Since the start of the first quarter, all four of the major North American indexes – Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – finished the quarter higher than they started, as did the three portfolios, thanks to a bull run in the Nasdaq and the S&P. Let’s look at what happened over the second quarter of 2023 ….

Second Quarter Portfolio Update

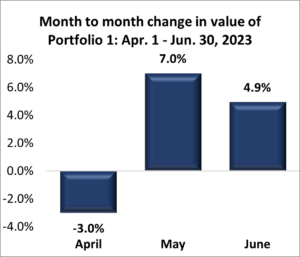

Portfolio 1 for the second quarter

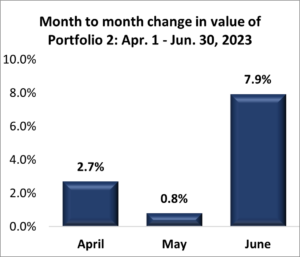

Portfolio 2 for the second quarte

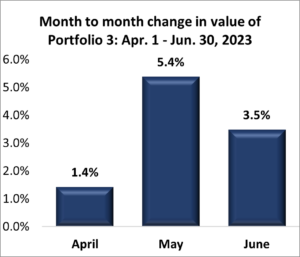

Portfolio 3 for the second quarter

Second Quarter Review

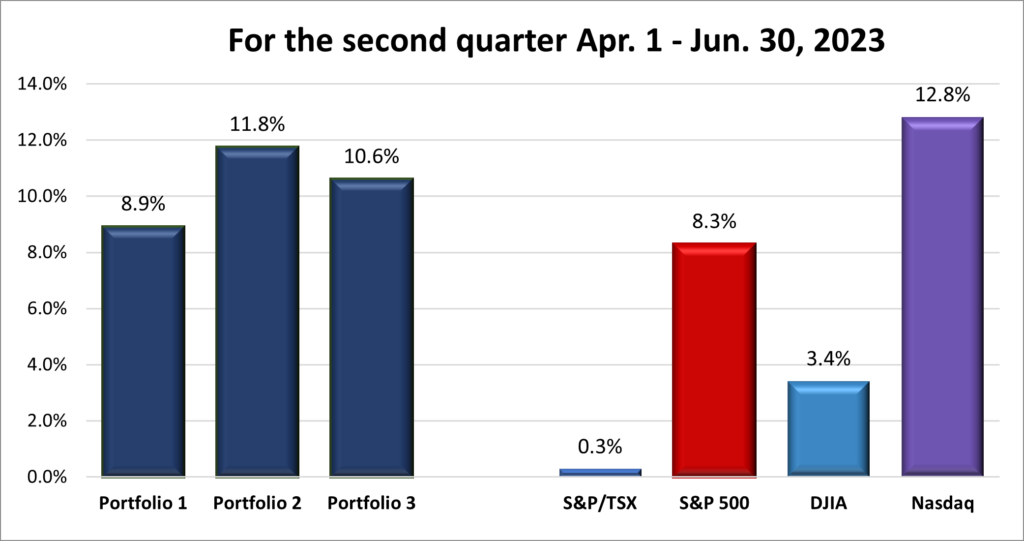

For the second quarter, the TSX (SPTSX) climbed 3.7%, the S&P (SPX) gained 7.0%, the DJIA (INDU) gained 0.4% while the Nasdaq (CCMP) surged 16.8%.

![]() The second quarter of 2023 was marked by a solid performance in the North American stock markets, with each of the four major North American indexes recording positive returns. The Nasdaq posted its best quarterly gain since the fourth quarter of 2020. As you can see in the chart above, the biggest gains came in June. The late surge even pushed the TSX into positive territory for the three months.

The second quarter of 2023 was marked by a solid performance in the North American stock markets, with each of the four major North American indexes recording positive returns. The Nasdaq posted its best quarterly gain since the fourth quarter of 2020. As you can see in the chart above, the biggest gains came in June. The late surge even pushed the TSX into positive territory for the three months.

The gains were driven by a number of factors, including stronger-than-expected corporate earnings in the first quarter, the resolution of the US debt ceiling, a pause in the Fed’s rate hike campaign and technology led by the Magnificent 7 — Alphabet (Google), Amazon, Apple, Meta (Facebook), Microsoft, Nvidia and Tesla. Without these seven companies, the overall market would have been flat, making for the most concentrated market in history. However, by the end of the quarter the rally did broaden. Technology continued to outperform as any company associated with artificial intelligence (AI) jumped, but the Communication Services, and Consumer Cyclical sectors started to rise. Other sectors like Healthcare and Financials also started to show signs of life.

On the downside, Utilities and Energy stocks suffered in the second quarter. Investors moved out of the defensive Utilities sector after sheltering there for dividends in 2022. The Energy sector fell because of fears of a recession and the uncertain situation in Russia, one of the largest global oil exporters. Oil prices posted their fourth straight quarterly loss as investors worried that sluggish global economic activity could curb fuel demand.

Overall, the second quarter of 2023 was a positive one for the North American stock markets. I would be happy if the indexes and portfolios put together a string of quarters like this one. 😊

Second Quarter Portfolio Update

Portfolio 1 for the second quarter: UP

The second quarter started off on the wrong foot for Portfolio 1 but resumed the upward march for the last two months. Portfolio 1 continued to benefit from the surge of the mega cap technology companies as five of the Magnificent Seven companies are in this portfolio.

Activity: Shaw & Magnet Forensics were acquired by other companies; sold shares of Innovative Industrial Properties, sold all Upwork; bought shares of Costco, Liberty Media (Formula 1); added shares of Amazon and Alphabet.

Portfolio 2 for the second quarter UP

Portfolio 2 posted gains in each month of the quarter. The portfolio was driven by its lone mega cap company, Microsoft, with help from its other technology companies. The bank stocks limited growth of the portfolio in May but rebounded in June leading to a stellar one month increase of 7.9%.

Activity: bought shares in Supremex, Airbnb, and Hammond Power Solutions.

Portfolio 3 for the second quarter: UP

Portfolio 3 also increased in value each month. As with the other portfolios, it benefitted from the technology bull run. Microsoft, Shopify and the other technology companies were the primary drivers of the portfolio’s growth during the quarter.

Activity: bought additional shares of Brookfield Asset Management; sold some shares of Shopify.

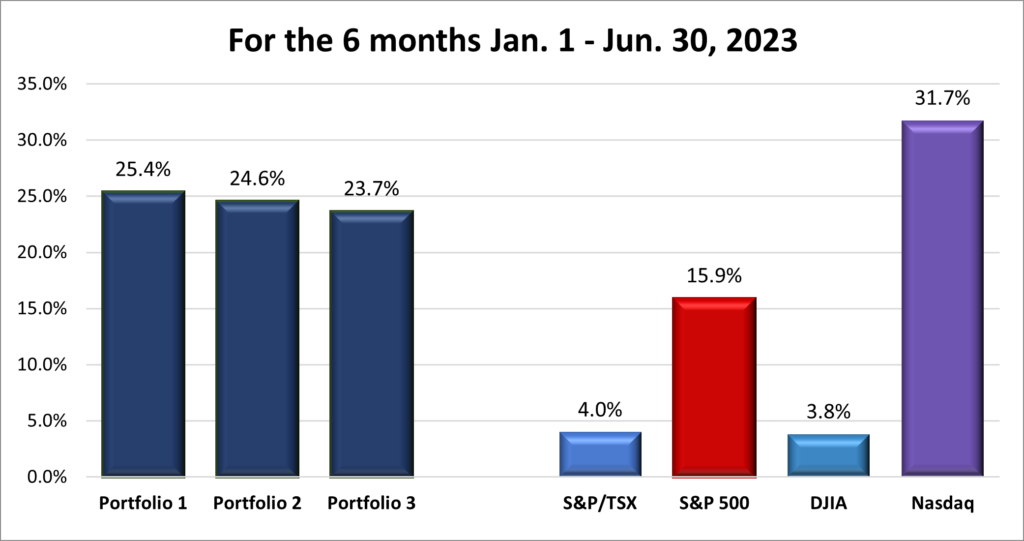

Six Month Review

For the first half of 2023, the TSX (SPTSX) climbed 4.0%, the S&P (SPX) jumped 15.9%, the DJIA (INDU) gained 3.8% while the Nasdaq (CCMP) surged 31.7%.

The year started on an optimistic note, with optimism stemming from China’s post-COVID-19 recovery, global economic resilience, and signs of inflation stabilizing. As you can see by the dips in the graph above, this optimism was shaken by the collapse of a few regional US banks raising concerns about the stability of the US financial system, the Credit Suisse failure in March raised concerns about the global banking system, central banks worldwide continued their rate hikes, and the US debt ceiling brinkmanship which was resolved in late May, early June.

Despite these challenges, the North American stock markets demonstrated remarkable strength throughout the first half of the year. With a gain of over 31% in the first half, the Nasdaq’s had its best first half performance since 1971, almost entirely erasing its losses from 2022. This rally was largely propelled by the buzz surrounding artificial intelligence (AI), in particular the Magnificent Seven’s AI efforts. Nvidia, in particular, experienced a remarkable 189.5% gain, marking its most exceptional first-half performance since going public in 1999.

The S&P 500 was no slouch either, up a respectable 15.9% for the first half. However, without the top 10 stocks, the remaining 490 would have only achieved a modest 4% gain. The DJIA was primarily powered by strong earnings from many of its 30 companies. While Canada’s resource heavy TSX was lifted by strong commodity prices and solid earnings from TSX listed companies.

Several key factors contributed to this market upward trajectory. First, were are no signs of an imminent recession. Second, investors were anticipating, correctly, that the Fed would soon pause its rate hikes. Third, the surge in artificial intelligence technologies has significantly shaped market dynamics. Finally, investors are optimistic about the future of the economy and the stock market, believing that the economy and corporate earnings will continue to grow in 2023. As investors became more optimistic about the future, they were more willing to invest in stocks.

Six Month portfolio Review

As bad as 2022 was, the first half of 2023 has been particularly good to all three Portfolios, as you can see in the chart below. All were lifted by the AI frenzy, especially their respective Magnificent Seven technology companies.

Looking forward

The impressive performance of the “Magnificent Seven” mega-cap stocks contributed to nearly 75% of the total market gains in the first half of 2023. However, for the ongoing bull market to sustain its momentum, it is crucial that the rally extends to companies beyond the technology sector. AI should remain a driving force behind earnings growth and investor sentiment.

However, the overall market gains are unlikely to match the gains seen in the first half of the year, partly due to the deceleration in economic growth in both countries. Additionally, the persistence of high interest rates through the remainder of 2023 will impact market dynamics.

Inflation continues to fall in Canada and the US as both the BoC and the Fed battle to get inflation down to their 2% target. However, getting there is likely to require at least one more rate hike. Despite the rate hikes the respective economies are slowing but remain strong, particularly the US economy. Investors are increasingly believing the Fed will be able to pull off a soft landing for the world’s largest economy, which is good news for all us investors. Investor and consumer optimism is growing and barring an unforeseen incident, it should remain high. This is good news for us investors as it means consumers will continue to spend, corporate earnings will continue to grow, and share prices should continue to rise. Of course, this prediction and a couple of bucks will buy you a cup of coffee. 😊

Thats a second bullish quarter this year, may there be two more this year!