Items that may only interest or educate me ….

Strong June for the markets, Canadian Economic news, US Economic news, Driving the markets, Global energy demand increases, …

Despite facing some concerns about a potential recession in the middle of the month, June ultimately turned out to be a positive month for the markets. Looking ahead, recent historical data suggests that July has been a favorable month for the North American stock markets. The S&P 500 Index (S&P) has posted a gain in the last eight consecutive Julys, the growth-oriented Nasdaq Composite Index (Nasdaq) rose in July in each of the last ten years, while the Dow Jones Industrial Average (DJIA), and the Toronto Stock Exchange Composite Index (TSX) each have strung together three straight winning Julys.

Before rushing into the market in anticipation of another positive July, it is important to remember that investing comes with no guarantees. The past week serves as a reminder of this fact. Let us hope this past week is simply investors taking a breather, rather than an omen for the rest of the month, before resuming the upward trend into July. I am hoping each index adds another positive July to their respective winning streak. 😊

Canadian Economic news

Statistics Canada’s recent international trade report reveals a potential slowdown in Canada’s economic growth, with the country recording a significant global trade deficit of C$3.44 billion in May, the largest since October 2020. This comes as a surprise, as Canada was expected to have a trade surplus of C$1.15 billion for the same month.

Imports saw a 3% increase from April to May, with sizable gains in sectors such as: metal ores and non-metallic minerals, and metal; and non-metallic mineral products. However, declines were observed in sectors including: farm, fishing and intermediate food products; basic and industrial chemical, plastic and rubber products; and industrial machinery, equipment, and parts. On an annual basis, imports increased by 1.5%, primarily due to growth in aircraft and other transportation equipment and parts, as well as motor vehicles and parts.

On the exports side, a majority of sectors experienced declines, leading to a total monthly decline of 3.8%. Farm, fishing and intermediate food products; as well as energy products, suffered the largest losses. Lower energy prices were a significant factor in the decline of energy products exports. However, there were gains in motor vehicles and parts, as well as industrial machinery, equipment and parts. On an annual basis, exports were down 9.8%, primarily driven by declines in energy products, and forestry products and building and packaging materials.

Despite these economic indicators pointing towards a potential slowdown, the labor market continued to expand. The Statistics Canada labour survey for June revealed that the economy added 59,000 jobs, blowing past expectations of 20,000 new jobs. This represented a 0.3% growth from May to June and a 2.2% increase on an annual basis. At the same time, the unemployment rate also saw a slight increase of 0.2% to 5.4%, marking the highest level since February 2022. The rise in unemployment can be attributed to an increase in the population, resulting in more individuals actively seeking employment. This combination of job growth and a higher unemployment rate presents a mixed picture for the Bank of Canada (BoC).

Despite the unexpected trade deficit and signs of a slowing economy, the surge in job creation indicates a strong labour market. This data all but guarantees another increase to the benchmark interest rate by the Bank of Canada (BoC). While the higher unemployment rate and slowing wage growth will be considered, they are unlikely to dissuade the BoC from implementing another 0.25% rate hike at their upcoming meeting.

US Economic news

After a streak of ten consecutive interest rate increases, the Federal Reserve’s rate setting committee, the Federal Open Market Committee (FOMC), decided to pause the rate increases at their June 13-14 meetings. The recently released minutes from these sessions shed light on their decision-making process. According to the minutes, “almost all participants” agreed to maintain the rate at 5.25%, which stands as the highest level since September 2007. This decision was made to allow the committee to assess the impact of previous rate hikes on the economy.

Looking ahead, the Federal Reserve (Fed) anticipates a mild recession towards the end of the year as part of their ongoing efforts to achieve their target inflation rate of 2%. The majority of FOMC members expected at least one more 0.25% rate increase would be necessary before the end of the year and have signalled they are likely to increase the rate at their July 25-26 meeting, subject to incoming data.

The decision to maintain higher interest rates for a longer duration is driven by the fact that various measures of inflation remain elevated. Last week, the Fed’s favourite measure of inflation, Personal Consumption Expenditures (PCE), fell to 3.8% in June. However, core PCE, which excludes volatile energy and food prices, remained at 4.6%. The Consumer Price Index (CPI) is a similar story. Overall CPI has dropped sharply, but the core CPI, excluding food and energy, remains elevated at 5%.

This week saw several employment reports. The latest Job Openings and Labor Turnover Survey (JOLTS) showed a surge in private hiring as job openings declined from 10.3 million in April to 9.8 million in May. The ADP employment report showed private sector jobs increased by 497,000 in June, easily surpassing May’s 267,000 and beating analysts’ 220,000 forecast. The Department of Labor’s June nonfarm payroll data indicated a cooling employment trend with the addition of 209,000 jobs, down from May’s 339,000 new jobs. The unemployment rate decreased to 3.6% in June from 3.7% in May. Average hourly earnings rose by 0.4% in June, compared to 0.3% in May, with a 12-month increase of 4.4%. The data suggests that the labor market remains strong but may be showing signs of softening.

A strong job market typically drives wage gains and consumer spending, contributing to higher inflation levels. Given the core PCE and core PCI show no clear indications of inflation falling towards the Fed’s 2% target, and the job market remains robust, it would appear another rate hike is more than likely at the next FOMC session n July 25-26.

Driving the markets

So far, 2023 looks to be a great year for the North American stock markets, at least the American ones. The American indexes are on quite a roll this year. As of July 7, the S&P 500 is up 14.65% year to date; the Nasdaq has surged over 30%; and the DJIA is up 1.7%. Meanwhile, thanks to a rally the last week of June, the TSX snuck into positive territory with a year-to-date gain of 2.36%. A year ago, I would have been happy with any index in the green. 😊

The upward trend in the North American stock markets since the start of the year has been impressive, with only a minor setback caused by the collapse of a few U.S. regional banks in late March. At first glance, this steady rise is positive news. However, upon closer examination, it becomes evident that the dramatic surge in both the Nasdaq and S&P indexes has been primarily driven by the performance of a handful of technology companies, particularly the mega cap companies such as Alphabet (NASD: GOOGL), Amazon (NASD: AMZN), Apple (NASD: AAPL) and Microsoft (NASD: MSFT) and Nvidia (NASD: NVDA). These are not the only big technology companies responsible for the gains, but these are the ones in my portfolios. 😊

Interestingly, these same companies played a significant role in dragging down the market last year. However, this year they have spearheaded the rally and played a crucial part in the current bull market. As of July 7, Amazon, Apple, Microsoft, and Alphabet have shown impressive year-to-date gains of 54.5%, 42.2%, 41.3% and 35.4%, respectively. While these returns would typically be considered great, they are overshadowed by Nvidia’s exceptional year-to-date gain of 190.9%, as depicted in the chart below.

The dominance of mega-cap technology companies in driving the markets, particularly in the US, is undeniable. Their strong performance has contributed significantly to the overall market gains. However, if sentiment towards the big technology companies’ changes, there could be a repeat of the 2022 market downturn. When market gains are concentrated in a few specific companies or sectors, it increases the vulnerability of the markets to any negative developments or shifts in sentiment towards those companies.

Since all five of these companies are in at least one of the three Portfolios, I am very happy with these gains 😊, but it would be better for the overall market, and the Portfolios, if the gains broaden beyond these handful of companies.

Global energy demand increases

According to the latest report from the Energy Institute, global energy demand experienced a slowdown, growing by only 1% in 2022 compared to a growth rate of 5.5% in 2021. Despite record growth in renewable energy sources, oil and other fossil fuels still dominate the global energy supply, accounting for 82% of the total. However, due to the disruption in the supply of oil and natural gas caused by the Russian invasion of Ukraine, many countries turned to coal, the dirtiest fossil fuel, to meet their energy needs.

Here is a breakdown of the sources of global energy:

- Renewable energy sources (excluding hydropower) grew by 1% and accounted for 7.5% of the total energy supply.

- Oil consumption and production continued to increase, although consumption remained below pre-Covid-19 levels.

- Natural gas demand dropped by 3%, and its share in primary energy decreased by 1% to 24%.

- Coal consumption increased by 0.6%, driven primarily by China and India. More concerning is the 7% increase in coal production, with most of the new production occurring in southeast Asia.

- Renewable power (excluding hydropower) experienced a growth of 14%, which is lower than the 16% growth rate in 2021. Solar energy accounted for 72% of this growth.

- Hydropower increased by 1.1%.

- Nuclear power witnessed a decline of 4.4%.

For more detailed information, you can refer to the complete report by clicking here.

With the likelihood of increased interest rates on the horizon, let’s see what happened this past week to increase those odds ….

Weekly Market Review

Monday: It was a short trading day to start the second half of the year as the Canadian exchanges were closed for the Canada Day national holiday and the American exchanges closed early ahead of their Independence Day national holiday tomorrow.

In the US, the three major American indexes – S&P, DJIA, and the Nasdaq – each ended slightly higher in this shortened trading day. Trading was light as many investors took the day off to extend their weekend. In the American sectors, the Consumer Cyclicals and Financials sectors led the advance. Only Healthcare and Technology failed to gain ground on a day of thin trading.

Tuesday: The American markets were closed for the American Independence Day holiday.

In Canada, the TSX picked up where it left off last week, posting a sixth consecutive day of advances. Today it was pulled higher by rising prices for oil and gold. Oil prices gained on supply cuts by Saudia Arabia and Russia, two of the largest global exporters.

Wednesday: Weak economic data out of China, and ongoing tensions between the world’s two largest economies, dragged all four indexes lower. The release of the minutes from the Fed’s last meeting suggested the members were leaning towards additional interest hikes to drive down inflation, almost guaranteeing another hike is coming.

In Canada, lower commodity prices and concerns about higher interest rates in both countries weighed down the TSX. In trading in the Canadian sectors, Telecommunications Services was the only sector to advance, while Basic Materials (miners and fertilizer manufacturers) led the rest of the sectors lower.

In the US, minutes from the June Federal Open Market Committee (FOMC) meeting showed most of the Fed members were in favour of skipping the June interest rate hike. Investors scrutinized the minutes to gather any additional clues about the Fed’s future actions. In trading in the American sectors, the only sectors to advance were Utilities and Healthcare. Basic Materials and Financials suffered the biggest drops.

Thursday: All four indexes ended sharply lower again as strong labour data left investors concerned the Fed will resume their interest rate hikes.

In Canada, interest rate fears led to a drop in commodity prices pushing the TSX lower. All Canadian sectors were in the red today. Consumer Cyclicals and Telecommunications Services fell the least while Technology and Basic Materials had the biggest drops.

In the US, private payroll data came in higher than expected leading to a broad-based decline in the stock markets. Consumer Staples and Technology fell the least while Energy and Consumer Cyclicals had the biggest declines.

Friday: The latest jobs reports for Canada and the US led to a mixed day for the indexes, with the TSX the only one to post a gain. Oil prices surged on supply concerns as production cuts from major producers Saudi Arabia and Russia kick in. It appears a shortage of oil outweighs fears of higher interest rates slowing global economic growth.

In Canada, a surprisingly strong jobs report is good for the economy but not so great if you were hoping the BoC would pause interest rate hikes at their meeting next week. More Canadians working means more upward pressure on prices which will likely cause the BoC do increase the interest rate by 0.25%. On Bay Street, Healthcare and Basic Materials posted the biggest gains of the Canadian sectors, while Industrials and Utilities fell the most.

In the US, all three American indexes fell when the latest jobs showed a slowdown in job creation, unemployment edged lower, but hourly wages continued to rise. The mixed data increased the odds the Fed will raise the interest rate at their next meeting later this month. In trading on Wall Street, the best performers in the American sectors were Energy and Basic Materials, with Healthcare and Consumer Staples suffering the biggest drops.

Weekly Market and Portfolio Review

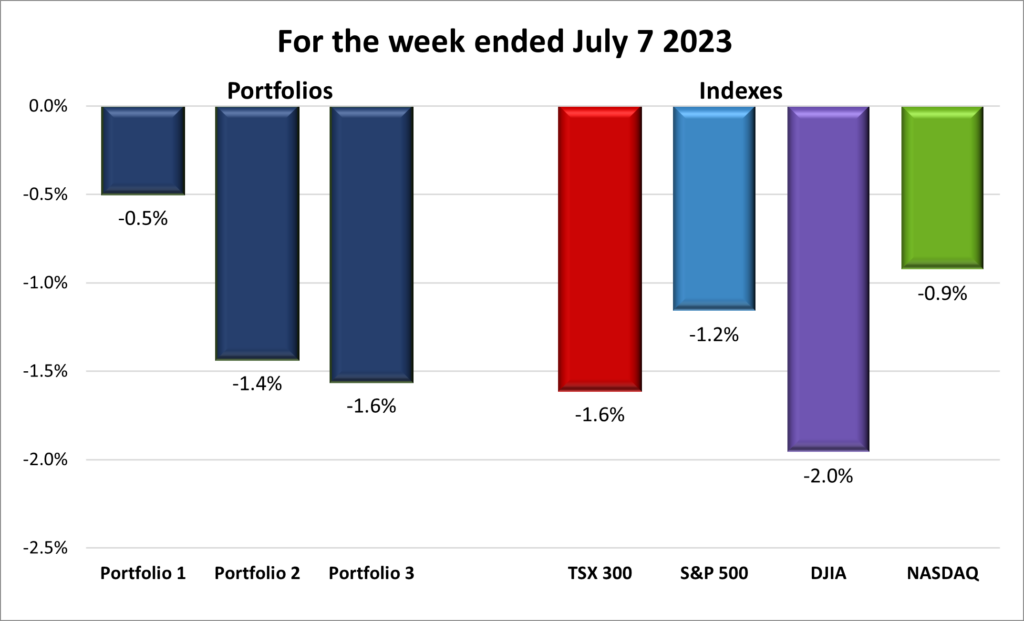

For the week, the TSX (SPTSX) fell 1.6%, the S&P 500 (SPX) lost 1.2%, the DJIA (INDU) dropped 2.0% and the Nasdaq (CCMP) declined 0.9%.

![]() It was a short week for the stock markets as Canada and America celebrated their birthdays. On the Canada Day holiday the American indexes rose and on Independence Day the TSX ended higher. Once investors returned from celebrating their respective countries birthdays, they sent the markets tumbling, leading to a weekly loss for each index, as you can see in the chart above. Belief that both the BoC and the Fed will increase their respective interest rates was the main cause of the downturn.

It was a short week for the stock markets as Canada and America celebrated their birthdays. On the Canada Day holiday the American indexes rose and on Independence Day the TSX ended higher. Once investors returned from celebrating their respective countries birthdays, they sent the markets tumbling, leading to a weekly loss for each index, as you can see in the chart above. Belief that both the BoC and the Fed will increase their respective interest rates was the main cause of the downturn.

![]() As the indexes go, typically the portfolios follow, and that was once again the case. As shown below, Portfolio 1 was the best of a bad lot as losses were limited by gains in its big technology companies. Portfolio 2 fell primarily on a 5% drop in MongoDB (NASD: MDB), otherwise many of the other companies were essentially flat. Finally, Portfolio 3 was dragged down by a general decline in the portfolio’s technology companies.

As the indexes go, typically the portfolios follow, and that was once again the case. As shown below, Portfolio 1 was the best of a bad lot as losses were limited by gains in its big technology companies. Portfolio 2 fell primarily on a 5% drop in MongoDB (NASD: MDB), otherwise many of the other companies were essentially flat. Finally, Portfolio 3 was dragged down by a general decline in the portfolio’s technology companies.

I hope this week was just a pothole and next week the markets return to their winning ways of June.

Smartcentres Real Estate Investment Trust (TSX: SRU.UN) leaves the Radar List to land in Portfolio 3. I’ve decided to pass on Intact Financial (TSX: IFC) since there are a number of financial companies across the three portfolios and the upside is relatively limited. If I were starting out in investing, I would definitely consider IFC as one of my first investments because of its steady growth and decent dividend (4%).

Smartcentres Real Estate Investment Trust (TSX: SRU.UN) leaves the Radar List to land in Portfolio 3. I’ve decided to pass on Intact Financial (TSX: IFC) since there are a number of financial companies across the three portfolios and the upside is relatively limited. If I were starting out in investing, I would definitely consider IFC as one of my first investments because of its steady growth and decent dividend (4%).

I am still working my way through deeper dives on the remaining three companies before deciding whether they can land in a portfolio or leave the list.

- Cameco (TSX: CCO): A large Canadian company involved in uranium mining, sales, and the construction of nuclear reactor components.

- BWX Technologies (NYSE: BWXT): A mid cap size American company specializing in the construction and sale of nuclear components to customers worldwide, including the US Navy.

- Lithium Americas (TSX: LAC): A mid size Canadian company operating lithium mines in the USA and Argentina. They are a provider of lithium to the emerging electric vehicle battery industry.

The Radar Check was last updated July 7, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended July 7, 2023: DOWN ![]()

- Tesla (NASD: TSLA) reported a record number of vehicles deliveries in the second quarter. Looks like those price cuts really worked. To further boost sales, Tesla started a referral program to provide extra incentive for new buyers.

- Alphabet, Amazon, Apple, and Microsoft are among a group of seven companies that meet the European Union’s ‘gatekeeper’ criteria and therefore must adhere to stricter rules. ‘Gatekeepers’ are defined as those companies that operate a core platform service that has more than 45 million active users and a market capitalization of more than US$ 82 billion. The ‘gatekeeper’ label requires companies to make their messaging apps interoperable with rivals, as well as letting users decide which apps to pre-install on their devices.

- Google announced they will start using their own custom phone chips for their Pixel line of smartphones in 2025. Google currently uses chips jointly designed with Samsung for its Pixel phones.

- Rivian (NASD: RIVN) must face a lawsuit alleging they defrauded shareholders by knowingly underpricing their vehicles prior to the company going public. The shareholders must prove Rivian knew they would have to raise prices because of higher materials costs which led to even higher losses.

Separately, Rivian reported better than expected second quarter deliveries of their electric vehicles. Finally, some good news for the company, which led to a good bump in their share price. 😊 - Amazon’s acquisition of iRobot (NASD: IRBT) will get a full scale review by the European Union’s antitrust regulator, the European Commission (EC). The EC alleges the acquisition of iRobot’s robot vacuums would reduce competition and boost Amazon’s position as an online marketplace vendor.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Cargojet Inc (TSX: CJT)

Telus Corp (TSX: T)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended July 7, 2023: DOWN ![]()

- The European Union’s anti trust regulator the European Committee (EC) is considering launching a formal investigation into Microsoft. The EC is looking into a complaint that Microsoft has unfairly integrated its Teams collaboration and video conferencing platform into their Office suite. Microsoft has offered to cut the price of a non-Teams version of Office, but the EC wants a bigger discount than Microsoft has proposed.

- Guardant health (NASD: GH) announced it will begin receiving national reimbursement approval from the Japanese government for its Guardant360 CDx liquid biopsy test, effective July 24. The test enables comprehensive genomic profiling for patients with advanced or metastatic solid tumor cancers.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Canadian Natural Resources Ltd (TSX: CNQ)

Brookfield Renewable Partners LP (TSX: BEP.UN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week, except for per share data.

Portfolio 3

Portfolio 3 for the week ended July 7, 2023: DOWN ![]()

- Alvopetro Energy Ltd. (TSXV: ALV) announced they had discovered a total of 35.4 metres of potential net oil pay, which should lead to the next stage of a development drilling program.

Activity

Bought: SmartCentres Real Estate Investment Trust (REIT). The Trust manages over 185 properties throughout Canada. They are Walmart’s only real estate development partner in the world, with Walmart stores the primary anchor tenant in many of the Trusts’ shopping centres. SmartCentres has recently started converting their shopping centres into city centres, or smart centres, that include retail, offices, residential and self-storage facilities.

SmartCentres provides diversification and stability to this technology heavy portfolio. It pays a monthly 7+% dividend but the reason I added this REIT was for the potential for earnings growth as their smart centres start to take hold.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.