Items that may only interest or educate me ….

Santa rally, US CPI report, US interest change, EVs killing the AM radio stars …

Will there be a Santa Claus rally in 2022? The stock markets typically get a boost in December’s holiday season thanks to upbeat retail/individual investors, many with year-end bonuses itching to be spent. Since professional and institutional investors tend to take the last week of December off, individual investors have the run of the markets, so to speak, and tend to buy stocks before the end of the year, providing a little boost to the markets to start off the new year. Given the trend of 2022, where rallies are followed by lower lows, if there is a rally, it is likely to be short lived before reverting to the downward trend of 2022.

The US Bureau of Labor Statistics released their Consumer Price Index (CPI) report for November showing US inflation rose 7.1% compared to November 2021 and the core CPI (CPI less volatile food and gas prices) rose 6.0%, year over year. Both numbers came in lower than expected, 7.3% for CPI and 6.1% for the core CPI. Coupled with the last five months of declining inflation data, the numbers suggest a downward trend and the US economy is starting to cool off. This gave the Fed some leeway to slow the pace of increases to the US benchmark interest rate….

As expected, the US Federal Reserve (Fed) did indeed ease off the gas pedal of higher interest rates, however slightly. In an effort to keep a recession at bay while reigning in inflation, the Fed announced an increase of 0.5% to the US benchmark interest rate, bringing the interest rate to 4.25%. Considering the previous four increases were 0.75%, a 0.5% increase was a relief. Another hike for sure, but at least its lower than the previous four increases. The Fed also stated it was no longer “as important how fast we go” indicating additional increases but not as big as recent increases.

As expected, the US Federal Reserve (Fed) did indeed ease off the gas pedal of higher interest rates, however slightly. In an effort to keep a recession at bay while reigning in inflation, the Fed announced an increase of 0.5% to the US benchmark interest rate, bringing the interest rate to 4.25%. Considering the previous four increases were 0.75%, a 0.5% increase was a relief. Another hike for sure, but at least its lower than the previous four increases. The Fed also stated it was no longer “as important how fast we go” indicating additional increases but not as big as recent increases.

The belief a smaller interest rate hike was coming, combined with the preceding five months of CPI data indicating inflation was declining, had boosted the optimism of investors and overall market sentiment. However, this week’s announcement by the Fed put an end to that optimism. It was not the hike itself (which was expected), but the Fed’s outlook for 2023 that sent the markets tumbling. The announcement suggested additional rate increases throughout 2023 would be necessary and that could push the interest rate above 5% by the end of 2023. Back in September, the Fed had projected a peak interest rate of 4.6%, so this latest projection came as a surprise. The market does not like surprises.

Going forward, the message from the Fed should be clear by now – the Fed is serious about getting inflation back down to its 2% target. The challenge is that increasing rates too aggressively would risk driving the economy into a painful recession. Not raising the interest rates enough would allow price increases to remain high, leading to stubbornly high inflation. We will see how well the Fed navigates between driving inflation down and avoiding a recession.

The impact of the interest rate hikes made in 2022 will start to have a noticeable impact by the end of spring, if not a few months before. While the US financial system is currently strong, economists are predicting the economy is expected to weaken or even slide into a recession. If a recession is declared, the markets can start looking forward to when the economy exits the recession. However, during the recession, demand will fall allowing supply chains to return to normal, employment and wage growth will soften, and companies that were on financially shaky ground before the recession could go out of business.

During a recession, a sort of law of the jungle take place with the survival of the fittest. Companies with strong Balance Sheets (lots of cash, little debt) can take advantage of weaker companies by acquiring those that would enhance or add value to their existing product line.

For individual companies, if they are going to have a weak earnings report or two (lower revenues and/or net income), they will take the opportunity to dump any useless assets. Its better to get all the bad news out under the cover of a recession than to have the bad news overshadow a good earnings report.

Its not only Canada and the US that are experiencing higher and rising benchmark interest rates. The Bank of Mexico increased its key interest rate by 0.5% to 10.50%, after hiking the rate by 0.75% to 10% in November. In the United Kingdom, The Bank of England raised the key British interest rate by 0.5% to 3.5%. The European Central Bank raised interest rates in the European Union by 0.5%, bringing the European Benchmark interest rate to 2.0%. Misery loves company. 😊

While video may have killed the radio stars, electric vehicles (EV) are slowly but surely killing off AM radios. Due to the electrical interference caused by the batteries in electric cars, electric vehicle manufacturers have decided rather than fix the problem with filters and shielded cables they would simply drop the AM signal all together. Already Audi, Porsche, and Tesla are a few of the companies that have already removed the AM band radios from their EVs, and Ford is planning to drop it from their upcoming electric F-150 models. Drivers currently tune into AM radio for the latest traffic and news updates, or listen to sporting event broadcasts, sports talk shows, or any other AM show. As well, the government utilizes the AM band to communicate directly with the public during an emergency. If/when you buy an EV, you will likely be cutting the AM cord and killing the AM radio industry.

Based on the market this past week, the Grinch may have come early and put an end to a hoped-for rally to end the year. However, there are two weeks left for a Santa rally to emerge. While we wait longingly for Santa to appear, lets take a look at the past week…

Weekly Market Review

Monday: Finally, the four major North American indexes start the week off on a winning note. In Canada, the Toronto Stock Exchange Composite Index (TSX) rose on higher oil prices and investor optimism that the US Consumer Price Index (CPI) will come in lower than the market expects. In the Canadian market, the Technology and the Utilities sectors led the Canadian sectors. The Consumer Staples and Consumer Cyclical sectors were the worst performers and the only two Canadian sectors to slip back.

In the US, the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) all gained more than 1%. Investors lifted the market in anticipation of a good news CPI report that would enable the US Federal Reserve (Fed) to raise the US benchmark interest rate by 0.5%.

It was a broad-based advance across all three indexes, with the S&P Energy sector and the Utilities sector gaining the most, with the Basic Materials (Mineral miners and fertilizer manufacturers) and the Consumer Cyclical sectors bringing up the rear.

Tuesday: For the second consecutive month, inflation in the US came in below expectations sending all four indexes sharply higher in morning trading. Concerns about the Fed’s interest rate hike due tomorrow brought the indexes back down before settling just above the bar. In Canada, oil, technology, and mining companies were the main beneficiaries of the good news out of the US. In the marketplace, Energy and Basic Materials were the best performing Canadian sectors with Financials, Consumer Cyclicals, and Telecommunications Services the only three Canadian sectors to end lower.

In the US, the lower-than-expected CPI data was offset by fears the Fed could remain aggressive with their interest rate increases. In trading, the S&P Energy and Technology sectors gained the most while the Telecommunications Services and Consumer Staples were the only sectors to fall back today.

Wednesday: The markets fell when the Fed announced an increase of 0.5% to the US benchmark interest rate, their seventh hike of 2022. This brought the US benchmark rate to 4.5%, its highest point since 2007. It was not so much the increase as it was the Fed’s forecast that it expected higher rates for longer than originally thought. Despite the markets ending down, the price of oil rebounded on forecasts for increased demand for oil in 2023.

On the TSX, the news out of the US was enough to end the TSX’s winning streak. Only the Canadian Consumer Cyclical sector was able to make it into the black today. The Canadian Financials and Industrials sectors had the biggest setbacks for the day.

In the US, estimates of the US interest rate going higher for longer sent the S&P, DJIA and Nasdaq indexes tumbling. Healthcare and Consumer Staples were the only two S&P sectors to inch into positive territory, while the Telecommunications Services and Financials sectors fell the most.

Thursday: On the heels of Wednesday’s pessimistic outlook from the Fed and fears of a recession in 2023, all four indexes fell sharply today. It was a broad-based retreat as all sectors in Canada and the US ended in the red. In Canada, the Canadian defensive sectors Utilities and Healthcare fell the least while the Canadian Basic Materials and Technology sectors were hit the hardest.

In the US, all three major American indexes each dropped by more than 2%. Of the approximately 500 companies in the S&P, only fourteen ended the day higher. The American S&P Energy and Utilities sectors were the best performers even though both sectors ended the day in the red. The S&P Technology and Basic Materials sectors fared the worst today.

Friday: Fears of a recession grew after data from the latest US Purchasing Managers’ Index (PMI) indicated the fastest decline in business activity in over 2 ½ years, sending all four indexes tumbling for the third day in a row. The latest comments from Fed officials only heightened those fears when they commented it was possible the interest rate could go higher than expected, and that the higher rate may last until 2024.

In Canada, the TSX fell on fears of a recession as well as concerns the demand for oil could decline if there were to be a global economic slowdown. The price of oil fell more than 2%. In trading today, the Canadian Basic Materials and Consumer Staples sectors were the only Canadian sectors to gain ground, while Energy and Utilities had the biggest drop.

In the US, all the S&P sector indexes ended in the red today. The Consumer Staples and Telecommunications Services sectors fell the least of the S&P sectors, with the Utilities and Energy sectors falling the most.

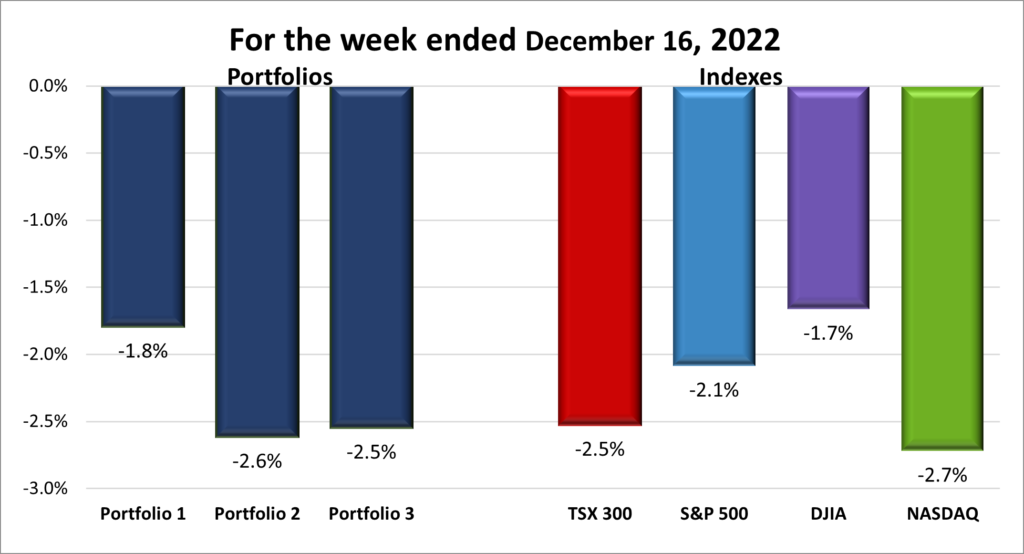

If last week was the hoped for start of a Santa rally, this week the Fed played the role of the Grinch. For the second week in a row the four indexes lost ground. For the week, the TSX dropped 2.5%, the S&P 500 fell 2.1%, the Dow sank 1.7% and the Nasdaq declined 2.7%.

Weekly Portfolio Review

![]() After a strong, optimism fueled start to the week by the bulls, the bears appeared and chased away any thoughts the bulls would carry the week. Fears of a recession in the US dominated the stock markets on both sides of the border. Once again, when the US sneezes, Canada gets a cold. The higher US interest rate dragged down the interest sensitive, high growth companies that tend to reside on the Nasdaq and S&P. The higher cost of borrowing negatively impacted the rest of the market because consumers and businesses have less money to spend thanks to higher product and service costs. A few years ago, when interest rates were near 1%, consumers and businesses were prepared to take on debt but with interest rates so high, and probably going higher, they are reluctant to take on debt. As a result, sales are lower and expected to stay down until interest rates fall. The lower revenues from sales impact all sectors and as a result even the less volatile TSX and NYSE saw their numbers fall.

After a strong, optimism fueled start to the week by the bulls, the bears appeared and chased away any thoughts the bulls would carry the week. Fears of a recession in the US dominated the stock markets on both sides of the border. Once again, when the US sneezes, Canada gets a cold. The higher US interest rate dragged down the interest sensitive, high growth companies that tend to reside on the Nasdaq and S&P. The higher cost of borrowing negatively impacted the rest of the market because consumers and businesses have less money to spend thanks to higher product and service costs. A few years ago, when interest rates were near 1%, consumers and businesses were prepared to take on debt but with interest rates so high, and probably going higher, they are reluctant to take on debt. As a result, sales are lower and expected to stay down until interest rates fall. The lower revenues from sales impact all sectors and as a result even the less volatile TSX and NYSE saw their numbers fall.

Another tough week. Sigh! Another down week for the indexes, another down week for the three portfolios. Once again, the more growth oriented a portfolio, the harder the fall in a bear market. ☹ While all three portfolios are growth oriented, Portfolio 3 has more technology companies as a percent of the portfolio, without the benefit of other sectors to cushion the fall, as is the case with Portfolio 1. Portfolio 2 had a rough week when investors punished Guardant Health (NASD:GH) for a test that performed well but not as high as the market expected, driving the share price down 25%.

Companies on the Radar

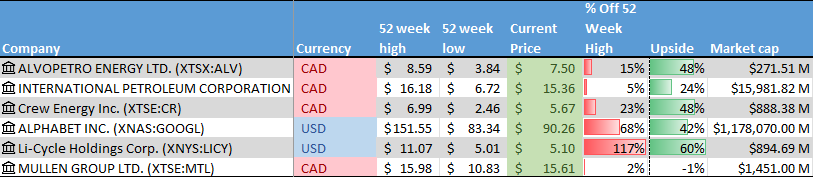

Two new companies briefly came on my Radar this week. The first is Li-Cycle Holdings Corp. (NYSE:LICY), a small cap Canadian company in the Industrials sector that recycles and recovers lithium-ion from lithium batteries. It did not do very well on the Radar Check, shown below, and I suspect it may take a while to become profitable. Plus, it has long term debt. In today’s higher interest environment, debt, negative cash flow and not generating a profit is not a good combination. For me, there are better opportunities out there.

The other company is the Mullin Group Ltd. (TSX:MTL). They are another small cap Canadian company in the Industrials sector, but this one pays a 4.5% dividend. The company provides trucking and logistics services throughout Canada and North America. I like this company better than the previous one but not better than any of the companies currently on my Radar List.

Once again, I will sit on the sidelines unless a tremendous opportunity presents itself. Otherwise, the four companies listed below, plus the two new companies mentioned above, are shown on this week’s Radar List.

- Crew Energy (TSX:CR): A Canadian oil and gas company with interests in British Columbia.

- International Petroleum (TSX:IPCO): A Canadian company with oil and gas assets in Canada, Malaysia, and France.

- Alvopetro Energy (TSXV:ALV): A Canadian natural gas company developing natural gas projects in Brazil.

- Alphabet (NASD:GOOGL): The leading online search engine and advertising company, dominant mobile operating system.

This week’s Radar Check was last updated December 16, 2022.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended December 16, 2022: DOWN ![]()

- Workers at General Motors’s (NYSE:GM) new Ultium factory in Ohio voted to join the United Auto Workers (UAW) union, becoming the first electric vehicle factory to unionize. Ultium plans to build two additional factories in the coming years so I would expect those workers to end up joining the UAW.

GM and its Ultium partner LG Energy were the beneficiary of a US$ 2.5 billion loan from the US Department of Energy. The money will go towards building three new lithium-ion battery manufacturing factories in the US.

GM is recalling over 800,000 trucks and SUVs throughout Canada and the US to fix daytime running lights that may not deactivate when the headlights are activated. The running lights are said to cause glare that could lead to collisions.

The US National Highway Traffic Safety Administration (NHTSA) has launched a safety probe into GM’s Cruise autonomous electric vehicles. The NHTSA said it has received numerous notices of Cruise cars that “engage in inappropriately hard braking or become immobilized” and become road hazards. - Good news, bad news. First the good news. During the annual reconstitution of the Nasdaq-100 Index, Rivian Automotive Inc. (NASD:RIVN) was added to the Nasdaq 100. Now the bad news. Skyworks Solutions Inc. (NASD:SWKS) was removed from the Nasdaq 100. Considering how the Nasdaq is down almost 30% for 2022, replacing Skyworks (down 45%) with Rivian (down 75%) is not going to help the Nasdaq 100.

- Rivian announced it was putting its deal with Mercedes-Benz on hold to focus on becoming cash flow positive. Rivian will concentrate on consumer vehicles and fulfilling existing deals for commercial electric vans to companies such as Amazon (NASD:AMZN).

- Apple (NASD:AAPL) and Alphabet’s Google have been forced by the European Union (EU) to allow third party app stores onto their respective smartphones and tablets. The EU’s Digital Markets Act is forcing the two dominant mobile device companies to allow other companies onto their respective platforms. I do not see a rush of consumers to these new, unproven app stores, but over time they could make a dent in Apple’s and Google’s revenue streams.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Automotive Properties Real Estate Investment Trust (TSE:APR.UN)

Yellow Pages Ltd (TSE:Y)

US $

BSR Real Estate Investment Trust (TSX:HOM.U)

Skyworks Solutions Inc (NASD:SWKS)

General Motors Co. (NYSE:GM)

Home Depot (NYSE:HD)

Quarterly Reports

Enwave Corporation

All currency listed in thousands of Canadian dollars, except per share data

Selected highlights from their year ended 2022 financial results on December 15, 2022

- Revenue of $23,703 for the year ended September 30, compared to $26,476 for the same period in 2021. A decrease of over 10%.

- Net earnings of $6,927 for the year ended September 30, compared to a net loss of $4,125 in the same period in 2021.

- Diluted loss per ordinary share of $0.06 for year ended September 30, compared to a loss of $0.04 for the same period in 2021.

Portfolio 2

Portfolio 2 for the week ended December 16, 2022: DOWN ![]()

- Microsoft (NASD:MSFT) is reaching a tentacle into the financial services industry. Microsoft made a US$ 2 billion investment for a 4% equity position in the London Stock Exchange Group (LSE) as part of a deal to move the LSE into the cloud. The LSE expects the deal to provide a significant lift to their revenues. I could not find any big win outside of the equity stake, but I expect this will provide Microsoft the opportunity to showcase its cloud and artificial intelligence services. LSE is a high profile opportunity, if Microsoft’s services and products perform as expected this will be a great win both in terms of the cash reward from their equity stack, and in proof of their products.

In other Microsoft news, in an attempt to obtain the approval of the US Federal Trade Commission for the acquisition of Activision Blizzard (NASD:ATVI), Microsoft offered a 10 year legally binding consent degree to provide their games to competitors at the same time they release the games on their Xbox platform.

Microsoft is partnering with ViaSat’s expand internet access in Africa. Through the use of ViaSat’s satellite network, Microsoft plans to provide internet access to over 5 million people throughout Africa. - Guardant Health reported their DNA blood test was able to identify 83% of colorectal cancers and 13% of advanced adenomas (a cancer precursor). This is great news for health reasons but also because the guidelines of the US Centers for Medicare and Medicaid Services indicate they will “reimburse for blood-based biomarker colorectal cancer screening tests with a minimum sensitivity of 74% if they are approved by the FDA.” If this test is reimbursable, it will likely get used more often, which means more sales for Guardant. Unfortunately, the market did not see it that way because a rival’s stool-based test produced better results.

- On Wednesday, TC Energy (TSX:TRP) reopened its Keystone pipeline at reduced capacity. The pipeline ships crude oil (diluted bitumen) from Alberta to Illinois and had been shutdown after spilling oil into a Kanas pasture last week.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Alimentation Couche-Tard Inc (TSX:ATD)

iA Financial Corporation Inc (TSX:IAG)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended December 16, 2022: DOWN ![]()

- On December 12, the company formerly known as Brookfield Asset Management officially became Brookfield Corporation (TSX:BN). Brookfield will remain focused on deploying capital across all its operating businesses (Renewable, Infrastructure and Reinsurance), grow its cash flows and compounding capital over the long term.

The spin out of its asset management unit assumed the name Brookfield Asset Management, trading under the ticker BAM on both the Toronto Stock Exchange (TSE) and the New York Stock Exchange (NYSE). BAM is a pure-play global alternative asset management business.

Not to miss out on the name changing, Brookfield Asset Management Reinsurance Partners Ltd changed their name to Brookfield Reinsurance Ltd. and their ticker symbol to BNRE on both the TSE and the NYSE. - Shopify (TSX:SHOP) committed US$ 11 million to encourage projects that remove carbon dioxide from the atmosphere and oceans. Initially Shopify will purchase over 7 million tonnes of carbon credits. However, they have not decided whether to use the credits themselves or offer them to their customers.

- Adyen (OTC:ADYEY) has been chosen by Instacart to be another of their payment processing partners. Adyen plans to further improve transactions and make the purchasing process even more seamless.

- Cloudflare (NYSE:NET) received ‘moderate’ status from the US General Services Administration’s Federal Risk and Authorization Management Program (FedRAMP). FedRAMP provides a standardized approach to security issues for cloud products and services. These are categorized into three levels — low, moderate, and high. This should open some more doors within the US government for their services.

Activity

Bought

Added a few more share of Brookfield Select Opportunities (TSX:BSO.UN). I treat BSO as a high interest bank account (11% dividend) to generate income while I wait for other opportunities, such as one of the companies on my Radar List. As long as the share price does not decline, I end up ahead. A bit of a risk but one I can accept. So, rather than leave a small amount of cash doing nothing I decided to invest the spare cash in this high interest fund managed by Brookfield Corporation, one of the top companies in Canada.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Enghouse Systems Limited

All currency listed in thousands of Canadian dollars, except per share data

Selected highlights from their fourth quarter and annual 2022 financial results on December 15, 2022

- Revenue of $108,060 for the three months ended September 30, compared to $113,099 for the same period in 2021. A decrease of over 4%.

- Net income of $36,949 for the three months ended September 30, compared to net income of $30,186 in the same period in 2021.

- Diluted earnings per ordinary share of $0.67 for the three months ended September 30, compared to $0.54 for the same period in 2021.

- Revenue of $427,585 for the year ended September 30, compared to $467,585 for the same period in 2021. A decrease of over 8%.

- Net earnings of $94,498 for the year ended September 30, compared to net earnings of $92,794 in the same period in 2021.

- Diluted earnings per ordinary share of $1.70 for the year ended September 30, compared to $1.66 for the same period in 2021.