AI Spending: When Hype Meets Reality

Artificial intelligence (AI) stocks are back on the move again – not because the businesses have changed, but because the price tag on building the future is getting harder to ignore. After climbing to new highs, many of the biggest companies in the AI industry have pulled back as investors start to question whether earnings can keep pace with the rapid run-up in share prices. With these companies now carrying so much weight in major indexes, even a shift in sentiment can quickly spill over into the broader market.

Behind that pullback is a much bigger question forming in the background: how long can the current wave of AI spending continue, and what does it actually take to keep funding it?

This week, I’ll look at what’s driving the latest move in AI and AI-adjacent stocks, and why it all circles back to the rising cost of building the infrastructure behind AI.

After years of leading the market higher, some of the biggest AI-linked stocks have come under pressure as investors question whether share prices have moved too far ahead of earnings and future growth. Because these companies now make up such a large share of major indexes, even relatively small pullbacks can have an outsized impact on broader market performance.

At the centre of this shift is something much bigger than short-term market noise: the massive wave of spending going into AI.

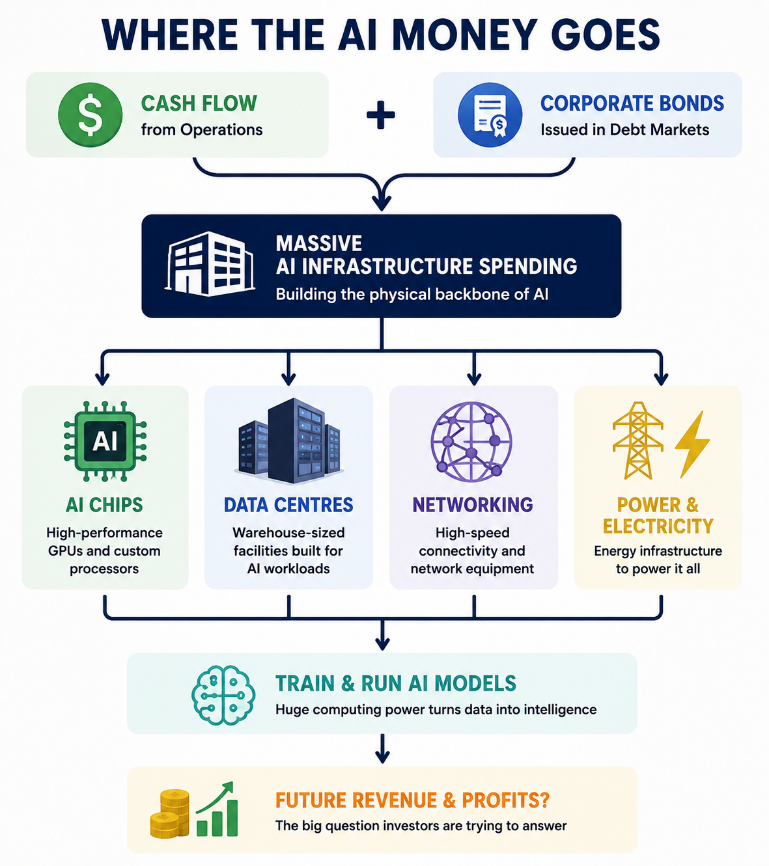

What started as a race to build better AI models has turned into a full-scale infrastructure buildout. Training and running advanced AI systems requires far more than software and talent. The money is flowing into next-generation chips, warehouse-sized data centres built for AI workloads, high-speed networking systems, and the energy infrastructure needed to power it all. In simple terms, the AI story is no longer just about who has the best model – it’s about who can build and maintain the physical backbone behind it.

Figure 1: The AI race has become an infrastructure race. The companies that can finance and build the physical backbone of AI may be the ones best positioned to benefit over the long term.

That matters because the cost of this buildout is rising quickly. For much of the past year, these investments were funded largely through the cash these companies generate from their normal operations – money coming in from sales after day-to-day expenses. But as AI spending has accelerated, several mega-cap technology companies have also turned more actively to debt markets through the issuance of corporate bonds. This isn’t a sign of financial strain. Microsoft (NASDAQ: MSFT), Amazon (NASDAQ: AMZN), and Alphabet (NASDAQ: GOOGL) all regularly access debt markets, and in the current cycle they’ve continued alongside rising capital spending on data centres, chips, and AI infrastructure. In other words, debt is being used as an accelerator, not a lifeline, allowing them to scale AI infrastructure faster than cash flow alone would comfortably allow.

While borrowing to support growth is nothing unusual, the scale of this shift has caught investors’ attention. Since the start of 2026, AI-related companies have issued roughly US$220 billion in investment-grade debt, already surpassing the full-year total from 2025 by 62%. Much of this has come from the biggest technology names, as they race to secure computing capacity and lock in long-term infrastructure before competitors catch up.

This has created a more complex picture for investors. On one hand, AI remains one of the strongest growth themes in the market. On the other, it’s increasingly tied to questions about financing, balance sheet strength, and whether investors have already accounted for the scale of spending in today’s stock prices.

Last week’s selloff brought that tension into focus. A sharp pullback in AI-linked chipmakers – sometimes dubbed a “chip-wreck” – dragged semiconductor stocks lower and weighed on broader technology indices. The Nasdaq fell 3.3%, marking only its second losing week in the past 13, as investors reassessed how sustainable the current level of AI-related spending really is.

Now that we’ve reviewed what drove last week’s swings in AI stocks, let’s move on to how markets performed over the past week and what it meant for my three portfolios.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Gross Domestic Product (GDP)

Canada’s economy, or GDP, grew 0.5% in April, beating expectations for a 0.4% increase and rebounding from a 0.1% contraction in March. It marked the strongest monthly expansion in about nine months, confirming the economy is still growing, even if that growth has been uneven. On an annual basis, the economy expanded 1.1%.

The rebound was broad-based, with goods-producing industries leading the way, rising 1.2%. Mining, quarrying, and oil and gas extraction posted particularly strong gains, while the services sector also contributed with a more modest 0.3% increase. Together, the results suggest the improvement wasn’t driven by just one area of the economy.

While April was an encouraging month, it doesn’t materially change the broader picture. Statistics Canada’s early estimate points to another 0.1% increase in May, suggesting the economy continues to shift between stronger and weaker months rather than gathering momentum. That’s another sign Canada’s economy is still growing, but it’s doing so in fits and starts instead of following a steady upward path.

Canadian Market Volatility

Canada’s version of the market “fear gauge” is the S&P/TSX 60 VIX Index (VIXC). Like the US VIX, it measures how much volatility investors expect in the Canadian stock market over the next 30 days. Higher readings signal greater uncertainty, while lower readings suggest investors are feeling more confident.

The VIXC typically runs lower than its US counterpart because the Canadian market has less exposure to high-growth technology companies and a greater weighting in sectors such as financials, energy, and materials. Those industries generally experience fewer sharp swings in investor sentiment, resulting in lower expected volatility.

The VIXC opened the week at 15.20, slightly above the previous week’s close of 14.70 as investors continued to monitor tensions following the recent exchange of missile strikes between the US and Iran. With no further escalation during the week, investor sentiment remained relatively steady. The index traded in a narrow range between 14.6 and 15.4 before finishing the week back at 14.19, suggesting Canadian investors remained broadly confident despite the uncertain global backdrop.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Labour data

This week’s labour data comes from three key reports: the Job Openings and Labor Turnover Survey (JOLTS), the ADP Employment Report, and the Employment Situation Summary (ESS). Each measures a different part of the US labour market, helping investors build a more complete picture of employment conditions.

JOLTS tracks demand for workers through job openings, hiring, and quits. ADP provides an early snapshot of private-sector hiring, while the ESS ties everything together with job creation, the unemployment rate, and wage growth. Together, they show whether the labour market is still holding up or gradually losing momentum.

Labor Department’s JOLTS

The Bureau of Labor Statistics’ JOLTS report showed job openings holding steady at around 7.6 million in May, broadly in line with April’s revised reading and slightly above expectations of 7.3 million. The data points to a labour market that is stabilising rather than gaining momentum, with demand for workers remaining firm but no longer building on earlier strength. Employers are still posting a high level of vacancies, suggesting hiring demand remains intact even as broader growth conditions have become more cautious.

ADP Employment Report

The ADP Employment Report showed private-sector employers added 98,000 jobs in June, down from May’s 122,000 and below expectations of 117,000. Hiring continued, but at a slower pace, pointing to a gradual loss of momentum rather than a sharp slowdown. Small businesses accounted for more than half of the gains, suggesting they remain willing to expand despite a more cautious backdrop. Overall, the report reinforces the JOLTS picture: hiring is still happening, just at a more measured pace.

The Employment Situation Summary (ESS).

The BLS’s latest jobs report showed the US economy added just 57,000 jobs in June, well below expectations of around 110,000 and down from May’s revised 129,000. The weaker result suggests employers are becoming more cautious about adding workers.

The unemployment rate edged down to 4.2% from 4.3%. While that may look positive, the decline was driven largely by fewer Americans actively looking for work rather than stronger hiring, making the improvement less meaningful than it appears.

Wage growth remained steady. Average hourly earnings rose 0.3% in June, matching May’s pace, while annual growth ticked up slightly to 3.5% from 3.4%.

Overall Labour Takeway

Taken together, this week’s data points to a US labour market that is still holding up but losing momentum. JOLTS showed steady demand for workers, ADP confirmed continued hiring at a slower pace, and the official jobs report highlighted a more pronounced slowdown than expected.

For investors, the key message is that the labour market is no longer providing the same level of support to the economy as it did over the past couple of years. Hiring is slowing, but not collapsing, and wage growth remains relatively stable.

If this trend continues, it could help ease inflation pressures and increase the likelihood that the Fed gains confidence to begin cutting interest rates later in the year. However, policymakers are unlikely to react to a single month of data, so investors will be watching upcoming labour and inflation reports closely for confirmation before expecting any shift in policy.

Consumer Confidence Index (CCI)

The Conference Board’s Consumer Confidence Index edged up to 91.2 in June from May’s downwardly revised 90.6, but still fell well short of expectations for 94.5. Lower gasoline prices helped lift confidence by easing some inflation concerns, but the report still painted a mixed picture beneath the surface.

The Present Situation Index, which measures how consumers feel about current business conditions and the job market, declined to 116.4, while the Expectations Index, which looks ahead over the next six months, improved modestly to 74.4.

Despite that improvement, the Expectations Index remains well below the 80 level that has historically been associated with elevated recession risk. It first moved below that threshold in late 2024 and has remained there since, reflecting a prolonged period of cautious sentiment. While this level has often signalled increased downside risk in past cycles, in recent years it has also persisted without an immediate downturn in economic activity, making it more of a warning about confidence than a precise timing indicator.

American Market Volatility

The VIX – often called the market’s “fear gauge” – measures expected volatility in the S&P 500 over the next 30 days. In simple terms, it reflects how much uncertainty investors are pricing into the market, rising when anxiety picks up and easing when conditions feel more stable. Readings above 20 are generally associated with heightened volatility, while lower levels tend to signal calmer markets.

The index began the week at 18.60 and briefly moved above 20 after the US and Iran exchanged tit-for-tat strikes, generating a sharp rise in geopolitical uncertainty. It then drifted back into the mid-teens as tensions cooled following a commitment to stop further strikes in order to maintain the ceasefire and continue peace negotiations. Oil flows through the Strait of Hormuz remained steady, helping ease fears of broader energy disruption and inflation pressure. The VIX later briefly moved above 17 after a weaker-than-expected June labour report, before fading again as investors digested the data, finishing the shortened trading week at 16.16.

Weekly Market and Portfolio Review

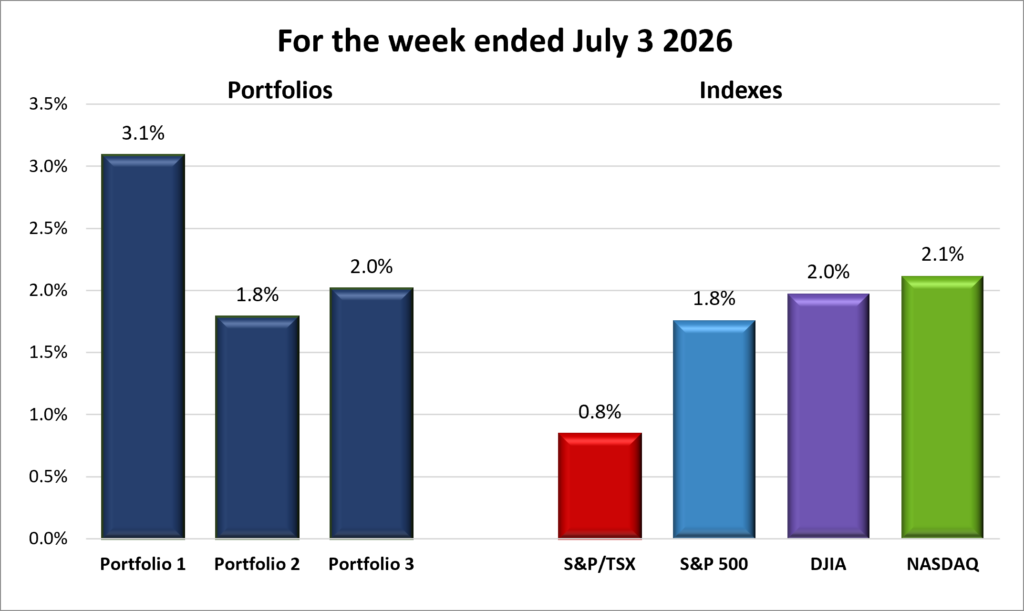

For the week, the TSX (SPTSX) added 0.8%, the S&P 500 (SPX) rose 1.8%, the DJIA (INDU) gained 2.0% and the Nasdaq (CCMP) climbed 2.1%.

| Index | Weekly Streak |

| TSX: | 1 – week winning streak |

| S&P: | 1 – week winning streak |

| DJIA: | 4 – week winning streak |

| Nasdaq: | 1 – week winning streak |

![]() It was a holiday-shortened trading week, with the TSX closed on Wednesday for Canada Day and US markets closed on Friday for Independence Day. Even with fewer trading days, there was still plenty for investors to process as they weighed easing geopolitical tensions and fresh economic data. The Nasdaq Composite Index (Nasdaq), S&P 500 Index (S&P), and Dow Jones Industrial Average (DJIA) all finished the week higher, with the DJIA standing out after setting two record closing highs at the end of June and another on July 2. Canada’s TSX got off to a slower start as falling oil prices weighed on the energy sector, but a recovery in oil alongside stronger gold prices over the final two trading days helped it finish the week with a gain.

It was a holiday-shortened trading week, with the TSX closed on Wednesday for Canada Day and US markets closed on Friday for Independence Day. Even with fewer trading days, there was still plenty for investors to process as they weighed easing geopolitical tensions and fresh economic data. The Nasdaq Composite Index (Nasdaq), S&P 500 Index (S&P), and Dow Jones Industrial Average (DJIA) all finished the week higher, with the DJIA standing out after setting two record closing highs at the end of June and another on July 2. Canada’s TSX got off to a slower start as falling oil prices weighed on the energy sector, but a recovery in oil alongside stronger gold prices over the final two trading days helped it finish the week with a gain.

Early in the week, sentiment was still shaped by the ongoing US-Iran conflict, with investors assessing the risk of further escalation following the exchange of strikes over the weekend. The key concern wasn’t just geopolitical tension, but the potential disruption to shipping through the Strait of Hormuz, which could have a significant impact on global oil supply. Any sustained disruption would likely push energy prices higher and add fresh inflation pressure at a time when investors were already focused on when the Fed might begin cutting interest rates. As the week progressed, tensions appeared contained and markets increasingly priced in a fragile but stabilising situation. Oil prices drifted lower, helping ease inflation concerns and supporting a more constructive tone across equities.

With geopolitical risks fading, attention shifted back to economic data. A series of US labour market reports pointed to a gradual cooling in hiring. While that would normally raise concerns about growth, investors largely welcomed the data because it reinforced expectations that the Fed will eventually have room to lower rates. That said, timing remains uncertain, with some investors still cautious that sticky inflation could delay rate cuts. Lower interest rates generally reduce borrowing costs and support stock prices, helping improve overall sentiment.

Beneath the surface, technology remained the key source of volatility. After a strong run, many AI and semiconductor stocks saw profit-taking, leading to sharper swings within the Nasdaq and S&P and limiting their relative performance. This was less a change in long-term sentiment and more a digestion phase after a significant rally. As money rotated out of high-flying technology names, it moved into more cyclical areas such as financials and industrials, helping support broader market gains and contributing to the DJIA’s relative strength.

In Canada, markets were closed on Wednesday for Canada Day, splitting the trading week into two halves. Even with that break, the TSX still had plenty to digest as investors reacted to oil, gold, and broader market moves. While the index finished the week higher, it still lagged the major US benchmarks.

Canada’s energy sector got off to a weak start as oil prices continued to slide, weighing on the index early in the week. However, oil prices recovered into the end of the week, while gold prices also strengthened after weaker-than-expected US labour data that lessened the likelihood of a rate cut later this year. Broad-based buying across several sectors added further support, lifting the Index into positive territory at the end of the week.

Overall, markets moved through a clear shift in focus over the week, from geopolitical risk to economic data and then to positioning within different parts of the market. While US equities were led higher by broad gains and a rotation beneath the surface, Canada’s market was shaped more by its sector mix, with energy and gold playing an outsized role. Both markets ultimately ended the week higher, but with slightly different drivers underneath the surface.

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week winning streak |

| Portfolio 2: | 1 – week winning streak |

| Portfolio 3: | 1 – week winning streak |

![]() After a little rain fell on the portfolios last week, the sun came back out as all three returned to their winning ways. Improving optimism around interest rates, combined with renewed buying in many technology and growth stocks, helped drive the rebound across all three portfolios.

After a little rain fell on the portfolios last week, the sun came back out as all three returned to their winning ways. Improving optimism around interest rates, combined with renewed buying in many technology and growth stocks, helped drive the rebound across all three portfolios.

Portfolio 1 had the strongest week, rising 3.1% and outperforming the other portfolios as well as all four major indexes. It also recorded the highest share of weekly winners at 72%, led by standout moves from SEA Ltd. (NYSE: SE) up 19%, Celsius Holdings (NASDAQ: CELH) up 18%, Magnite (NASDAQ: MGNI) and Datadog (NASDAQ: DDOG) both up 16%, and Apple (NASDAQ: AAPL) and Grab Holdings (NASDAQ: GRAB) both up 12%.

It was also a notable week for CrowdStrike (NASDAQ: CRWD). The cybersecurity company completed a 4-for-1 stock split, set a new record high, and finished the week up 12%. It was another reminder that investors continue to favour many of the market’s strongest technology companies. 😊

Portfolio 2 posted a 1.8% gain for the week, with 57% of holdings finishing in positive territory. The main contributors were MongoDB (NASDAQ: MDB), which rose 19%, and Guardant Health (NASDAQ: GH), which gained 15%. iA Financial (TSE: IAG) also contributed to the portfolio’s positive performance after reaching a new record high.

Portfolio 3 also returned to positive territory, rising 2.0% over the week. Strength was broad-based, with 69% of holdings finishing higher. MDA Space (TSX: MDA) led the way with a 17% gain, followed by Magnite at 16%, 5N Plus (TSE: VNP) at 10%, while Royal Bank of Canada (TSE: RY) reached a new record high. And then there was Rocket Lab (NASDAQ: RKLB). The stock rocketed 22% after announcing its acquisition of satellite communications provider Iridium Communications (NASDAQ: IRDM). The deal expands Rocket Lab’s position in the satellite industry by adding an established communications network and a large base of enterprise and government customers. It also strengthens the company’s long-term ambitions in the emerging direct-to-device market, where satellites connect directly with smartphones and other devices.

With Rocket Lab rocketing higher, all three portfolios finishing in the green, and several companies setting new record highs, it was a welcome return to form after last week’s brief shower. Hopefully the sunny skies stick around next week. 😊

Companies on the Radar

It was a quiet week for my stock radar, with no changes to the list. The four companies below remain on my watchlist, although I’m just as interested in adding to some of my existing winners if the right opportunities come along.

It was a quiet week for my stock radar, with no changes to the list. The four companies below remain on my watchlist, although I’m just as interested in adding to some of my existing winners if the right opportunities come along.

- S&P Global (NYSE: SPGI): A large cap American company and one of the world’s most important financial information companies. Most investors know it for the S&P 500 Index, but the business also provides credit ratings, market data, analytics, and research used by banks, corporations, governments, and investors worldwide. Think of it as one of the key information providers that helps global financial markets function, generating revenue through subscriptions, licensing fees, and rating services.

- Perimeter Solutions (NYSE: PRM): An American mid-cap company that produces specialty chemicals. Its best-known products are the fire retardants used to fight wildfires. If you’ve seen aircraft dropping bright red retardant over a wildfire, there’s a good chance it came from Perimeter. The company operates in a niche but essential market, supplying products and services that help protect communities, infrastructure, and natural resources during increasingly active wildfire seasons.

- TerraVest Industries (TSE: TVK): A mid-cap Canadian industrial company that produces equipment for energy, storage, and transportation markets, including propane tanks, pressure vessels, and heating systems. It grows through a mix of organic expansion and acquisitions, serving steady, asset-heavy industrial niches across North America.

- Forgent Power Solutions (NYSE: FPS): An American large-cap industrial company that builds the electrical infrastructure needed to power data centres, factories, and other large facilities. In simple terms, it makes the equipment that helps move electricity from the grid to where it is needed. It’s not the company building AI models, but rather one of the companies supplying the critical infrastructure that helps keep the AI boom running.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated July 3, 2026.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!