Items that may only interest or educate me ….

Canadian Economic news, US Economic news, Global interest rates ….

Canadian Economic news

The latest of the key economic reports that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Consumer Price Index

The August inflation data, as measured by the Consumer Price Index (CPI), revealed a significant increase in the annual inflation rate, rising to 4.0% following a 3.3% jump in July. This marks the second consecutive month of inflationary upticks and doubles the BoC’s targeted rate of 2%. On a monthly basis, inflation registered a 0.4% increase, a slight slowdown from July’s 0.6% rise. Analysts had anticipated an annual increase of 3.8% and a monthly increase of 0.3%.

The primary driver behind these increases was surging gas prices, which may not be a surprise, considering recent government-imposed taxes on gasoline. However, the cost of food and shelter continued to climb, with increases of 6.9% and 6.0%, respectively.

Core CPI, which excludes energy and food prices, also recorded a 4.1% increase, mirroring July’s figures. On a monthly basis, core CPI showed a 0.6% increase. While the core CPI’s pace remained stable from July, underlying inflation remained “well above the level consistent with our 2% target.”

These unexpectedly high headline and core inflation numbers signal that inflationary pressure is rising in Canada, potentially paving the way for the BoC to raise interest rates if prices continue to climb. With the likelihood of higher oil prices on the horizon, inflation is expected to continue to rise, given the outsized influence of fuel costs on the overall inflation rate. Higher energy prices have a cascading effect, impacting everything from production expenses to the transportation of goods.

The CPI serves as a crucial economic indicator, tracking changes in the average prices paid by consumers for a basket of goods and services over time. It is an essential tool for gauging inflation or deflation within an economy.

Minutes from last Bank of Canada meeting

The minutes from the BoC’s September 6 meeting revealed members discussed the state of the Canadian and global economies. Here is a quick breakdown:

- US Economy: The US economy was doing better than expected, with strong growth.

- Global Economy: However, the global economy was slowing down, mainly due to a slowdown in China, one of the world’s largest economies.

In Canada:

- Consumer Spending: During the second quarter, Canadians were not spending as much as before.

- Housing Market: The housing market was slowing down, despite high demand and low supply.

- Jobs: Employment was still good but not growing as fast.

- Inflation: The inflation rate was 3.5%, which is higher than the BoC’s target of 2%, and prices are expected to continue to climb.

So, what did the BoC decide? They chose to keep the benchmark interest rate at 5%. But here is the part that spooked the markets: they made it clear that they might raise rates again if prices keep going up. In fact, the BoC’s Governor even said that interest rates might need to go even higher to bring prices back to their target.

Given the recent report on prices (the CPI report), I would not be surprised if things get more expensive, especially energy. If the next report shows that prices are still high or going up, I expect the BoC will have to raise interest rates again.

US Economic news

US interest rate update

Last Wednesday, the Federal Reserve’s committee (FOMC) decided not to change the main interest rate, which is currently between 5.25% and 5.50%. This was what most experts anticipated. After the meeting, the Fed said they expect one more 0.25% increase in 2023 and then the rate will remain high with possible cuts in 2024.

The Fed started raising interest rates in March 2022 when rates were at 1.25%. They did this to tackle rising prices (inflation). Since then, they have raised rates a total of 10 times, with six of those increases occurring in 2023. Their main goal is to bring inflation down to 2%. However, even though the Fed has been increasing rates, consumer spending and economic growth have remained robust. Inflation currently stands at 3.7%, which is much better than the 9% rate from a year ago, but it is still far from the Fed’s 2% target. Additionally, with the price of oil on the rise, it presents a challenge for the Fed to further reduce inflation.

For consumers with loans or mortgages that have variable interest rates, be prepared for higher costs. For us investors, when the Fed raises rates, it usually leads to a drop in stock prices, making it harder to generate returns in the stock markets, especially if rates remain elevated for an extended period. Furthermore, businesses will face increased borrowing costs, which could result in slower growth for both companies and the overall economy.

The Fed’s decision to keep interest rates unchanged is a sign that they are taking a cautious approach to fighting inflation. They are aware of the risks of raising rates too quickly, such as causing a recession. However, as Fed Chair Jerome Powell said, they are committed to bringing inflation down to its 2% target. Investors and businesses will be closely watching upcoming data to try and gain insight into the Fed’s future actions.

Global interest rates

Great Britain

By a vote of 5 – 4, the Bank of England’s (BoE) Monetary Policy Committee decided to hold their benchmark interest rate at 5.25%, a fifteen year high. It was the first time since December 2021 that the BoE has not raised Britain’s key interest rate. The latest British CPI report showed that inflation had dropped to 6.7%, its lowest since February 2022, and down from July’s 6.8%.

European Union

The European Central Bank (ECB) raised interest rates 0.25% to 4%. This was the tenth consecutive increase, bringing the rate to its highest level since the start of the Euro in 1999. The ECB hinted this could be the last increase in their fight to bring down inflation.

Switzerland

The Swiss National Bank kept its rates on hold at 1.75% after the Swiss inflation rate came in at 1.6% for August, within their 0 – 2% target range. However, they left the door open for future hikes should inflation rise above the acceptable range.

Sweden

Sweden’s Riksbank raised its benchmark rate 0.25% to 4.0%, as expected. That was the eighth consecutive increase since inflation spiked to 10% in December 2022. Since then, the Riksbank has been able to bring inflation down to 4.7% in August.

Norway

Norges Bank, Norway’s central bank, raised its benchmark rate by 0.25% to 4.25%. The bank signaled there could be another increase in December to bring down inflation which is forecast to be 4.7% in 2024.

Australia

Australia’s central bank, the Reserve Bank of Australia (RBA), left the country’s benchmark rate at 4.1%, an eleven year high. They RBA decided to wait for the previous rate increases to work their way through the Australian economy to see the full effects of the rate hikes before deciding whether to raise or lower the rate.

New Zealand

The Reserve Bank of New Zealand (RBNZ) increased its benchmark rate to 5.5% in May, a fourteen year high, and has kept it their ever since. The RBNZ does not plan to raise rates again, however, they do not expect to start lowering the rate until 2025.

Japan

The Bank of Japan left its ultra low interest rate unchanged at -0.1% (yes, negative 0.1% 😊) for the short term, and 0% for the ten-year bond yield. The government also said it would continue to support the Japanese economy until inflation hit the bank’s 2% goal.

At the start of month, I said September has historically not been kind to the markets. This week did nothing to dispel that trend. Let’s see what happened ….

Weekly Market Review

Monday: The four major North American indexes were largely flat other than the Toronto Stock Exchange Composite Index (TSX). Oil prices rose on supply concerns and recovery of Chinese demand.

In Canada, the TSX was sharply lower by the end of the day as investors prepare for Tuesday’s latest CPI inflation report. Analysts are expecting the report to show inflation rose in August. Investors are concerned the data will come in higher than expected, causing the BoC to respond with an increase to the benchmark rate. In trading, Consumer Staples was the only Canadian sector to advance, while the Technology and Healthcare sectors led broad-based declines.

In the US, all three indexes – the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – were in the green but essentially flat with minimal gains. The FOMC meeting starts Tuesday. Wednesday they will announce interest rates and release projections about the economy and the likely path forward for interest rates. Until then, investors are sitting on the sidelines to avoid getting caught on the wrong side of the announcement. In trading, Energy and Technology were the best performing American sectors, while Consumer Cyclicals and Healthcare posted the biggest declines.

Tuesday: Not a good day for any of the four indexes as all ended in negative territory. Several central banks are meeting this week to update their monetary policies, with none having more impact than the Fed’s update. Oil prices touched ten-month highs during today’s trading session before retreating.

In Canada, higher than expected inflation numbers raised fears of another interest rate hike. As a result, the TSX fell sharply at the start of the trading session and stayed low for the remainder of the day, sending all Canadian sectors lower. Consumer Cyclicals and Financials declined the least, while Technology and Utilities were the biggest losers.

In the US, the three indexes dropped in morning trading before rebounding in afternoon trading, but it was not enough to recover the morning’s losses. The broad sell off was a result of investors taking money off the table ahead of the Fed’s monetary update announcement tomorrow. In trading, Telecommunications Services and Healthcare were the only American sectors to end in positive territory. Utilities and Energy declined the most.

Wednesday: All four indexes were in the green for most of the day until a last-minute dip put all of them into the red. The markets fell after the FOMC announced they were holding the US benchmark interest rate to 5.5% but suggested one more hike by the end of the year. They also forecast the rate would remain higher for longer, likely through most of 2024. Oil prices also felt the impact of the Fed’s announcement, dropping on worries of higher interest rates.

In Canada, the Fed’s hawkish stance on US interest rates unsettled the TSX. To make matters worse, the energy sector accounts for 20% of the TSX so lower oil prices also dragged the index lower. In trading on Bay Street, the Basic Materials (miners and fertilizer manufacturers) and Utilities led advancers, while Technology, Energy and Consumer Cyclicals were the only sectors to decline.

In the US of A, the markets fell after Fed Chair Jerome Powell said the Fed was focused on bringing inflation down rather than on a soft landing, where inflation falls without a significant economic downturn. In trading on Wall Street, Telecommunications Services, Consumer Staples, and Utilities were the only sectors to end higher. Leading the other sectors downward were the interest rate sensitive Technology and Consumer Cyclicals sectors.

Thursday: All four indexes plummeted today as investors spent most of the day digesting yesterday’s comments from the Fed that rates will go higher and remain their longer.

In Canada, The TSX posted its biggest drop in a year thanks to a decline in oil and commodity prices caused by the Fed’s comments. In trading, all the Canadian sectors ended solidly in the red. Consumer Staples and Healthcare were down the least. The worst performer was Technology, by far, followed by Basic Materials and Industrials.

In the US, the three indexes fell for a third straight day as the Fed’s hawkish tone from yesterday weighed heavily on investors. The good news is the US economy remains strong as the jobless claims fell to their lowest since January 2023. In trading, all sectors were down. The defensive sectors Utilities and Consumer Staples posted the smallest losses, while Consumer Cyclicals and Basic Materials dropped the most.

Friday: The indexes spent most of the day in positive territory before dropping into negative territory in afternoon trading. Investors continued to assess the hawkish comments from the Fed earlier in the week and are not liking the central message of higher interest rates for longer. The higher borrowing costs mean companies will have to use more of their money to pay off their debt rather than invest in their business. For consumers, it means they will have higher interest payments on loans and mortgages and less money to spend on other items. Oil prices inched upward on ongoing supply concerns.

In Canada, the TSX ran its losing streak to five. Already knocked around by the Fed’s hawkish comments, investors are worried the BoC will follow the Fed’s lead and raise the Canadian benchmark rate and hold it longer. In trading on Bay Street, Telecommunications Services and Utilities posted the biggest gains, while the interest sensitive sectors Technology and Consumer Cyclicals posted the biggest declines.

In the US, all three indexes posted a fourth day of losses as investors have become wary of what higher rates will do to the economy. In trading on Wall Street, Technology and Energy had the biggest gains while Consumer Cyclicals and Financials dropped the most.

Weekly Market and Portfolio Review

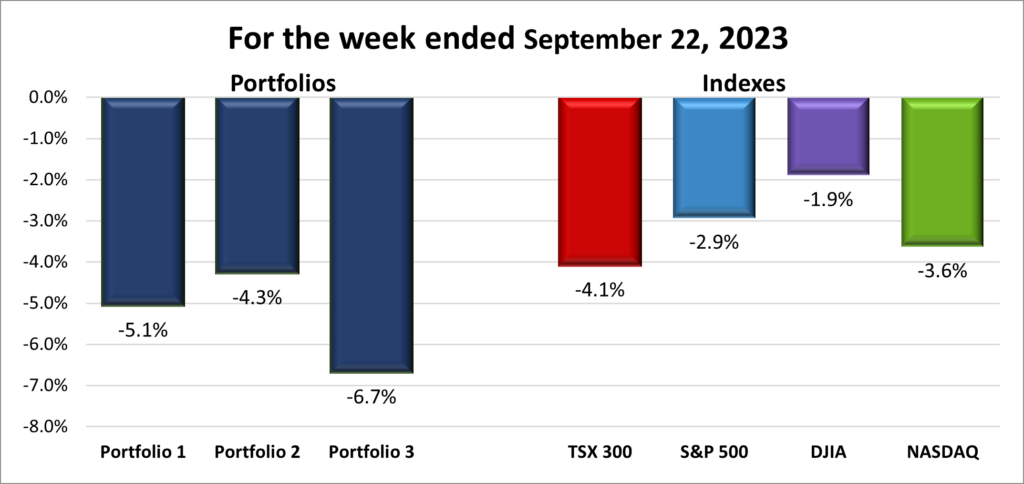

For the week, the TSX (SPTSX) plummeted 4.1%, the S&P 500 (SPX) sank 2.9%, the DJIA (INDU) fell 1.9% and the Nasdaq (CCMP) plunged 3.6%.

![]() “Higher for Longer.” These three words, expressed in comments by Fed Chair Jerome Powell at the end of the FOMC meeting, triggered a sharp drop in the four major North American indexes. On Thursday, as illustrated in the graph above, American indexes experienced their most significant single-day decline since March. Investors rushed out of riskier stocks and sought refuge in safer assets, including government bonds and less risky companies. Both the Nasdaq and the S&P recorded their third consecutive weekly losses, while the DJIA, consisting of larger blue-chip firms, faced more modest declines.

“Higher for Longer.” These three words, expressed in comments by Fed Chair Jerome Powell at the end of the FOMC meeting, triggered a sharp drop in the four major North American indexes. On Thursday, as illustrated in the graph above, American indexes experienced their most significant single-day decline since March. Investors rushed out of riskier stocks and sought refuge in safer assets, including government bonds and less risky companies. Both the Nasdaq and the S&P recorded their third consecutive weekly losses, while the DJIA, consisting of larger blue-chip firms, faced more modest declines.

The impact of the Fed’s hawkish comments extended beyond the U.S., affecting the TSX, which suffered its most substantial weekly drop since September 2022.

![]() As bad as a week as it was for the indexes, it was worse for the three Portfolios, as you can see in the chart below. All three portfolios fell more than the TSX, the worst performing index. The overall decline in the market, especially the riskier technology companies, contributed to the decline of all three portfolios. Even the more balanced Portfolio 2 dropped more than the TSX. Sigh!

As bad as a week as it was for the indexes, it was worse for the three Portfolios, as you can see in the chart below. All three portfolios fell more than the TSX, the worst performing index. The overall decline in the market, especially the riskier technology companies, contributed to the decline of all three portfolios. Even the more balanced Portfolio 2 dropped more than the TSX. Sigh!

It was a dismal week all around. For the indexes and more importantly, the portfolios. I will be glad to see the end of September!

Companies on the Radar

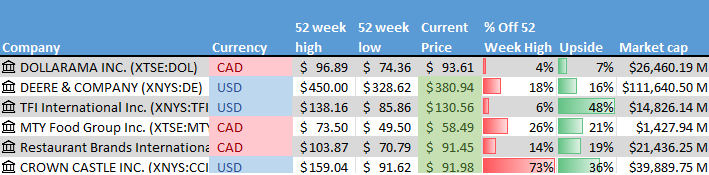

A new company came onto my radar this past week – TFI International Inc (TSE: TFII). They are a large Canadian trucking and logistics company that operates throughout North America. Over the last three years, their sales, net income, and cash flow have all shown positive growth trends. Additionally, with the increasing trend of online shopping, the company is benefiting from the growing demand for shipping and logistics services.

A new company came onto my radar this past week – TFI International Inc (TSE: TFII). They are a large Canadian trucking and logistics company that operates throughout North America. Over the last three years, their sales, net income, and cash flow have all shown positive growth trends. Additionally, with the increasing trend of online shopping, the company is benefiting from the growing demand for shipping and logistics services.

I have added this company to the five from last week so there are now six companies I want to take a closer look at.

- Dollarama (TSX: DOL), a large Canadian company that operates dollar stores across Canada.

- Deere & Company (NYSE: DE), a large American company that manufactures and sells agricultural equipment worldwide.

- MTY Food Group Inc. (TSE: MTY), A small cap Canadian consumer cyclical company that operates and franchises quick service and casual dining restaurants throughout North America and internationally.

- Restaurant Brands International Inc. (TSE: QSR), A large cap Canadian consumer cyclical company that operates in the North American quick serve restaurant industry. The company owns Tim Horton’s, Burger King, and Popeye’s Louisiana Kitchen among others.

- Crown Castle Inc. (NYSE: CCI), a large cap American company that owns and operates cell towers throughout America. The company is currently at its lowest price in five years and offers a 6+% dividend.

The Radar Check was last updated September 22, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended September 22, 2023: DOWN ![]()

- Tesla (NASD: TSLA) had initial talks with Saudi Arabia about building an electric vehicle (EV) factory in the country. This comes after the Turkish government asked the company to build a factory in Turkey. Both countries are wooing Tesla so you can be sure the company will get a great deal. Currently, Tesla makes it vehicles in the US, China, Germany, and another factory in Mexico under construction.

Its not an EV factory, but Tesla has proposed to the Indian government to build and sell battery storage systems in India. Tesla is seeking incentives from the government to build the factory in India but so far, the government has indicated there are no incentives on the table. It will be interesting to see who blinks first in these discussions. Tesla would like to build an EV factory in India and the government knows this. I would not be surprised to see a quid pro quo here. Tesla gets to build an EV plant in exchange they will also build a battery storage factory without any taxpayer dollars being spent. - Alphabet’s (NASD: GOOGL) Google has started to integrate its artificial intelligence (AI) chatbot into their products. Bard will be able to find information embedded in users’ Gmail accounts, find useful videos on YouTube, get directions from Google Maps, and extract information from files saved on Google Drive. To address privacy concerns, Google has said any data retrieved will not be used to sell targeted ads.

In unrelated news, Alphabet’s Waymo One ride robotaxis company, fresh off gaining permission to expand service in San Francisco from the California Public Utilities Commission, announced a six-month tour throughout Los Angeles. The plan is to build up excitement in the Waymo service by providing free rides within designated neighbourhoods before Waymo officially rolls out the service across Los Angeles. - The United Auto Workers increased the number of strikes at General Motors (NYSE: GM) and Stellantis (NYSE: STLA) distribution centres across the US. Ford (NYSE: F) was spared the additional strikes after it provided key concessions to the union.

- PayPal (NASD: PYPL) gets a new Chief Executive Officer next week. Alex Chriss, an executive from Intuit (NASD: INTU), will take over from current CEO Dan Schulman on September 27, with Schulman to staying on the board until May 2024.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

No C$ dividends this past week.

US $

Skyworks Solutions Inc (NASD: SWKS)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended September 22, 2023: DOWN ![]()

- Disney (NYSE: DIS) plans to spend US$ 60 billion over the next ten years to improve their parks and cruise experiences in order to continue to grow attendance numbers.

- MongoDB (NASD: MDB) announced their MongoDB Atlas for Manufacturing and Automotive initiative. This will allow manufacturers and automotive companies create applications that take advantage of real time data by using the latest in connected technology.

Activity

Cashed in the one-year cashable GIC in order buy ….

Bought: Telus (TSX: T) Added a few more shares of Telus. Although the share price has fallen, I am confident Telus will rebound and prosper over the next 5+ years. In effect, I see this as a buying opportunity for a low-risk company. In addition, with the share price down, the dividend yield is up to 6.36%, almost double the 3.35% yield of the GIC.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX: DIR.UN) DRIP

Hammond Power Solutions (TSX: HPS.A)

Supremex (TSX: SPX)

US $

No US$ dividends this past week

Quarterly Reports

No quarterly reports this past week, except for per share data.

Portfolio 3

Portfolio 3 for the week ended September 22, 2023: DOWN ![]()

- After 20 years at Microsoft (NASD: MSFT), longtime product chief Panos Panay has left to join Amazon (NASD: AMZN) where he will oversee the Alexa and Echo devices division. While at Microsoft, he helped create the Surface brand of products as well as the release of Microsoft’s Windows 11.

in other Microsoft news, Microsoft announced additional integration of AI with their products. Copilot, the name of their AI tool, is being integrated into their Bing search engine, Edge Browser, Office productivity suite and the latest update to the Windows 11 operating system. The company also announced a few new products in their Surface line of hardware devices.

Britain’s anti trust regulator, the Competition and Markets Authority (CMA), indicated that Microsoft’s restructured proposal to acquire Activision Blizzard (NASD: ATVI) “substantially addresses previous concerns”. A few minor concerns remain but if/when they are resolved it clear the path for the deal to complete.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.