Types of Investments FAQ

Types of Investments

Stocks, bonds, TFSAs, RRSPs—there are many ways to invest. This section explains the different types of investments, helping you understand your options and how they fit into your financial plan.

Questions Covered:

What are stocks, actually?

What are the different types of stocks?

What about Bonds?

Is it better to invest in Canadian or American stocks?

How is a TFSA different from an RRSP?

Explore More Investing FAQs:

- Investing Basics – Learn the fundamentals of investing.

- Getting Started with Investing – Step-by-step guide to beginning your investment journey.

- Understanding Risk & Strategy – Key risks and how to invest wisely.

- Maximizing Your Investment Returns – Tips for growing your portfolio.

- Return to Questions and Answers Main Page

Questions

What are stocks, actually?

Stocks, commonly referred to as shares, represent ownership in a corporation. When you buy a stock, you’re buying a piece of that company, entitling you to a fraction of its assets and profits proportional to the amount of stock you own.

Corporations can raise capital in two primary ways: by issuing stocks or by borrowing money through bonds or loans. Each unit of stock is referred to as a “share.” While the terms ‘stocks’ and ‘shares’ are often used interchangeably, ‘stock’ can refer to overall ownership in one or more companies, whereas a ‘share’ signifies the smallest unit of that ownership.

Shares are primarily bought and sold on stock exchanges, such as the Toronto Stock Exchange, the New York Stock Exchange, or NASDAQ. Trading on these regulated exchanges ensures transparency and reduces the risk of fraudulent practices, safeguarding investor interests.

When you buy or sell shares, whether through a brokerage or a direct investing account, you will receive confirmation of the transaction. This confirmation details the number of shares you bought or sold and the price per share. It’s worth noting that today, it’s rare to receive a physical stock certificate as evidence of ownership since most records are kept electronically.

Shares of public companies like TD Bank (TSE: TD) and Apple (NASD: AAPL) are integral to many investors’ portfolios, representing a tangible link between personal finance and the broader economic landscape.

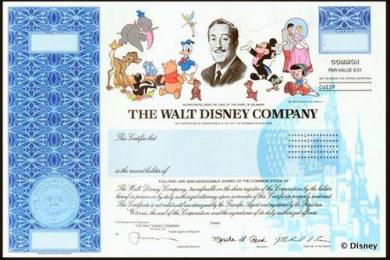

The Walt Disney Company (NYSE: DIS) stock certificates were once among the most sought-after because of their colorful designs featuring beloved Disney characters. These certificates were not only investments but also popular gifts from parents and grandparents eager to introduce children to the world of investing. On October 16, 2013, Disney ceased issuing these decorative paper stock certificates to shareholders. Although no longer available, Disney now offers ‘certificates of acquisition’ upon request, which carry no monetary value but maintain the tradition for collectors and fans.

What are the different types of stocks?

There are two main types of stocks: common and preferred. They differ in terms of voting rights, dividend priority, and risk profile.

Common Stocks

Common stocks are the most prevalent type of shares, typically what people refer to when they discuss stocks. Holders of common stocks usually have voting rights, which allow them to participate in corporate decisions such as electing board members and approving corporate policies. However, the influence of an individual investor is minimal, given the enormous number of outstanding shares. For example, owning 1,000 shares of Apple (NASD: AAPL) is negligible compared to its billions of outstanding shares.

These stocks are associated with higher potential returns, particularly from young, high-growth companies, such as Shopify, which prefer to reinvest profits to fuel further growth rather than pay dividends. In contrast, well-established companies in slower-growing industries (like utilities or mature tech firms such as Microsoft (NASD: MSFT)) often offer steady dividends, attracting those seeking regular income.

The primary risk with common stocks is evident during a company’s bankruptcy; common shareholders are last in line for any remaining assets, positioning these shares as the riskiest in times of financial distress.

Preferred stocks are less common and operate somewhat like bonds, providing a fixed dividend and thus a regular income stream, which is attractive to income-focused investors. For example, The Royal Bank of Canada’s Series BO preferred shares (TSE: RY.PR.S). These shares pay a fixed non-cumulative preferential cash dividends, payable quarterly. For more detailed information on this series of preferred shares, click here. Preferred shares typically do not confer voting rights, which might deter investors seeking a say in company governance.

Preferred shareholders enjoy a priority over common shareholders in the distribution of assets upon company liquidation, offering a greater degree of security in adverse conditions. However, they still rank below debt holders in the repayment hierarchy. Additionally, issuers of preferred stocks may retain the option to buy back these shares at predetermined prices, providing companies with financial flexibility but potentially capping the gains for investors.

What about Bonds?

While Canada Savings Bonds are no longer available, bonds remain a popular investment option with various types offering different characteristics and risk profiles.

Bonds essentially represent loans you make to a government or corporation. In return, the issuer promises to pay you regular interest and repay the principal amount at maturity. Compared to stocks, bonds generally offer lower potential returns but also lower volatility, making them a good choice for income generation and diversification.

Different types of bonds exist:

- Government bonds: Considered safer due to government backing.

- Corporate bonds: Issued by companies and vary in risk based on the company’s creditworthiness.

- Municipal bonds: Issued by local governments and may offer tax benefits depending on location.

My experience with bonds is limited, but I encourage you to learn more if they align with your investment goals. If you want to learn more about bonds, check out Beginners’ Guide to Investing in Bonds from Wealthsimple, the Securities and Exchange Commission, or check with your financial institution. If you decide to purchase a bond, make sure to speak a reputable financial advisor who can provide you with personalized guidance to meet your needs.

As with stocks, remember that when investing, the value of your investment may rise or fall, and your capital is at risk.

Is it better to invest in Canadian or American stocks?

As Canadian investors, we have the unique advantage of being able to access both Canadian and American markets, offering a wide array of investment opportunities. The decision to invest domestically or across the border involves various factors, including exchange rates and tax implications. Consulting with a CPA tax expert or a certified financial adviser can provide clarity on the latter.

Sector Considerations:

- Energy and Natural Resources: The Toronto Stock Exchange (TSE) is renowned for these sectors, making it a practical choice for those investments to avoid foreign exchange fees.

- Technology, Healthcare, Consumer Goods: The US markets, such as the New York Stock Exchange (NYSE) and the Nasdaq Stock Market, offer broader selections in these industries. Although there are strong contenders in Canada, the variety and scale in the US are greater.

The table below showcases the top 10 companies by market capitalization in Canada and the US, as of May 2024. It highlights the sectoral strengths of each market, with Canadian companies excelling in Financials and Energy, while US giants dominate in Technology and Communication Services.

| Largest Canadian companies | Sector | |

| 1 | Royal Bank of Canada | Financials |

| 2 | Shopify | Technology |

| 3 | Toronto Dominion Bank | Financials |

| 4 | Canadian Natural Resources Limited | Energy |

| 5 | Enbridge Inc. | Energy |

| 6 | The Bank of Nova Scotia | Financials |

| 7 | Canadian National Railway | Industrials |

| 8 | Brookfield Asset Management | Financials |

| 9 | Manulife Financial Corporation | Financials |

| 10 | BCE Inc. | Communication Services |

| Largest American companies | Sector | |

| 1 | Microsoft Corporation | Technology |

| 2 | Apple Inc. | Technology |

| 3 | Nvidia Corporation | Technology |

| 4 | Alphabet Inc. (Google) | Communication Services |

| 5 | Amazon.com, Inc. | Consumer Cyclical |

| 6 | Berkshire Hathaway Inc. | Financials |

| 7 | Johnson & Johnson | Healthcare |

| 8 | Tesla, Inc. | Consumer Cyclical |

| 9 | Meta Platforms, Inc. (Facebook) | Communication Services |

| 10 | Exxon Mobil | Energy |

Given this distribution, your sector interest should guide where to invest. For technology, the US market is compelling. For financials, especially banks, staying within Canada may be more beneficial unless you are looking at multinational financial services where U.S. companies like Visa (NYSE: V) and Mastercard (NYSE: MA) also play significant roles.

Strategic Considerations:

Many Canadian companies aim to list on US exchanges to gain exposure and credibility. Conversely, it is rare for US companies to seek listings in Canada. However, when a company, such as Shopify (TSE: SHOP / NYSE: SHOP), is listed on both a Canadian exchange and an American exchange it is called cross listed. Companies cross list to gain broader exposure to investors. For Canadians, purchasing shares on the Canadian exchange can be more economical due to savings on exchange rates. Conversely, US investors would likely buy shares on the American exchange, assuming you can even buy shares on the TSE.

Conclusion:

Choosing between Canadian and American stocks is not straightforward, as both markets offer unique advantages. The TSE excels in the energy, resources, and financial sectors, while the US markets, including NYSE and Nasdaq, are noted for their diverse range of companies, particularly in technology, consumer cyclicals, and healthcare. Implementing a strategy that includes diversification across both countries can be beneficial, helping to balance risks and leverage strengths from each country. However, investors must consider factors like currency exchange rates and tax implications, which can influence returns on foreign investments. Ultimately, your investment decisions should align with your personal financial goals, sector preferences, and risk tolerance.

How is a TFSA different from an RRSP?

As this question involves tax implications, consulting with a financial advisor or tax accountant is recommended to get personalized advice to maximize the benefits of these registered accounts.

Here is my take (remember, I’m not a Certified Financial Planner nor an accountant). Inside a TFSA (Tax Free Savings Account) and RRSP (Registered Retirement Savings Plan) you are limited to:

- Cash

- Investment funds including mutual funds, exchange-traded funds, and other pooled money products

- Securities listed on a designated stock exchange

- Corporate bonds

- Government bonds

For a complete list of qualifying investments and prohibited investments for RRSPs and TFSAs, check out these links on the CRA website: qualified investments and prohibited investments.

TFSAs and RRSPs are both tax-advantaged accounts, with yearly maximum contribution limits with penalties for exceeding the maximum contribution. However, they differ in how contributions and withdrawals are taxed.

RRSPs: Contributions are tax-deductible, lowering your current taxable income. However, when you withdraw money from the RRSP you will have to pay taxes at your tax rate at the time of the withdrawal. In theory you won’t make any withdrawals until you retire, and your income is lower than when you made the deposit, allowing you to pay less in taxes than you would have when you made the deposit.

TFSAs: A TFSA is an after-tax savings account where your money can grow tax free. Contributions are made with after-tax dollars, but all growth and withdrawals within the account are tax-free. This is a great place for growth stocks as there will be no capital gains taxes on your investments.

Choosing between a TFSA and RRSP depends on your tax bracket now and when you expect to withdraw the money. While both types of accounts are a great way to grow your wealth, you should be aware that if an investment loses money, you cannot claim a capital loss to offset capital gains, as you should do with non-registered accounts.

Other differences governing RRSPs and TFSAs, include:

- age requirements (you must be 18 to set up a TFSA);

- terminal age (RRSPs must end by age 71);

- contribution eligibility (you must have earned income to contribute to an RRSP);

- TFSA withdrawals may be recontributed the following year;

- withdrawals from an RRSP may affect the taxpayer’s entitlement to benefits and tax credits, while TFSA withdrawals do not.

At this point, I remind you that I’m not a financial planner nor a tax expert. 😊 Consulting a professional financial advisor can help you determine which option is best for your situation.

To illustrate the difference between an RRSP and a TFSA, here is an example. If you deposited $5000 in your RRSP and bought 100 shares of Shopify in 2015 when it was $50 per share it would’ve cost you $5000. If you decided to sell your Shopify shares in 2021 it would be worth around $1900 per share or $190,000 for a profit of 185,000. While you would have received a tax deduction in 2015, you would have to pay income tax on the withdrawal. If you withdrew the $190,000 all at once you would put yourself in a very high tax bracket and be taxed accordingly.

In a TFSA, in the same scenario as above, you’d now have $190,000 in your TFSA. However, your $190,000 could be withdrawn with no tax deductions. While you wouldn’t have gotten a tax deduction in 2015, you could withdraw the full $190,000 without having to pay any tax.

While this is an extreme but true example, not every investment grows that much that quickly. For me, I try to take advantage of my TFSA by placing investments with high growth potential inside my TFSA.

The taxman always gets their pound of flesh, and tax laws can change. To make the most of your TFSA and RRSP to minimize your taxes, it is wise to consult a financial advisor. They can help you make informed decisions, ensuring your investment strategies are tailored to your personal financial situation.