After twelve months of watching global storm clouds constantly pound the three portfolios lower, finally a ray of light. Not much of a ray but at least the storm clouds started to recede. Since the start of the fourth quarter, three of the four major North American indexes finished the quarter higher than they started. The three portfolios are still in the red at the end of the quarter, just not as deeply as they were at the end of the third quarter. Let’s take a look at what transpired over the last three months….

Contents

Fourth Quarter Portfolio Update

Portfolio 1 for the fourth quarter

Portfolio 2 for the fourth quarter

Portfolio 3 for the fourth quarter

Going Forward: The First Quarter 2023

Fourth Quarter Review

In the third quarter, the rollercoaster that is the stock market, was heading down with no bottom in sight. In the fourth quarter of 2022 (October 1 through December 31), the rollercoaster finally bottomed in early October and started climbing, as you can see in the chart below. Finally!

In the third quarter, the rollercoaster that is the stock market, was heading down with no bottom in sight. In the fourth quarter of 2022 (October 1 through December 31), the rollercoaster finally bottomed in early October and started climbing, as you can see in the chart below. Finally!

Of course, there were many ups and downs during the ride to the end of the quarter, before a slight dip to end the quarter and the year. It was great not talking about bear markets (drops of 20% or more from recent highs) or bear traps (when markets rise for a few days before resuming their downward trajectory).

The primary driver of the fourth quarter was concerns about inflation and corresponding rising interest rates in Canada and the US. The indexes largely moved on investor optimism, rumours the Bank of Canada (BoC) and to a greater extent the US Federal Reserve (Fed) would slow down the pace of its interest rate hikes, hawkish commentary from the Fed, and investors ignoring the Fed’s comments about the need for additional rate hikes. Looking at the chart below, you can see the indexes climbing higher, leading up to the Fed’s Federal Open Market Committee (FOMC) meeting in early November. Upon the announcement of another 0.75% increase the indexes dropped sharply. The same pattern occurred around mid December. The indexes rallied on hopes the interest rate would increase by only 0.25%. However, the Fed dashed those hopes and increased the rate by 0.5%, sending all four indexes tumbling downward. The Dow Jones Industrial Average (DJIA), the S&P 500 Index (S&P) and Toronto Stock Exchange Composite Index (TSX), were able to hold some of their quarterly gains and end the quarter in positive territory, but the Nasdaq Composite Index (Nasdaq) plunged on the December 14 announcement, ending the quarter in the red.

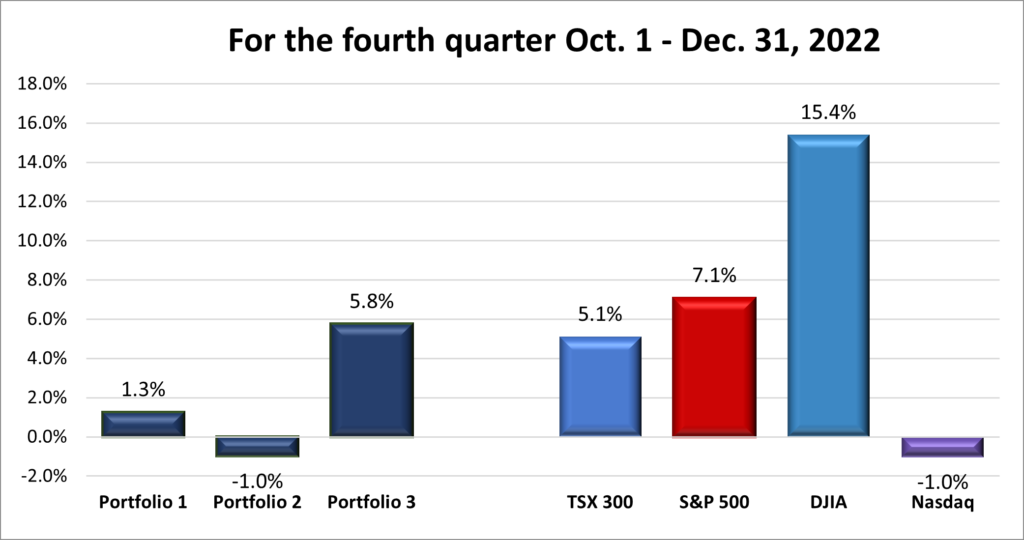

For the fourth quarter, the TSX, rose 5.1%, the S&P, gained 7.1%, the DJIA, jumped 15.4% while the Nasdaq slipped 1.0%.

Fourth Quarter Portfolio Update

Portfolio 1 for the fourth quarter: DOWN

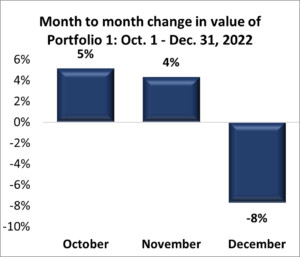

Portfolio 1 benefitted from the October to mid December rally before being dragged lower by the Nasdaq plunge in late December. Energy companies continued to buoy the portfolio, but the technology companies lifted, then sank the portfolio. Portfolio 1 clawed out a 1.3% gain for the quarter.

Portfolio 2 for the fourth quarter: DOWN

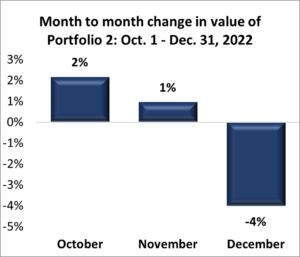

The fourth quarter saw the portfolio post wins in October and November, before a sharp drop in December to end the quarter. Being the least aggressive portfolio of the three, its gains were moderate, but its technology bias still hurt in December. Fortunately, the dividend paying companies and non technology companies were able to soften the December drop. Overall, Portfolio 2 fell back in the fourth quarter, dropping 1.0%.

Portfolio 3 for the fourth quarter: DOWN

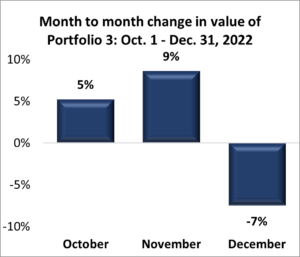

The fourth quarter was much better for Portfolio 3, riding the technology tide higher before plummeting in the last half of December. The gains in October and November more than compensated for December’s losses. Portfolio 3 advanced 5.8%, easily outperforming the other two portfolios.

Twelve Month Review

It was no surprise that all four indexes ended the year down significantly, as shown in the chart below. The TSX was able to stay above water until late April before it dropped into red as interest rates started to climb. The TSX stayed in the red for the rest of the year. Along the way, the TSX dropped into a market correction (a drop of 10% or more) twice, each time for a few weeks before climbing back out. The DJIA was under water from February onward but was able to avoid a market correction except for a dip in June and again for a month starting in early September. Despite ending the year lower, the DJIA was the best of the three American indexes.

The S&P spent a good amount of time in a market correction, with a dip into a bear market in late September, resulting in its biggest annual decline in 15 years. The Nasdaq, home of the high-flying technology stocks, felt the wrath of the bears, plummeting into bear territory in early May and staying there for the rest of the year. Of the eleven S&P sectors that span the DJIA, the S&P and the Nasdaq, six had double digit drops in earnings. The only sectors to post gains in 2022 were energy, industrials, real estate, utilities, and consumer staples. The gains in these sectors ranged from 90% in energy down to 3% in Consumer Staples.

The main reasons for a dismal 2022 were:

- Rising inflation caused by increased demand from countries emerging from Covid-19 restrictions.

- Holdover supply chain problems caused by the pandemic.

- The Russian invasion of Ukraine lead to shortages of oil, natural gas, and wheat.

- Both the Canadian and American central banks’ delayed response to inflation, then the historic increase in their respective benchmark interest rates, climbing from 0.25% to over 4%, a 15 year high.

- A flare up in supply chain issues caused by China’s lockdowns in their fight against a covid-19 outbreak.

- Finally, geopolitical tensions between the west and Russia, and the USA and China.

That’s a lot in one year but I believe rising inflation and the corresponding rising interest rates were the two biggest reasons the North American markets had such a poor year.

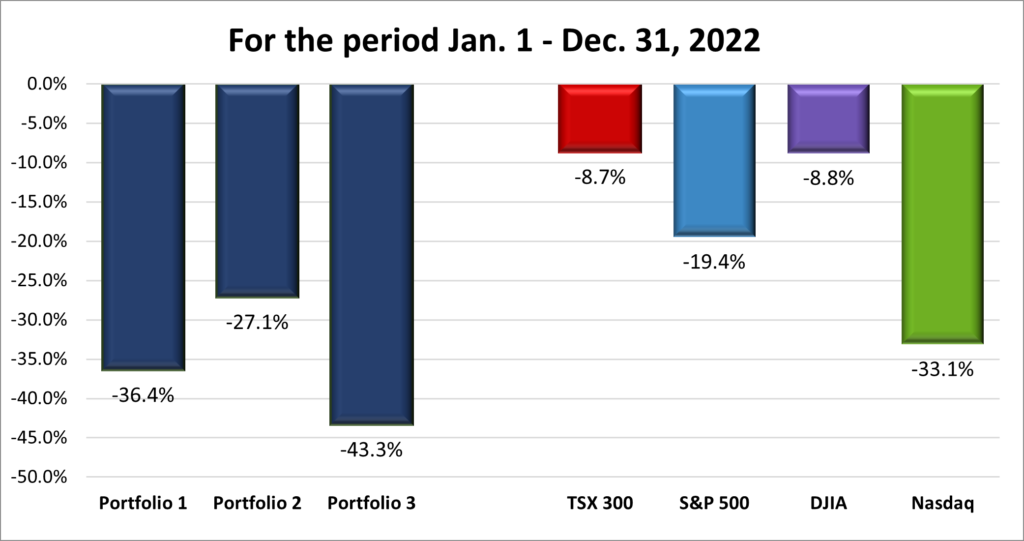

The TSX was the ‘best’ of the major North American indexes, limiting losses to 8.7%, closely followed by the DJIA which fell 8.8%. of the thirty companies that make up the DJIA, ten finished the year higher. The S&P barely avoided bear market territory plunging 19.4% and wiping out roughly $8 trillion in market capitalization from the companies listed in the S&P 500 index. Bringing up the rear was the growth-oriented Nasdaq which plummeted 33.1%, well into bear market country. The past year was the largest percentage decline for all three American indexes since the financial crisis of 2008.

Twelve Month Portfolio Review

It would be an understatement to say 2022 was not kind to the Indexes, but it was brutal on the three Portfolios, as you can see below. With all three portfolios oriented towards technology companies, and the technology heavy Nasdaq down 33%, it was no surprise the Portfolios were down drastically. All three portfolios paid heavily for their technology orientation, with Portfolio 2 the best of a bad lot, ‘only’ losing 27% of its value. ☹ As bad as that was, the more aggressive Portfolios 1 and 3 lost 36% and 43%, respectively, of their value in 2022. It was largely the energy stocks in Portfolio 1 that prevented it from plunging as far as Portfolio 3. Fortunately beating the S&P is not a priority (but it would be nice) because I failed miserably this year. ☹

2022 in Review

2022 will not be remembered fondly by this investor. In fact, it will go down as one of the worst years on record for stocks and my worst year of investing. Most of the damage was done in the first half of the year when the Fed spooked the markets with the first of a series of aggressive interest rate increases. Throughout the year there were rallies which turned out to be bear traps, with each rally followed by a drop to a lower low.

2022 will not be remembered fondly by this investor. In fact, it will go down as one of the worst years on record for stocks and my worst year of investing. Most of the damage was done in the first half of the year when the Fed spooked the markets with the first of a series of aggressive interest rate increases. Throughout the year there were rallies which turned out to be bear traps, with each rally followed by a drop to a lower low.

In Canada and the US, Interest rates went from 0.25% to over 4.0% in record time, sending the markets sharply downward. The worst off were the interest sensitive technology companies. Across the board, tech companies announced plans late in the year to rein in projects and focus on generating profits, made sizeable cuts to their respective work forces, and operate more strategically and efficiently. As well as higher interest rates eating into their cash flows, an overall market slowdown, higher costs (especially energy), and over expansion during the pandemic years caused many of them to grow faster than they should have. The result was companies lowered their guidance for earnings and future growth and their share prices paid the price.

Going Forward: The First Quarter 2023

Gone but not forgotten is Covid-19. Most of the world has learned they will have to live with it and are getting back to normal. Replacing Covid-19 concerns is the fear of a recession, especially in the USA (the world’s largest economy). Joining fears of a recession are most of the events that roiled the stock markets during 2022 – supply chain issues, the ongoing war in Ukraine, high inflation, rising interest rates – remain as we start 2023. There is already talk about additional increases to interest rates in Canada and the US in 2023, making it harder for high growth oriented companies, and those with significant debt.

However, there are reasons to believe 2023 will be better (2022 should not be hard to beat 😊). One of these is China’s reversal on their Covid-19 lockdowns. China is the world’s second largest economy and if they can successfully get their economy back on track it will have a significant positive impact not just on China, but for the rest of the world. The BoC and the Fed have already slowed the pace of their interest rate hikes. Despite comments from the Fed that rates will continue to rise, many investors believe the worst is behind us. As a result, investor sentiment has gone from a negative stance in the third quarter to a cautiously optimistic position as we head into 2023. Interest rates should peak and start falling in the second half of 2023 but it would be wise to remember the saying “Don’t fight the Fed” and invest conservatively while the Fed fights its battle with inflation.

Good luck in the coming year. May the bulls return and long may they run.