This week’s update kicks off with some promising news that could impact your future investments and for borrowers across the board, whether they are individuals with mortgages, personal loans, or businesses with loans. As anticipated, the Bank of Canada trimmed the Canadian benchmark interest rate by 0.25%. While it may seem like a small adjustment, it is a step in the right direction. Additionally, positive developments emerged on the US economic front, indicating a cooling job market, which often signals a slowdown in the US economy. This shift raises the possibility of a rate cut in the US later this fall.

In addition to the economic updates, we will continue our series addressing frequent questions from those new to investing, along with insights gained from my personal experiences. This week, while researching our question of the week, I stumbled upon something new of which I was not previously aware. Once again, the process of writing this blog proves to be a learning experience for me. 😊 Let’s take a look at other highlights from this past week….

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, What about fractional shares?, What I learned this week, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Interest rate update

As expected, the Bank of Canada (BoC) reduced the Canadian benchmark interest rate by 0.25%, bringing it down to 4.75%. This move marked the first rate cut in over four years and positioned Canada’s central bank as the first among the G7 nations (Canada, France, Germany, Italy, Japan, United Kingdom, and the USA) to take such action. The rate had remained steady at 5.0% for eleven consecutive months prior to this adjustment.

The rate cut was prompted by inflation dropping below 3.0%, putting it within the BoC’s target range of 1.0% – 3.0%. BoC officials expressed confidence in the direction of inflation, anticipating reaching the 2% target sometime in 2025. However, they also noted concerns about a slowdown in the Canadian economy. The BoC is attempting to achieve a ‘soft landing,’ where inflation returns to 2% without stalling economic growth entirely. Additionally, they pointed out that the US economy is starting to slow, which could lead to decreased demand for Canadian products.

The modest 0.25% rate cut suggests the BoC is taking a gradual approach to adjusting interest rates while carefully monitoring the impact of their actions on inflation and economic growth. BoC Governor Tiff Macklem hinted at further cuts in the future but cautioned against expecting a return to pre-pandemic levels. For those who believe high rates have been a drag on stocks for the last two years, lower rates cannot come soon enough.

Lowering interest rates carries the risk of widening the gap between the Canadian and US benchmark rates. With US Federal Reserve officials signaling no imminent cuts to the US rate, such a gap could weaken the Canadian dollar against the US dollar, making imports more expensive for Canadians. Following the announcement, the Canadian dollar only experienced a slight decline. However, if the BoC follows through on its indications to lower the Canadian rate further, the disparity with the US rate could widen, potentially resulting in a more pronounced drop in the Canadian dollar’s value.

Labour Force Survey (LFS)

Statistics Canada’s May Labour Force Survey (LFS) presented a mixed picture of the job market, with jobs, unemployment and wages all higher. The Canadian economy added 27,000 jobs in May, surpassing analysts’ expectations of 22,500 jobs. This follows an unexpected surge of 90,400 jobs in April. The increase was mainly due to a 1.7% rise in part-time employment, while full-time employment dipped by 0.2%.

The unemployment rate matched analysts’ predictions, coming in at 6.2% in May, slightly up from 6.1% in April. Unemployment has been on the rise since April 2023, climbing by 1.1% over that period.

Wage growth, a key concern for the BoC, also picked up pace, accelerating to an annual rate of 5.1%, compared to 4.7% in April.

Following April’s unexpected surge of 90,400 jobs, the lower number of jobs in May suggests the Canadian economy is cooling. However, the job numbers were still higher than expected. Of more concern to the BoC would be the increased wage growth. Yet, as far as the BoC is concerned, the rise in unemployment might offset the impact of higher jobs and wages.

After the BoC’s recent decision to lower the benchmark rate by 0.25% to 4.75%, many analysts anticipated another 0.25% cut in July. However, this mixed report has reduced the likelihood of a July cut.

Canadian market volatility

During the past week, Canada’s Volatility Index (VIXC), measured by the TSX 60, experienced a slight uptick, closing at 9.73, up from 8.30, amidst an otherwise stable period. This rise could be attributed to investor optimism stemming from the BoC’s interest rate cut and mixed US labour reports, which have fueled expectations of a potential rate cuts by the US Federal Reserve.

Often referred to as Canada’s ‘fear gauge,’ the VIXC offers insights into expected volatility within the Canadian stock markets. Readings above 20 typically indicate high volatility, while those below 20 suggest lower levels.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Labour data

Each month, three labour market reports provide a snapshot of the current state of the American economy. Analyzing the latest data from the Job Openings and Labor Turnover Survey (JOLTS), ADP National Employment Report, and the Employment Situation Summary (ESS) provides a comprehensive view of the US labour market and reveals key trends in employment, and wage growth that can influence future economic policy.

Labor Department’s Job Openings and Labor Turnover Survey (JOLTS)

The Labor Department’s April JOLTS report revealed fewer job openings than expected, with 8.1 million available positions on the last business day of April. Analysts had been anticipating 8.340 million. This represents a 4% drop from the 8.488 million openings in March and an 18% decrease from the 9.9 million openings a year ago. These April numbers are the lowest since June 2021. Additionally, the ratio of job openings to each unemployed person fell to 1.24 from 1.3 in March.

When we look at the year-over-year data, ‘Private education and health services’ saw the largest increase in job openings, rising by 6.2%. In contrast, the ‘Information’ industry had the smallest increase at 3.5%. On a month-to-month basis, ‘Professional business services’ led the way with a 0.5% increase, while the ‘Information’ sector again underperformed, dropping by 1.3%. This decline in information sector jobs aligns with recent news that Alphabet (NASD: GOOGL) and Microsoft (NASD: MSFT) are planning to lay off hundreds of employees in the coming weeks.

The reduced number of job openings suggests that the labour market is continuing to cool down and is heading towards a more balanced state between labour supply and demand. This cooling labour market could help ease upward pressure on prices and continue to reduce inflation. However, with 1.24 job openings per unemployed person, the labour market remains relatively tight, indicating that there are still more job openings than unemployed individuals available to fill them.

ADP Employment Report

The May ADP Employment Report showed private payrolls growing by 152,000, a noticeable drop from the revised 188,000 in April and well below the analysts’ forecast of 175,000. Annual pay growth held steady at 5.0% for those who stayed in the same job. However, for job switchers, pay growth continued its decline, slipping to 7.8% from a revised 8.0% in April.

These lower hiring numbers and slower wage growth hint at a cooling job market, suggesting the possibility of a broader economic slowdown.

Bureau of Labor Statistics’ Employment Situation Summary (ESS).

The Labor Department’s ESS for May brought some surprises to the table. Nonfarm payroll employment saw a significant uptick, surging to 272,000 jobs, compared to a gain of 175,000 jobs in April. Analysts, who were expecting an increase of 185,000, were caught off guard by the robust numbers following a slowdown in April. Meanwhile, the unemployment rate saw a slight increase, coming in at 4.0% in May, contrary to analysts’ predictions of it remaining unchanged at 3.9%. This marked the first time in 27 months that it was not below 4.0%. Additionally, average hourly earnings rose 0.4% in May, up slightly from April’s 0.2% gain. On a year over year basis, the pace of wage growth accelerated to 4.1% from April’s 3.9% increase. Both number came in higher than analysts’ expectations of increases of 0.3% and 3.9%, respectively.

Despite April’s data showing signs of a slowing labour market, the May report paints a different picture. With more people joining the workforce and wages showing steady growth, the labour market remains robust. However, this unexpected surge in employment and wages does little to advance the case for the Fed to lower the interest rate.

Conclusion

Taken together, these reports paint a somewhat complex picture of the US labour market. The JOLTS report suggests a potential cooling down with fewer job openings compared to recent months. Similarly, the ADP report shows a decrease in hiring activity. However, the robust job growth and continued wage gains in the latest Employment Situation Summary (ESS) contradict this notion.

This discrepancy highlights the importance of considering multiple data points to understand the labour market’s true condition. While there might be signs of a slowdown in some sectors (like the ADP report suggesting), the overall picture from the ESS indicates a resilient job market.

The Fed will likely closely monitor these trends as they decide on future interest rate decisions. It will be crucial to see if the robust job market numbers from the ESS are sustained in the coming months, or if they were simply an anomaly.

American market volatility

The CBOE Volatility Index (VIX), known as the market’s fear gauge, dipped to 12.22 after reaching 12.91 the previous week. This decline could be attributed to mixed labour data and increasing speculation regarding potential rate cuts by the Fed later this year. With the VIX below the 20 threshold, commonly linked with market calmness, investors are feeling less apprehensive in the short term.

What about fractional shares?

Fractional shares are a revolutionary way to invest, allowing you to own a piece of even the most expensive companies without needing a huge amount of money upfront. The ease of buying fractional shares makes it super simple to start investing in some of the top companies. Think of investing in Constellation Software (TSE: CSU) for just $50 instead of needing thousands! While this feature is more common in the US at brokers such as Robinhood, Fidelity, and Charles Schwab, Canadian options are limited. Fortunately, a few Canadian brokerages such as Wealthsimple and Interactive Brokers offer fractional share purchases allowing you to invest in expensive companies with smaller amounts. Unfortunately, trading accounts with most Canadian banks do not support this capability (at least my TD Direct Investing account does not).

If the companies you are interested in are very expensive, buying a fraction of share might be an effective way to become an owner. Fractional shares offer several advantages over whole shares, especially for beginning investors or those on a budget:

- Lower barrier to entry: This is the biggest perk. Fractional shares allow you to invest in companies with high share prices that might otherwise be out of reach. For instance, if a stock trades at $1,000 per share, you can still invest in the company with a smaller amount, say $200, which would buy you a fraction of a share.

- Improved diversification: A core tenet of investing is diversification, which means spreading your money across various investments to reduce risk. Fractional shares allow you to include more companies in your portfolio without a significant upfront investment. This helps you achieve better diversification even with limited capital.

- Dollar-cost averaging: This strategy involves investing a fixed amount of money at regular intervals. Fractional shares can be particularly useful for dollar-cost averaging because you can invest your set amount regardless of the stock price. This allows for consistent participation in the market.

- Invest leftover cash: If you have small amounts of money leftover after other investments, fractional shares enable you to put that money to work rather than letting it sit idle.

- Potentially faster returns: With fractional shares, you can start benefiting from potential growth and dividends sooner rather than waiting to save enough for a whole share.

Remember, while there are advantages, there are also some things to consider with fractional shares:

- Voting rights: Generally, only holders of whole shares get voting rights on company matters. Fractional share ownership typically does not come with voting rights.

- Dividend distribution: Dividends are typically paid per share. With a fractional share, you might receive a very small fraction of a dividend, which some brokerages may round down to zero.

- Potential fees: Some brokers may have minimum fees per trade. With fractional shares, this could eat into a smaller investment more proportionally than with a whole share purchase.

- Psychology: Some investors may prefer the simplicity of owning whole shares. It can be easier to track and understand your portfolio holdings when dealing in whole numbers.

If you are interested in buying fractional shares, check with your broker to confirm they offer this service and understand any potential transaction fees, as policies can vary. To optimize your investment, consider using an online broker that does not charge transaction fees. After all, buying a $100 fractional share only to lose $10 in fees each time you purchase a fractional share would almost defeat the purpose.

What I learned this week

- The group of five mega-cap tech companies – Nvidia (NASD: NVDA), Microsoft, Amazon.com (NASD: AMZN), Meta (NASD: META), and Alphabet – have been given the nickname “Fab Five” due to their outstanding returns over the last two years. All five have seen their share price rise on strong earnings because of high demand for artificial intelligence (AI) products and services.

The big question is, can that high demand continue? Many analysts believe it can. Companies need to invest in AI to stay competitive. When times are good and cash is flowing, companies invest in AI to keep up with their rivals. When times are tough, AI can help companies’ lower costs by reducing expenses. - Here is something else I discovered: you can buy stocks in fractional units in Canada. Who knew? There is always something to learn in investing. 😊

Weekly Market Review

Monday: the markets got off to a shaky start this month with the Toronto Stock Exchange Composite Index (TSX) and the Dow Jones Industrial Average (DJIA) ending in the red while the S&P 500 Index (S&P), and the Nasdaq Composite Index (Nasdaq) ended in the green. Oil prices dropped sharply on demand concerns, despite OPEC+ members (Organization of the Petroleum Exporting Countries and allies) extending their oil production cuts until the end of 2025.

In Canada, lower oil prices acted as a lead weight for the TSX, offsetting gains in Consumer Staples and Utilities, the top two performers in the Canadian sectors. The biggest drops were in the Energy and Healthcare sectors.

In the US, a glitch at the NYSE caused many of the NYSE listed stocks to be halted due to massive price swings. Lower manufacturing data weighed on the markets for the second month in a row, giving investors hope the Fed could start lowering rates in September. In trading, Technology, Healthcare and Consumer Staples were the only American sectors to post a daily gain. At the other end of the spectrum, Energy and Utilities posted the biggest daily drops.

Tuesday: in a choppy day of trading, the American indexes ended higher, while the TSX ended lower. Oil prices have fallen to their lowest price in over four months on concerns of oversupply.

In Canada, signs of a slowdown in the global economy has led to a drop in commodity prices which in turn has weighed on the resource heavy TSX. investors await tomorrow’s rate decision by the BoC. In trading, Consumer Staples and Industrials sported the biggest wins while Basic Materials (miners and fertilizer manufacturers) and Energy lost the most.

In the USA, a weaker than expected job openings report provided further evidence that the US economy is slowing. For those wanting a rate cut this is good news. For those looking for work, not so good news. In trading, Telecommunications Services and Consumer Staples advanced the most while Basic Materials and Energy suffered the biggest decline.

Wednesday: a cut to Canadian interest rates and US economic data suggesting a cooling US economy propelled all four indexes solidly into positive territory for the day. The price of oil rose on optimism the Fed will cut interest rates later this year.

In Canada, the BoC lowered the benchmark rate to 4.75% and suggested more rate cuts were likely. The expectations of a US rate cut later in the year led to a rise in commodity prices, adding to the TSX’s gains. All Canadian sectors ended higher, led by Basic Materials and Technology, with Telecommunications Services and Financials bringing up the rear.

In the US, the S&P and Nasdaq closed at record highs as the job market continues to slow, causing investors to believe the Fed will lower rates later this year. In trading, it was a day of broad-based gains, led by Technology and Industrials. Utilities was the only sector to end lower.

Thursday: the indexes ended with mixed results as investors await tomorrow’s US labour report, looking for further signs of a slowing US economy. The TSX and DJIA ended in the green while the S&P and the Nasdaq ended in the red. The European Union’s European Central Bank joined Canada and lowered its benchmark rate for the first time since 2019, dropping the rate 0.25% to 3.75%. Oil prices continued to rally on speculation the Fed will lower interest rates in the fall.

In Canada, commodity prices rose, boosting the resource oriented TSX higher. Investors are waiting for the latest employment number from Canada and the US, due Friday. In trading, Basic Materials and Energy led all Canadian sectors, while Consumer Cyclicals and Telecommunications Services suffered the biggest declines.

In the USA, this week’s softer than expected labour reports have investors once again believing the Fed will lower rates this year. In trading, Basic Materials and Consumer Cyclicals gained the most, while Utilities and Industrials lost the most.

Friday: all four indexes ended the session lower after a stronger-than-expected US labour report pushed back expectations of an interest rate cut by the Fed until this fall at the earliest. Oil was down on lowered expectations of a rate cut, offsetting news Saudi Arabia and Russia were prepared to halt or reverse output increases scheduled for this fall if there was an oversupply of oil.

In Canada, stronger than expected Canadian labour data may have pushed back the timing of the next cut to Canadian rates. As well, concerns that the Fed will hold interest rates higher for longer weighed on the TSX. In trading, Technology and Consumer Cyclicals were the only sectors to record a gain. Basic Materials and Industrials had the biggest declines.

In the US, all three indexes were bouncing up and down throughout the session as investors were uncertain about the mixed messages from the labour report. On one hand, it indicated a strong economy. While on the other, it likely delayed a possible rate cut. The mixed messages resulted in a sector wide decline during trading. Technology and Healthcare had the smallest drop, while Basic Materials and Telecommunications Services had the steepest drops.

Weekly Market and Portfolio Review

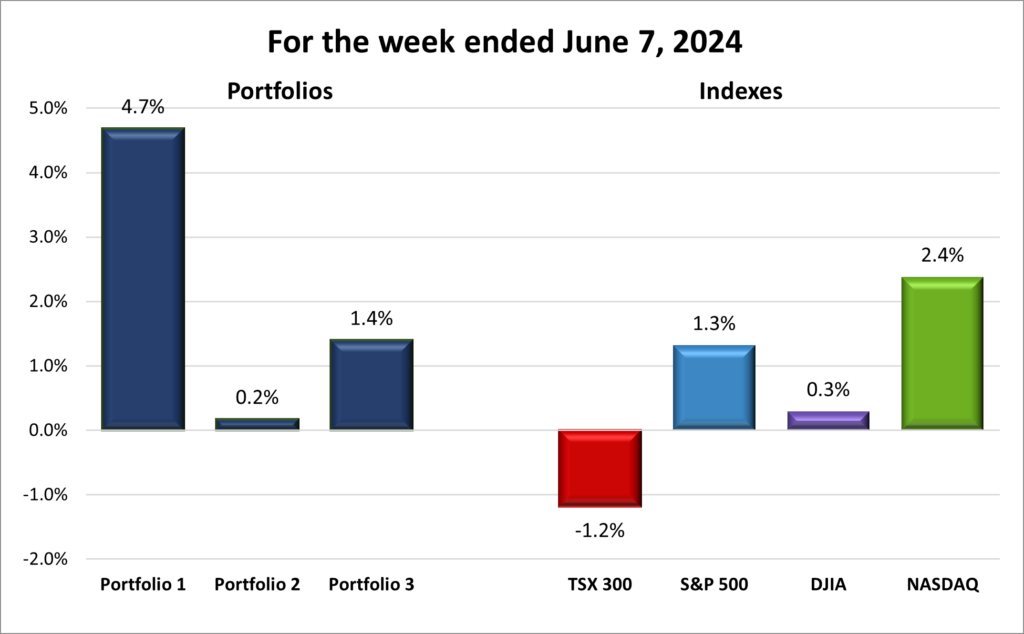

For the week, the TSX (SPTSX) slipped 1.2%, the S&P 500 (SPX) rose 1.3%, the DJIA (INDU) inched higher 0.3% and the Nasdaq (CCMP) gained 2.4%.

| Index | Weekly Streak |

| TSX: | 3 – week losing streak |

| S&P: | 1 – week winning streak |

| DJIA: | 1 – week winning streak |

| Nasdaq: | 1 – week winning streak |

![]() June started off on a positive note with the Nasdaq and S&P posting solid gains, and the DJIA also finishing in the win column. Unfortunately, the TSX slid lower, as illustrated in the chart above.

June started off on a positive note with the Nasdaq and S&P posting solid gains, and the DJIA also finishing in the win column. Unfortunately, the TSX slid lower, as illustrated in the chart above.

In Canada, the BoC became the first G7 central bank to lower its interest rate, giving the TSX a mid week boost. Later in the week, the European Union’s central bank followed suit. Canadian and American labour reports also played a significant role. On Friday, stronger-than-expected Canadian labour data possibly postponed a second interest rate cut in July. On the same day, mixed US jobs data weighed on the TSX, reversing gains from earlier in the week and ensuring a weekly loss.

In the US, the three major indexes carried over the previous week’s momentum and moved into positive territory early following two favorable labour reports. They maintained this upward trend until Friday’s third labour report of the week, which showed more jobs and accelerating wage gains but also higher unemployment, stalling their progress. This has led many investors to believe this has increased the chances the Fed could leave the rate at 5.5% for the next several months.

The price of oil continued its downward trend that began in early April. However, analysts predict it should rebound later this summer, which is encouraging news for the energy sector and those investors holding oil stocks.

Overall, it was a decent week in the North American markets and a good way to start the new month. The interest rate cuts in Canada and the European Union, along with signs of a slowing US economy, provided mostly positive news. Next week, all eyes will be on the Fed’s Federal Open Market Committee meeting to get a sense of when and how much the Fed plans to lower interest rates over the next six months. Hopefully, we will get favourable news and see the markets respond positively. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week winning streak |

| Portfolio 2: | 1 – week winning streak |

| Portfolio 3: | 1 – week winning streak |

![]() It was great to see all three portfolios rebound this week after they all ended lower last week. As shown in the chart below, all three posted weekly gains, with Portfolio 1 leading the pack with an impressive 4.7% increase.

It was great to see all three portfolios rebound this week after they all ended lower last week. As shown in the chart below, all three posted weekly gains, with Portfolio 1 leading the pack with an impressive 4.7% increase.

Portfolio 1 was the standout performer, surpassing not only the other two portfolios but also all four major indexes. While no stocks experienced significant (more than 10%) gains or losses, the majority advanced. Nvidia gave the portfolio a sizable boost, rising over $75.08 per share, and Costco (NASD: COST) added over $34 per share. To top it off, Nvidia executed a 10-for-1 stock split following Friday’s close.

Portfolio 2 lagged well behind the other two but still outperformed the TSX. Although MongoDB (NASD: MDB) continued its downward trend, its descent was not as steep as the previous week.

Portfolio 3 had a much better week compared to last. Most stocks in this portfolio gained value, although Lithium Americas (TSE: LAC) did drop by 10%.

Overall, it is great to see all three portfolios bouncing back into the weekly win column. Fingers crossed that the Fed leaves the door open for a September rate cut next week, so we can look forward to two-week winning streaks! 😊

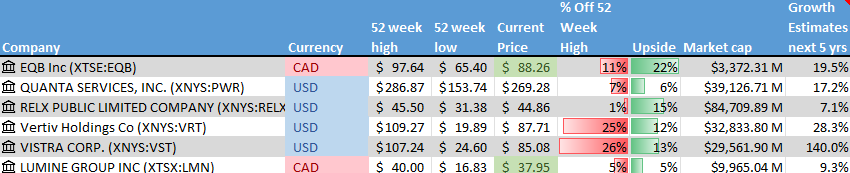

Companies on the Radar

This past week, Vistra Corp (NYSE: VST) caught my attention. Vistra is an American Fortune 500 company operating in the integrated retail electricity and power generation sector. They provide reliable and affordable electricity to customers in several US states, and they own and operate numerous power generation facilities across the country. On top of that, the company is making significant strides towards a cleaner energy future with growing investments in renewables.

This past week, Vistra Corp (NYSE: VST) caught my attention. Vistra is an American Fortune 500 company operating in the integrated retail electricity and power generation sector. They provide reliable and affordable electricity to customers in several US states, and they own and operate numerous power generation facilities across the country. On top of that, the company is making significant strides towards a cleaner energy future with growing investments in renewables.

What makes Vistra particularly interesting is their dual advantage. Not only can they benefit from the shift to renewable energy, but they can also capitalize on the huge demand for clean power driven by the growth of data centers providing AI services.

Vistra joins the five other companies, listed below, on my radar list.

- Equitable Bank (TSE: EQB), a mid sized Canadian bank, considered Canada’s 7th bank, that provides financial services to consumers and businesses.

- Quanta Services, Ltd. (NYSE: PWR), a large-cap American company offering a wide range of specialty infrastructure solutions throughout the world

- RELX PLC (NYSE: RELX), provides information-based analytics and decision tools for professional and business customers worldwide.

- Vertiv Holdings (NYSE: VRT), an American company that designs and builds infrastructure and continuity solutions to businesses around the world.

- Lumine Group (TSE: LMN), a young Canadian mid sized company that acquires communications and media software companies, and then strengthens and grows those companies.

Please keep in mind that these are only companies that have piqued my interest. This is not a recommendation or financial advice. You should do your own research or contact a professional before making any investment decisions.

The Radar Check was last updated June 7, 2024.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended June 7, 2024: UP ![]()

- Alphabet’s Google unit plans to layoff over 100 employees across several roles in their cloud computing unit.

In other Google news, the United Kingdom’s (UK) Competition Appeal Tribunal (CAT) ruled the company must face a mass lawsuit that accuses it of abusing its dominant position in online advertising. The lawsuit is seeking damages worth up to US$ 17.4 billion for website and app publishers in the UK. Naturally, Google rejects the claim.

In the US, Google was able to convince a US judge to dismiss a proposed class action lawsuit claiming the company misused personal and copyrighted information to train its chatbots.

Alphabet has a new Chief Financial Officer (CFO). Anat Ashkenazi joins Alphabet from Eli Lilly (NYSE: LLY) where she was the CFO. Alphabet’s previous CFO has moved over to the role of Chief Investment Officer. - Berkshire Hathaway’s (NYSE: BRK.B) power utility company PacifiCorp has agreed to pay US$ 178 million to resolve the claims that resulted from wildfires in Oregon in 2020.

Elsewhere in the Berkshire universe, their BHE Renewables unit has entered into a joint venture with Occidental Petroleum (NYSE: OXY) to extract lithium. Occidental would extract the lithium from the earth and BHE Renewables would produce high grade lithium at their geothermal facility in California. Side note: Berkshire Hathaway, the parent of BHE, owns 27% of Occidental. - Nvidia continues its climb to become the most valuable company in the world. The rise in share price has lifted the company over the US$ 3 trillion mark and past #2 Apple (NASD: AAPL).

- Amazon.com’s robotaxi unit Zoox announced they plan to start testing their autonomous vehicles in Austin, TX and Miami, FL. Zoox uses customized Toyota Highlanders with human safety drivers. They will be used in small areas near the business and entertainment areas of each city. This follows ongoing tests in California and Nevada.

In other Amazon news, the company is being sued for US$ 1.3 billion by the British Independent Retailers Association (BIRA), claiming Amazon misused BIRA members data to further their own profits. - Walmart (NYSE: WMT) is replacing all of its paper shelf price labels with digital shelf labels. Weekly updates that took an employee two days to complete will now be done in two minutes

Activity

Bought: TD Investment Savings Account (TSE: TDB8150) (ISA) I initially planned to purchase a 1-year cashable Guaranteed Income Certificate (GIC) with a 3.55% interest rate to hold some excess cash for potential short-term needs. However, when I called TD Direct Investing, the rep informed me about TD Investment Savings Accounts (ISA) offering an interest rate of 4.55%.

The rep explained that ISAs are similar to mutual funds in that they can be bought and sold online through TD Direct Investing, but they have no management fees, no back or front-loaded fees, and no penalties for early withdrawal. In my case, the ISA not only provided a higher return but also offered more flexibility since I could sell anytime without penalty. Plus, my investment would be insured by the Canada Deposit Insurance Corporation (CDIC) in case of bank failure.

I repeatedly asked about any hidden catches, but the rep assured me there were none. The only potential downside is the variable interest rate, which could change with the BoC’s benchmark rate. However, even if the rate drops by 0.25%, matching the recent cut by the BoC, the return would still be 4.30%, still better than the GIC I was considering. Moreover, I could always move the cash if a better option came along.

With this information, I decided to park the cash in an ISA, where it would work harder for me than in a GIC.

Note that TD’s ISA tickers do not show up on Yahoo! Finance or MSN Money but are available on TD Direct Investing’s WebBroker. For more details on TD ISAs, click here. If you do not use TD Direct Investing, other Canadian banks likely offer comparable products. If you have a third-party trading account, check with them to see if they provide access to these or similar products.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

No C$ dividends this past week.

US $

Visa Inc. (NYSE: V)

Quarterly Reports

CrowdStrike Holdings, Inc.

First quarter 2024 financial results on June 4, 2024

Portfolio 2

Portfolio 2 for the week ended June 7, 2024: UP ![]()

- Microsoft is joining Google in trimming hundreds of employees in their Azure cloud computing division.

The US Department of Justice (DOJ) and the Federal Trade Commission (FTC) have struck a deal that will see them to initiate antitrust investigations into Microsoft, OpenAI and Nvidia regarding their dominant roles in the rapidly growing AI industry. The DOJ will take the lead against Nvidia, while the FTC will have the lead against Microsoft and OpenAI. - MongoDB hit its lowest close in over a year this past week. Along the way the stock set a number of records, including longest losing streak on record (Based on available data back to Oct. 19, 2017), and worst 11 day stretch on record (Based on available data back to Oct. 19, 2017). Those are records I would rather not hold. ☹

- TC Energy (TSE: TRP) shareholders voted to split off the company’s liquids pipeline business. The new company will be called South Bow Corp, and their assets include the Keystone oil pipeline that moves crude oil from Alberta to the US Midwest and South. The spin off will allow TC Energy to reduce its debt and focus on shipping natural gas.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Fortis (TSE: FTS)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended June 7, 2024: UP ![]()

- goeasy (TSE: GSY) announced their loan portfolios has surpassed C$ 4 billion in gross balances and they anticipate successfully meeting their goal of a $4.55 billion loan portfolio by the end of the year.

- TD Bank (TSE: TD) was in the news again. Once again, not for a good reason. A branch employee in Florida has been accused of accepting bribes to move millions of dollars to Columbia. This is another instance of where TD’s anti money laundering practises fell short.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.