 😊

These impressive performances comes on the heels of a dismal 2022 that saw the S&P decline 19.4%, the DJIA fell 8.8%, the Nasdaq tumble 33.1% and the TSX drop 8.2%. Despite the higher interest rates in both countries that started climbing in 2022, the markets demonstrated remarkable resilience.

While the monetary decisions made by the BoC can weigh on the TSX, the Canadian stock markets are more influenced by what the Fed does when it comes to interest rate movements. The markets tend to move to the beat of the Fed. On June 7, 2023, the BoC raised the Canadian key interest rate, or benchmark rate, to 5.0% where it remained as of December 31, 2023. In July, the Fed raised the benchmark interest rate to the current target range of 5.25% to 5.50% where it remained at the end of the year.

In December, at the last meeting of the Federal Open Market Committee (FOMC), the Fed forecast up to three rate cuts in 2024, making it the only central bank in the world to signal a readiness for lowering interest rates in the coming year. Investors are now keenly watching for signs of when the Fed might start lowering the rate. Given the considerable influence of the Fed’s monetary policies (interest rate decisions) on market dynamics, especially in sectors sensitive to interest rate changes, the anticipation around these potential cuts is considerable. The sooner both central banks start lowering their respective rates the better, I say. 😊

Reflecting on the past year, the anticipated economic downturn due to aggressive interest rate hikes did not unfold as expected. Instead, inflation rates moderated in both Canada and the US, displaying resilience in the American economy and a period of stagnation in Canada. Stock markets across North America rebounded impressively, with technology and AI advancements driving significant gains, particularly within the technology heavy S&P and Nasdaq indexes. The focus now shifts to central banks, especially the Fed, which hinted at potential rate cuts in 2024, highlighting the critical influence of monetary policy on market dynamics and investor sentiment.

Twelve Month Portfolio Review

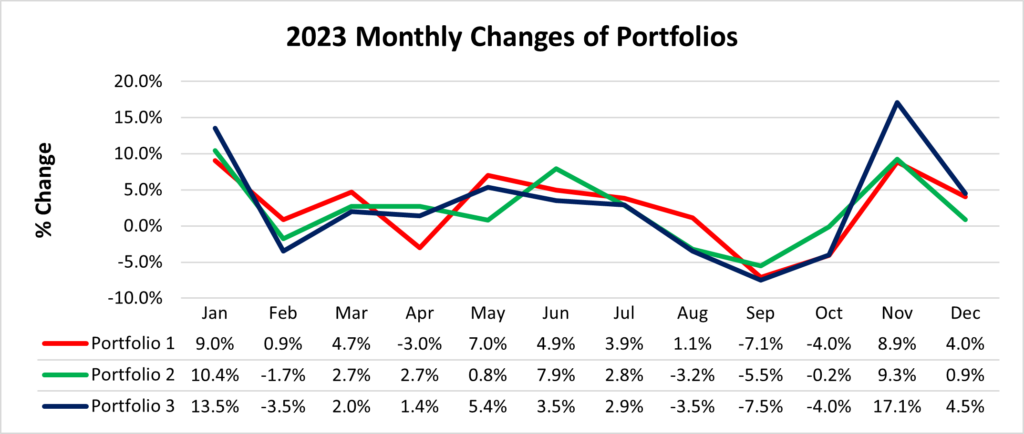

2023 was a year that saw the American markets soar and the Canadian markets climb steadily, but our portfolios did something spectacular—they mostly outperformed the S&P, DJIA, and the TSX, with only the Nasdaq’s staggering 43% gain edging them out, as shown in the char below. Each portfolio’s journey through 2023 was a testament to forward thinking and patience in the dynamic world of investing.

The journey was not smooth, as seen in the chart below, but the result was rewarding. Each portfolio had its unique set of ups and downs, resembling a rollercoaster ride more than a straightforward path to success. Despite this volatility, each portfolio managed to record eight months of gains against four months of losses, with the best performances in January and November when each portfolio posted outsized gains.

Portfolio 1 benefited significantly from its investment in six of the “Magnificent 7” technology giants, highlighting the power of leading tech firms in driving growth. Despite a brief setback due to falling oil prices and interest rate worries, strategic investments led to a strong finish, especially as worries over central bank rate hikes began to subside.

Portfolio 2 rode the early tailwind of technology stocks higher and, despite the shake-up from the US banking crisis, managed to rebound through most of the summer. After a dip in the fall, Portfolio 2 closed the year strongly, propelled by a late surge caused by positive investor sentiment toward impending lower interest rates.

Portfolio 3 demonstrated the impact of having surging tech giants like Microsoft and Shopify (TSE: SHOP), with their significant gains highlighting the portfolio’s strength. Despite interest rate concerns, a late-year rally, particularly in Shopify, underscored the value of strategic stock selection.

As the chart below vividly shows, 2023 was indeed a remarkable year for each portfolio. I am looking forward to more years like this past one. 😊

2023 in Review

Looking back on 2023, it was an eventful year. The year kicked off with the meteoric rise of what has been dubbed the “Magnificent 7” – a group of large American technology companies. These firms carried the S&P in 2023, gaining nearly 75%, while the remaining 493 companies of the index only gained about 9%. The rising tide of these companies also helped lift the DJIA and the TSX. The common thread among these companies was their significant involvement in, or benefit from, a burgeoning tailwind in AI. These companies gained momentum in late 2022 and investor optimism about the promise of AI carried them and others associated with AI throughout 2023.

By the end of the first quarter, a banking crisis unfolded in the US, marked by the collapse of several regional banks. This was primarily due to the strain of rising interest rates, which exposed vulnerabilities in their financial health. As the year progressed, the focus shifted to the trajectory of interest rates. Both the BoC and the Fed had raised benchmark interest rates in 2022 to combat inflation, a trend that continued into 2023. The cessation of rate hikes in the latter half of the year led to speculation about potential decreases. However, both central banks maintained a stance that higher rates would persist to ensure inflation returned to target levels, signaling a ‘higher for longer’ policy approach.

November saw the markets embark on a rally that persisted until year’s end, fueled by declining inflation, the halt of interest rate increases in the US, and optimism that the Fed could achieve a ‘soft landing’. To end the year, supply chain issues, which first burst into consumers’ consciousness during the COVID-19 pandemic, made a surprising return. Initially thought to be resolved, these challenges were reignited by geopolitical tensions in the Middle East that impacted the vital Red Sea shipping lane, once again threw global supply chains into disarray.

However, a review of 2023 would be incomplete without highlighting the profound impact of AI. This sector was a focal point throughout the year, with any company involved in AI experiencing a surge in both sales and stock prices. Two companies stood at the forefront of this AI revolution: Nvidia and Microsoft. Nvidia’s share price skyrocketed by 230%, thanks to its dominance in supplying the chips crucial for AI development. This demand for Nvidia’s hardware underscored the integral role of AI-specific infrastructure in technological advancement.

Microsoft, on the other hand, emerged as a pioneer with its rollout of AI-enhanced applications, establishing itself as a leader in this nascent industry. This strategic positioning rewarded Microsoft with a 53% increase in its share price—a remarkable achievement for a corporation of its size and a testament to the transformative potential of AI.

As we bid farewell to 2023, a year marked by both headwinds and tailwinds, it is clear that economic resilience and innovation have driven the investment landscape. From the resurgence of supply chain issues to the AI revolution, there were many challenges and opportunities. With markets moving higher, it was a much easier time mentally to be an investor. 😊

Going Forward: The First Quarter 2024 and beyond

2024 brings a mix of familiar trends and exciting new opportunities in the investment world. Smart planning, combined with lessons learned in the past, should help you ride these waves with confidence. Let’s delve into the key themes shaping our investment strategies in the year ahead.

The drive to fortify supply chains, a lesson underscored by the COVID-19 pandemic, continues with vigor. Efforts to minimize dependencies by enhancing North American infrastructure signal robust opportunities in sectors like semiconductors, renewable energy, raw materials, and resources, as well as infrastructure. Investors should watch for companies and projects at the forefront of this transformation, as they stand to gain from governmental and corporate investments aimed at ensuring resilience against future disruptions.

The remarkable performance of the ‘Magnificent 7’ dominated market narratives in 2023, but as these giants face the law of large numbers, attention is shifting. The landscape is ripe for the emergence of new leaders or the reconfiguration of market dominance. This transition period presents an opportunity for investors to diversify, seeking growth in undervalued sectors or companies poised to benefit from broader economic shifts, including technology, healthcare, and green energy.

The Fed has signaled potential interest rate cuts in 2024 with the BoC likely to follow suit, the overall market appears conducive to a broader market rally. Lower interest rates could relieve pressure on consumer and corporate debt, thereby stimulating spending and investment. However, investors should remain vigilant, adapting to the pace and scale of policy shifts, and considering their implications across asset classes—from equities to real estate.

While the cooling American economy and stabilizing inflation rates suggest a move towards a ‘soft-landing’, unforeseen geopolitical events, including the US presidential election, could introduce volatility. Investors would benefit from maintaining a balanced portfolio, hedging against potential market turbulence through diversification across geographies and sectors.

On a personal note, the gradual consolidation of holdings—from 65 to 60 companies in Portfolio 1—reflects a strategic choice to focus on quality over quantity. Hopefully, some of the companies will become the next stars of the investing world, with Nvidia like performance, while others will just continue their relentless ascent in value. 😊 The aim is not just to replicate the success of 2023 but to build a resilient and dynamic portfolio prepared for the opportunities and challenges of 2024.

As we look ahead with cautious optimism, we will need to maintain an eye on evolving market dynamics, to improve the chances for success in 2024. Wishing you all the best in your investments in the year ahead. Good luck, and long may the bulls run! 😊