Items that may only interest or educate me ….

Canadian Economic news, US Economic news, Oil prices surge, Amazon goes to court, US government shutdown …

But first …. Happy 25th birthday to Google

Google was launched on September 27, 1998. Originally conceived as a search engine by founders Larry Page and Sergey Brin, it has since evolved into the dominant global search engine, handling over 9 billion searches per day, meaning that Google handles over 99,000 searches every second. Additionally, Google holds a significant presence in online advertising, leveraging its Google search page and YouTube platform. On August 19, 2004, Google went public. It has since grown into one of the world’s leading technology companies, operating under the umbrella of Alphabet Inc.

On August 10, 2015, a significant restructuring occurred, transforming Google into a subsidiary of Alphabet Inc. Under this new arrangement, Google became one of Alphabet’s subsidiaries, with each subsidiary focusing on distinct areas of business. This restructuring provided Alphabet with improved organizational clarity and flexibility. It allowed Alphabet to effectively manage its diverse portfolio of businesses, expanding beyond Google’s core internet search and advertising operations to encompass ventures such as self-driving cars and life sciences.

Canadian Economic news

Gross Domestic Product

In Statistics Canada’s July Gross Domestic Product (GDP) report, Canada’s economy showed no growth, remaining stagnant at 0%, contrary to analysts’ expectations of a 0.1% increase after a 0.2% contraction in June. The service sector saw a slight uptick at 0.1%, driven by a 2.3% surge in accommodation and food services. However, goods producers experienced a 0.3% decline, despite a 1.8% rise in the mining, quarrying, and oil and gas extraction sector.

On an annual basis, GDP grew by 1.1%, propelled by a 2.0% increase in service-producing industries. The public administration (government) sector led the way, showing a significant 3.8% expansion. In contrast, goods-producing industries saw a 1.4% decline, with construction being the best-performing sector, albeit ending flat with a 0.0% change.

Advance data for August indicates that real GDP inched up 0.1%.

GDP stands as a pivotal indicator used by the Bank of Canada (BoC). It provides a snapshot of a country’s economic well-being by reflecting its overall economic activity and growth trends.

Canadian budget update

The Canadian budget posted a C$1.2 billion deficit for the first four months of fiscal 2023/2024. The deficit was driven by a decrease in revenues and an increase in spending. Revenues were down 1.2% from the same period last year, due to a decrease in corporate income taxes and GST/HST revenues. Spending was up 2.3% from the same period last year, due to an increase in federal government program spending and debt servicing costs. Higher interest rates increased public debt charges by $3.3 billion, an increase of 29.9% from the previous year.

Canada runs a budget deficit which is financed by borrowing money. When the government borrows money, it increases the national debt, which must be paid back eventually. A large budget deficit can lead to higher interest rates and inflation.

US Economic news

Personal Consumption Expenditures

The August data for the Personal Consumption Expenditures (PCE) price index came in below expectations, showing a 0.4% increase compared to the projected 0.5%. The annual rise of 3.5% matched expectations. The core PCE, which is PCE excluding the volatile food and energy components, saw a 0.1% increase, below the anticipated 0.2%. On an annual basis, core PCE matched expectations of a 3.9% rate of growth, slightly down from July’s 4.2% pace.

These numbers indicate a slight dip in inflation, a trend welcomed by the Federal Reserve (Fed) and investors alike. The Fed closely monitors these figures, and a decrease in inflation might provide room for the Fed to refrain from raising the benchmark interest rate, which would please investors and consumers. PCE represents the total value of goods and services purchased by American consumers, while Core PCE offers a more stable measure of inflation, making it the Fed’s preferred metric for assessing economic trends.

Gross Domestic Product

The third estimate of Gross Domestic Product (GDP) for the second quarter (April through June) revealed a 2.1% annual increase, slightly lower than the first quarter’s 2.1%. This figure, despite the ongoing auto workers’ strike and the looming government shutdown, signifies the economy’s resilience and strength.

Gross Domestic Product is a crucial economic indicator used by the Fed. It represents the total monetary value of all finished goods and services produced within a country’s borders during a specific period.

For those interested in real-time updates on US GDP, check out GDPNow at the Federal Reserve Bank of Atlanta. It provides a running assessment of the US’s economic performance.

Consumer Confidence Index

The Conference Board’s Consumer Confidence Index (CCI) unexpectedly fell to 103.0 in September, a four-month low. Analysts had been expecting a reading of 105.5, down slightly from August’s 106.1. The fall was a result of higher prices, higher interest rates, a possible recession, and concerns about a government shutdown.

The CCI measures how consumers feel about the job market, the economy in general, and their financial situation. When the CCI drops, it suggests that consumers are more uncertain about the job market, the overall economic conditions, and their financial situations. A lower CCI can lead to reduced consumer spending, which could have a negative economic impact.

Consumer Sentiment Index

On Friday, the University of Michigan’s final reading on the Consumer Sentiment Index (CSI) for September came in higher than expected at 69.5, slightly above August’s 67.7.

A higher CSI typically indicates that consumers are feeling more optimistic and confident about the current and future state of the economy. It suggests that consumers are more likely to spend money on goods and services, which can have a positive impact on businesses and overall economic growth.

Oil prices surge

While the Nasdaq and S&P have fallen for most of this September, one sector that has steadily advanced is the energy sector, specifically the oil industry. Oil prices have surged nearly 30% since June to their highest levels of the year. Several factors contribute to this rise.

On the supply side, Saudi Arabia and Russia extended their production cutbacks through to the end of the year, shrinking supply. Together these two countries account for over 20% of global output. On the demand side, there is increased demand as global economic activity increases. The International Energy Agency (IEA) expects global oil demand to reach 102 million barrels per day in 2023, up from 100 million barrels per day in 2022. One reason for higher demand is China, the world’s second largest economy, is boosting its demand for oil. In addition to reduced supply and increased demand, Russia’s invasion of Ukraine has disrupted supply chains in that region. Together, these conditions have sent oil prices higher, with the possibility oil could reach US$100 per barrel this year.

Higher oil prices equate to increased profits for oil companies, and these gains are often passed on to shareholders in the form of dividends, which benefits investors. However, the surge in oil prices presents a formidable challenge for central banks worldwide, not only the BoC and the Fed. The consequences of higher oil prices can lead to an increase in inflation which could trigger the BoC and the Fed to hike their respective interest rates. Higher oil prices are also felt by consumers, who struggle with a higher cost of living, as well as businesses and governments that must raise prices to offset increased costs in delivering products and services.

Amazon goes to court

The US Federal Trade Commission (FTC) finally filed its long-awaited antitrust lawsuit against Amazon (NASD: AMZN) after a four-year investigation. In this major antitrust case, the FTC alleges that Amazon is a monopoly that abuses its market powers, such as overcharging sellers and stifling competition, which negatively impacting consumers and merchants who use the platform.

The lawsuit is one of the most significant antitrust cases in recent years, signaling a more aggressive approach by the agency. The case’s outcome has the potential to significantly affect Amazon’s business and the e-commerce industry as a whole.

The FTC accused the company of:

- Favoring their own products and services over those of competitors on its platform. For example, the FTC alleges that Amazon gives its own products better placement on search results pages, and that it uses its Prime program to give Amazon products a shipping advantage.

- Using its data to give its own products and services an unfair advantage over other merchants on the Amazon platform. The FTC alleges that Amazon uses data from third-party sellers to develop its own competing products.

- Pressuring third-party sellers to raise prices or sell exclusively on Amazon. For instance, the FTC alleges that Amazon threatens to demote sellers’ products in search results or to charge them higher fees if they sell on other platforms.

The FTC has requested the court to issue a permanent injunction against Amazon, ordering the company to halt its illegal conduct. At this stage, the FTC’s focus is on proving that Amazon violated the law. If Amazon is found guilty, the FTC will propose remedies, including the possibility of breaking up the company.

Apart from the FTC’s lawsuit, Amazon faces antitrust investigations by regulators worldwide, including the European Union and the United Kingdom, with similar allegations of market power abuse.

For investors, the FTC’s lawsuit presents a low-risk situation. If the FTC loses, nothing changes for Amazon, and it can continue its operations as usual. If the FTC prevails and Amazon is broken up, shareholders would end up with shares in multiple companies, including the highly valuable Amazon Web Services.

In summary, the FTC’s lawsuit against Amazon is a significant development. Whether you are a shareholder or considering investing in Amazon, it is crucial to be aware of the lawsuit and its potential consequences. While it is too early to predict the case’s resolution, it holds the potential to profoundly impact Amazon’s business and the broader e-commerce industry.

US government shutdown

As highlighted in the September 15 post, the US government finds itself in a precarious situation, once again engaging in a high-stakes standoff with far-right Republicans in the House of Representatives.

Beyond the immediate impact of putting thousands of Americans out of work or compelling them to work without pay until a resolution is reached, a government shutdown has historically been a non-event for the stock market, other than possible increased volatility.

However, this shutdown could interfere with the collection and reporting of economic data used by the Fed to make decisions in their battle against inflation. Reports such as the GDP and PCE, vital metrics for the Fed, would face delays. Moreover, other economic reports that form the foundation of various economic analyses would also be significantly impacted.

The Fed has said their upcoming decisions are data dependent. The absence of timely and accurate data due to a government shutdown would make the already challenging task of steering the economy even more difficult.

While the US government may shutdown, the markets do not. Let’s see what happened this past week….

Weekly Market Review

Monday: The indexes started the day in negative territory but slowly recouped the losses to end the day in positive territory as investors shook off a tough few days last week. The concern of higher interest rates for longer has led to rising yields on US government bonds, causing investors to move money from riskier assets such as stocks to more secure government bonds. Next up on the list of items for investors to worry about is a possible US government shutdown at the end of this week.

In Canada, the Toronto Stock Exchange Composite Index (TSX) finally ended its losing streak thanks to a rally in energy companies. In trading, Energy and Consumer Cyclicals were the top gainers in the Canadian sectors, with the Telecommunications Services and the Utilities sectors experiencing the biggest drops.

In the US, the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) all got back in the win column as investors came to grips with higher rates for longer. In the American sectors, Energy and Technology posted the biggest gains, while Telecommunications Services and Consumer Staples posted the biggest losses.

Tuesday: All four indexes ended down sharply when a Fed official suggested the resilient US economy will likely result in another interest hike. Concerns of higher for longer interest rates again weighed heavily on the markets. From an investor perspective, higher oil prices were the only positive on a dismal day.

In Canada, the TSX fell to a three-month low as investors worried about a recession caused by the higher rates. The Consumer Staples sector was the only Canadian sector to end in positive territory, while Basic Materials (miners and fertilizer manufacturers) and Utilities had the biggest declines.

In the US, the Moody’s credit rating agency warned the US government it could lose its “AAA” credit rating. The US has already lost its “AAA” rating from the two other global rating agencies. The yield on US government bonds continued to rise, reaching their highest level in a dozen years. The FTC launched a lawsuit claiming Amazon limits consumer choice in online markets. All the American sectors ended in negative territory. Healthcare and Energy dropped the least while Utilities and Consumer Cyclicals dropped the most.

Wednesday: The markets were like a yoyo today. An early morning bump, followed by a steep drop before recovering most of the losses. At the end of the day, the S&P and Nasdaq were able to limp back into the green, but the TSX and the DJIA remained in the red. Higher interest rates continue to worry investors in both countries. Oil prices reached their highest point of the year after US crude oil supplies dropped significantly. Good for oil company shareholders, not so good for the central banks’ battle with inflation.

In Canada, the TSX was weighed down by concerns of weaker demand for commodities from China as well as higher interest rates having a negative impact on demand. In trading, the Energy and Technology sectors were the only one to end in the green. Utilities and Basic Materials fell the deepest into the red.

In the US, investors went bargain hunting after yesterday’s decline, while at the same time remained wary of a government shutdown. In the trading in the American sectors, Energy and Industrials posted the biggest gains while Utilities and Consumer Staples suffered the biggest losses.

Thursday: All four indexes ended higher as investors come to terms with higher for longer interest rates. On a positive note, lower consumer spending data gave investors hope the Fed would hold off on another rate hike. Oil prices ended lower after many investors took profits after the recent surge.

In Canada, the TSX moved solidly into the green after the losses of the previous days. Leading the really were the interest sensitive Technology and Consumer cyclicals sectors. Healthcare and Energy were the only sectors to lose ground.

In the US, investors are waiting to see if the US can avoid a government shutdown. They are also anticipating tomorrow’s PCE data which is expected to come in lower or with no change from last month. It was a broad-based rally in the American sectors, led by Basic Materials and Consumer Cyclicals. Utilities was the only sector to fall back.

Friday: The last day of trading in September, and the third quarter, got off to a good start with all four indexes moving higher when the latest core PCE data came in lower than expected. However, the likelihood of a US government shutdown remained. At the end of the day only the Nasdaq remained in the positive territory. Oil prices drifted lower as many investors took profits as the month and the third quarter came to an end.

In Canada, the TSX ended lower, driven down by lower demand for commodities, caused by higher interest rates, which led to lower commodity prices. In trading on Bay Street, Technology and Consumer Cyclicals posted the biggest gains of the Canadian sectors. The Energy and Utilities sectors experienced the biggest declines.

In the US, morning optimism was caused by core PCE coming in below 4% for the first time in more than two years. Unfortunately, the good news gave way to pessimism as a government shutdown appeared more and more likely. In trading on Wall Street, Consumer Cyclicals, Utilities and Technology were the only sectors to end in positive territory, while the Energy and Industrials sectors fell the deepest into the red.

Weekly Market and Portfolio Review

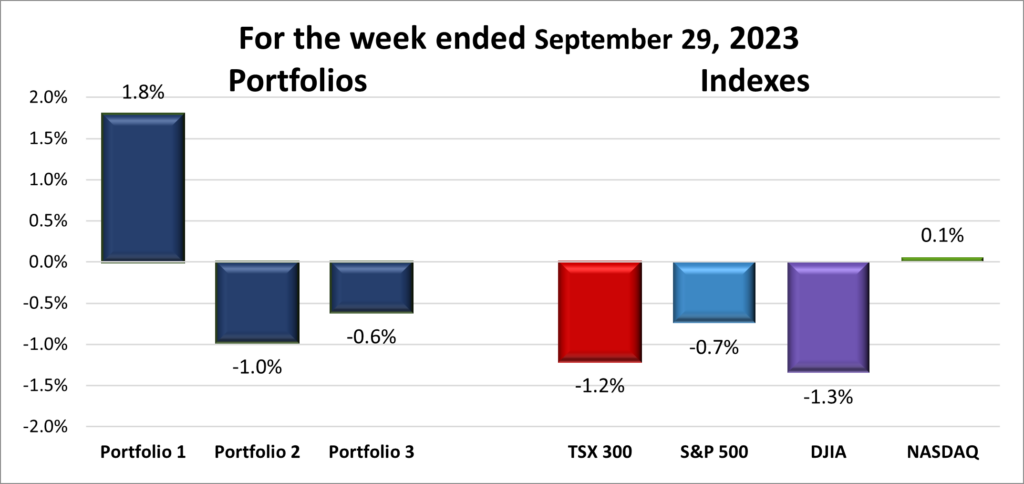

For the week, the TSX (SPTSX) dropped 1.2%, the S&P 500 (SPX) fell 0.7%, the DJIA (INDU) declined 1.3% and the Nasdaq (CCMP) rose 0.1%.

![]() The last week of September concluded with three out of four major indexes ending in the red, as you can see in the chart above. While it was not entirely unexpected, there were some surprises. The Nasdaq managed to eke out a slight gain for the week, albeit a modest one, after touching its lowest point in three months earlier in the week. Both the TSX and S&P also hit their lowest levels in three months, and the DJIA experienced its most significant single day drop since March.

The last week of September concluded with three out of four major indexes ending in the red, as you can see in the chart above. While it was not entirely unexpected, there were some surprises. The Nasdaq managed to eke out a slight gain for the week, albeit a modest one, after touching its lowest point in three months earlier in the week. Both the TSX and S&P also hit their lowest levels in three months, and the DJIA experienced its most significant single day drop since March.

The prevailing factor behind this week’s market downturn was the commitment from the Fed and the BoC to maintain higher interest rates for an extended period. Investors also grew apprehensive due to comments from Fed members suggesting the need for another interest rate hike to reach the 2% inflation target. Rising oil prices, which could sustain high inflation, and the looming possibility of a U.S. government shutdown further fueled investor concerns.

Additionally, as interest rates appear poised to rise and remain elevated for longer than anticipated, investors are increasingly drawn to US government bonds that are approaching a 5% yield. These bonds, backed by the US government, are often viewed as virtually risk-free. Consequently, they present a viable alternative to the volatility of stock prices.

![]()

![]() In terms of the portfolios, the week didn’t turn out as bad as anticipated. I had expected all three portfolios to end the week lower, so it came as a pleasant surprise to see Portfolio 1 posting a respectable weekly gain, as illustrated below. There were no significant winners, but, crucially, no substantial losers either. Many holdings, particularly in the technology sector, demonstrated decent performances. Portfolio 2 had reasonable performances from its energy and technology companies, although several Canadian financial holdings didn’t fare well. Portfolio 3’s technology holdings performed strongly, but these gains were offset by losses in its financial companies and the Brookfield family of companies.

In terms of the portfolios, the week didn’t turn out as bad as anticipated. I had expected all three portfolios to end the week lower, so it came as a pleasant surprise to see Portfolio 1 posting a respectable weekly gain, as illustrated below. There were no significant winners, but, crucially, no substantial losers either. Many holdings, particularly in the technology sector, demonstrated decent performances. Portfolio 2 had reasonable performances from its energy and technology companies, although several Canadian financial holdings didn’t fare well. Portfolio 3’s technology holdings performed strongly, but these gains were offset by losses in its financial companies and the Brookfield family of companies.

Given the gains in Portfolio 1 outweighing the combined losses in the other two portfolios, I decided to award the weekly portfolio performance with both a bull and bear award. Additionally, Portfolios 2 and 3 outperformed both the TSX and the DJIA (a hollow victory, I know). The week, while not as bad as expected, still didn’t achieve the ideal outcome with all three portfolios ending in positive territory. As we say goodbye to September, here’s to hoping for more ups than downs in the coming weeks for both the indexes and the portfolios.

Monthly Market and Portfolio Review

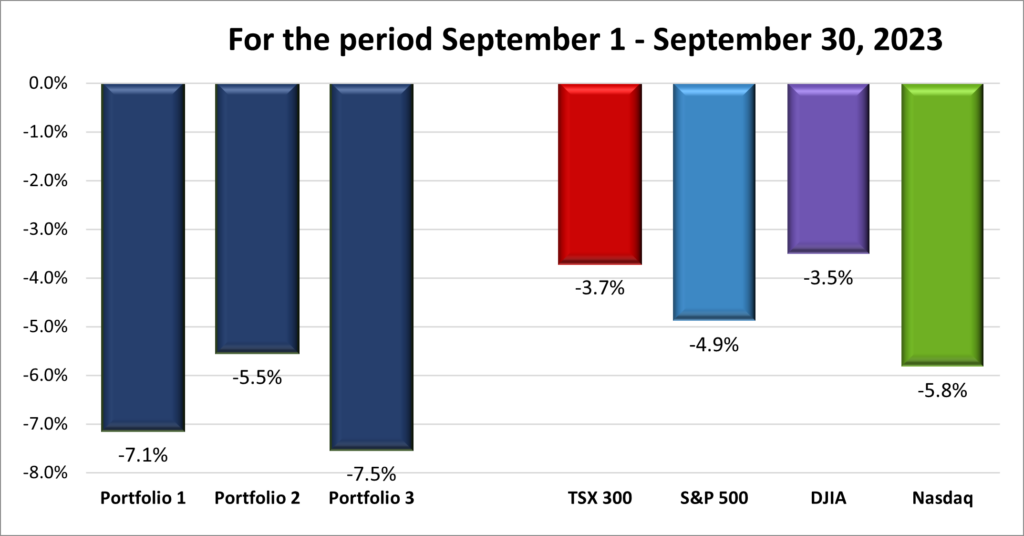

For the month, the TSX (SPTSX) fell 3.7%, the S&P 500 (SPX) sank 4.9%, the DJIA (INDU) dropped 3.5% and the Nasdaq (CCMP) plunged 5.8%.

![]() Historically, September stands out as one of the worst months for the North American stock markets, and this year was no exception. In fact, September is easily the frontrunner to be the worst month in 2023.

Historically, September stands out as one of the worst months for the North American stock markets, and this year was no exception. In fact, September is easily the frontrunner to be the worst month in 2023.

Following the tailwinds of summer, the markets encountered substantial headwinds. A major factor was the Fed’s decision at their September 20 meeting to maintain the US benchmark rate at its highest level in 22 years. Post-meeting, a few Fed members indicated that these elevated rates might remain for an extended period, which analysts refer to as “higher for longer.” The BoC echoed this higher rates for longer stance.

The impact of these heightened interest rates was felt keenly, not just by the tech-heavy Nasdaq and the S&P but also by the more traditional TSX and the DJIA. Yet, the challenges didn’t end there. Other headwinds, like surging oil prices leading to inflationary pressures, affected all four indexes. Additionally, an autoworkers strike hit the American indexes, while decreased demand for commodities weighed on the resource-centric TSX. Moreover, market volatility prompted many investors to shift from risky stocks to safer government bonds, further weighing down the markets.

The end of September brings a collective sigh of relief. One can only hope that as October unfolds and the year progresses, all four indexes will rebound, and investor confidence will return to both Canadian and American stock markets. Time will tell if this hope turns into reality. 😊

![]() The fate of the Portfolios often mirrors that of the broader indexes, and September exemplified this trend. Unfortunately, this month saw the portfolios experience even steeper losses than the indexes, as shown in the chart below. Portfolios 1 and 3, heavily laden with Nasdaq-based technology companies, faced significant declines. These once high-flying mega-cap technology companies, which fueled the summer rally, became a weight, pulling down not only the indexes but also the value of all three portfolios.

The fate of the Portfolios often mirrors that of the broader indexes, and September exemplified this trend. Unfortunately, this month saw the portfolios experience even steeper losses than the indexes, as shown in the chart below. Portfolios 1 and 3, heavily laden with Nasdaq-based technology companies, faced significant declines. These once high-flying mega-cap technology companies, which fueled the summer rally, became a weight, pulling down not only the indexes but also the value of all three portfolios.

Portfolio 2 fared relatively better due to its more balanced nature. With a focus on dividend-paying, stable Canadian blue-chip companies, it weathered the storm better (but not much) than its counterparts.

As we move into a new month, I hope that September’s challenges were merely a temporary setback on the road to better returns in October. Here’s to a more positive trajectory in the coming month. 😊

Companies on the Radar

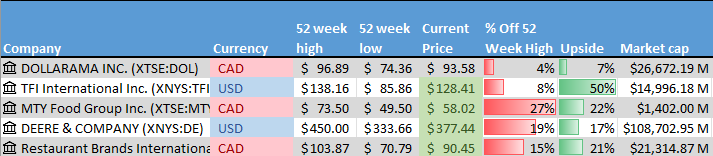

During the past week, I decided to remove Crown Castle Inc. (NYSE: CCI) from my watchlist due to its substantial debt load, especially in the current environment of prolonged higher interest rates. If I am seeking stability, a robust dividend yield (almost 7%), and promising growth, I would definitely consider this company.

During the past week, I decided to remove Crown Castle Inc. (NYSE: CCI) from my watchlist due to its substantial debt load, especially in the current environment of prolonged higher interest rates. If I am seeking stability, a robust dividend yield (almost 7%), and promising growth, I would definitely consider this company.

Catching my attention this past week was TFI International Inc. (TSX: TFII), a mid-sized Canadian transportation and logistics company operating across North America. This company has shown consistent growth in its sales, net income, earnings per share, and free cash flow over the past three years. Additionally, it offers a 1.1% dividend yield, making it an interesting prospect for further exploration.

I have added this company to the four holdovers from last week:

- Dollarama (TSX: DOL), a large Canadian company that operates dollar stores across Canada.

- MTY Food Group Inc. (TSE: MTY), A small cap Canadian consumer cyclical company that operates and franchises quick service and casual dining restaurants throughout North America and internationally.

- Deere & Company (NYSE: DE), a large American company that manufactures and sells agricultural equipment worldwide.

- Restaurant Brands International Inc. (TSE: QSR), A large cap Canadian consumer cyclical company that operates in the North American quick serve restaurant industry. The company owns Tim Horton’s, Burger King, and Popeye’s Louisiana Kitchen among others.

The Radar Check was last updated September 29, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended September 29, 2023: UP ![]()

- Amazon has signed a deal to invest up to US$4 billion in startup Anthropic, an artificial intelligence (AI) startup company. Amazon will receive early access to Anthropic’s AI technology, in return Anthropic will use Amazon’s Amazon Web Services for most of their needs. The deal provides Amazon with a key partner in the race for AI market share and should help them compete far more effectively with Google (NASD: GOOGL) and Microsoft (NASD: MSFT). Apparently, the market approved and gave Amazon’s share price a nice bump, sending the S&P and Nasdaq higher on Monday.

- Apple (NASD: AAPL) is appealing a court order requiring it to change its App Store policies after losing an anti trust claim. Apple is arguing the case was brought by a single company rather than a wide range of developers, thereby not requiring a nationwide remedy.

- Docebo (TSX: DCBO) announced the launch of ‘Docebo for Microsoft Teams’, an app that can be integrated in the Teams collaboration tool. The app help employees learn and train on corporate software and procedures.

Activity

Received interest on TD 1-year cashable GIC.

Sold Arm Holdings (NASD: ARM) My original reason for investing in Arm was to capitalize on the temporary spike when the company went public. The share price did spike on the Initial Public Offering (IPO), but it quickly fell below the price it went public (and the price I paid) so I decided to sell my shares.

I still like Arm as a long-term investment, but I do not want to ride the price lower. I may invest in Arm in the future but for now there are other less risky options available.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Canadian National Railway Co (TSX: CNR)

US $

NVIDIA Corp (NASD: NVDA)

Quarterly Reports

Costco Wholesale Corporation

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their fourth quarter 2023 financial results on September 26, 2023

- Revenue of $78,939 for the 17 weeks ended September 3, 2023, compared to $72,091 for the 16 weeks ended August 28, 2022. An increase of over 9%.

- Net income of $2,160 for the 17 weeks ended September 3, 2023, compared to net income of $1,868 in the 16 weeks ended August 28, 2022.

- Diluted earnings per ordinary share of $4.86 for the 17 weeks ended September 3, 2023, compared to earnings of $4.20 per share for the 16 weeks ended August 28, 2022.

- Revenue of $242,290 for the 53 weeks ended September 3, 2023, compared to $226,954 for the 52 weeks ended August 28, 2022. An increase of almost 7%.

- Net earnings of $6,292 for the 53 weeks ended September 3, 2023, compared to net earnings of $5,844 in the 52 weeks ended August 28, 2022.

- Diluted earnings per ordinary share of $14.16 for the 53 weeks ended September 3, 2023, compared to earnings of $13.14 per share for the 52 weeks ended August 28, 2022.

Portfolio 2

Portfolio 2 for the week ended September 29, 2023: DOWN ![]()

- MongoDB (NASD: MDB) announced four new AI powered capabilities to help developers quickly and easily automate data migrations, build data driven applications and enhance dashboard creation capabilities. In addition, MongoDB also launched MongoDB Atlas for the Edge, which makes it easier for companies to “deploy applications closer to where real-time data is generated, processed, and stored—across devices, on-premises data centers, and major cloud providers.”

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Alimentation Couche-Tard Inc (TSX: ATD)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week, except for per share data.

Portfolio 3

Portfolio 3 for the week ended September 29, 2023: DOWN ![]()

- E-commerce king Shopify (TSX: SHOP) invested in Faire, a global wholesale marketplace platform. The deal will allow Shopify’s merchants to find wholesale buyers and enable retailers to source products from Faire’s network of brands.

- Brookfield Asset Management (TSX: BAM) has entered into a joint venture with Axis Energy Ventures to create a renewable energy development platform in India. The venture plans to take advantage of the growth in demand for clean energy to supply energy to government, corporations, and emerging industries in the region.

- Lithium Americas (TSX: LAC) announced they plan to complete the spin out of their Argentina project next week. The new entity will be called Lithium Argentina and trade under the ticker LAAC on the Toronto Stock Exchange and the New York Stock Exchange.

Separately, LAC is speaking with the US Department of Energy about securing a US$1 billion loan for their Thacker Pass, Nevada mining project. When this mine goes into production it could be the largest source of lithium in North America and go a long way to replacing China as the leading supplier of lithium to North American electric battery makers.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Brookfield Renewable Corp (TSX: BEPC)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.