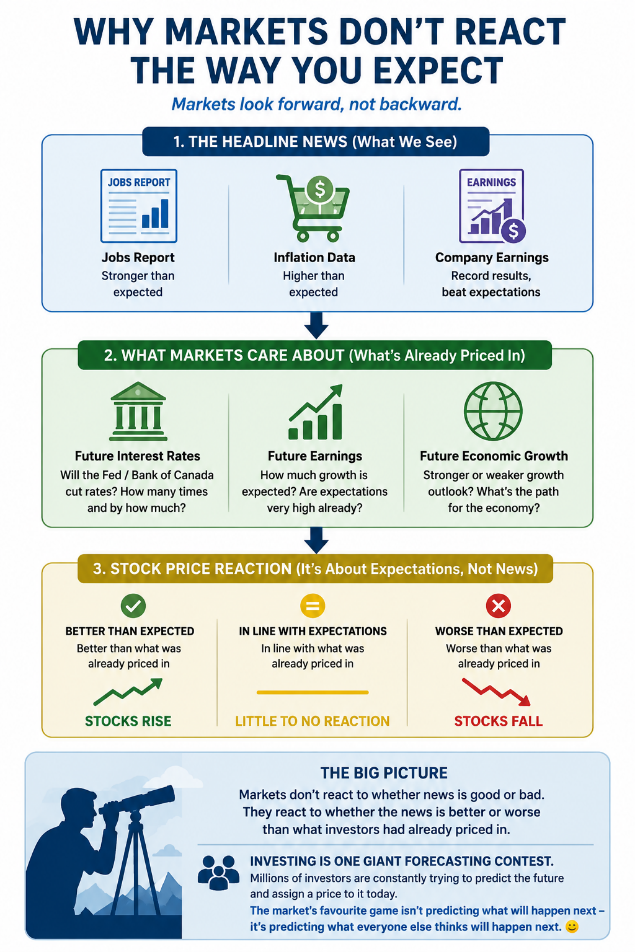

What’s Priced In? Why Markets Don’t React the Way You Expect

When I first started investing, one of the most confusing things I found was watching stocks rise on bad news or fall on good news.

The economy adds jobs, yet stocks decline. Inflation comes in higher than expected, yet markets rally. A company reports record earnings, yet its share price drops. As an Nvidia (NASDAQ: NVDA) investor, I’ve experienced this more than once over the past few years.

The missing piece is a simple concept called “pricing in.”

Unlike the evening news, markets don’t dwell on the past. Investors are constantly looking ahead and trying to estimate what the future will look like. They aren’t buying stocks based on what happened yesterday, but on what they expect will happen tomorrow.

Think of a weather forecast calling for a major snowstorm next week. Most people wouldn’t wait for the first snowflake to buy a shovel or stock up on supplies – they’d prepare early. Investors do the same. If they expect interest rates to fall, earnings to rise, or the economy to strengthen, they often buy long before those events happen.

That’s why you’ll often hear whether something is “already priced in.” If investors expect the Federal Reserve – or the Bank of Canada – to cut rates, stocks may start rising months in advance. By the time the cut arrives, there may be little reaction because it’s already been accounted for.

Recent events show this clearly.

The previous week’s US labour report showed job growth coming in much stronger than expected. On the surface, that’s good news – more jobs mean more spending, stronger consumer confidence, and healthier economic growth. But investors focused on rates. A stronger labour market reduces pressure on the Federal Reserve to cut rates, leading investors to scale back expectations for future cuts.

A similar dynamic played out with Broadcom’s (NASDAQ: AVGO) latest earnings. The company beat expectations and continues to benefit from strong artificial intelligence (AI) demand. Yet the stock sold off. Why? Investors weren’t just pricing in strong results – they were pricing in exceptional ones. When expectations are high enough, even good news can disappoint.

In both cases, the reaction wasn’t about whether the news was good or bad, but whether it was better or worse than what was already priced in.

Markets don’t react to the news itself. They react to how the news compares with what investors were already expecting.

Markets don’t react to whether news is good or bad. They react to whether the news is better or worse than what investors had already priced in.

Of course, nobody knows the future. Investors constantly update expectations as new information comes in. That’s why markets can move sharply after inflation data, earnings misses, or policy changes – they force investors to reassess what they thought was already priced in.

For us long-term investors, the lesson is simple. Instead of focusing only on headlines, it helps to ask: what is the market already expecting? Often, the reaction matters more than the news itself.

In many ways, investing is one giant forecasting contest. Millions of investors are constantly trying to predict the future and assign a price to it today. But the market’s favourite game isn’t predicting what will happen next – it’s predicting what everyone else thinks will happen next. 😊

The theory is one thing, but seeing it in real time is another. With that in mind, let’s turn to this week’s events, what the markets were pricing in, how they reacted, and how those moves affected my three portfolios.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, …

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Interest Rate Decision

This week, the BoC left its policy interest rate unchanged at 2.25%, marking its fifth consecutive rate hold. The decision wasn’t particularly surprising, as the Bank finds itself caught between two competing forces.

Normally, two quarters of economic contraction would strengthen the case for lower interest rates. Growth has been weaker than expected, and recent GDP data suggests Canada has experienced two consecutive quarters of contraction. Lower rates could help stimulate borrowing, spending, and investment, giving the economy a much-needed boost.

On the other side is inflation. Rising oil and gasoline prices, driven by the conflict in the Middle East, have pushed inflation higher and are expected to keep it near 3% in the coming months. Since the BoC’s target is 2%, cutting rates now could risk making inflation worse.

That leaves Governor Tiff Macklem and the other governors in a difficult position. While they believe much of the recent inflation pressure is being driven by higher energy prices rather than excessive demand, they also don’t want those higher costs spreading throughout the economy.

For now, the BoC appears content to wait for clearer evidence about which force will win out. Officials aren’t seeing enough weakness to justify a rate cut, but they’re also not seeing enough broad-based inflation to consider a rate hike. As a result, Canadians may be living with today’s interest rates for a while longer.

Canadian Market Volatility

Canada’s version of the market “fear gauge” is the S&P/TSX 60 VIX Index (VIXC), often shown on trading platforms as VIXI.TO. Like the better-known CBOE Volatility Index in the US, it measures how much volatility investors expect in the Canadian stock market over the next 30 days.

The VIXC opened the week at 15.19, slightly above the previous week’s close of 14.96. Despite ongoing US–Iran tensions and swings in oil prices, the index mostly hovered around the 15 level, signalling relatively calm conditions in Canadian markets.

By the end of the week, the VIXC had settled at 14.18, finishing lower than where it started and reinforcing the sense that market fears eased as geopolitical risks cooled.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Consumer Price Index (CPI)

The latest inflation data from the Bureau of Labor Statistics showed that US consumer prices continued to rise in May, with headline, or all items, CPI coming in at 4.2% year-over-year, up from 3.8% in April and the highest reading since early 2023. Monthly inflation rose 0.5%, in line with expectations.

At first glance, that looks like a step in the wrong direction. However, the details tell a more nuanced story.

Core inflation, which excludes the more volatile food and energy components, rose just 0.2% on the month, down from 0.4% in April and slightly below expectations. On an annual basis, it edged up to 2.9% from 2.8%, suggesting underlying price pressures are still relatively contained even as headline inflation is lifted by energy costs.

The breakdown makes that contrast clear. Gasoline prices jumped 7% on the month, making energy the main driver of inflation. Fuel oil prices were up nearly 59% year-over-year, reflecting higher global oil prices. By contrast, some categories cooled, with medical care costs falling 0.7% on the month and used vehicle prices down 2% year-over-year.

Shelter, the largest component of the inflation basket covering rent and homeowner costs, rose a more modest 0.3% in May. On an annual basis, shelter inflation ticked slightly higher to 3.4% from 3.3%, showing housing costs remain sticky but aren’t re-accelerating.

For us investors, the key point is that inflation is being driven more by energy volatility than broad-based price pressures. That likely keeps the Fed in a holding pattern for now, maintaining the benchmark rate around 4.50% while it waits to see whether higher energy costs spread through the economy or fade as conditions stabilise.

Consumer Sentiment Index (CSI)

The preliminary June reading of the University of Michigan CSI came in at 48.9, up from May’s record-low reading of 44.8 and well above economists’ expectations of 46. While sentiment improved during the month, it is still almost 20% below the 60.7 reading recorded a year ago, highlighting that many Americans are still concerned about the economic outlook.

The improvement in sentiment was broad-based. The Current Economic Conditions Index, which reflects how consumers feel about their finances and job security today, rose to 48.4, up 5.7% from May but still 25.3% lower than a year ago. The Expectations Index, which measures how consumers feel about the economy over the next six months, climbed to 49.3, up 11.8% from May but still down 15.1% year over year. Together, the two measures suggest consumer confidence may be stabilizing after several months of decline.

The biggest reason for the improvement appears to be relief at the gas pump. Gasoline prices fell nearly 10% from May levels, easing financial pressure on households. Lower fuel costs tend to have an outsized impact on consumer confidence because they are one of the most visible expenses in everyday life.

This report provides a modestly encouraging sign. While consumer sentiment remains near historic lows, the improvement suggests Americans are becoming slightly less pessimistic about the economy and inflation than they were just a month ago.

American Market Volatility

The VIX, often called the market’s “fear gauge,” measures how much volatility investors expect in the S&P 500 over the next 30 days. In simple terms, it reflects how much uncertainty is being priced into markets. The VIX tends to rise when fear increases and fall when confidence improves. Readings above 20 are typically associated with elevated stress, while levels below that point to calmer conditions.

The index opened the week at 18.52, down from the previous week’s close of 21.51. Early in the week, easing concerns around AI spending and a temporary cooling in US–Iran tensions helped reduce investor anxiety.

However, volatility later spiked above 23 — its highest level since early April — as renewed US–Iran escalation triggered sharp moves in oil prices and raised concerns around potential supply disruptions. This came alongside ongoing sensitivity to inflation data, which remains at its highest level since 2023, keeping volatility elevated near the 21 level for part of the week.

Following reports that planned US military action against Iran had been called off and that a peace agreement was close, sentiment improved and volatility quickly reversed, dropping back below 20. Investor optimism around technology stocks, supported by the SpaceX (NASDAQ: SPCX) IPO, also helped lower risk concerns, with the index ultimately finishing the week at 17.68.

Overall, the VIX saw a sharp mid-week surge in uncertainty before easing as geopolitical tensions cooled. While the spike into the low-20s was brief, the index ended the week slightly below where it started, suggesting investors stay alert to potential shocks even as broader conditions stabilize.

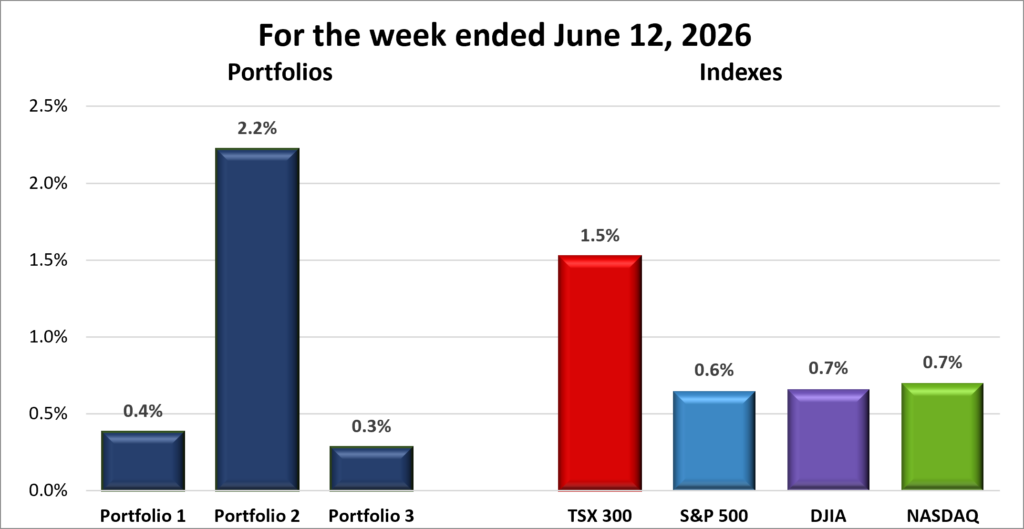

Weekly Market and Portfolio Review

For the week, the TSX (SPTSX) surged 1.5%, the S&P 500 (SPX) added 0.6%, the DJIA (INDU) advanced 0.7% and the Nasdaq (CCMP) rose 0.7%.

| Index | Weekly Streak |

| TSX: | 1 – week winning streak |

| S&P: | 1 – week winning streak |

| DJIA: | 1 – week winning streak |

| Nasdaq: | 1 – week winning streak |

![]() The market rollercoaster continued this week, with stocks moving up, then sharply lower, before recovering from a midweek pullback to finish in positive territory. All four major North American indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite (Nasdaq) – ended the week in the green.

The market rollercoaster continued this week, with stocks moving up, then sharply lower, before recovering from a midweek pullback to finish in positive territory. All four major North American indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite (Nasdaq) – ended the week in the green.

Markets were driven by a tug-of-war between AI optimism, concerns that sticky inflation could delay rate cuts, and periodic geopolitical shocks in the Middle East.

The week began with investors still digesting the previous Friday’s stronger-than-expected labour report. While a resilient job market is positive for the economy, it also reduced the likelihood of near-term rate cuts from the Fed, weighing on sentiment, particularly in technology stocks, which are more sensitive to interest rate expectations.

AI remained another key driver. Investors reassessed expectations following Broadcom’s earnings report and concerns that AI-related valuations had become stretched, triggering an early-week pullback in technology stocks and a rotation into defensive sectors such as Consumer Staples and Healthcare. Sentiment later improved as confidence in the long-term AI growth story returned, helping technology shares recover earlier losses. Friday’s record-setting SpaceX IPO added further fuel to the rally, reinforcing enthusiasm for innovation-focused companies and investors’ continued appetite for growth-oriented investments.

Inflation remained in focus following the latest CPI report. Headline inflation rose to its highest level since 2023, driven largely by higher energy prices linked to Middle East tensions. However, core inflation eased slightly, suggesting energy rather than broad-based price pressures was responsible for the increase. For the Fed, the key question is still whether this is a temporary spike or the start of more persistent inflation pressures.

Geopolitical developments added further volatility. Renewed US–Iran tensions pushed oil prices higher, raising fears of supply disruptions and additional inflation pressure. Markets later rebounded after both sides signalled a peace agreement could be within reach, easing concerns about a broader conflict. The prospect of a deal helped push oil prices lower and improved sentiment into the weekend by reducing inflation and interest rate risks tied to energy prices.

In Canada, the TSX faced many of the same drivers, with oil prices, interest rates, and sector rotation shaping performance.

Energy was a key support for the index. Rising oil prices boosted Canadian energy stocks and reinforced the sector’s outsized influence on the market. Higher energy prices also helped Canada post a second consecutive monthly trade surplus in April, underscoring the economy’s link to commodities.

Interest rates remained in focus after the Bank of Canada held its policy rate at 2.25%. While expected, the decision left investors weighing weak growth against still-elevated inflation, extending uncertainty around the timing of future rate cuts.

Technology and AI-linked stocks added to volatility in Canada as well. As investors reassessed expectations following Broadcom’s earnings, some rotated out of high-growth names into more defensive sectors, mirroring moves in US markets.

Overall, investors balanced AI-driven momentum against concerns that sticky inflation could limit how quickly central banks can ease policy. Despite several volatile sessions, both US and Canadian markets finished the week higher, supported by optimism surrounding the SpaceX IPO, improving prospects for a US–Iran peace agreement, and strength in key sectors such as technology and energy. In Canada, financials also added to the positive tone, with several major banks reaching record highs. Looking ahead, investors will be watching next week’s Fed meeting, the first under new Chair Kevin Warsh, for further clues on where interest rates are headed.

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week winning streak |

| Portfolio 2: | 1 – week winning streak |

| Portfolio 3: | 1 – week winning streak |

![]() This week played out almost the mirror opposite of last week, when portfolios were strong heading into Friday but faded into the close. This time, portfolios were in the red midweek before a strong finish lifted all three into positive territory. The gains were modest, but a win is still a win. 😊 Across all three portfolios, the Canadian banks were a consistent source of strength, with all three reaching record highs and helping offset volatility elsewhere.

This week played out almost the mirror opposite of last week, when portfolios were strong heading into Friday but faded into the close. This time, portfolios were in the red midweek before a strong finish lifted all three into positive territory. The gains were modest, but a win is still a win. 😊 Across all three portfolios, the Canadian banks were a consistent source of strength, with all three reaching record highs and helping offset volatility elsewhere.

Portfolio 1 returned to the weekly win column with a slight gain of 0.4%. Just over half of its holdings finished higher, helped by a 10% gain in Magnite (NASDAQ: MGNI), which was largely offset by a 10% decline in Navitas Semiconductor (NASDAQ: NVTS). The Canadian banks were a key support, with TD Bank (TSE: TD) and Bank of Nova Scotia (TSE: BNS) both reaching record highs and posting weekly gains.

Portfolio 2 was the top performer among the portfolios and indexes, rising 2.2%. Around 55% of holdings were positive, led by a 14% gain in Birkenstock (NYSE: BIRK). Aritzia (TSE: ATZ) also set multiple record highs during the week, while South Bow (TSE: SOBO) and Bank of Nova Scotia reached new highs as all three finished the week with gains.

Portfolio 3 edged into positive territory with a 0.3% gain, completing a clean sweep of weekly gains across all three portfolios. Just over half of holdings finished higher, including Magnite’s 10% rise. Royal Bank (TSE: RY) set multiple record highs throughout the week, while TD Bank also reached record highs and posted a weekly gain.

Offsetting some of the gains were the space-related holdings, Rocket Lab (NASDAQ: RKLB) and MDA Space (TSE: MDA), which had rallied ahead of SpaceX’s IPO but reversed sharply afterward, erasing earlier weekly gains. ☹

This week was another reminder that short-term market movements can be unpredictable. A few days ago, the portfolios were staring at a losing week, yet they ultimately finished in the green. While I always enjoy seeing portfolio values rise, I’m even more encouraged to see so many holdings continuing to grow their businesses, reach new highs, and improve their competitive positions. Over the long run, that’s what ultimately drives returns. 😊

On a separate note, Portfolio 3 now stands at 26 holdings following last week’s additions of MDA Space, Corning (NYSE: GLW), and Amphenol (NYSE: APH). The long-term target remains around 25 names, which is now effectively in range. Portfolio 1 is still being gradually trimmed toward that level, while for Portfolios 2 and 3, future additions will likely be balanced by selling companies where growth in revenue, earnings, and share price has stalled.

Companies on the Radar

After the previous week’s flurry of activity, this week was much quieter, with no new companies making their way onto my radar list. Instead, I used the time to review the makeup of my portfolios, and the results confirmed what I already knew.

After the previous week’s flurry of activity, this week was much quieter, with no new companies making their way onto my radar list. Instead, I used the time to review the makeup of my portfolios, and the results confirmed what I already knew.

Portfolios 1 and 3 have become heavily concentrated in technology stocks, with the sector accounting for 59% and 58% of each portfolio respectively. Portfolio 2 is much more balanced, with technology representing just 17% of holdings, while financial companies make up 37%.

While I still believe technology will remain a powerful long-term growth driver, too much exposure to any one sector can increase volatility. When technology stocks are leading the market, concentration can feel like a superpower. When sentiment shifts, however, it can feel like an anchor.

With that in mind, I’ll be focusing my research on non-technology companies in the weeks ahead. The goal isn’t to eliminate the technology bias in Portfolios 1 and 3, but to add a little more balance and reduce risk.

As part of that process, I’m moving Lumentum Holdings (NASDAQ: LITE) to the back burner. I still believe the company has strong long-term potential, but the current share price appears to leave little room for error. As analysts often say, the stock looks “priced to perfection.” If the company disappoints, even slightly, the share price could fall sharply.

I’d rather wait for a better entry point than buy today and spend months hoping the stock eventually climbs back above my purchase price. That’s a lesson I’ve learned the hard way more than once. 😊

So while Portfolios 1 and 3 will likely remain technology-focused, hopefully they won’t be quite as technology-heavy in the future.

With Lumentum moving to the sidelines, my radar list now has just one company:

- TerraVest Industries (TSE: TVK) Industries: A mid-cap Canadian industrial company that produces equipment for energy, storage, and transportation markets, including propane tanks, pressure vessels, and heating systems. It grows through a mix of organic expansion and acquisitions, serving steady, asset-heavy industrial niches across North America.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated June 12, 2026.

Portfolio Update

Portfolio 2

Bought: Whitecap Resources (TSE: WCP) This is my third investment in Whitecap, following initial purchases in August and December 2024. Since that first buy, the share price is up 62%, and including dividends, the total return is over 68%. Higher oil prices have helped along the way, especially with ongoing geopolitical tensions, but that’s not the reason I’m adding more here.

When I first became an owner, Whitecap was a solid mid-sized energy producer with an attractive monthly dividend. Since then, it’s been transformed through its merger with Veren Inc., formerly known as Crescent Point Energy. This wasn’t a small deal – it combined two major Canadian energy producers. The result is a much larger company, now the seventh-largest oil and natural gas producer and the fifth-largest natural gas producer in Canada. Beyond scale, the merger expanded its drilling inventory and created efficiencies that should support stronger cash flow over time.

Just as importantly, management is staying disciplined on the balance sheet. Whitecap expects to reduce net debt by more than $1 billion during 2026, which matters in a business where commodity prices can swing hard and fast. A stronger balance sheet helps smooth out those cycles and keeps shareholder returns intact.

At its core, I still see Whitecap as an income generating investment. The monthly dividend has done exactly what I wanted – providing steady cash flow that can be reinvested over time. The share price can move around with oil prices, and I wouldn’t be surprised to see some pullback if energy prices cool off. But that’s not really the focus here. It’s about long-term cash flow and compounding.

In the meantime, I’ll keep collecting the dividends, reinvesting them, and letting compounding do what it does best – build wealth through investing. 😊

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!