Items that may only interest or educate me ….

Canadian economic news, US economic news, …

I realize Canada’s birthday is July 1 and this week covers the week ended June 30, but what the heck, next week will be too late. Happy 156th birthday Canada.

Canadian economic news

CPI

Statistics Canada released the latest inflation figures for May, indicating a growth of 0.4% following a rise of 0.7% in April. On an annual basis, inflation increased by 3.4% in May, marking a significant slowdown compared to April’s rate of 4.4%. In fact, the May figure represents the smallest annual inflation increase since June 2021.

The primary factor contributing to the annual decline in inflation was the drop in gas prices, which decreased by 18.3% compared to the previous year. However, even after excluding the volatile fuel component, several other sectors continued to experience considerable inflationary growth. For example, grocery prices rose by 9%, slightly lower than the 9.1% increase seen in April. Mortgage interest costs also contributed significantly to annual inflation, surging by 29.9% in May, surpassing the 29.5% increase seen in April.

GDP

In terms of Gross Domestic Product (GDP), the Canadian economy showed signs of regaining momentum after a stagnant period in April. The preliminary data suggests a monthly gain of 0.4% in May, although this estimate is subject to change when the final data is released on July 28. On an annual basis, GDP grew by 1.7% in April.

Considering the overall slowdown in inflation, it is possible that the Bank of Canada (BoC) may decide to skip a rate increase at their next meeting in July. However, the BoC will take into account the underlying Consumer Price Index (CPI) data and the growth of the economy when making their decision. While the CPI report suggests a potential pause in rate hikes, the combination of inflationary pressures and the growing economy may still lead to a 0.25% increase in the Canadian benchmark interest rate. We will have to wait for the official announcement from the BoC in a few weeks to know their if interest rates go higher.

US economic news

This week has seen a slew of economic data releases. Let us start with the US Federal Reserve’s (Fed) preferred measure, the Personal Consumption Expenditure (PCE) index. The May data shows a 0.1% monthly gain, slightly lower than the 0.4% increase in April. On an annual basis, PCE rose by 3.8%, a slight decrease from April’s 4.3%. The Core PCE, which excludes food and energy components, also increased by 0.3% in May, down from April’s 0.4%. Annually, the Core PCE for May stood at 4.6%, slightly lower than April’s 4.7%. While these figures suggest a decline in inflation, the pace of the decline may not be fast enough for the Fed.

Turning to consumer spending, the growth rate in May slowed to a 0.1% increase, compared to the 0.6% increase seen in April. This growth fell short of analysts’ expectations of a 0.2% increase for May. The higher interest rates have prompted many consumers to scale back their spending on bigger ticket purchases.

Shifting our focus to the Commerce Department, their latest GDP report reveals that the US economy grew by 2.0% in the first quarter on an annual basis, surpassing the initial estimate of 1.4%.

In addition, the Labor Department reported an unexpected drop of 26,000 in initial claims for state unemployment benefits, marking the largest decline in unemployment in 20 months. The total number of claims reached 239,000 for the week ending June 24. This unexpected decrease in jobless claims underscores the strength and resilience of the largest economy in the world, beating analysts’ expectations of around 265,000 claims.

In other economic news, the CBOE Volatility Index, which measures market volatility and investor sentiment, closed the week at 13.59, its lowest level since January 2020. Moreover, the Consumer Sentiment Index (CSI) increased to 64.4 in June, representing an 8.8% monthly increase and a 28.8% annual increase. This rise can be attributed to the resolution of the debt ceiling and falling inflation. Similarly, the Consumer Confidence Index (CCI) increased to 109.7 in June from 102.3 in May, indicating a positive sentiment among consumers.

Taking all this data into consideration, a mixed picture for inflation emerges. On one hand, the May PCE and Core PCE showed a decrease in inflation compared to the previous month, indicating a potential slowdown. However, the annual PCE and Core PCE figures still indicate inflationary pressures, albeit at a slightly lower rate.

Unfortunately, these numbers may not be declining at a fast enough pace for the Fed who are concerned about the potential for inflation to persist or even accelerate in the future. Following a pause in rate adjustments in June, the Fed has been signalling the likelihood they will return to rate hikes at their next meeting in late July. If there is another increase, it won’t be the likely 0.25% increase, but what they say about future increases.

Lots of economic data this past week as the first half of the year drew to a close. Now, let’s see how the four major North American indexes responded this past week….

Weekly Market Review

Monday: The Toronto Stock Exchange Composite Index (TSX) was the only index to end the day in positive territory. Weighing down the indexes were uncertainty over Russia after a weekend challenge to Russian leadership. From an investing perspective, the situation in Russia led to higher oil prices over concerns of disruption to Russian oil supplies. Investors are also concerned rate hikes in many of the first world countries could lead to a global economic slowdown.

In Canada, investors booked gains in technology companies and moved to energy and resource companies, as well as banks. in trading, the Energy and Consumer Staples sectors posted the biggest gains, while Technology and Healthcare were the only Canadian sectors to slide backward.

In the US, all three American indexes – the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – fell as investors are becoming concerned upcoming economic data could lead to additional rate hikes. Investors were also taking profit after the rally in technology stocks. The Energy and Telecommunications Services sectors were the big winners on the day, while growth sectors Technology and Consumer Cyclicals were the big losers.

Tuesday: All four indexes were green from the opening bell and stayed higher for the entire day. Despite the Canadian and American central banks indicating future interest rate hikes were likely, investors are feeling more confident in the economies of both countries. The market has also been busier with institutional investors rebalancing their portfolios as the second quarter and first half of 2023 winds down. Oil prices retreated on concerns of higher interest rates.

In Canada, the TSX rose on news inflation cooled off significantly in May. Investors are hoping the drop in the inflation rate will prompt the Bank of Canada to not raise the interest rate at their next meeting. In trading, Consumer Cyclicals and Technology led the Canadian sectors while Consumer Staples, Basic Materials (miners and fertilizer manufacturers), and Energy were the only sectors to lose ground.

In the US, positive economic data soothed investors concerns of a recession, giving investors a reason to re-enter the markets. In trading, Consumer Cyclicals and Technology posted the biggest gains in the American sectors, while Healthcare and Energy were the only sectors to fallback.

Wednesday: All four indexes got off to a shaky start, headed higher before ending the day with mixed results. The odd couple of the resource heavy TSX and technology laden Nasdaq both ended the day in the green, while the S&P and DJIA spent most of the day in the red before a late uptick mitigated their losses. Weighing on the markets were comments from the Fed Chair that he would not take two consecutive hikes ‘off the table’ and he did not see inflation falling to the Fed’s 2% target in 2023. A larger than expected drop in US oil stockpiles led to a rise in oil prices.

In Canada, yesterday’s CPI report showed the rate of inflation declining, leading to increased investor confidence that interest rates will stop rising soon. In trading on Bay Street, the Technology and Energy sectors posted the biggest gains, while the Utilities, Industrials and Basic Materials sectors were the only Canadian sectors to end lower.

In the US, semiconductor companies lost ground after reports the US government plans to increase restrictions on chip sales to China. However, those concerns did not carry over to other subsectors of the Technology sector as a few of the big mega cap technology companies all advanced. In trading on Wall Street, Energy and Consumer Cyclicals had the largest advances, while Utilities and Basic Materials posted the largest drops.

Thursday: It has been a while since this has happened but the only index to not to end higher was the Nasdaq, and even then, it was essentially flat. Strong economic data out of the US drove the markets today.

In Canada, the positive economic news out of the US and an uptick in the energy sector boosted the TSX higher. Today’s rally covered almost all the Canadian sectors, led by Consumer Cyclicals and Energy. Technology was the only sector to end lower.

In the US, the big US banks passed the Fed’s annual stress test (enough capital to ride out a severe economic slump), pushed the DJIA higher. On the economic front, the final GDP number for the first quarter came in higher than expected, and there was an unexpected drop in the number of people filing unemployment claims. Both suggest the US economy remains strong, but on the downside, it likely means the Fed will raise the interest rate at their next session. In trading, Financials and Basic Materials led the way higher, while Consumer Staples was the only sector to lose ground and the Technology sector was flat.

Friday: The combination of lower inflation and strong economies in both Canada and the US powered all four indexes sharply higher today. It was a positive way to close the second quarter and the first half of 2023. Hopefully a promising sign for the rest of the year.

In Canada, the TSX closed at its highest point since January and its best weekly performance since February 2021. Today’s gains were a result of the latest CPI data showing inflation slowing. Every Canadian sector ended higher, led by Consumer Cyclicals and Basic Materials. The Telecommunications Services and Energy sectors posted gains but trailed the other sectors.

In the USA, an upward adjustment of first quarter US GDP, indicating the US economy remains strong, and falling inflation from the CPI report earlier this week drove the markets higher. In trading, the oddball combination of the high growth Technology and the defensive Utilities sectors led all American sectors. Bringing up the rear were Telecommunications Services and Financials

Weekly Market and Portfolio Review

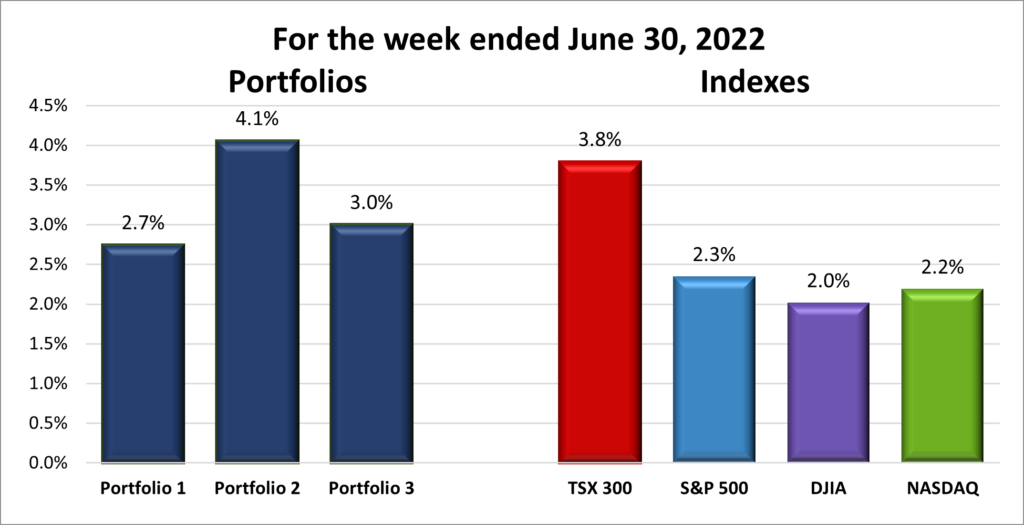

For the week, the TSX (SPTSX) jumped 3.8%, the S&P 500 (SPX) surged 2.3%, the DJIA (INDU) advanced 2.0% and the Nasdaq (CCMP) gained 2.2%.

![]() Looking at the chart above, after a minor pothole on Tuesday, it was nothing but clear open roads for all four indexes. Last week, all four indexes trended upward, with the TSX leading the way and posting the largest weekly gain. This unexpected surge in the TSX was primarily driven by the easing of inflationary pressures in Canada, which led investors to believe that the BoC may soon halt its series of interest rate hikes. Additionally, a rebound in energy prices also contributed to the TSX’s strong performance.

Looking at the chart above, after a minor pothole on Tuesday, it was nothing but clear open roads for all four indexes. Last week, all four indexes trended upward, with the TSX leading the way and posting the largest weekly gain. This unexpected surge in the TSX was primarily driven by the easing of inflationary pressures in Canada, which led investors to believe that the BoC may soon halt its series of interest rate hikes. Additionally, a rebound in energy prices also contributed to the TSX’s strong performance.

In the US, the three American indexes saw gains as well, propelled by improved economic data showing a robust economy and a slowdown in inflationary pressures. Furthermore, the successful passage of the Fed’s financial stress test by major American banks added to the positive sentiment in the market.

Overall, it was a good week for North America’s stock markets, with increasing investor optimism in the economy and the markets.

![]() Of course, a strong week for the indexes generally means a good week for the Portfolios. Once again, that occurred as all three gained at least 2.7%, as shown below. The rise in bank and financial companies following the Fed’s stress test, the ongoing rally in technology companies and improving oil prices all helped propel the portfolios higher. To paraphrase Marvin the Martian, more weeks like this would be very good, very good indeed! 😊

Of course, a strong week for the indexes generally means a good week for the Portfolios. Once again, that occurred as all three gained at least 2.7%, as shown below. The rise in bank and financial companies following the Fed’s stress test, the ongoing rally in technology companies and improving oil prices all helped propel the portfolios higher. To paraphrase Marvin the Martian, more weeks like this would be very good, very good indeed! 😊

Monthly Market and Portfolio Review

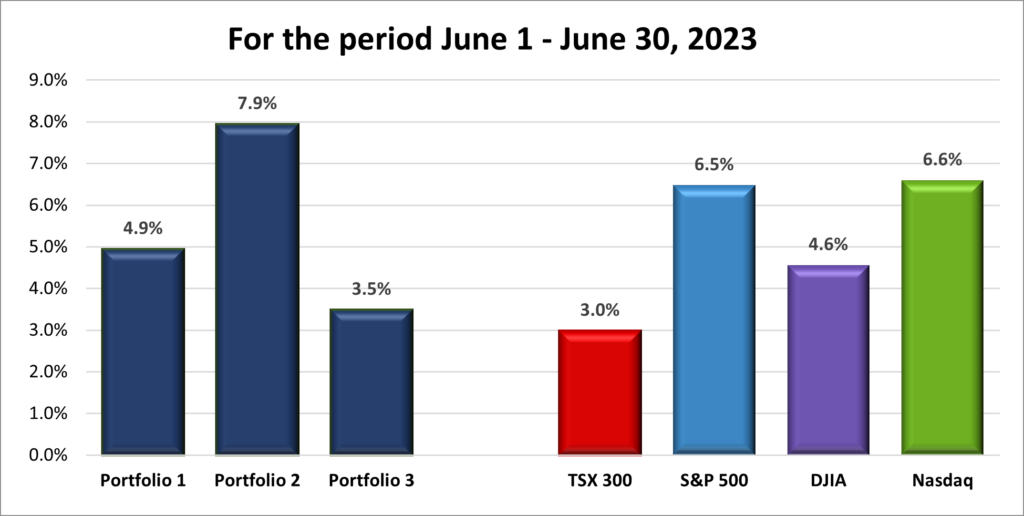

For the month of June, the TSX (SPTSX) rose 3.0%, the S&P 500 (SPX) rallied 6.5%, the DJIA (INDU) grew 4.6% and the Nasdaq (CCMP) surged 6.6%.

![]() After a lackluster performance in May, the indexes experienced a significant rebound in June. The rally began with the successful negotiations surrounding the US debt ceiling at the beginning of the month. The hype surrounding artificial intelligence (AI) and the increasing interest in mega-cap technology companies further fueled the market’s upward momentum.

After a lackluster performance in May, the indexes experienced a significant rebound in June. The rally began with the successful negotiations surrounding the US debt ceiling at the beginning of the month. The hype surrounding artificial intelligence (AI) and the increasing interest in mega-cap technology companies further fueled the market’s upward momentum.

Another positive development came from the Fed’s decision to pause the hikes in US interest rates, which provided an additional boost to the markets. Following a brief pause, the indexes resumed their rally and ended the month on a high note. The TSX, in particular, experienced a strong surge towards the end of the month, enabling all four indexes to end the month on a positive note.

This upward momentum bodes well for the North American stock markets as they enter a typically favorable month. The positive market sentiment suggest that the momentum may carry forward, setting a positive tone going forward.

![]() The portfolios had another impressive month, benefiting from the strong performance of the indexes. Portfolio 2 emerged as the top performer in June, surpassing its previous month’s gain with the help of a rebound in bank stocks and its technology holdings. Despite not matching May’s performance, Portfolio 1 still delivered a solid return of 4.9%, primarily driven by its mega-cap companies: Alphabet (NASD: GOOGL), Amazon (NASD: AMZN), Nvidia (NASD: NVDA), Tesla’s (NASD: TSLA) and Apple (NASD: AAPL), the first company valued at more than US$ 3 trillion. Portfolio 3 also had a positive month, although it didn’t outperform its previous month. Nonetheless, a gain of 3.5% is still commendable.

The portfolios had another impressive month, benefiting from the strong performance of the indexes. Portfolio 2 emerged as the top performer in June, surpassing its previous month’s gain with the help of a rebound in bank stocks and its technology holdings. Despite not matching May’s performance, Portfolio 1 still delivered a solid return of 4.9%, primarily driven by its mega-cap companies: Alphabet (NASD: GOOGL), Amazon (NASD: AMZN), Nvidia (NASD: NVDA), Tesla’s (NASD: TSLA) and Apple (NASD: AAPL), the first company valued at more than US$ 3 trillion. Portfolio 3 also had a positive month, although it didn’t outperform its previous month. Nonetheless, a gain of 3.5% is still commendable.

With all three portfolios ending the month in the green, that makes two consecutive months of gains for the portfolios. With the positive momentum, I am hoping they can all stretch their respective winning streaks to three, and hopefully much higher.😊

Companies on the Radar

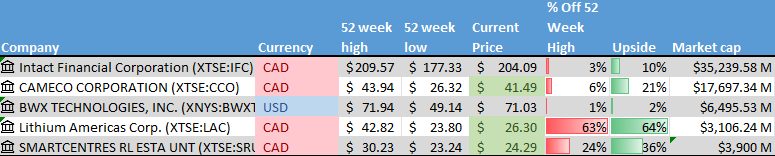

Another week where no new companies came onto my radar. My Radar List remains the same as in previous weeks:

Another week where no new companies came onto my radar. My Radar List remains the same as in previous weeks:

- Intact Financial (TSX: IFC): A Canadian mid-size insurance company that offers home, car, and business insurance in Canada, the US, and the UK.

- Cameco (TSX: CCO): A large Canadian company involved in uranium mining, sales, and the construction of nuclear reactor components.

- BWX Technologies (NYSE: BWXT): A mid cap size American company specializing in the construction and sale of nuclear components to customers worldwide, including the US Navy.

- Lithium Americas (TSX: LAC): A mid size Canadian company operating lithium mines in the USA and Argentina. They are a provider of lithium to the emerging electric vehicle battery industry.

- Smartcentres Real Estate Investment Trust (TSX: SRU.UN): A mid size fully integrated REIT that owns and manages a number of income producing shopping centres and retails spaces throughout Canada. They are planning to develop these properties for mixed retail, office, residential and storage.

The Radar Check was last updated June 30, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended June 30, 2023: UP ![]()

- Amazon’s Amazon Web Services (AWS) plans to invest US$ 7.8 billion to expand its data centre capabilities and meet the demand for growing cloud services.

In an unrelated matter, Amazon is about to be investigated by the US Federal Trade Commission (FTC), again. The investigation will examine their online marketplace to determine whether Amazon abused its power to reward the merchants that used Amazon’s logistics services and punish the ones that did not. - Tesla’s electric vehicle (EV) charging technology is being fast tracked to become the charging standard for the USA. Volvo and Volkswagen have become the latest auto makers to adopt the Tesla’s charging design.

- As if Nvidia was not already the chip of choice for artificial intelligence (AI), Nvidia’s H100 chip recently came out as top dog for training chatbots like ChatGPT.

In an unrelated matter, the US Commerce Department is considering new restrictions on exports of AI chips to China. This would prohibit Nvidia’s A800 chip, specifically made for export to China. - Alphabet’s plans to cut off access to news stories from Canadian based companies after failing to reach an agreement with the Canadian government. The impasse comes over the new Bill C-18, the Online News Act, which requires technology giants like Google to pay Canadian news organizations for linking to their online content.

- Apple once again broke the US$ 3 trillion market capitalization mark. On Friday, it made history when it became the first company to remain above that mark when the markets closed. Apple is up 49% so far this year. 😊

Activity

Received monthly interest payment on TD 1-year cashable GIC. It was good to finally see some form of interest on the cash component of the portfolio.

Bought: Alphabet. The parent company of Google experienced a decline in its share price following the initial public display of its AI chatbot Bard back in March. The demonstration did not go smoothly, as Bard provided an incorrect response. As someone who has been using OpenAI’s ChatGPT for a few months, I have noticed that even advanced AI models like ChatGPT can make mistakes. Unfortunately, Bard is currently unavailable in Canada, so I have not had the opportunity to try it myself.

However, I believe that Google and Bard have the potential to bounce back from that setback and regain ground against Microsoft’s (NASD: MSFT) implementation of ChatGPT. I have high expectations for Google, and I anticipate that it will emerge as one of the leading AI companies in the coming years. I believe this is a good time to add more shares while it is currently being overshadowed by Microsoft.

Sold: Upwork (NASD: UPWK). With strong economies and low unemployment in Canada and the US, the demand for outsourced works is slipping. Share price has been in decline since late 2021 and I do not see it returning to those 2021 prices (US$ 50+) any time soon. I should have sold these shares a long time ago. ☹

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Canadian National Railway Co (TSX: CNR)

US $

NVIDIA Corp (NASD: NVDA)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended June 30, 2023: UP ![]()

- Telus (TSX: T) has partnered with Check Point Software Technologies (NASD: CHKP) to create a Cloud Security Posture Management service for Telus client. The new service will allow Canadian clients to monitor their cloud security status in real-time.

- Microsoft announced it will proceed with its appeal of Britain’s Competition and Markets Authority veto of Microsoft’s acquisition of Activision Blizzard (NASD: ATVI).

On a related note, Canada’s Department of Justice has ruled the acquisition “is likely to” lead to less competition in some aspects of gaming. I have no idea if this means they accept or reject the proposed deal.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX: DIR.UN) DRIP

Brookfield Infrastructure Partners LP (TSX: BIP.UN)

Brookfield Renewable Partners LP (TSX: BEP.UN)

Hammond Power Supply (TSX: HPS.A)

US $

No US$ dividends this past week.

Quarterly Reports

Alimentation Couche-Tard Inc

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their fourth quarter 2023 financial results on June 27, 2023

- Revenue of $16,264.4 for the thirteen weeks ended April 30, compared to $16,434.9 for the 12-week period ended April 24, 2022. A decrease of 1%.

- Net income of $670.7 for the thirteen weeks ended April 30, compared to net income of $477.7 for the 12-week period ended April 24, 2022.

- Diluted earnings per ordinary share of $0.68 for the thirteen weeks ended April 30, compared to earnings of $0.46 per share for the 12-week period ended April 24, 2022.

- Revenue of $71,856.7 for the 53-week period ended April 30, compared to $62,809.9 for the 52-week period ended April 24, 2022. An increase of over 14%.

- Net earnings of $3,090.9 for the 53-week period ended April 30, compared to net earnings of $2,683.3 for the 52-week period ended April 24, 2022.

- Diluted earnings per ordinary share of $3.07 for the 53-week period ended April 30, compared to earnings of $2.53 per share for the 52-week period ended April 24, 2022.

Mitek Systems, Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their fourth quarter 2022 financial results on June 29, 2023

- Revenue of $19,815 for the three months ended September 30, compared to $17,781 for the same period in 2022. An increase of over 11%.

- Net loss of $311 for the three months ended September 30, compared to net income of $1,807 for the same period in 2022.

- Diluted loss per ordinary share of $0.01 for the three months ended September 30, compared to earnings of $0.04 per share for the same period in 2022.

- Revenue of $72,925 for the 12-month period ended April 30, compared to $30,069 for the same period in 2022. An increase of over 14%.

- Net earnings of $3,032 for the 12-month period ended April 30, compared to net earnings of $7,948 for the same period in 2022.

- Diluted earnings per ordinary share of $0.07 for the 12-month period ended April 30, compared to earnings of $0.18 per share for the same period in 2022.

Portfolio 3

Portfolio 3 for the week ended June 30, 2023: UP ![]()

- Shopify (TSX: SHOP) has been requested by the Canada Revenue Agency to turn over six years of records for Canadian stores that use Shopify’s software. The government agency wants the records to ensure Canadian merchants were paying their appropriate taxes. Shopify has said they will fight the request.

- Brookfield Reinsurance (TSX: BNRE) has put in an offer to by the shares of American Equity Investment Life Holding (NASD: AEL) that it does not already own. They valued the merger at US$ 4.3 billion. AEL said it will review the offer before deciding.

- Brookfield Reinsurance’s parent company, Brookfield Corporation (TSX: BN) is the front runner in acquisitions so far this year. All totaled, they have made more than US$ 50 billion in of purchases.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Brookfield Reinsurance Ltd (TSX: BNRE)

Brookfield Renewable Partners LP (TSX: BEP.UN)

Brookfield Renewable Corp (TSX: BEPC)

Brookfield Asset Management (TSX: BAM)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.