Items that may only interest or educate me ….

Oil price caps, latest change to the Canadian interest rate, electric vehicles are not enough to offset the energy consumption of global population and economic growth, will there be a Nickel cartel, …

This week marked the start of the Group of 7 (Canada, France, Germany, Italy, Japan, the United Kingdom, and the USA) and Australia attempting to impose a US$ 60 a barrel price cap on Russian oil. The G7 is hoping the price cap on Russian oil will limit Russia’s ability to finance their invasion of Ukraine. Russia has stated it will cut oil supplies to any country that attempts to implement the G7’s price cap.

As well, at the start of the week, OPEC+ (OPEC members and eleven other non-OPEC nations), who account for 90% of global oil reserves, announced they will maintain their October plan to lower their production by two million barrels a day. The lower OPEC+ output, combined with Russia’s plan not to provide oil to countries that comply with the G7’s price cap on Russian oil, could lead to oil shortages during the coldest part of the year in the northern hemisphere. This in turn would cause the price of oil to return to OPEC+’s desired US$ 90 a barrel. OPEC’s next planned meeting to review production levels is not until June 2023. Assuming the G7 can enforce their price cap, and Russia and OPEC+ stick to their quotas, oil prices should remain high for another six months unless non-OPEC oil producing nations (such as Canada and the US) can fill the void.

That should be good news for those invested in oil companies. However, and those are three major assumptions that need to hold. A break in one and oil prices could fall lower. Either way, I expect shares of oil companies to remain volatile.

On December 7, the Bank of Canada (BoC) delivered an increase of 0.5% to Canada’s benchmark interest rate, the seventh consecutive increase. This brings the rate to 4.25%, its highest point in 15 years. Economists expected 0.5% increase while the market was hoping for 0.25%. The good news was the BoC indicated the interest rate increases were nearing an end and will now consider upcoming data to determine if further hikes are necessary. Economic data has shown the labour market remains strong and high inflation persists, but demand slowed significantly in the third quarter (July 1 – September 30). The question now is what the BoC’s magic number is when they will stop increasing rates. We will get our next clue at their subsequent meeting planned for January 25, 2023.

Canada’s rate has gone from 0.25% in March to 4.25% nine months later. A record pace that puts it slightly above the current US interest rate of 4.0%. However, the US rate will go higher next week when the US Federal Reserve (Fed) announces its latest change to the US cost of borrowing.

It did not take long for Canada’s big five banks to bump their lending rate. They raised their prime lending rate by 0.5%, effective December 8. For anyone borrowing money from the banks, this is not good news whether you are borrowing is done in the form of credit cards, mortgages, lines of credit, or loans (personal or business).

One would think with the growing number of electric vehicles (EVs) they would at least put a dent in conventional energy (oil, natural gas, and coal) consumption. However, according to Morgan Stanley’s Martin Rats, head of European Oil and Gas Research, that is not the case. Norwegians have readily taken to EVs with over 70% of new cars being EVs, but Norway’s oil consumption has stayed the same, if not grown. On the surface it appears there is a disconnect between the claims that EVs will lower oil consumption, (therefore reduce greenhouse gases) and cold, hard reality.

According to the report, Norwegian population growth and rising standards of living increased the use of oil more than enough to offset oil consumption saved by driving EVs. While the study only looked at Norway, if the data is extrapolated to a global scale, growing population and an increasing standard of living may be the biggest challenge to climate change. While EVs are a step in the right direction, they are not the silver bullet. Renewable energy must scale up considerably, but that cannot happen overnight. Until then the world will require traditional fossil fuels to continue to raise the standard of living for a growing global population.

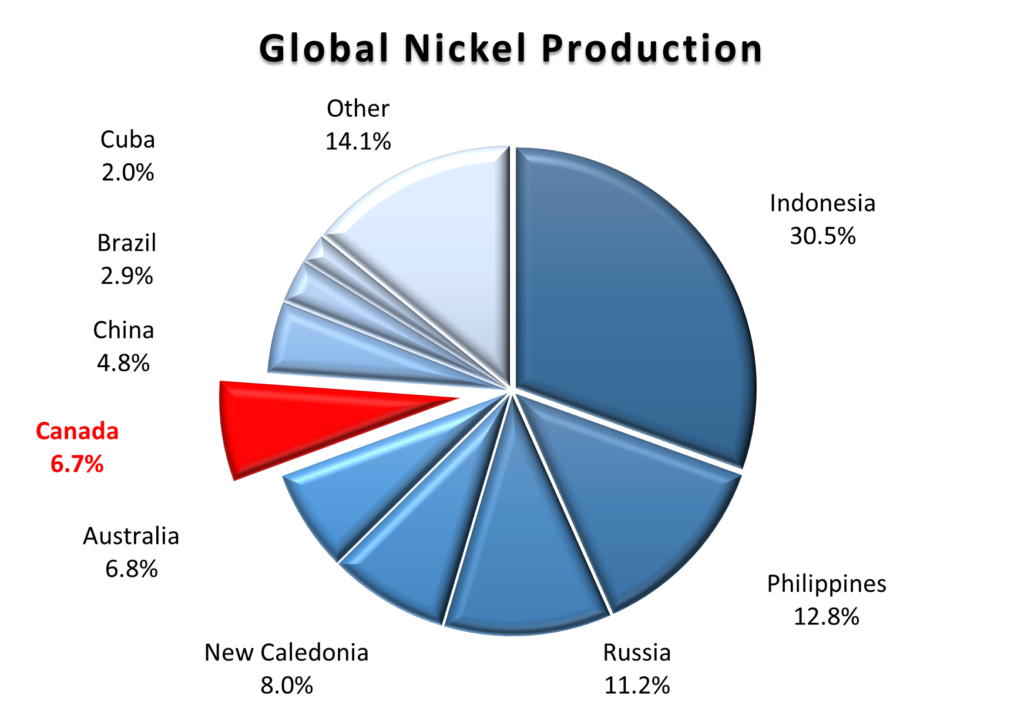

Indonesia wants to be the main player in the electric vehicle industry and has invited other big producers, including Canada, to form a nickel alliance. At the recent United Nations Climate Change Conference, also known as COP27, Canada was approached by Indonesia about joining together with other nickel producing countries to become what would essentially be a nickel cartel. As you can see in the chart below, Indonesia (30.5%), Philippines (12.8%) and Russia (11.2%) currently provide over 54% of the world’s nickel supply. Canada currently provides almost 7% of global production. Add Canada, or one of the other top five nickel producers, and a nickel cartel would have more control over nickel than the Organization of the Petroleum Exporting Countries’ (OPEC) had over the control of oil supply at its highest point of 54% in the early 1970s.

Managing the supply and price of nickel would benefit all member countries, much like OPEC’s supply control benefits its members. However, Canadian producers plan to market their nickel as a better grade of nickel – cleaner and purer – as well as being better for the climate thanks to Canadian producers’ overall lower total carbon footprint to mine and produce the nickel. If companies are prepared to pay more for Canada’s higher-grade nickel, then joining a cartel would eliminate those advantages because Canadian producers would have less control over the price.

So, why does Indonesia want to create a cartel to control the price of nickel? While over 70% of nickel goes to the production of stainless steel, the growing production of electric vehicles (EV) is causing a surge in the demand for nickel to produce the batteries that power them. As a result, high grade Canadian nickel, which once accounted for 80% of global supply back in the 1960s, is seeing new demand as a key component in batteries. In order to secure a supply of exceptionally pure nickel, car manufacturers are starting to sign deals with miners. A good example is General Motors (NYSE:GM) recent agreement with Vale S.A.’s (NYSE:VALE) Canadian unit to supply GM with battery grade nickel, starting in 2026. Not only does this lock in a supply of high-grade nickel but it also allows GM to take advantage of the US’s Inflation Reduction Act (IRA), which offers tax credits for new and used EVs. It also provides a secure source of nickel from the US’s largest trading partner. For Vale, they have secured a long-term contract for their nickel.

Canada is correct to avoid a cartel if their product is in fact a higher-grade nickel, produced in a more environmentally friendly manner. With the concerns about the environment, companies should be prepared to pay a premium for a better grade of product from a trusted, reliable, and nearby source (lower transportation costs). Not to say that other nickel producing countries are not dependable, but I do not think many companies will want to rely on Russia for their supply given events of 2022. I also think GM’s deal with Vale is a good deal for both companies as it will lock in a supplier and a market for both companies. I suspect there will be similar deals between EV companies and mining companies in the coming months and years.

With that eclectic collection of news tidbits to chew on, lets look back at the week that was December 5 to December 9. As Daenerys would say, “Let’s begin.”

Weekly Market Review

Monday: Once again the bell tolled for the four major North American indexes as they each dropped by more than 1% today. In Canada, on the Toronto Stock Exchange Composite Index (TSX), investors took some money off the table after two weeks of gains and ahead of the Bank of Canada (BoC) announcement. In trading, the defensive Canadian sectors Telecommunications Services and Utilities were the only Canadian sectors to gain any ground. The Canadian Technology and Consumer Cyclical sectors dropped the most.

In the US, it was a case of good news equals bad news that caused a broad retreat across the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq). The good news was the better-than-expected US services industry data that followed on last week’s strong job and wage growth in November. The services data, job growth and higher wages suggest the US economy is still strong. The bad news was the strong economic data could lead to a higher interest rate target by the US Federal Reserve (Fed), and the higher rate staying in place longer. In the market, it was broad based retreat where the S&P Utilities and Healthcare sectors were the best of a bad lot, dropping the least.

Tuesday: All four indexes failed to rebound from yesterday’s losses as each index each dropped by more than 1% again. In the US, investors were concerned about next week’s interest rate increase by the Fed, and the possibility the US economy could fall into a recession. In the markets, only the S&P Utilities sector was able make headway today, with the Technology and Energy sectors tumbling the farthest.

In Canada, investors prepared for Wednesday’s BoC interest rate hike. Investors are anticipating a 0.25% hike to the benchmark Canadian interest rate with an outside shot at a 0.5% hike. For what its worth (nothing), I will go with a 0.5% increase. In trading, the TSX was dragged lower by falling oil and natural resources prices. All Canadian sectors fell back with the Healthcare and Energy sectors the worst performers.

Wednesday: The North American markets continued this week’s slide into the third day, causing three of the four major indexes to end lower, while the DJIA was flat. In Canada, lower oil prices, combined with the 0.5% increase to the Canadian interest rate dragged the TSX lower. The 4.25% Canadian interest rate is the highest it has been since January 2008. In the market, the Canadian Consumer Staples and Consumer Cyclical sectors performed the best of five sectors that ended in the black, while the Healthcare and Technology sectors fell the most.

In the US, investors were concerned the Fed will maintain higher interest rates longer than anticipated, which could put the American economy into a recession. Of the S&P sectors, only the Healthcare and Consumer Staples sectors were able to end in the black, with Technology and Consumer Cyclical were the deepest in the red.

Thursday: It was the first time in December that all three American indexes were on the winning side on the same day. Unfortunately, the TSX did not get the memo until late in the day and ended just below the bar, extending its losing streak to five days. In Canada, oil prices fell to their lowest level this year, dragging the TSX lower. Despite the TSX ending lower, the Canadian sectors were evenly split, with Consumer Staples and Consumer Cyclicals leading the way of the group of sectors that ended higher. Of the sectors that dropped, the Telecommunications Services and Energy sectors fell the farthest.

In the US, investors took an increase in weekly jobless claims as a sign interest rate hikes could finally slow down. Investors decided to take advantage of the recent downturn and cautiously waded back into the markets. On the trading floor, the S&P Technology and Consumer Cyclicals sectors advanced the most with the Telecommunications Services and Energy sectors the only S&P sectors to end lower.

Friday: The week ended the same way it started with all four major indexes ending the day lower. The main driver of the markets was on-going fears that higher interest rates in both Canada and the US would push their respective economies into a recession.

In Canada, the TSX ran its losing streak to six days as a late afternoon decline nudged the TSX under the line and into the red. Investors are worried the BoC will need to keep the Canadian interest rate above 4% for most of 2023. Softer global oil prices also contributed to the TSX’s decline. In trading, the odd combination of the defensive Canadian Utilities sector and the growth oriented Canadian Technology sector led the gainers while Consumer Cyclical and Energy sectors fell the most.

In the US, a higher-than-expected Producer Price Index (PPI) showing an increase of 7.4% (investors were expecting 7.2%) triggered a broad-based sell off across the three American indexes, causing all of them to end slightly lower. The PPI report ignited fears the Fed would continue their aggressive rate hike with a 0.5% boost next week. On the real and virtual trading floors, the S&P’s Telecommunications Services and Financials sectors were the best performers because they dropped the least, with Energy and Healthcare tumbling the most.

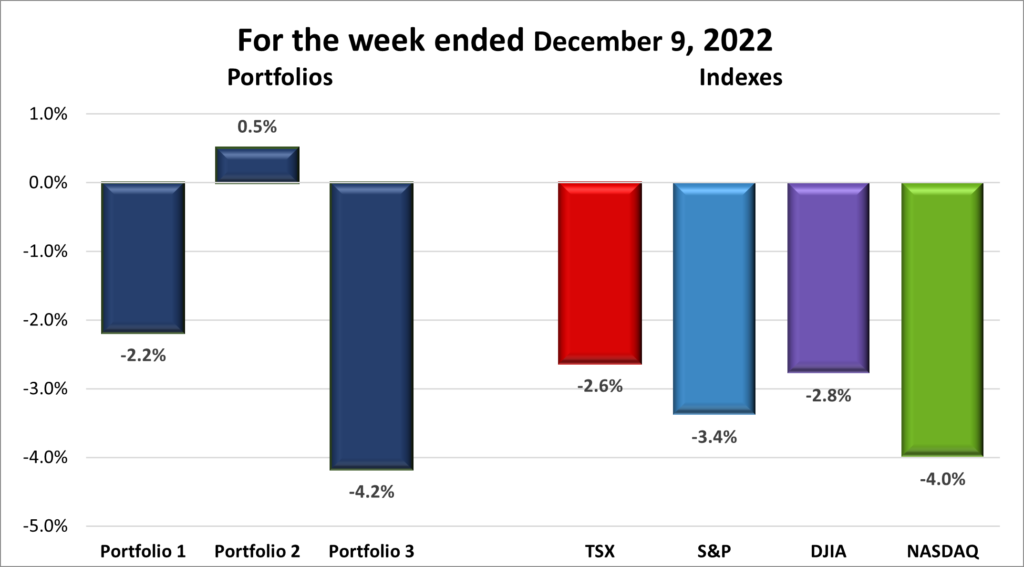

After two straight weeks of weekly gains, all four indexes ended this week lower. As you can see on the chart below, for the week, the TSX (SPTSX) dropped 2.6 %, the S&P 500 (SPX) fell 3.2%, the DJIA (INDU) sank back 2.8% and the Nasdaq (CCMP) declined 4.0%.

Weekly Portfolio Review

Given the downward trend of 2022, its not surprising after 2 consecutive weeks of weekly gains that all four indexes resumed their respective downward trends. Rising interest rates and fear of recessions were the big market drivers this week. Once again, the most interest rate sensitive indexes dropped the most (Nasdaq and S&P). Lower oil prices contributed to the TSX’s fall while the DJIA probably was dragged down by the negative market sentiment.

Given the overall performance of the four indexes, I was surprised to see Portfolio 2 was able to creep higher this week. Normally I would say because its more balanced but this week the credit must go to a high growth technology company – MongoDB (NASD:MDB). The company had a great third quarter earnings report, causing the share price to pop 32% this week. A jump like that will do wonders for a portfolio. As for Portfolio 1 and 3, nothing jumps out other than they were dragged down by the overall market’s downward trend. Portfolio 3’s heavier technology weighting caused it to fall farther than Portfolio 1.

Companies on the Radar

Several professional investment strategists are predicting a further drop in the market for 2023. I do not know what is going to happen in the market on a day-by-day basis, let alone a few months from now. I suspect it will go down, so I will just sit on the sidelines unless a tremendous opportunity presents itself. In the meantime, I will continue to monitor the three portfolios for opportunities to add to winners such as the ones currently on the Radar list, below.

- Crew Energy (TSX:CR): A Canadian oil and gas company with interests in British Columbia.

- International Petroleum (TSX:IPCO): A Canadian company with oil and gas assets in Canada, Malaysia, and France.

- Alvopetro Energy (TSXV:ALV): A Canadian natural gas company developing natural gas projects in Brazil.

- Alphabet (NASD:GOOGL): The leading online search engine and advertising company, dominant mobile operating system.

Below are my Radar Checks on these companies, updated December 9, 2022.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended December 9, 2022: DOWN ![]()

- Amazon (NASD:AMZN) launched a new service called Amazon Omics aimed at healthcare and life science organizations. This service will provide healthcare researchers the ability to take raw data and convert it into more useful formats. It will also provide more computing power than most medical researchers have available inhouse.

- General Motors’ (NYSE:GM) BrightDrop electric delivery truck unit saw its first vehicles leave their new, retooled factory in Ontario. BrightDrop also signed DHL Express Canada as its first customer outside the US.

GM said it is seeing strong demand for its products and expects 2023 to be better than 2022 in terms of new car sales - Apple (NASD:AAPL) has rolled back the target date for its self-driving electric car until some time in 2026. Personally, I would be more interested in an electric vehicle from Apple than a self driving version.

- Tesla (NASD:TSLA) announced a temporary stoppage of production of their Model Y electric vehicles from December 25 to January 1 at their Shanghai facility. While it may be common to take the week off between Christmas and New Year’s Day here in Canada, it is not common in China for the factory to be shut down for the week.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

No C$ dividends this past week.

US $

ZIM Integrated Shipping Services Ltd (NYSE:ZIM)

Quarterly Reports

Docusign, Inc.

All currency listed in thousands of US dollars, except per share data

Selected highlights from their third quarter 2022 financial results on December 8, 2022

- Revenue of $645,463 for the three months ended October 31, compared to $545,463 for the same period in 2021. An increase of over 19%.

- Net loss of $29,866 for the three months ended October 31, compared to net loss of $5,676 in the same period in 2021.

- Diluted loss per ordinary share of $0.15 for the three months ended October 31, compared to a loss of $0.03 for the same period in 2021.

- Revenue of $1,856,339 for the nine months ended October 31, compared to $1,526,385 for the same period in 2021. An increase of almost 22%.

- Net loss of $102,317 for the nine months ended October 31, compared to net loss of $39,531 in the same period in 2021.

- Diluted loss per ordinary share of $0.51 for the nine months ended October 31, compared to a loss of $0.20 for the same period in 2021.

Portfolio 2

Portfolio 2 for the week ended December 9, 2022: UP ![]()

- Disney’s (NYSE:DIS) recently launched its ad-based Disney+ streaming service to complement its ad free Disney+ subscription service. It looks like there are plenty of companies ready to advertise on this new service as more than 100 companies from a variety of sectors plan to advertise on Disney’s lower cost option. The ad version of Disney+ goes for US$ 7.99 per month while the ad free Disney+ is available for US$ 10.99 per month. In Canada, its C$11.99 per month for the ad free subscription. The ad supported version is currently not available in Canada.

- TC Energy (TSX:TRP) temporarily shutdown its Keystone pipeline due to 14,000 barrels of crude oil leaking into a pasture in Kansas. The pipeline is a primary feeder of Alberta crude oil to the US refineries in the US Midwest and Gulf coast regions. Without the pipeline, Alberta oil producers may have to turn to rail to get the oil to the refineries. The company immediately dispatched teams to respond to the leak and provide an estimate when the pipeline will be back online.

- As part of a larger strategy, Guardant Health (NASD:GH) will work with AstraZeneca to create a companion diagnostic test that can be used to identify patients with certain forms of metastatic breast cancer. The project is part of a plan to use a liquid biopsy “as a tool to inform early therapy intervention.”

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

No C$ dividends this past week.

US $

Microsoft Corp (NASD:MSFT)

Quarterly Reports

MongoDB, Inc.

All currency listed in thousands of US dollars, except per share data

Selected highlights from their third quarter 2022 financial results on December 6, 2022

- Revenue of $333,621 for the three months ended October 31, compared to $226,893 for the same period in 2021. An increase of over 47%.

- Net loss of $84,841 for the three months ended October 30, compared to net loss of $81,293 in the same period in 2021.

- Diluted loss per ordinary share of $1.23 for the three months ended October 30, compared to a net loss of $1.22 for the same period in 2021.

- Revenue of $922,728 for the nine months ended October 31, compared to $607,288 for the same period in 2021. An increase of almost 52%.

- Net loss of $281,000 for the nine months ended October 31, compared to net loss of $222,418 in the same period in 2021.

- Diluted earnings per ordinary share of $4.11 for the nine months ended October 31, compared to a net loss of $3.49 for the same period in 2021.

Portfolio 3

Portfolio 3 for the week December 9, 2022: DOWN ![]()

- Brookfield Asset Management (TSX:BAM.A) announced the spinoff of its asset management unit will start trading December 12. Shareholders of Brookfield will receive one share of the spinoff for every four shares they own of Brookfield. Starting December 12, what is currently known as Brookfield Asset Management will be known as Brookfield Corporation and trade under the ticker BN on the TSX and New York Stock Exchange (NYSE). The spinoff will retain the name Brookfield Asset Management and trade under the ticker BAM on the TSX and NYSE. I wonder how many people will be confused when they see their monthly statements and try to figure out that BAM is the spinoff of BN, a company they knew nothing about on their previous monthly statement? 😊

- Microsoft (NASD:MSFT) entered into a 10-year commitment to make the popular game ‘Call of Duty’ available on Sony’s PlayStation and Nintendo’s Switch the same day it was released on Xbox. Despite this attempt to appease regulators over their acquisition of Activision Blizzard (NASD:ATVI), the US government took steps to stop Microsoft from gaining control of Activision. The government claims Microsoft will use control of the Activision games and content to harm its competitors in the gaming industry. Microsoft claims it acquired Activision to draw gamers to their various platforms and their Xbox subscription gaming service.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

No C$ dividends this past week.

US $

Microsoft Corp (NASD:MSFT)

Quarterly Reports

No quarterly reports this past week.