Items that may only interest or educate me ….

Canadian Economic news, US Economic news, NASDAQ’s balancing act, ….

Canadian Economic news

As was expected, the Bank of Canada (BoC) raised the Canadian benchmark interest rate by 0.25% to 5.0%, reaching its highest level in 22 years. This marks the tenth increase by the central bank since March 2022.

In their announcement, the BoC acknowledged the downward trajectory of global inflation and the strength of the Canadian economy, which is supported by a tight labor market. While inflation fell to 3.4% in May, a significant drop from the peak of 8.1% last summer, underlying inflation, as measured by the core Consumer Price Index (CPI), which excludes food and fuel prices, remained at 4%.

The BoC expects inflation to continue easing, but they are concerned that progress towards their 2% target could stall, and inflation could potentially rise again if there are unexpected upward surprises. BoC Governor Tiff Macklem emphasized the importance of taking necessary actions now to prevent the need for more significant measures in the future. The central bank projects that inflation will hover around 3% for the next twelve months before eventually reaching the BoC’s 2% target by 2025. The rate increase serves as a reminder that achieving a 2% inflation rate remains the BoC’s primary objective.

While the BoC did not explicitly state that this would be the last rate increase, they did not rule out further rate hikes. The central bank will continue to monitor the data and assess the need for additional rate adjustments as the effects of the rate hikes work their way through the economy. Analysts are split on whether there will be another increase at their next meeting on September 6. Hopefully, this will be the last increase before the BoC starts lowering the rate.

Of course, Canada’s big banks announced they will raise their rates, accordingly, making it more expensive for anyone with a variable rate mortgage or outstanding loan. ☹

US Economic news

Consumer Price Index

Data from the Bureau of Labor Statistics indicates that the June Consumer Price Index (CPI) showed moderate increases, both on a monthly and annual basis, but both came in lower than expected. In June, the CPI increased by 0.2%, following a 0.1% gain in May. On an annual basis, the CPI grew by 3.0%, a decrease from May’s 4.0% growth rate.

The core CPI, which excludes the volatile components of energy and food prices, also experienced a 0.2% increase in June, compared to a larger gain of 0.4% in May. The annual growth rate for core CPI stood at 4.8%, a significant decline from May’s 5.3% increase and the lowest rate of growth in over two years.

Energy prices saw a substantial decrease of 16.7% on a yearly basis, while food prices increased by 5.7%. In terms of monthly drivers, shelter costs played a significant role, accounting for 70% of the overall increase in CPI.

The positive aspect of this data is that overall CPI, or headline CPI, continues to decline, indicating some easing in price pressures. Additionally, the deceleration in core CPI suggests that many of the various subsectors are experiencing slower growth rates in prices.

Producer Price Index

The June Producer Price Index (PPI) for final demand, as reported by the Labor Department, experienced a modest increase of 0.1% following a 0.4% decline in May. On an annual basis, the PPI rose by 0.1%, a decrease from May’s 0.9% increase.

The core PPI, which excludes the volatile components of food, energy, and trade services, also saw a 0.1% increase in June, compared to no change in May. Over the twelve months through June, the core PPI increased by 2.6%, slightly lower than the 2.8% growth rate recorded in May.

The PPI is a measure of the average price changes received by American producers for their goods and services. A decrease in the PPI suggests lower production costs for producers, which may lead to lower prices for consumers. The latest data indicates that the annual increase in US producer inflation was the smallest seen in nearly three years.

Jobs report and unemployment rate

The Department of Labor’s latest data revealed that the number of Americans filing new claims for unemployment benefits unexpectedly dropped to 237,000, which was below both the expected 250,000 claims and the previous week’s 249,000 claims. This decline indicates that the American labour market remains tight, as fewer individuals are seeking unemployment assistance.

A tight labour market is generally considered a positive sign for the economy, as it indicates lower levels of unemployment and a higher demand for workers. However, in the context of the Federal Reserve (Fed) and their interest rate decision, a tight labour market can also raise concerns about inflationary pressures. When there is strong demand for labour and a limited supply of available workers, it can lead to wage increases and potentially contribute to rising inflation.

Given this unexpected decline in unemployment claims and the continued tightness of the labor market, it may provide another reason for the Federal Reserve (Fed) to consider raising the interest rate again.

What does it all mean?

The drop in CPI and slowing PPI indicate a decrease in inflationary pressures, which could potentially lead the Federal Reserve to leave the interest rate unchanged. However, the lower jobless claims data suggests a tight job market and the possibility of inflation reversing course. While one month of positive data is unlikely to prevent the Fed from proceeding with an interest rate hike, continued positive results in CPI, PPI, and jobless claims data in July and August could potentially signal that the last rate increase has already taken place.

For us investors, this environment could be favorable for stocks. If second quarter corporate earnings are strong, we could find ourselves in a bull market. Second quarter earnings reports started this week so we shall know shortly.

Consumer Sentiment Index

The University of Michigan’s initial consumer sentiment index (CSI) reading for July came in 72.6, its highest since September 2021. The CSI is up 12.7% from June, and on an annual basis, it is up 41.0%. The sharp increase is largely a result of the continuing drop in inflation.

NASDAQ over concentration

The operators of the Nasdaq have announced a “special rebalance” of the Nasdaq 100 index. The rebalance aims to reduce the weight of the mega cap companies and allow smaller companies to have a greater influence on the index. This adjustment is necessary to ensure the index remains a relevant benchmark for investors.

At the beginning of the year, Amazon (NASD: AMZN), Apple (NASD: AAPL), Microsoft (NASD: MSFT), Nvidia (NASD: NVDA), and Tesla (NASD: TSLA) accounted for 43.8% of the Nasdaq 100 index’s weight. However, the rally in mega-cap technology companies this year, including a recent surge in Tesla’s share price, pushed the combined weight of these five companies over the 48% threshold that triggers a rebalancing. After the rebalance, these five companies will drop to 38.5% of the Nasdaq 100.

This special rebalancing will likely have some impact on investors as index funds and mutual funds that track the Nasdaq 100 will need to buy and sell billions of dollars’ worth of shares to align with the updated weightings. The increased buying and selling activity may lead to price volatility, presenting opportunities for investors. However, given the liquidity of the shares in the Nasdaq 100 companies, significant impacts on share prices are not expected, especially for long-term investors.

The rebalance will take place before the markets open on July 24 and does not involve the removal or addition of any companies. The Nasdaq 100 was previously rebalanced in 1998 and 2011.

Retail Investor index

I recently discovered the TD Direct Investing Index (DII). I do not and will not use it for my investment decisions, but it was interesting to see how my market sentiment compared to other TD Direct Investing customers. If you are interested in the market sentiment of other individual investors, check out TD’s Direct Investing Index.

If you made it through all that economic news, please try and stay with me and let’s see what happened this past week….

Weekly Market Review

Monday: Weak economic data out of China, upcoming inflation data out of the US, and the next BoC interest rate decision all factored into market movements today. Concerns of higher interest rates caused the price of oil to slip.

In Canada, the Toronto Stock Exchange Composite Index (TSX) ended lower as investors anticipate the BoC will raise the interest rate by 0.25% for the second time in a row. In trading, the biggest gains in the Canadian sectors were made by the Basic Materials (miners and fertilizer manufacturers) and Healthcare sectors. The biggest losses were posted by the Telecommunications Services and Utilities.

In the US, the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) each snapped three day losing streaks. The indexes rebounded from last week’s stumble after several members of the Fed suggested the end of rate hikes is getting closer. In trading, Industrials and Healthcare led the way upward while Telecommunications Services and Utilities were the only two American sectors not to post a gain.

Tuesday: In anticipation of Wednesday’s US CPI report, investors pushed all four indexes higher, betting inflation will be lower and an end to rate hikes will be in sight. China, the world’s second largest economy, announced they will implement measures to support their sagging economy. Oil prices surged thanks to a combination of tighter supplies (supply cuts by Saudia Arabia and Russia) and higher demand (analysts anticipate higher demand from developing countries).

In Canada, analysts and investors expect the BoC to raise the interest rate by 0.25% and are hoping for a sign it will be the last increase. The TSX ended higher thanks to sharply higher oil prices lifting many of the energy companies. A strike at Canada’s Pacific ports that started July 11 is starting to impact Canadian exporters and importers alike. In trading, Energy and Technology posted the biggest gains, while Consumer Staples and Industrials had the largest decline.

In the US, south of the 49th, investors are waiting to see the latest inflation numbers from the world’s largest economy. It was a day of broad-based gains in trading, led by Energy and Financials. Healthcare was the only sector to end in the red.

Wednesday: All four indexes rose as US inflation fell to its slowest pace since March 2021. Investors are hoping the Fed is near the end of their interest rate hiking campaign and will reconsider the need for additional rate hikes. Slowing inflation led to higher oil prices as analysts anticipate more demand.

In Canada, the TSX rose as news of cooling US inflation was more than enough to overcome the news of the higher interest rate. In trading on Bay Street, the Basic Materials and Utilities sectors led the gainers, while Healthcare, Consumer Cyclicals and Consumer Staples were the only sectors to end lower.

In the US, inflation continued its downward trend with a rate of 3%, the smallest annual increase since March 2021, down from May’s 4%. It was a good day on Wall Street, with all sectors in the green. Basic Materials and Utilities were the top gainers, while Healthcare and Telecommunications Services posted the smallest gains.

Thursday: The four indexes extended this week’s rally, as each ended higher. Yesterdays’ news of lower inflation in June, followed by today’s better than expected PPI suggested the Fed may finally be winning their battle with inflation. Today’s PPI news further raised investor hopes the Fed would ease up on interest rate hikes. Oil prices continued their rally after inflation data suggested inflation had peaked.

In Canada, optimism the BoC is finished with raising the interest rate propelled the TSX higher. As well, the 13-day port strike on the Pacific Coast was tentatively resolved, unclogging supply chain bottlenecks that threatened to raise inflation in Canada. Every Canadian sector advanced today, led by Technology and Utilities, with Consumer Cyclicals and Consumer Staples bringing up the rear.

South of the border, the Nasdaq improved by more than 1% for the second straight session. With inflation headed in the right direction, big institutional investors, and us individual investors 😊, prepare for the second quarter earnings session which starts this week. All the American sectors ended higher, led by Technology and Basic Materials with Telecommunications Services and Energy trailing the pack.

Friday: Despite decent earnings reports from big American banks, three of the four indexes ended lower in the red. After the strong rally throughout the week, it appears investors took some profits off the table as the second quarter earnings season got underway. Oil prices fell as investors took profits after a strong rally.

In Canada, the TSX ended just below the breakeven line. The Canadian banks rose on the news of strong earnings reports by the big US banks, but it was not enough to drag the TSX into positive territory. In trading, Consumer Staples and Industrials were the biggest gainers of the Canadian sectors. On the losing side, Telecommunications Services and Energy had the biggest losses.

In the US, the DJIA was the only index to end higher, buoyed by American banks and a strong showing from UnitedHealth Group (NYSE: UNH). In trading, Healthcare and Consumer Staples were the only American sectors to end higher, while the Energy and Telecommunications Services sectors suffered the largest declines.

Weekly Market and Portfolio Review

For the week, the TSX (SPTSX) advanced 2.2%, the S&P 500 (SPX) gained 2.4%, the DJIA (INDU) rose 2.3% and the Nasdaq (CCMP) jumped 3.3%.

![]() Better-than-expected inflation data and a robust labour market led to a four-day rally that saw all four major North American indexes end the week higher, as seen in the chart above. What really got investors excited was the data suggested inflation is actually decelerating, opening the door for the end of the central bank’s fastest interest raising cycle since the 1980s. As usual, when investor optimism is high, the technology companies are the big winners pushing the Nasdaq and S&P higher. This week’s rally was still fairly narrow but other sectors started to rise. Strong earnings reports from America’s big banks lifted the Financials sector which in turn pushed the DJIA to its best week since March. Finally, the TSX advanced on higher oil prices and overall market optimism.

Better-than-expected inflation data and a robust labour market led to a four-day rally that saw all four major North American indexes end the week higher, as seen in the chart above. What really got investors excited was the data suggested inflation is actually decelerating, opening the door for the end of the central bank’s fastest interest raising cycle since the 1980s. As usual, when investor optimism is high, the technology companies are the big winners pushing the Nasdaq and S&P higher. This week’s rally was still fairly narrow but other sectors started to rise. Strong earnings reports from America’s big banks lifted the Financials sector which in turn pushed the DJIA to its best week since March. Finally, the TSX advanced on higher oil prices and overall market optimism.

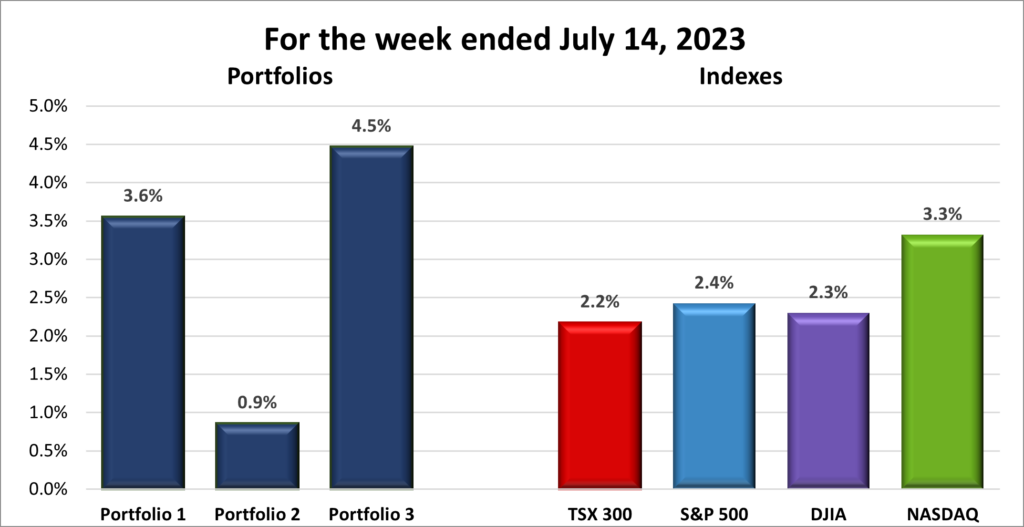

![]() After a rough start to July last week, it is good to see all three portfolios advancing and getting back on the winning track, as illustrated below. It is particularly satisfying to note that Portfolio 1 and 3 outperformed the Nasdaq. However, I was a bit surprised that Portfolio 2 significantly underperformed. Upon closer inspection of Portfolio 2, there were some mid-week stumbles by a few companies that brought their performance back to where they started the week. Aside from that, there were no significant winners or losers in the portfolio.

After a rough start to July last week, it is good to see all three portfolios advancing and getting back on the winning track, as illustrated below. It is particularly satisfying to note that Portfolio 1 and 3 outperformed the Nasdaq. However, I was a bit surprised that Portfolio 2 significantly underperformed. Upon closer inspection of Portfolio 2, there were some mid-week stumbles by a few companies that brought their performance back to where they started the week. Aside from that, there were no significant winners or losers in the portfolio.

Portfolio 1 once again benefited from the strength of mega-cap companies and the overall surge in the technology sector. Meanwhile, Portfolio 3 had an impressive week with almost every company ending higher, except for Telus International (TSX: TIXT), which experienced a 30% drop after the company estimated a loss for the second quarter. Without the stumble by Telus International it could have been a great week for Portfolio 3.

Companies on the Radar

My radar has looked relatively empty the last few weeks. Other than these three companies listed below, nothing has really jumped out at me. For now, I am looking deeper into these companies to get a better understanding of their business, competitive advantages, financial performance, and their potential for future success.

- Cameco (TSX: CCO): A large Canadian company involved in uranium mining, sales, and the construction of nuclear reactor components.

- BWX Technologies (NYSE: BWXT): A mid cap size American company specializing in the construction and sale of nuclear components to customers worldwide, including the US Navy.

- Lithium Americas (TSX: LAC): A mid size Canadian company operating lithium mines in the USA and Argentina. They are a provider of lithium to the emerging electric vehicle battery industry.

The Radar Check was last updated July 14, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended July 14, 2023: UP ![]()

- General Motors (NYSE: GM) has dropped the price of their Cadillac Lyriq electric vehicle (EV) by 14% in China. GM slashed the price to match price cuts announced by other foreign EV companies to better compete with domestic Chinese EV companies.

In separate news, the US National Highway Traffic Safety Administration (NHTSA) said they will announce in a few weeks if GM’s Cruise division of self driving cars can be deployed without human controls. Items used by human drivers such as steering wheels, mirrors, turn signals or windshield wipers are obviously not needed for self driving cars. - Berkshire Hathaway Energy, a unit of Berkshire Hathaway (NYSE: BRK.B) purchased Dominion Energy’s 50% stake in the Cove Point liquefied natural gas facility, bringing Berkshire’s stake to 75%. Brookfield Infrastructure Partners (TSX: BIP.UN) owns the remainder.

- The new MacBook Air helped Apple grow its market share of the personal computing market from 6.4% to 11%, on an annual basis.

- Nuvei (TSX: NVEI), announced they have been selected by inDrive, a mobility solutions provider available in 47 countries, as its payments provider for payouts to its drivers in Latin America.

- Amazon reported that Americans alone purchased US$ 12.7 billion during the two-day Amazon Prime event, up 6.1% over last year’s Prime Days.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX: DIR.UN)

Algonquin Power & Utilities Corp (TSX: AQN)

US $

Innovative Industrial Properties Inc (NYSE: IIPR)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended July 14, 2023: UP ![]()

- It was a double win for Microsoft this week. First, a US judge ruled that Microsoft can move forward with its planned acquisition of Activision Blizzard (NASD: ATVI). A judge ruled the regulators were unable to show how the merger “is likely to substantially lessen competition.” An hour later, Britain’s anti trust regulator, the Competition and Markets Authority (CMA), said it would consider proposals from Microsoft to address the CMA’s concerns. If you are keeping score, the biggest merger in technology history has now received a green light from the US and the European Union, and an amber light from Britain.

- The Walt Disney company (NYSE: DIS) extended the contract of their Chief Executive Officer Bob Iger by two years, expiring at the end of 2026.

Separately, Disney has decided to hold onto their ESPN business unit and are looking for strategic partners to help with content and distribution.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Telus Corp (TSX: T) DRIP

Brookfield Infrastructure Partners LP (TSX: BIP.UN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week, except for per share data.

Portfolio 3

Portfolio 3 for the week ended July 14, 2023: UP ![]()

- Shopify (TSX: SHOP) has become the latest company to integrate an AI assistant into their offerings. The AI assistant, called ‘Sidekick’, will be able to answer questions from Shopify merchants, as well as provide them with insights about their sales trends.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

TD US Equity Index ETF (TSX: TPU)

Alvopetro Energy Ltd (TSXV: ALV)

Brookfield Asset Management (TSX: BAM)

Brookfield Corp (TSX: BN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.