Investing Basics FAQ

Investing Basics

If you’re new to investing, start here! This section answers fundamental questions about what investing is, why it matters, and common concerns like risk. Understanding these basics will help you feel more confident as you start your investing journey.

What is Investing?

What are the perceived barriers to investing?

Why should I invest in the stock market?

But isn’t it too risky to invest in the stock market?

Why is investing in the stock market better than putting your money under your mattress?

Explore More Investing FAQs:

- Types of Investments – Discover different investment options.

- Getting Started with Investing – Step-by-step guide to beginning your investment journey.

- Understanding Risk & Strategy – Key risks and how to invest wisely.

- Maximizing Your Investment Returns – Tips for growing your portfolio.

- Return to Questions and Answers Main Page

Questions

What is Investing?

Let me start by saying investing is not gambling. Gambling is a form of instant gratification. It is like playing a game of chance, with the house often having an advantage. Investing is about growing your money over time, like planting seeds and nurturing them to grow into a bountiful harvest. You can do this by putting your money to work in various assets, such as shares of companies (stocks), bonds, or even funds that hold a mix of these. While the hope is to see your investments grow in value, it is important to remember that there is also a chance they could lose some value. Different investments have different levels of risk, so finding the right ones for you depends on your goals and how comfortable you are with potential losses.

Remember, investing should be a long-term strategy, not a get-rich-quick scheme. By investing in well run companies, with strong financials, good track records, promising prospects and staying patient, you can increase your chances of achieving your financial goals over time. By spreading your investments across companies in different sectors, with a mix of growth, dividend paying and defensive companies (those that provide essential products or services, such as utility companies) can help mitigate the impact of losses in any one area.

What are the perceived barriers to investing?

Here are a few common barriers that I’ve either encountered myself or heard other people mention:

- Lack of knowledge: Many people feel they do not have enough knowledge about the financial markets or investing strategies, making them hesitant to start.

- Limited financial resources: Investing often requires some initial capital, which can be a barrier for those with limited savings.

- Risk Aversion: Fear of losing money often holds people back from investing, as the potential for financial loss can seem overwhelming.

- Investment complexity: The vast array of investment options and complex financial jargon can be intimidating for new investors.

- Time constraints: Investing requires research and ongoing monitoring, which can be challenging for busy individuals.

- Debt: Debt payments can limit available funds for investing and create financial pressure.

- Life events: Major life events like starting a family or buying a home can impact your financial situation and risk tolerance, potentially affecting investment decisions.

- Inertia: Even with knowledge and resources, you need to avoid procrastination and take the first step.

Do any of them look familiar to you? I have faced them all at one time or another. The first step to overcoming these barriers is to acknowledge them, then make a plan to address them head-on.

Do not be discouraged by the initial complexity. Do not overthink it, avoid paralysis by analysis. It becomes easier once you overcome the initial inertia and get started. Open a free trading account and deposit a bit of cash. There, you have made your first investment. 😊 Keep adding money to your investing account while you learn and decide what to invest in. When you find an investment that fits your plan and risk tolerance, you will have already put some money aside.

Why should I invest in the stock market?

There are two primary reasons to invest in the stock market. The first is to grow your financial wealth to help you reach your financial goals and build up your nest egg for retirement or other goals. Currently, the average savings account provides interest at a rate of approximately 1%. In 2021, most GIC (Guaranteed Investment Certificate) paid 1 – 2%, depending on the length of term. Meanwhile the stock market (represented by the S&P 500 index, a collection of the 500 largest companies in the US) has averaged 12.32%, or had an annual return of 10.46%, for the last 100 years (January 1, 1920, to December 31, 2020. When adjusted for inflation, the stock market has an average return of 8.53% and an annualized return of 7.63% for the same period.

Now, the market rarely hits the average, instead the yearly returns can vary wildly. It’s great to be invested when the S&P 500 is up over 25% as in 2019 but not so great when the S&P 500 was down 37% during the 2008 banking crisis. The key is to leave your money invested over time as the markets have shown they will recover and continue to grow. Keep in mind, past performance does not guarantee future results.

The second reason is to protect your savings from inflation. Inflation is where money loses its purchasing power over time. Or, to put it another way, over time, prices for goods and services tend to rise.

With an inflation rate of 3.4% in Canada (3.4% in the US), in January 2024, the purchasing power of your hard earned cash is weakening. So, let me flip that around and ask why wouldn’t you invest in the market and get your money working for you?

Take the following example: If I wanted to purchase a $1,000 widget and if I had the money, I could buy it today for $1,000. However, if I decide to put off the purchase for a year and leave the money in a savings account earning interest, a year from now, thanks to inflation, I would no longer be able to purchase the widget for $1,000. The widget would cost $1034.00 ($1000 x 1.034) and the money in the savings account would have grown to only $1010 ($1000 x 1.01). And it gets worse as the years add up.

The chart below illustrates the increasing gap between the cost of a widget and the amount put away in a regular bank account. Each year you will need more money to buy the same product.

Keep in mind that investing involves inherent risks, and it is important that you understand your own risk tolerance. If you plan to invest in stocks, only invest in companies where you would be proud to call yourself an owner. With any investment, you should be able to sleep at night.

While there may be other ways to protect your money from inflation, investing wisely in the market is the best way to not only keep up with inflation but also get your money working for you, even when you are sleeping. 😊

But isn’t it too risky to invest in the stock market?

Investing in the stock market offers significant growth potential, but it also carries the risk of financial loss. As someone who has experienced both wins and losses in the market, I understand this reality all too well. Historically, the market has demonstrated promising long-term growth; for instance, the S&P has risen over 310% since 2001. However, it is important to remember that past performance is not a guarantee of future results. Responsible investing demands a long-term perspective and effective risk management.

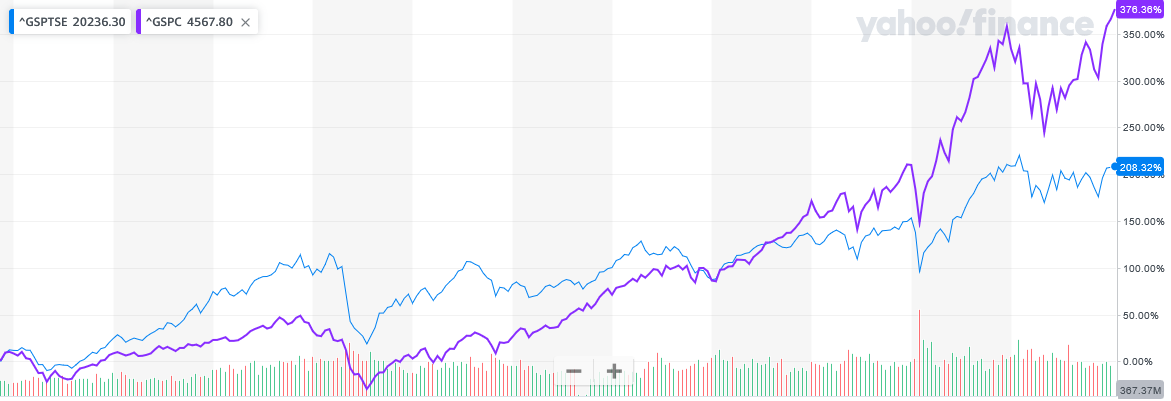

In the past two decades, we have witnessed three major ‘black swan’ events – unforeseen occurrences like 9/11, the banking crisis of 2008, and the COVID-19 pandemic. Despite the initial market downturns these events caused, recovery has always followed. From September 11, 2001, to February 2, 2024, the Canadian TSX Composite Index (TSX) has grown over 208%, and the S&P has increased by more than 376%, as shown in this chart below.

While short-term market dips are inevitable, with patience and time, the markets have historically recovered, allowing investments to grow. However, if you anticipate a need for your funds in the short term (within one to three years), it is advisable to avoid investing in the stock market due to potential downturns.

Investment decisions are highly personal. You should only venture into the stock market if you are comfortable with the idea of investing, can tolerate market volatility, and accept the risk of potential losses. If you decide to invest, be prepared to dedicate time to researching companies or understanding the fees associated with Electronically Traded Funds (ETFs) and mutual funds. Just as you would not buy the first car you see on a lot, you should not invest without doing your homework.

However, be honest about how much time and effort you are willing to invest. At a minimum you will need to set up an investment account and transfer funds into your new investing account. For those seeking minimal effort, consider ETFs, which bundle a group of stocks together. For example, an S&P ETF tracks the top 500 companies in the US, and a TSX ETF covers the top companies on the Toronto Stock Exchange, offering a mix of Canadian and American market exposure and some risk diversification.

Remember, when indexes like the S&P or TSX rise, so does the value of your investment, and vice versa. But historically, over the long term, these indexes have trended upward.

Consider setting up a monthly automatic transfer from your bank to your investment account, periodically purchasing additional shares in your ETFs. This approach allows your investment to grow over time with minimal effort.

Keep in mind, I am not a financial advisor, and it is crucial to seek professional advice before making any investment decisions.

Why is investing in the stock market better than putting your money under your mattress

Most mattresses pay 0% interest and are not a very secure way to stash your money. In the event of a robbery or fire the cash could literally go up in smoke and you’ll be left with nothing. Besides a lack of security, a mattress provides no return at all. 😊

While financial institutions (banks, credit unions, etc.) are significantly more secure than a mattress, they currently provide less than 1% interest on standard savings accounts. While they are safer, your money essentially sits idle, losing purchasing power due to inflation. Most financial institutions provide an investment product called a GIC (Guaranteed Investment Certificate) that pays 1 – 2%, depending on the length of term. During the term you do not have access to your money without incurring a withdrawal penalty which could leave you with less than you started.

The other option is to invest in the stock markets which offer the potential for higher returns that outpace inflation. Historically, the stock market has averaged approximately an 8% average annual growth rate. However, unlike the previous options, the stock market fluctuates, and you could experience losses. With that in mind, you can invest in the market in a few ways including mutual funds, index funds, Electronic Traded Funds or by purchasing shares of individual companies directly. The table and chart below illustrate the potential growth of $1,000.00 put into a mattress at 0%, a typical savings account at 1.0%, a GIC at 2% and in the stock market with the average 8% return.

My initial forays into the stock market involved mutual funds (described below). I later transitioned to buying shares of individual companies through a stockbroker and then an online brokerage account. While I do keep some cash in a savings account, I avoid keeping any money under a mattress.