Market meltdown

This past week began on a shaky note. Weak economic data and disappointing corporate earnings from the previous week fueled fears of a potential recession in the US, the world’s largest economy. A recession—a period of significant economic slowdown marked by declining business profits, rising unemployment, and reduced consumer spending—can spark widespread anxiety. This unease led to a sharp selloff on Monday, starting in Japan and sweeping westward through European markets before hitting North America. By the end of the day, the S&P 500 (S&P) saw its biggest drop in nearly two years, the Dow Jones Industrial Average (DJIA) plunged by 1,000 points, and the tech-heavy Nasdaq Composite index (Nasdaq) recorded its worst start to a month since 2008. The Canadian market, fortunately, avoided the chaos, as it was closed during the selloff.

By Tuesday, experienced investors were suggesting that the sharp decline was more about panic than fundamentals. They believed fears of an imminent downturn were likely overstated, leading to a market recovery by the end of the session, with all three major indexes closing higher.

Reflecting on similar market turmoil from 2020 at the start of the pandemic, I understand the anxiety many new investors are feeling. Back then, despite the urge to sell, I chose to hold onto my stocks, and I am grateful I did. The markets rebounded strongly in 2020 and 2021.

The key lesson from that experience is to stay calm and avoid knee-jerk reactions. Watching your investments drop sharply can be distressing, but panicking and selling is often the worst response. By focusing on the long term—understanding that a time horizon of several years or even decades can smooth out short-term fluctuations—and remembering that markets do recover, Monday’s turbulence felt more manageable.

Looking ahead, analysts predict continued market volatility until September, when the Fed is expected to cut interest rates. This means we might experience more ups and downs on this roller-coaster ride. The key strategy is to stay calm and stick to your investment plan. Use this turbulence as an opportunity to pick up shares of solid companies at a discount when prices drop.

For tips on managing anxiety during market downturns, check out ‘When the Market Falls…’ below.

Besides the volatile start to the week, let’s see what else unfolded over the past few days…

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, When the market falls…, What I learned, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

BoC meeting minutes

Following their June decision to cut rates, the BoC’s Governing Council next met on July 24th to once again review the nation’s monetary policy. Following this meeting, they opted to lower the benchmark interest rate by another 0.25%, down to 4.5%. This adjustment reflects their ongoing strategy to navigate the economic landscape while bringing inflation down to their target of 2%.

Globally, the economic outlook remains steady, with growth expected to hover around 3%. Major economies are seeing inflation gradually ease towards their central bank targets. In the US, signs of a slowing economy are emerging, marked by reduced consumer spending and a cooling job market. Despite this, there is a concern that consumption might rebound unexpectedly. While inflation in the US trends downward, certain service sectors still see stubborn price pressures. Meanwhile, the exchange rate between Canada and the US has stayed stable since the last rate adjustment.

At home, after a sluggish second half of 2023, Canadian GDP growth rebounded in early 2024. Although growth is expected to remain positive, it is subdued, driven largely by high immigration. However, on a per capita basis, GDP has seen a decline. Uncertainty around population growth makes it tricky to forecast future GDP growth. Consumer spending is projected to improve in 2025, even with slower population growth. Unemployment has risen to 6.4%, with slack in the labour market due to immigration outpacing job creation. Wage growth is above 4%, which, despite slowing productivity, fuels inflationary concerns. Yet, inflation has cooled to within the Bank’s target range of 1% to 3% and is expected to drop to 2% by late 2025.

After reviewing the current economic landscape, the Council shifted their focus to the future of economic growth. While higher interest rates have helped ease inflation, they are also unveiling new risks. Economic growth is currently trailing behind population growth, creating excess supply and slack in the labour market. High interest rates are dampening consumer spending, and while spending might bounce back as rates decline, high mortgage costs could pose risks for consumer spending into 2025 and 2026. The housing market also faces potential challenges from high demand and slow construction, which could push rents higher. Although inflation in wage-sensitive services remains a concern, its overall impact on inflation may be limited.

Prior to their June meeting, the Council had been primarily focused on bringing inflation down. With inflation trending towards their target, the Council is now carefully balancing the risks of both rising and falling inflation as they navigate these uncertain economic conditions.

Labour Force Survey (LFS)

Canada’s latest Labour Force Survey from Statistics Canada reveals a mixed picture for July. The economy shed 2,800 jobs in July, following a loss of 1,400 in June, defying analysts’ expectations for a gain of 22,500 jobs. This marks the third consecutive month of virtually flat employment. On a positive note, employment is up 1.7% year-over-year.

Breaking it down further, private sector jobs fell by 0.3% in July but saw a 0.6% increase over the past year. Public sector employment, however, climbed 0.9% monthly and 4.8% annually. Self-employment held steady for the month and grew by 2.1% year-over-year.

Sector-wise, the biggest monthly boost was in ‘Utilities,’ which saw a 4.2% increase, while ‘Wholesale and retail trade’ experienced a 1.5% decline. Annually, ‘Natural Resources’ led with a 9.2% job increase, whereas ‘Agriculture’ saw the largest decrease, down 9.3%.

The unemployment rate remained steady at 6.4%, matching June’s rate and its highest level since January 2022. Analysts had anticipated a rise to 6.5%. The stable unemployment rate, despite the rising population, suggests the economy is struggling to keep pace with workforce growth.

In July, annual wage growth slowed to 5.2%, down from 5.4% in June. As the job market weakens and unemployment rises, wage growth is expected to continue slowing. This cooling trend in wages may help alleviate some inflationary pressures.

The decline in private sector jobs alongside rising public sector employment is concerning. Private sector jobs are vital for economic growth and innovation, and their drop may indicate a slowdown in these areas. Moreover, increasing public sector jobs could lead to higher government spending, potentially resulting in larger budget deficits and growing public debt, which could strain fiscal resources and impact long-term economic stability.

Overall, despite adding jobs over the past year, the recent trend of stagnant employment and rising unemployment raises concerns about the country’s ability to keep up with population growth. With no major surprises in this report, the combination of flat employment, declining inflation, and a sluggish economy have left the door open for the BoC to lower interest rates by another 0.25% at their next meeting on September 4.

Canadian market volatility

In the past week, Canada’s Volatility Index (CVIX) experienced a dramatic swing. It surged from 18.48 at the end of the previous week to a high of 23.56, before settling at 15.79—an overall drop of over 14%. This spike was largely due to investor overreaction to a recent US labour report, which hinted at a slowing economy. However, as the dust settled, investor sentiment calmed, and the CVIX returned to a more balanced level. This volatility could have ripple effects on Canada’s own economic landscape.

Tracked as the VIXI on the Toronto Stock Exchange (TSE), the CVIX gauges expected market volatility. A reading below 10 indicates a calm and stable market, while a reading between 10 and 20 reflects moderate volatility and normal market fluctuations. Readings above 20 suggest high volatility and significant market uncertainty. With the CVIX currently at 15.79, it signals a market environment with somewhat elevated volatility but not extreme, reflecting a cautious yet not panicked investor sentiment.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

American market volatility

The CBOE Volatility Index (VIX), known as the market’s “fear gauge,” soared to a high of 65.73 before the markets opened on Monday, a dramatic leap from the previous Friday close of 23.39. However, the VIX pulled back to close at 38.57, marking its highest one-day spike and peak since October 2020. Despite this sharp increase, the VIX ended the week at 20.37, reflecting an overall decline of almost 12% from the previous week. This marks the second consecutive week the VIX has closed above 20, following a period of being in the teens since last October.

The initial spike was fueled by investor anxiety over weaker-than-expected labour data from the previous week, raising concerns about a potential recession. However, reassuring comments from a member of the Fed and other experienced, professional investors helped temper these fears, bringing the VIX down to a more moderate level.

The VIX measures expected market volatility over the next 30 days. Readings below 12 suggest a calm and stable market, while values between 12 and 20 indicate normal fluctuations. Levels between 20 and 30 signal heightened volatility and uncertainty, and readings above 30 reflect extreme stress, often seen during crises. The recent rise in the VIX indicates increased market tension and suggests that investors are bracing for more volatile conditions ahead.

When the market falls…

A market selloff like the one we experienced at the start of the past week can be particularly daunting for new investors, shaking your confidence and raising questions about your investments. Understanding how to navigate these challenging periods is crucial. Here are some strategies to help you stay steady and make informed decisions during market turbulence.

- Stay calm. It is natural to feel anxious when the market drops sharply. However, reacting emotionally can lead to poor decisions and unnecessary losses. Investing is generally about long-term growth, and short-term market fluctuations are a normal part of the process. Instead of panicking, take a step back, assess the situation calmly, and remember that these dips are part of the journey. Staying patient and calm will help you make more informed choices.

- Understand Market Cycles: Markets naturally go through ups and downs. History shows that they recover from downturns, sometimes the next day others take longer and can take several months. Do not be tempted to try and time the market—predicting its highs and lows is challenging even for experts. By focusing on the long term, you will be better prepared to handle these fluctuations, knowing that recovery is part of the market’s rhythm.

- Review Your Portfolio: Check if the fundamentals of your investments have changed or if the sell-off is more about market sentiment. Focus on the quality of your investments rather than short-term price changes. A well-diversified portfolio of high-quality companies can help reduce losses, so consider rebalancing it to stay aligned with your long-term goals. Make sure your investment strategy reflects your comfort level with market fluctuations.

- Stick to Your Plan: Revisit your investment goals and strategy. If you have a well-thought-out investment plan based on your risk tolerance and financial objectives, stick with it. Avoid making hasty adjustments based solely on short-term market movements.

- Consult a Financial Advisor: If you are unsure how to navigate a market sell-off, consider consulting a financial advisor. Not only can they offer guidance tailored to your financial situation and goals, but also help build your investing knowledge and confidence.

Although watching your investments drop in value can be tough, remember that market selloffs can offer golden opportunities for long-term investors. A market dip often means you can acquire high-quality stocks at discounted prices. If your financial situation permits, this might be the perfect time to invest in companies you believe in at lower prices, potentially setting the stage for future gains.

By keeping these principles in mind, you can better manage your reactions and make more informed decisions during market downturns.

What I learned this week

Fractional shares

This past week, TD’s Direct Investing and Easy Trade services introduced fractional shares, enabling investors to buy partial shares instead of whole ones. This allows you to invest a specific dollar amount and receive a fraction of a share, rather than rounding down to the nearest whole share. For instance, with a $200 investment in TD (TSE: TD), trading at C$78.36 at the close of this week, you would receive approximately 2.55 shares instead of 2 full shares with some cash left over.

Fractional shares enhance your ability to diversify and balance your portfolio by giving you access to stocks and Electronically Traded Funds (ETFs) at various price points. While you can still trade whole shares if you prefer, fractional shares offer more flexibility in managing your investments. Dividends for fractional shares will be prorated based on the portion you own.

Like whole shares, you can buy and sell fractional shares in real-time trades during market hours, and dollar-based orders can be placed only when the market is open. The addition of this capability simplifies investing, making it easier to access a wider range of securities in both Canadian and US markets.

Although I have not tried it yet, fractional shares mean that rather than needing approximately C$4,000.00 to buy one full share of Constellation Software (TSE: CSU), I could gradually build up to a single share and beyond.

For more on fractional shares, check out the June 7 Weekly Update.

Carry trades

Prior to this past week, I had never heard the term ‘carry trade.’ However, given its role in Monday’s market meltdown, I decided it was time to learn more. Essentially, a carry trade is a strategy that capitalizes on the interest rate differential between currencies or asset.

Here is how it typically works:

- Borrowing in Low-Interest Currency: Investors borrow funds in a currency with a low interest rate, such as the Japanese yen.

- Investing in High-Interest Assets: They then invest these borrowed funds in assets or currencies that offer higher interest rates or returns, such as government bonds, higher-yielding currencies, or stocks.

- Earning the Carry: The profit comes from the difference between the low cost of borrowing and the higher returns on the investments. For example, if you borrow at an interest rate of 1% and invest in an asset yielding 5%, you earn a 4% carry.

Key Points:

- Interest Rate Differential: The success of a carry trade largely depends on the interest rate differential between the borrowing and investment currencies.

- Exchange Rate Risk: If the value of the currency you borrowed strengthens significantly, it can reduce or even negate the profits from the carry trade due to the increased cost of repaying the loan in that stronger currency.

- Market Conditions: Carry trades are highly sensitive to changes in market conditions and investor sentiment. When financial stress increases, or if the value of higher-yielding assets drops or borrowing costs rise, these types of trades can quickly turn unprofitable. This shift can lead to substantial losses or even trigger a market sell-off, as was evident last Monday.

Example: Imagine you borrow yen at 0.5% and invest in American bonds yielding 3%. The 2.5% difference is your potential profit from the carry trade. It is like getting paid to move money from a low-interest account into a high-yield one!

Weekly Market Review

Monday: the selloff that began on Thursday intensified today as the S&P, the DJIA, and the Nasdaq all dropped more than 2.5%. Last week’s lower than expected jobs data has investors concerned the Fed may have waited to long to start lowering the US interest rate. The sell off spread across the globe, dragging other markets down with the American market.

In Canada, the markets were closed for a Civic Holiday, thus avoiding today’s carnage. I suspect the Toronto Stock Exchange Composite Index (TSX) will join in the selloff tomorrow.

In the US, the DJIA fell over 1,000 points, the S&P is off to its worst start of a month since 2002, and the Nasdaq is now down almost 8% since the start of the month. The Nasdaq and S&P closed at their lowest levels since early May. Not surprisingly, all sectors ended lower today. Industrials fell the least while Technology had the biggest plunge.

Tuesday: the Monday panic selling appears to be over for the American indexes as all finished in the green, snapping a three-session losing streak. Meanwhile, the TSX, which missed yesterday’s selloff, did not want to miss the fun, and ended in the red. The price of oil rose on concerns of lower oil supplies.

In Canada, after a 3-day long weekend, the TSX fell to its lowest point at the start of the day before clawing back some of the losses as investors started picking up bargains from the pile of beaten down stocks. In trading, Telecommunications Services was the only sector to advance, while Basic Materials (miners and fertilizer manufacturers) declined the most.

In the US, indexes initially surged but lost ground by the end of the day. However, comments from a Fed official, signaling that the Fed was ready to take action if the economy weakened further, helped ease investor worries. All sectors finished the day in positive territory, with the Financials sector leading the way, while the Energy sector lagged behind.

Wednesday: the indexes started the day in positive territory before all four fell into negative territory by the end of the day. With little economic news and no comments from the Fed, concerns about a possible US recession continue to weigh on investors. The price of oil rose for the second straight day as investors grew concerned about declines in American crude oil stockpiles.

In Canada, the TSX stretched its losing streak to 4 days. in trading, the Technology sector was the top performer, while Basic Materials was the worst performer.

In the US, technology stocks initially lifted the indexes but later dragged them down as investors sought safer assets. The S&P 500 experienced its largest single-day swing in over two years, shifting from a notable gain to a significant loss by the close. Among the sectors, Utilities saw the biggest gain, while Consumer Staples faced the largest decline.

Thursday: all four indexes moved strongly upward following the US weekly jobless claims which dropped more than anticipated, reassuring investors that the economy may not be as bad as they feared. Oil prices continued to rise as a result of the better-than-expected weekly jobs report and ongoing tensions in the Middle East.

In Canada, the TSX rode the upward momentum from the US labour news to close at its highest level in six months. In trading, all sectors finished in the green, led by Healthcare while Utilities brought up the rear.

In the US, the S&P had its best single day since November 2022 as investors moved back into stocks, particularly technology companies. In trading, all sectors ended higher, led by Technology with Utilities trailing the pack.

Friday: the indexes wobbled throughout the day but managed to close higher, ending the week close to where they started. Thursday’s US labour report eased investors’ concerns, leading to a return to the markets. Additionally, rising tensions in the Middle East drove oil prices up, marking the first weekly gain for oil since early July.

In Canada, the TSX rose on higher oil and commodity prices. In trading on Bay Street, Basic Materials gained the most while Utilities dropped the farthest.

In the US, the three indexes bounced above and below the baseline for most of the morning before heading upward in the afternoon. In trading, Telecommunications Services advanced the most while Basic Materials was the only sector to end lower.

Weekly Market and Portfolio Review

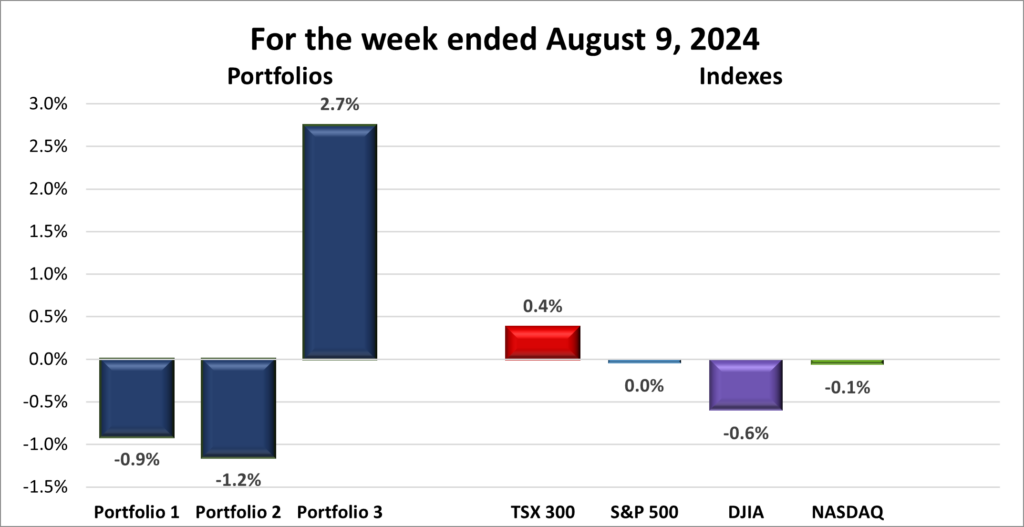

For the week, the TSX (SPTSX) gained 0.4%, the S&P 500 (SPX) was essentially flat slipping 0.04%, the DJIA (INDU) fell 0.6% and the Nasdaq (CCMP) declined 0.1%.

| Index | Weekly Streak |

| TSX: | 1 – week winning streak |

| S&P: | 4 – week losing streak |

| DJIA: | 2 – week losing streak |

| Nasdaq: | 4 – week losing streak |

![]() The week kicked off with a dramatic plunge, setting the stage for a turbulent few days as the indexes struggled to recover. Despite the rocky start, the TSX managed to gain ground, buoyed by rising energy and commodity prices, while the S&P 500 recouped much of its initial losses. The Nasdaq experienced significant volatility, with daily swings of 1% or more before ending close to where it began the week. The DJIA, too, ended lower but recovered a substantial portion of its early-week losses.

The week kicked off with a dramatic plunge, setting the stage for a turbulent few days as the indexes struggled to recover. Despite the rocky start, the TSX managed to gain ground, buoyed by rising energy and commodity prices, while the S&P 500 recouped much of its initial losses. The Nasdaq experienced significant volatility, with daily swings of 1% or more before ending close to where it began the week. The DJIA, too, ended lower but recovered a substantial portion of its early-week losses.

Monday’s market meltdown was fueled by a series of impactful events. News that the world’s greatest investor, Warren Buffet, had sold US $ 75.5 billion worth of stocks, including half of his Apple shares, and built-up cash caused investors to wonder if they should follow suit. This came amid a broader shift away from technology stocks, pushing the Nasdaq into a market correction of over 10% within three weeks. The previous week’s disappointing US labour report heightened fears of a potential recession, further amplifying investor anxiety, and prompting a wave of profit-taking.

Compounding the chaos was the unwinding of carry trades. Investors, particularly hedge funds, had borrowed cheap yen to invest in higher-yielding assets like US technology stocks. However, a surprise interest rate hike by the Bank of Japan strengthened the yen, diminishing the profitability of these trades and prompting a sell-off of riskier assets to cover losses. This, in turn, intensified the market declines.

On Monday, the S&P 500 and DJIA experienced their largest daily losses since September 2022, with technology stocks bearing the brunt of the sell-off. The Magnificent Seven tech giants alone lost $800 billion in value. The global sell-off began with Japan’s Nikkei 225, which plunged 12%—its steepest one-day drop since 1987—and spread to major exchanges worldwide, including the London Stock Exchange.

This week highlighted how emotions can drive market movements, particularly when investor sentiment is high. Weak economic data led to profit-taking and a panic-driven sell-off, which evolved into a week of significant volatility. Fortunately, the week ended with some stability, providing a reminder of how swiftly market conditions can change. Here is hoping the upward momentum from the last two days carries into the upcoming week, and we experience a bit less ‘excitement’ ahead. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 4 – week losing streak |

| Portfolio 2: | 2 – week losing streak |

| Portfolio 3: | 1 – week winning streak |

![]()

![]() Given the market’s rocky start on Monday, I anticipated a challenging week, and indeed, two of the three portfolios ended lower, as shown in the chart below. However, one portfolio exceeded expectations with a solid weekly gain, outpacing all four indexes.

Given the market’s rocky start on Monday, I anticipated a challenging week, and indeed, two of the three portfolios ended lower, as shown in the chart below. However, one portfolio exceeded expectations with a solid weekly gain, outpacing all four indexes.

Portfolio 1 dropped in value despite 60% of its holdings posting weekly gains. While there were no significant losses, several stocks saw impressive increases. After hitting a 52-week low on Monday morning, Nvidia (NASD: NVDA) bounced back with a 13% gain for the week. Other notable performers included Trade Desk (NASD: TTD) up 27%, Shopify (TSE: SHOP) up 25%, CrowdStrike (NASD: CRWD) and Sea Ltd (NYSE: SE) both up 17%, Docebo (TSE: DCBO) up 13%, and Datadog (NASD: DDOG) and Cloudflare (NYSE: NET) both up 11%.

Despite these gains, the portfolio’s overall value decreased. Initially, this was puzzling. On closer inspection, I found that the share prices at the end of the previous week were significantly higher than their Monday opening prices. For example, Nvidia closed the previous week at $107.27 but opened Monday at $92.63 and ended the week at $104.70.

I calculate weekly gains based on the Monday opening price and the Friday closing price, which showed a 13% gain. However, comparing the previous Friday’s close to this past Friday’s close reveals a 2% loss. This discrepancy highlights why Portfolio 1 lost value despite strong weekly performances—sometimes the surface gains do not tell the whole story.

Portfolio 2 had the weakest weekly performance among the portfolios, despite 60% of its stocks showing gains. iA Financial (TSE: IAG) led with a solid 10% increase, but this wasn’t enough to counteract the losses in the portfolio. Mitek Systems (NASD: MITK) suffered a substantial 25% decline, and although Airbnb (NASD: ABNB) didn’t post a significant weekly loss, hitting a 52-week low didn’t help.

Portfolio 3 had a relatively decent week despite a rocky start. Although only 45% of the holdings increased in value, Shopify and Cloudflare led with notable gains, as mentioned earlier. However, the portfolio faced challenges from Telus International (TSE: TIXT), which dropped 36%, and Lithium Americas (TSE: LAC), which declined by 11%.

Looking at the portfolios, it appears that having the majority of stocks post weekly gains does not always translate to an overall increase in portfolio value. ☹ Nonetheless, seeing most holdings with positive weekly performance is still preferable. Hopefully, the upward momentum we saw at the end of the week will carry into the next, leading to more companies advancing in each portfolio and a rise in overall portfolio values. 😊

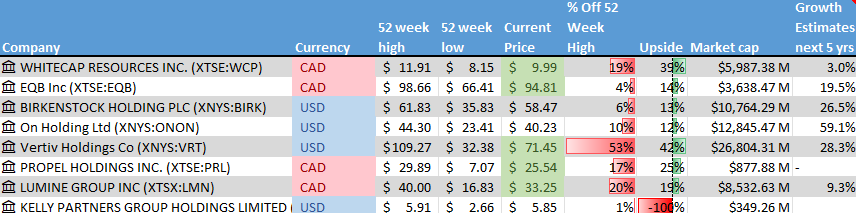

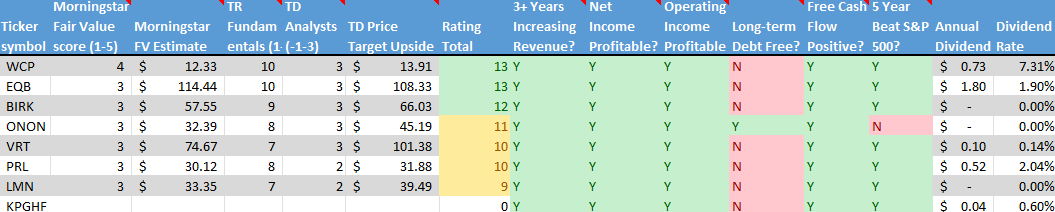

Companies on the Radar

Last week, I mentioned that my radar was packed with six companies, and I aimed to trim the list down to five or fewer. However, this past week, I could not resist adding two more interesting names to the mix.

Last week, I mentioned that my radar was packed with six companies, and I aimed to trim the list down to five or fewer. However, this past week, I could not resist adding two more interesting names to the mix.

First up is Propel Holdings (TSE: PRL), a small-cap Canadian company with a market value under $2 billion. They specialize in providing credit to individuals who cannot access traditional financial institutions like banks.

Next up is Whitecap Resources (TSE: WCP), a medium-cap Canadian oil and gas company. After a sluggish July, oil prices have recently started to climb, making Whitecap an intriguing prospect. The company offers an attractive dividend yield of over 7% per month, which has been steadily growing. The potential for monthly cash flow combined with the possibility of share price appreciation if oil prices continue to recover makes Whitecap a compelling investment opportunity. 😊

So, despite my initial plan to narrow down the list, it is now grown to eight companies. Looks like I will need to make some tough decisions to trim it down to a more manageable number.

- Equitable Bank (TSE: EQB), a mid sized (when the number of outstanding shares times the shares prices is between $2 billion to $10 billion) Canadian bank, considered Canada’s 7th bank, that provides financial services to consumers and businesses.

- Birkenstock Holding plc (NYSE: BIRK), a medium cap British company that has been making shoes since 1774.

- On Holding AG (NYSE: ONON), a medium cap Swiss company, founder-run, sports products company.

- Vertiv Holdings (NYSE: VRT), a large American company that designs and builds infrastructure and continuity solutions to businesses around the world.

- Lumine Group (TSE: LMN), a young Canadian mid sized company that acquires communications and media software companies, and then strengthens and grows those companies.

- Kelly Partners Group (OTCM: KPGHF), a small Australian accounting firm that is growing through serial acquisition of other small accounting firms in Australia. They have recently expanded into the USA and other English-speaking countries.

Please keep in mind that these are only companies that have piqued my interest. This is not a recommendation or financial advice. You should do your own research or contact a professional before making any investment decisions.

The Radar Check was last updated August 9, 2024.

NOTE: Morningstar and Thomson-Reuters analysis is unavailable for Kelly Partners Group most likely because it is a small-cap Australian company with a market value of less than US$360 million and primarily listed on the Australian Stock Exchange. While you can invest in Kelly Partners through the Over-the-Counter Market (OTCM) here in North America, the analysis is not as readily available as it is for companies on major North American exchanges like the Toronto Stock Exchange, New York Stock Exchange, and Nasdaq.

Unlike other non-North American companies I have researched, Yahoo! Finance had no information under the Analysis tab for Kelly Partners. This lack of data meant I could not access any ratings during my routine radar check.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended August 9, 2024: DOWN ![]()

- Alphabet’s (NASD: GOOGL) was ruled to have engaged in illegal practices to maintain it search engine monopoly. A federal judge ruled the company used its dominant market position to eliminate competitors and paid billions of dollar to become the default search engine of smartphones and web browsers.

- Berkshire Hathaway (NYSE: BRK.B) seems to have gone defensive and built up its cash pile to US$ 276.9 billion, as of June 30, from what was then a record US$ 189 billion at the end of April. To build up its stockpile of cash, the company sold half of its Apple (NASD: AAPL) shares.

- CrowdStrike (NASD: CRWD) has firmly denied Delta Air Lines’ (NYSE: DAL) allegation that it should be held responsible for the flight disruptions caused by a global outage on July 19, which was linked to a faulty update. CrowdStrike contends that their CEO reached out to a Delta board member within four hours of the incident, and their Chief Security Officer directly contacted Delta’s Chief Information Security Officer. CrowdStrike also claims that they offered help, which Delta chose to ignore or decline. Additionally, CrowdStrike asserts that its liability is limited by contract to “single-digit millions,” not the hundreds of millions Delta is seeking.

- TMX Group (TSE: X) announced they have acquired news release service company Newsfile Corp., a private company that provides news release distribution and regulatory filings services. TMX is the operator of many of the Canadian stock exchanges, including the Toronto Stock Exchange. This acquisition bolsters the services TMX can provide the companies that list on their exchanges.

- Britain’s anti trust regulator, the Competition and Markets Authority (CMA), announced they were investigating Amazon’s (NASD: AMZN) relationship with artificial intelligence (AI) startup Anthropic. The CMA has until October 4 to either clear the companies of anti competition concerns or refer the case for a deeper investigation. Both companies claim their relationship does not create any competition concerns. This will be a tough case for the CMA as they are already investigating Alphabet’s Google and Anthropic for the same reason. With Anthropic working with both technology juggernauts, it would appear hard any of the three companies are being anti competitive.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

No C$ dividends this past week.

US $

Costco Wholesale Corp (NASD: COST)

Quarterly Reports

Navitas Semiconductor Corporation

Second quarter 2024 financial results on August 5, 2024

Innovative Industrial Properties, Inc.

Second quarter 2024 financial results on August 5, 2024

Rivian Automotive, Inc.

Second quarter 2024 financial results on August 6, 2024

Celsius Holdings, Inc.

Second quarter 2024 financial results on August 6, 2024

Magnite, Inc.

Second quarter 2024 financial results on August 7, 2024

Crew Energy Inc.

Second quarter 2024 financial results on August 7, 2024

Shopify Inc.

Second quarter 2024 financial results on August 7, 2024

GDI Integrated Facility Services Inc.

Second quarter 2024 financial results on August 7, 2024

Datadog, Inc.

Second quarter 2024 financial results on August 8, 2024

The Trade Desk, Inc.

Second quarter 2024 financial results on August 8, 2024

Formula 1 Group (Liberty Media)

Second quarter 2024 financial results on August 8, 2024

indie Semiconductor, Inc.

Second quarter 2024 financial results on August 8, 2024

Docebo Inc.

Second quarter 2024 financial results on August 8, 2024

Atlanta Braves Holdings, Inc.

Second quarter 2024 financial results on August 8, 2024

Decisive Dividend Corporation

Second quarter 2024 financial results on August 9, 2024

Portfolio 2

Portfolio 2 for the week ended August 9, 2024: DOWN ![]()

- The Walt Disney Company (NYSE: DIS) announced it was raising the monthly fee for its Disney+ and other Disney streaming services.

In other Disney news, the company said it plans to invest a minimum of US$ 1 billion annually over the next five years in the United Kingdom, Europe, the Middle East, and Africa to produce movies and TV shows.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Airbnb, Inc.

Second quarter 2024 financial results on August 6, 2024

Crew Energy Inc.

See report under Portfolio 1.

Guardant Health, Inc.

Second quarter 2024 financial results on August 7, 2024

The Walt Disney Company

Third quarter 2024 financial results on August 7, 2024

Mitek Systems, Inc.

Third quarter 2024 financial results on August 8, 2024

Supremex Inc.

Second quarter 2024 financial results on August 8, 2024

Portfolio 3

Portfolio 3 for the week ended August 9, 2024: UP ![]()

- Microsoft (NASD: MSFT) has partnered with Palantir Technologies (NYSE: PLTR) to provide enhanced cloud, AI and analytics capabilities to the US defense and intelligence agencies.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Alvopetro Energy Ltd.

Second quarter 2024 financial results on August 7, 2024

Magnite, Inc.

See report under Portfolio 1.

Shopify Inc.

See report under Portfolio 1.

GDI Integrated Facility Services Inc.

See report under Portfolio 1.

goeasy Ltd.

Second quarter 2024 financial results on August 8, 2024

Brookfield Corporation

Second quarter 2024 financial results on August 8, 2024